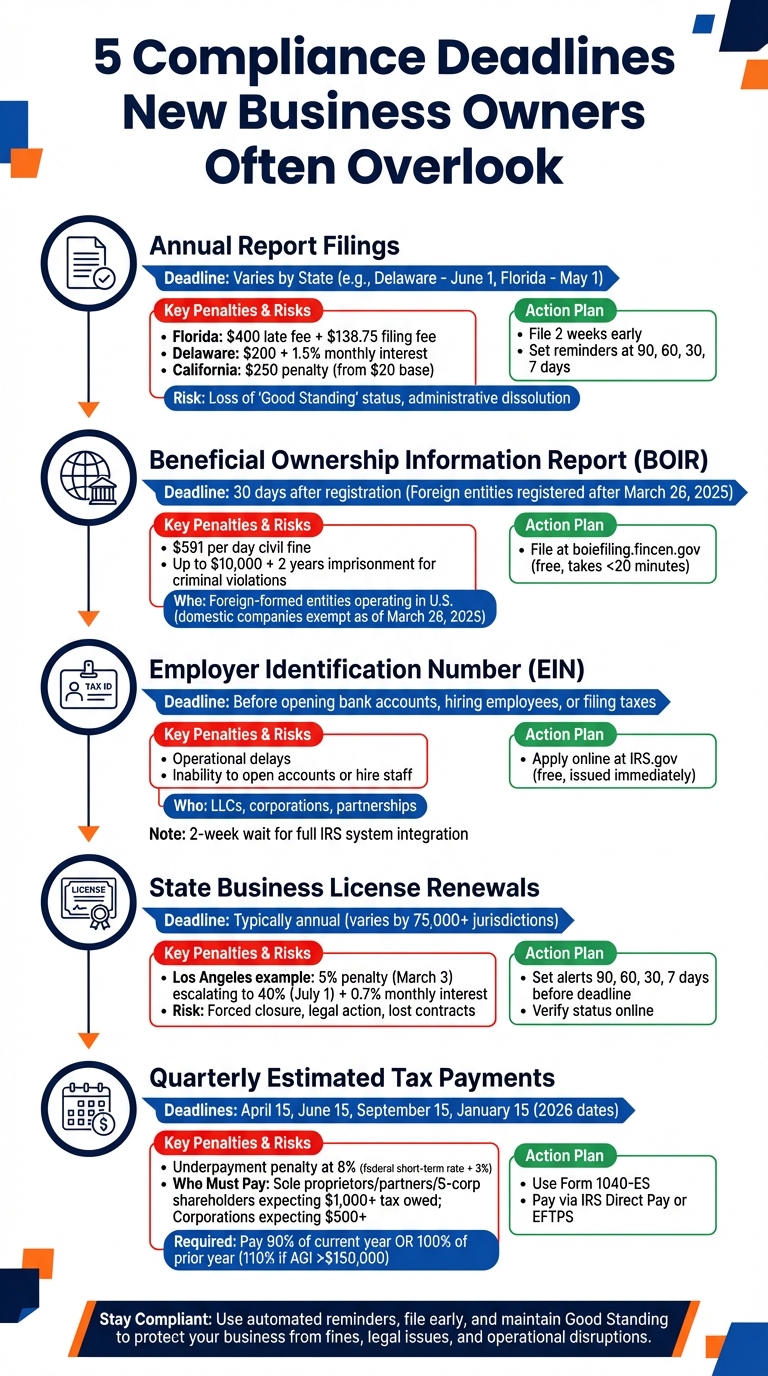

Missing compliance deadlines can cost your business big – financially, legally, and operationally. New business owners frequently overlook key dates, exposing themselves to penalties, loss of legal protections, and even business closure. Here’s a quick rundown of the five most commonly missed compliance deadlines and why they matter:

- Annual Report Filings: Failing to file can lead to fines (e.g., $400 in Florida) and loss of "Good Standing" status, which is critical for loans, contracts, and legal protections.

- Beneficial Ownership Information Report (BOIR): Required for foreign-formed entities operating in the U.S. Missing this could result in daily fines of $591 or criminal penalties.

- Employer Identification Number (EIN) Application: Essential for taxes, bank accounts, and hiring employees. Without it, operations can stall.

- State Business License Renewals: Expired licenses can lead to forced closures, fines, or legal troubles. Deadlines vary by jurisdiction.

- Quarterly Estimated Tax Payments: The IRS requires taxes as income is earned. Missing payments results in penalties and interest charges.

Key takeaway: Staying ahead of these deadlines protects your business from fines, legal issues, and operational disruptions. Use reminders, file early, and leverage tools like compliance platforms to stay on track.

