Starting a business is only half the battle – staying compliant is where many startups fall short. Missing deadlines for state filings, annual reports, and other compliance tasks can lead to fines, administrative dissolution, or even losing liability protections. Here’s a quick rundown of the five most overlooked compliance tasks and how you can stay on top of them:

- State Annual or Biennial Reports: These administrative updates keep your business records current. Deadlines and fees vary by state, with penalties for late filings reaching up to $400 (e.g., Florida).

- Registered Agent Compliance: Every business must maintain a registered agent to handle legal documents. Non-compliance could result in lawsuits, asset seizures, or administrative dissolution.

- Beneficial Ownership Information Report (BOIR): Starting in 2025, foreign businesses operating in the US must report ownership details under the Corporate Transparency Act. Non-compliance can result in fines up to $10,000 or imprisonment.

- Multi-State Operations Filings: Managing filings across multiple states adds complexity. Deadlines, fees, and rules differ widely, requiring extra attention to avoid penalties.

- S-Corp Tax Election and Reports: Missing the March 15 deadline for Form 2553 or Form 1120-S can cost your business thousands in taxes or penalties.

Avoid costly mistakes by using automated reminders, professional services, or compliance management tools like BusinessAnywhere. Staying ahead of deadlines ensures your startup remains in good standing and avoids unnecessary risks.

1. Filing State Annual or Biennial Reports

State annual reports aren’t about finances – they’re administrative updates that ensure your business details stay current in public records. These reports confirm essential information like your registered agent, principal office address, and key personnel, keeping your business compliant and records accurate.

State-Specific Compliance Requirements

Filing requirements vary widely by state, making it crucial to understand the rules where your business operates. For example, Ohio generally doesn’t require annual reports for most LLCs and corporations. On the other hand, while annual filings are the norm in most states, some – like Alaska, California (for LLCs), and New York – only require reports every two years.

Deadlines can also differ. Some states set fixed calendar dates: Florida requires filings by May 1, Delaware corporations by March 1, and Maine by June 1. Others tie deadlines to the month your business was formed, as seen in states like California, Arizona, New Jersey, and Virginia. A few states base deadlines on the fiscal year, which can make tracking more complicated.

Even within a single state, LLCs and corporations may have separate rules. In Delaware, for instance, corporations must file a report and pay a franchise tax by March 1, with fees starting at $50. LLCs, however, skip the report but must pay a flat $300 tax by June 1.

Deadlines and Penalties for Non-Compliance

Missing a deadline can be costly. States impose strict penalties for late filings. For example, Florida charges a $400 late fee – nearly triple its $138.75 filing fee. Delaware imposes a $200 late fee plus 1.5% monthly interest on unpaid balances, and California adds a $250 penalty to its filing fee .

The consequences go beyond financial penalties. Falling out of compliance can lead to administrative dissolution, freezing your bank accounts, loss of the right to sue in state courts, and even defaults on contracts. As Pavel Konopelko, a Financial Analyst at Able Finance, explains:

"A state-mandated business annual report is a non-financial compliance update."

This makes timely filing critical to maintaining good standing.

Costs Associated with Filings

Filing fees can range from $0 in states like Idaho, Minnesota, Mississippi, and Texas (if under the tax threshold) to $500 for Massachusetts LLCs. Most states charge between $50 and $100, with New York’s biennial LLC fee being just $9.

Reinstating a dissolved business is far more expensive than filing on time. For example, California charges a $30 reinstatement fee plus a $250 penalty. Delaware requires $200, back taxes, and accrued interest. In Florida, you’ll need to pay $100 in addition to late fees and the original filing fee.

Practical Tools to Simplify Compliance

To avoid last-minute stress, set up automated reminders well ahead of your filing deadline. Filing at least two weeks early can help you dodge technical issues or portal congestion. Double-check your registered agent details before filing, as outdated information can lead to rejections and missed legal notices. Many Secretary of State websites offer email or SMS notifications to alert you about upcoming deadlines.

For businesses operating in multiple states, services like BusinessAnywhere can be a lifesaver. They provide automated compliance reminders and handle official state notices for you. It’s also a good habit to regularly check your status online through your state’s database to spot any "delinquent" or "pending inactive" statuses before they escalate to dissolution. If you have inactive entities, formally dissolving them can save you from unnecessary reporting obligations and franchise taxes.