5 Critical Compliance Deadlines for New Business Owners: Penalties and Filing Requirements

1. Annual Report Filings

Why This Matters for New Business Owners

Filing an annual report is more than just a formality – it’s a critical step in keeping your business legally compliant. This report updates the state on key details, such as your legal name, principal office address, registered agent, and officers’ names. Skipping this requirement can have serious consequences. Without it, you might struggle to open bank accounts, secure loans, or expand your operations into new states. Even more concerning, you could lose the "corporate veil", which protects your personal assets from business liabilities.

"Annual report filing mistakes are the number one mistake companies make that may put them at risk of facing penalties, losing corporate privileges, and damaging their reputation." – Logan Jackonis, Head of Operations and Services at Commenda

Penalties for Missing the Deadline

Missing your annual report deadline can be costly – both financially and operationally. For instance:

- In Florida, you’ll face a $400 non-waivable late fee in addition to the standard $138.75 filing fee.

- Delaware imposes a $200 penalty plus 1.5% monthly interest on unpaid amounts.

- In California, a simple $20 filing fee can balloon into a $250 penalty if you’re late.

But the penalties don’t stop at fees. Your business’s public status could be downgraded to "Delinquent" or "Suspended", which can harm your reputation with clients and investors. If non-compliance continues, your business could face administrative dissolution. This means your company would legally cease to exist, lose its ability to sue or defend in court, and risk its name being taken by someone else. Alarmingly, delinquent businesses also become easy targets for identity thieves who exploit these vulnerabilities.

Steps to File on Time

Avoiding these pitfalls is easier than you think. Here’s how to stay on track with your annual report:

- Know your deadline: Some states have fixed deadlines, like Delaware (June 1) or Florida (May 1), while others tie the deadline to your business’s formation month.

- Set reminders: Schedule alerts at 90, 60, 30, and 7 days before the deadline to give yourself plenty of time to review and submit.

- Update your registered agent’s info: Ensure their address is accurate since they receive official compliance notices.

- File early: Submit your report at least two weeks before the deadline to avoid last-minute technical issues with state portals.

- Confirm your status: After filing, check your state’s business database to ensure your status is listed as "Active" or in Good Standing.

2. Beneficial Ownership Information Report (BOIR)

Why This Matters for New Business Owners

If you’re launching a business, understanding the BOIR is crucial, especially if your company has ties outside the U.S. While domestic companies in the U.S. are exempt from filing this report starting March 26, 2025, foreign-formed entities registered to operate in the U.S. must comply. The BOIR, established under the Corporate Transparency Act, is designed to reveal the individuals who ultimately own or control a company. This measure aims to curb money laundering and other illegal financial activities.

For foreign reporting companies, filing is typically a one-time task. Updates are only required if there’s a change in ownership details.

"All entities created in the United States – including those previously known as ‘domestic reporting companies’ – and their beneficial owners are now exempt from the requirement to report beneficial ownership information (BOI) to FinCEN." – FinCEN

Penalties for Missing the Deadline

Failing to comply with BOIR requirements can lead to steep penalties. Civil fines can reach up to $591 per day, while criminal penalties may include fines of up to $10,000 and up to two years of imprisonment for intentional violations.

Be cautious of scams: FinCEN does not send unsolicited messages requesting payments. Any mention of "Form 4022", "Form 5102", or the "US Business Regulations Dept." in unsolicited communication is fraudulent.

Steps to File on Time

Start by confirming whether you need to register a company in the USA and file. U.S.-based companies are exempt, but if your business was formed abroad and registered to operate in a U.S. state, you must file within 30 calendar days of your registration becoming effective (for registrations after March 26, 2025).

Use the official FinCEN BOI E-Filing System at boiefiling.fincen.gov to file your report for free. You’ll need to provide:

- Your company’s legal name, U.S. address, formation jurisdiction, and Tax ID.

- Information about each beneficial owner (anyone owning 25% or more or with significant control), including their name, birth date, address, and an acceptable form of ID.

For straightforward ownership structures, the process takes less than 20 minutes, according to FinCEN. If your company’s ownership details change, you must submit an updated report within 30 days. Staying on top of this ensures compliance and helps you avoid unnecessary penalties.

3. Employer Identification Number (EIN) Application

Why This Matters for New Business Owners

An EIN, or Employer Identification Number, acts as your business’s federal tax ID. If you’re starting an LLC, corporation, or partnership, having an EIN is a legal requirement. It’s a cornerstone for handling taxes and meeting other compliance obligations.

Without an EIN, you’ll face roadblocks like being unable to open a business bank account, apply for local licenses, or hire employees. The good news? The IRS issues EINs for free through its official website. Avoid paying third-party services that charge fees for something you can do yourself at no cost.

Steps to File on Time

The fastest way to secure an EIN is through the IRS’s online application. It’s quick – your EIN is issued immediately after you complete the process. The online portal operates during extended hours, but keep in mind that sessions expire after 15 minutes of inactivity. To avoid disruptions, gather all required details beforehand.

Before applying, ensure your business entity is already registered with the state. When completing the application, you’ll need to provide your business’s legal name, entity type, and the Social Security Number or ITIN of the "responsible party" (the individual managing the entity). Also, note that the IRS allows only one EIN application per responsible party per day.

Once you’ve got your EIN, you can use it right away for tasks like opening a bank account or applying for licenses. However, it typically takes about two weeks for the number to be fully integrated into the IRS system. During this time, you won’t be able to e-file tax returns or make electronic payments. If a tax return is due before your EIN is processed, simply enter "Applied For" along with the application date in the EIN field. For tax deposits, send a check or money order to your state’s IRS service center, including your business name, address, tax type, and application date.

If you’d rather not handle the process yourself, services like BusinessAnywhere’s EIN application service can take care of the filing for you. Acting quickly to secure your EIN not only simplifies other compliance steps but also helps protect your business from potential fines or penalties.

4. State Business License Renewals

Why This Matters for New Business Owners

A state business license is your official green light to operate legally, usually valid for about a year. Once it expires, continuing operations without renewal puts your business in hot water. With over 75,000 federal, state, and local jurisdictions in the U.S. – each with its own renewal schedules and requirements – staying compliant can feel overwhelming. But keeping your license current is non-negotiable if you want to protect your business and its reputation.

Renewing on time is more than just a legal formality. It ensures your company remains in good standing, a crucial factor for securing loans or expanding into new markets. Plus, licenses are public records – an expired status can harm your reputation with clients and partners alike.

"As a business owner, it is your responsibility to pay the license renewal fee by the due date, even if you did not receive a renewal notice." – CT Corporation Staff

Penalties for Missing the Deadline

Miss your renewal deadline, and the consequences can pile up fast. Take Los Angeles as an example: For 2026, business tax renewals were due January 1, with penalties starting at 5% on March 3 and climbing to 40% by July 1, along with a 0.7% monthly interest rate. Some jurisdictions are even stricter, marking licenses as expired after just one day.

The fallout doesn’t stop at fines. Non-renewal can lead to forced closures or legal trouble. In August 2025, several funeral homes in Georgia faced cease-and-desist orders and fines for operating with expired licenses. A South Carolina business owner was arrested in 2026 for running a retail business without a valid license. Meanwhile, a California subcontractor lost work on a $100 million contract and was hit with a $200,000 fine for failing to renew their state contractor license. Staying ahead of deadlines is the only way to avoid these costly headaches.

Steps to File on Time

Avoid penalties and disruptions by planning your renewal process well in advance. Set up calendar alerts at 90, 60, 30, and 7 days before your renewal deadline. Don’t rely on reminder notices – many jurisdictions won’t send one, and the responsibility to renew falls squarely on you. Regularly check your license status online to catch any potential issues early.

Before filing, ensure all your business details are accurate. Changes like a new business name, ownership structure, address, or activities may require updates outside the typical renewal schedule. Always keep copies – both digital and physical – of your renewal confirmations for your records.

If juggling multiple deadlines feels like too much, services like BusinessAnywhere’s registered agent service can help. They provide compliance alerts to keep you on track, saving you from costly penalties and ensuring your operations run smoothly.

sbb-itb-ba0a4be

5. Quarterly Estimated Tax Payments

This deadline plays a crucial role in keeping your business financially and legally on track.

Why This Matters for New Business Owners

The IRS follows a "pay-as-you-go" system, meaning taxes must be paid as income is earned, not just at the end of the year when filing your annual return. For new business owners, this means making quarterly estimated tax payments to cover income tax, self-employment tax (Social Security and Medicare), and alternative minimum tax. If you’re a sole proprietor, partner, or S-corp shareholder and expect to owe $1,000 or more in taxes, you’re required to make these payments. For corporations, the threshold is $500.

"Estimated taxes are a vital part of managing your tax obligations if you earn income outside of having a ‘traditional’ job." – Jacob Dayan, CEO, Community Tax LLC

Unlike employees with automatic paycheck withholdings, business owners must calculate and submit payments themselves. This applies to income from self-employment, interest, dividends, rents, and capital gains. Failing to manage this responsibility can lead to more than cash flow issues – it can result in penalties and interest charges.

Meeting quarterly payment deadlines not only helps you avoid penalties but also ensures your business remains financially stable.

Penalties for Missing the Deadline

The IRS doesn’t wait until tax season to collect what’s owed. If you fail to pay at least 90% of your current year’s tax liability or 100% of your prior year’s tax (110% if your adjusted gross income exceeded $150,000), you’ll incur an underpayment penalty. This penalty is calculated using the federal short-term interest rate plus 3%, which stood at 8% as of late 2025. Interest continues to accrue from the original due date of each payment until the full amount is paid.