Taking these steps can help you stay ahead of compliance issues and avoid costly mistakes.

sbb-itb-ba0a4be

2. Maintaining Registered Agent Compliance

In the U.S., every business entity must designate a registered agent to handle legal documents, tax notices, and government correspondence on behalf of the company. This agent must be at least 18 years old, have a physical street address in the state (P.O. boxes are not allowed), and be available during standard business hours.

State-Specific Compliance Requirements

Each state has its own rules and terminology for registered agents, which can vary significantly. While most states use the term "Registered Agent", some have unique names for the role. For example, Ohio uses "Statutory Agent", Maine refers to them as "Commercial Clerk", and Vermont calls them "Process Agent."

Certain states add extra layers of compliance. For instance, in Kentucky, Missouri, Nebraska, and Wyoming, the agent must formally acknowledge their responsibilities by signing a consent form. In California, corporations serving as agents must file a "1505 Certificate." Meanwhile, Virginia prohibits business entities from acting as their own registered agents.

If your registered agent becomes unreachable, states handle the issue differently. In Illinois, the Secretary of State automatically steps in to receive documents, while states like Iowa, Montana, and Pennsylvania redirect correspondence to your principal business address.

Deadlines and Penalties for Non-Compliance

Failing to maintain an accessible registered agent can lead to serious consequences. If your agent doesn’t receive a summons, you risk losing lawsuits by default, which can result in wage garnishment or asset seizure.

Additionally, states may take administrative action against your business. In 2022 alone, over 1.2 million businesses were dissolved or revoked due to compliance failures. Once dissolved, your company loses its limited liability protection, putting personal assets in jeopardy. Sandra Feldman, Publications Attorney at CT Corporation, highlights the severity of this:

"The state can administratively dissolve the company if the failure to comply continues long enough. Once administratively dissolved, the company can no longer conduct its usual business and anyone doing business on its behalf may be held personally liable for company debts."

Non-compliance can also block you from opening bank accounts, securing loans, or defending yourself in court. Many contracts require businesses to stay in good standing, and falling out of compliance could trigger defaults on these agreements. Keeping your registered agent compliant ensures your business avoids these risks, allowing it to operate smoothly.

Costs Associated with Filings or Services

Acting as your own registered agent might save money upfront, but it comes with trade-offs. Your home address becomes public record, increasing the risk of unsolicited mail, predatory lending offers, and even identity theft. It also ties you to your office during business hours, limiting flexibility.

Professional registered agent services typically cost between $100 and $200 annually. For example, BusinessAnywhere charges $147 per year, offering the first year free if you register your business through their platform. If you need to switch agents, most states charge a filing fee. These fees are generally minimal compared to the steep penalties for non-compliance, such as California’s $250 fine for missed deadlines or Delaware’s $200 penalty plus 1.5% monthly interest.

Practical Tools or Services to Simplify Compliance

Using professional registered agent services not only manages costs but also simplifies compliance, especially for businesses operating in multiple states. National providers consolidate alerts and scanned documents into a single dashboard, making it easier to stay organized.

When choosing a service, prioritize those that offer quick document scanning, giving you ample time to respond to urgent notices. Many services also include reminders for filing annual reports and other deadlines, helping you stay ahead of compliance requirements.

After updating your registered agent, confirm the change within 24–48 hours using your state’s business search database. To avoid missing deadlines, set up alerts at least 60 days in advance for annual reports and other filings. These practices help keep your registered agent information current and ensure you’re prepared for additional compliance needs.

3. Submitting Beneficial Ownership Information Report (BOIR)

The Beneficial Ownership Information Report (BOIR) is a federal filing requirement created under the Corporate Transparency Act (CTA) and managed by the Financial Crimes Enforcement Network (FinCEN). Its purpose is to combat issues like money laundering, terrorism financing, and tax fraud by building a database of individuals who own or control companies that need to file.

A "Beneficial Owner" refers to anyone who directly or indirectly owns at least 25% of a company’s ownership interests or has significant control over the business. This typically includes senior executives. Startups must provide detailed information for each beneficial owner, including their full legal name, date of birth, residential address, and a copy of a government-issued ID.

Deadlines and Penalties for Non-Compliance

Starting March 2025, BOI reporting is voluntary for domestic U.S. companies and individuals but remains mandatory for foreign reporting companies – entities formed under foreign laws and registered to do business in the U.S.. For foreign entities registered before March 26, 2025, the filing deadline is April 25, 2025. Entities registered on or after March 26, 2025, must file within 30 days of their registration date. Additionally, any updates to previously reported information must be submitted within 30 days.

While FinCEN announced on February 27, 2025, that it wouldn’t impose fines for missing current deadlines, the consequences for willful non-compliance are serious. Civil penalties can reach up to $606 per day for ongoing violations, while criminal penalties include fines up to $10,000 and up to two years in prison. These strict measures emphasize the importance of timely BOIR filings, similar to other compliance requirements.

Costs Associated with Filings or Services

Filing the BOIR directly through FinCEN’s electronic portal is completely free. FinCEN has also issued warnings about scams, stating:

"FinCEN does not charge a fee for filing. Do not send money in response to any mailing that claims to be from FinCEN or another government agency".

For startups seeking professional help, third-party services are available. For example, BusinessAnywhere offers BOIR filing for $37 as a one-time service, handling the process on your behalf.

Practical Tools or Services to Simplify Compliance

If you manage multiple companies, you can apply for a free FinCEN Identifier to avoid repeatedly submitting sensitive documents. This identifier is available directly through the FinCEN website at no cost.

It’s also a good idea to maintain internal records, such as ownership interests and shareholder agreements, even if filing isn’t mandatory. These records can be invaluable during audits or if reporting requirements change. To stay on top of compliance, set reminders for the 30-day update window – especially when adding investors or appointing new executives. Treat BOIR updates with the same diligence as other filings to ensure your startup remains in good standing.

4. Updating Statement of Information for Multi-State Operations

Handling filings in a single state is already a meticulous process, but when your business operates across multiple states, things get even trickier. Each state has its own rules, terminology, and deadlines for updating essential business details like officer names, business addresses, and registered agent information. To keep your business in good standing, you’ll need to pay close attention to these state-specific requirements when updating your Statement of Information.

State-Specific Compliance Requirements

Different states have their own filing schedules and fees, which can add complexity to multi-state operations. For example, in California, businesses must file the "Statement of Information" (Form LLC-12) within 90 days of formation, and then every two years during the anniversary month. Filing fees are $20 for LLCs and $25 for corporations. Meanwhile, Connecticut will require businesses, starting January 1, 2025, to file an amended annual report immediately whenever there are changes to officers, directors, addresses, or registered agents. Each amendment will cost $25 .

Other states are also introducing new requirements. Washington, starting January 20, 2026, mandates valid email addresses for the registered agent and the principal office in all annual reports. Delaware is adding a "nature of business" disclosure requirement for reports due March 1, 2026, covering the 2025 reporting year. Pennsylvania is moving from a 10-year reporting cycle to an annual verification process beginning in 2025.

Deadlines and Penalties for Non-Compliance

Missing filing deadlines isn’t just a minor inconvenience – it can lead to serious consequences like administrative dissolution, where your business loses its legal standing and, with it, the liability protections an LLC or corporation provides. This could leave your personal assets exposed to business debts.

California, for instance, imposes a hefty $250 penalty if you fail to file within 60 days of receiving a delinquency notice, far exceeding the standard $20–$25 filing fee. Delaware charges a $200 late penalty plus 1.5% monthly interest on unpaid taxes and fees . In Florida, filing after May 1 incurs a flat $400 late fee. Anderson Cox, Founder of Policy Risk Center, highlights the stakes:

"The entire purpose of forming an LLC is to separate your personal assets from business liabilities. When your LLC loses good standing or is administratively dissolved, you may lose this protection".

Costs Associated with Filings or Services

The cost of filing varies widely depending on the state. For instance, Massachusetts charges up to $500 for LLC filings, while New York’s biennial LLC statement costs just $9. Delaware imposes a flat $300 annual tax on LLCs, while corporations must pay at least $50, plus any applicable franchise taxes . Tennessee is currently debating legislation that could raise annual report fees to $300 for both corporations and LLCs.

Many businesses turn to professional registered agent services to simplify multi-state compliance. These services help ensure filings are handled on time and provide a consistent address for state records.

Practical Tools or Services to Simplify Compliance

Staying on top of multi-state compliance requires organization and the right tools. Here are a few practical tips:

- Set reminders: Schedule alerts at 90, 60, and 30 days before each filing deadline to avoid last-minute scrambles.

- Conduct yearly audits: Review and confirm that officer lists and addresses are consistent across all states.

- Use registered agent services: These services provide a single, reliable address across states, helping to keep personal home addresses private.

- File early: Submitting forms at least two weeks before the deadline can help you avoid issues like overloaded state portals or technical glitches.

- Leverage compliance software: For businesses operating in many states, specialized software can centralize filings, automate deadline tracking, and reduce administrative headaches .

5. Filing S-Corp Tax Election and Reports

Securing your S-Corp tax election is a crucial step in maintaining compliance and saving on taxes. This election can significantly reduce self-employment taxes, but timing is everything. Many founders mistakenly believe their accountant will handle it all, only to find out too late that critical deadlines were missed. Such oversights can cost your business thousands in tax savings or lead to hefty penalties.

Deadlines and Penalties for Non-Compliance

For businesses operating on a calendar year, Form 2553 must be filed by March 15. If you’re a new corporation, you have two months and 15 days from your start date to file. For 2026, if March 15 falls on a weekend or holiday, the deadline shifts to Monday, March 16.

Missing this deadline can have serious consequences. Your business might remain taxed as a C-Corporation, leading to double taxation, or as an LLC, requiring full self-employment taxes until the next tax year. These tax costs can range from $10,000 to $40,000 annually for startups with substantial revenue. If you miss the deadline, there’s still hope. Under Revenue Procedure 2013-30, you can request late election relief if you file within three years and 75 days of your intended effective date and can show "reasonable cause." Beyond this window, you’ll need a Private Letter Ruling, which can cost between $3,500 and $28,000.

Once you’ve elected S-Corp status, you’ll need to file Form 1120-S by March 15, a month before individual tax returns are due. Filing late can result in penalties of $220 per shareholder, per month. As SDO CPA illustrates:

"A 3-shareholder S-Corp filed two months late. The IRS penalty? $1,320. Not for owing taxes. Just for filing late."

State-Specific Compliance Requirements

It’s important to note that S-Corp is a federal tax classification, not a state entity type. Your business will still be treated as an LLC or corporation at the state level, meaning you’ll need to comply with state-specific annual report requirements. Some states have additional rules. For example:

- New York and New Jersey require separate state-level S-Corp elections.

- California imposes a minimum $800 annual franchise tax on S-Corps.

Failing to file state annual reports can lead to administrative dissolution of your business, which could result in the IRS revoking your S-Corp status. This could expose your company to double taxation. To avoid such issues, aim to file your state annual reports early in January or February. Don’t assume your CPA will handle these filings automatically – double-check to ensure everything is submitted on time.

Practical Tools and Strategies for Compliance

Even if you’re confident about meeting deadlines, it’s a good idea to file Form 7004 by March 15. This grants a six-month extension for filing your annual return, moving the deadline to September 15. When submitting Form 2553, use certified or registered mail for proof of timely filing – fax confirmations aren’t always accepted. If filing late, label your Form 2553 with "FILED PURSUANT TO REV. PROC. 2013-30" and include a detailed explanation.

If your business has maintained a clean compliance record for the past three years, you may qualify for First-Time Penalty Abatement (FTA) from the IRS to waive late-filing fees. For ongoing compliance, services like Business Anywhere offer assistance with Form 2553 filings for a one-time fee of $147.

Filing your S-Corp election on time not only safeguards tax benefits but also strengthens your startup’s compliance and operational stability. Proper planning and attention to detail can save you from costly mistakes down the road.

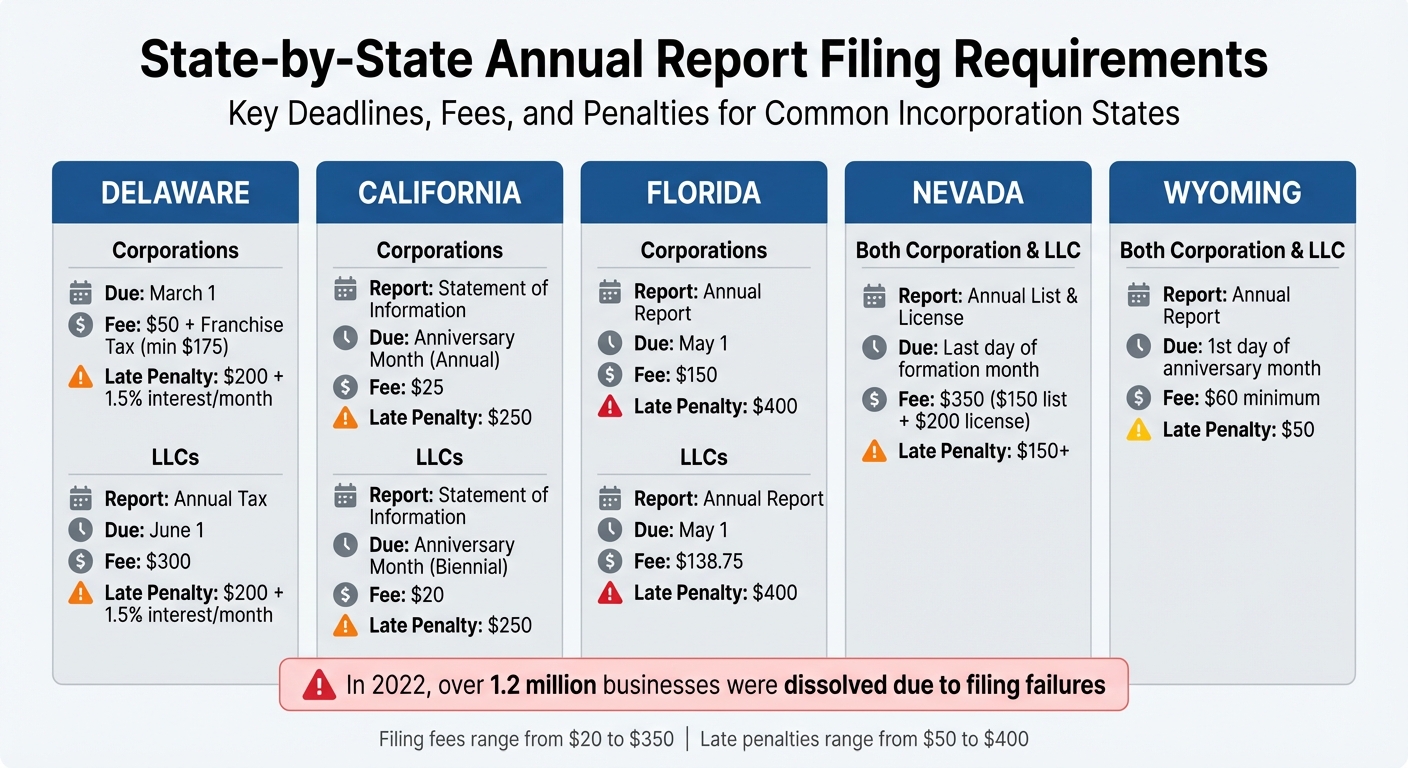

State-by-State Filing Requirements Comparison

State-by-State Annual Report Filing Requirements and Penalties Comparison

Filing requirements for businesses vary by state, so it’s crucial for startups to understand the specific rules where they operate. Some states set deadlines based on the calendar year, while others tie them to the company’s formation anniversary. Filing fees range significantly, from $20 in California to $350 in Nevada, with late penalties reaching as high as $400 in Florida.

Here’s a breakdown of key filing details for some of the most common states for incorporation. This table highlights the essential information you’ll need to stay compliant:

| State | Entity Type | Report Name | Due Date | Filing Fee | Late Penalty |

|---|---|---|---|---|---|

| Delaware | Corporation | Annual Report | March 1 | $50 + Franchise Tax (min $175) | $200 + 1.5% interest/month |

| LLC | Annual Tax | June 1 | $300 | $200 + 1.5% interest/month | |

| California | Corporation | Statement of Information | Anniversary Month (Annual) | $25 | $250 |

| LLC | Statement of Information | Anniversary Month (Biennial) | $20 | $250 | |

| Florida | Corporation | Annual Report | May 1 | $150 | $400 |

| LLC | Annual Report | May 1 | $138.75 | $400 | |

| Nevada | Corporation & LLC | Annual List & License | Last day of formation month | $350 ($150 list fee + $200 license fee) | $150+ |

| Wyoming | Corporation & LLC | Annual Report | 1st Day of Anniversary Month | $60 minimum | $50 |

Delaware has unique deadlines: corporations must file their Annual Report by March 1, while LLCs only need to pay an annual tax of $300 by June 1 without submitting a formal report. For corporations, the franchise tax can range from $175 to over $200,000, depending on the number of authorized shares.

In California, corporations file annually, while LLCs submit their Statement of Information every two years. On top of this, all California entities are subject to an $800 annual franchise tax, regardless of profitability.

Florida enforces a fixed deadline of May 1 for all entities, with a harsh late penalty of $400 for missed filings. Nevada combines its Annual List with a $200 business license renewal, making the total filing fee $350. Meanwhile, Wyoming calculates its filing fee based on the value of assets located in the state, starting at $60 for every $250,000 in assets, with a $60 minimum.

If your startup operates in multiple states, staying on top of these varying requirements is essential to avoid compliance issues. Consider setting reminders 90, 60, and 30 days before each deadline. Keep in mind that some states, like New York and Florida, may not send out paper reminders, so relying solely on state notifications could leave you exposed. Also, double-check your formation dates – some states base deadlines on your incorporation month rather than the calendar year-end. Missing these deadlines can result in costly penalties or even administrative dissolution.

This comparison underscores the importance of understanding and managing state-specific filing obligations to keep your business in good standing.

Conclusion

Staying on top of annual report compliance is crucial for protecting your startup’s legal foundation. Missing even a single deadline can lead to penalties ranging from $25 to $400, the loss of limited liability protection, or, in severe cases, administrative dissolution. In 2022 alone, over 1.2 million business entities faced dissolution due to filing failures.

The five compliance tasks we’ve discussed – state annual reports, registered agent requirements, BOIR filings, multi-state Statements of Information, and S-Corp elections – are essential for maintaining your "Good Standing" status. This status is far more than just a box to check; it’s what allows you to open bank accounts, secure funding, defend against lawsuits, and expand into new markets. Investors are even beginning to factor compliance history into their ESG evaluations, viewing filing lapses as indicators of poor governance.

BusinessAnywhere simplifies compliance management by consolidating everything into one easy-to-use dashboard. Instead of navigating multiple state portals and tracking countless deadlines, you’ll have access to automated tracking, registered agent services (free for the first year), and compliance alerts. With tiered reminders sent 90, 60, 30, and 7 days before deadlines , BusinessAnywhere helps ensure you never miss a critical filing, even for multi-state operations.

FAQs

How do I find my exact annual report due date in each state?

To determine the exact due date for your annual report, visit your state’s Secretary of State website or other state-specific resources. Deadlines can differ depending on the state and might be tied to factors like your business’s fiscal year or the date it was registered. These sites usually offer clear filing instructions and outline key details, including potential late fees or penalties.

What should I do if my business is marked “delinquent” or “inactive” by a state?

If your business is labeled as “delinquent” or “inactive,” it usually means you’ve missed important compliance steps, like filing an annual report. To resolve this, you’ll need to file the overdue report, pay any associated late fees, and make sure your business information is up to date. If your business has been administratively dissolved, most states offer a way to reinstate it by submitting the necessary filings and fees. Taking action promptly is key to avoiding further penalties or, worse, permanent dissolution.

Do I need to file a BOIR if I add investors or change executives?

If your business falls under the Corporate Transparency Act (CTA), you’re required to file a Beneficial Ownership Information Report (BOIR) whenever there are changes in beneficial ownership. This includes scenarios like bringing on new investors or altering your executive team. Non-compliance isn’t something to take lightly – it can lead to penalties of up to $592 per day, hefty fines, or even imprisonment. Stay on top of your reporting duties to steer clear of these serious repercussions.