"If you don’t pay enough tax by the due date of each of the payment periods, you may be charged a penalty even if you are due a refund when you file your income tax return." – Internal Revenue Service

To avoid penalties, you must owe less than $1,000 after accounting for withholding and credits or meet the safe harbor thresholds outlined above. While the IRS may waive penalties for "reasonable cause" – like a disaster, retirement after age 62, or becoming disabled during the tax year – these exceptions are rare.

Staying on top of your estimated tax payments is the best way to avoid these financial setbacks.

Steps to File on Time

To manage your quarterly payments effectively:

- Use Form 1040-ES to estimate your adjusted gross income, taxes, deductions, and credits for the year. Mark these 2026 quarterly deadlines: April 15, June 15, September 15, and January 15, 2027. If a deadline falls on a weekend or holiday, payments are due the next business day.

- Open a separate bank account for estimated taxes and regularly transfer a percentage of your income into it. This ensures you’re prepared when payments are due.

- Recalculate mid-year using a new Form 1040-ES worksheet if your income changes significantly. Seasonal businesses can use the "annualized income installment method" on Form 2210 to make payments that align with their cash flow.

- Pay electronically through IRS Direct Pay or EFTPS to schedule payments and keep records.

- Adjust W-2 withholdings if you also have a traditional job. Submitting a new Form W-4 can help cover your business tax obligations and possibly eliminate the need for separate quarterly payments.

How BusinessAnywhere Helps You Stay Compliant

Staying on top of compliance deadlines can feel overwhelming, especially when juggling multiple tasks. BusinessAnywhere simplifies this process by consolidating all your compliance responsibilities into one easy-to-navigate dashboard. From annual report filings and BOIR submissions to EIN applications and renewals, everything is organized in one place. The platform also takes care of sending automated reminders for critical deadlines, including tax filings, compliance renewals, your company’s formation anniversary (key for maintaining liability protection), and even contract renewals with vendors or landlords. Plus, it doesn’t just track tasks – it automates key filings to save time and reduce stress.

As your registered agent service, BusinessAnywhere steps in as the official point of contact for state and legal notifications, ensuring you never miss an important update. This service is available for $147 per year, offering peace of mind that your compliance obligations are in good hands.

"Never miss a deadline or important notification again." – BusinessAnywhere

The platform takes automation a step further by handling filings for you. Whether it’s managing annual reports across all 50 states, BOIR submissions, or EIN applications, BusinessAnywhere ensures these tasks are completed seamlessly and at clear, upfront fees. Forget about navigating confusing government websites or deciphering complex forms – everything is managed directly through the platform.

For those already running a business, integrating your existing company into the system is quick and efficient, typically taking just 1–2 business days. Once set up, you’ll gain access to features like document management tools, mail scanning and forwarding through a virtual mailbox, and robust compliance tracking. These tools not only keep your business compliant but also free up your time to focus on growth.

"It’s a business entity that updates clients using customized email alerts." – BusinessAnywhere

Conclusion

Missing deadlines can jeopardize your business’s legal standing and operational status. Each compliance deadline serves as a safeguard, protecting your business from serious legal and financial risks. Falling behind could mean losing the corporate veil that separates your personal assets from business liabilities, forfeiting legal protections, or even facing administrative dissolution, which opens the door for others to claim your business name.

Staying on top of compliance deadlines also helps you avoid costly penalties from both federal and state authorities. These fines can quickly add up, ranging from monthly IRS charges to steep state-level penalties and BOIR violations.

"Compliance functions may seem like a business expense, but the costs of non-compliance – such as failed deals or financing, severed partnerships and costly penalties – far exceed the investment in compliance."

This highlights the importance of viewing compliance not as a cost but as an investment in your business’s stability and future. A strong compliance record boosts your company’s appeal to investors and buyers during due diligence, while also ensuring that you maintain Good Standing. This status is critical for keeping business bank accounts, securing loans, processing credit card payments, and bidding on government contracts.

BusinessAnywhere simplifies compliance with automated reminders, centralized tracking, and professional registered agent services – all for $147 per year. From annual reports to BOIR submissions, the platform handles the heavy lifting, ensuring your business stays protected and compliant. By staying ahead of deadlines with reliable tools, you safeguard your company’s assets and position it for growth.

FAQs

How can I find my exact annual report due date by state?

To figure out when your annual report is due, visit your state’s official Secretary of State website or use trusted compliance resources. These platforms usually provide clear deadlines based on your business type and the date you registered. Make sure to double-check your state’s specific rules to ensure you don’t miss any important filing dates.

Does my business need to file a BOIR if it’s U.S.-formed but has foreign owners?

Yes, businesses formed in the U.S. with foreign owners are typically required to file a BOIR. Most entities with foreign ownership that are registered to operate in the U.S. must report their beneficial ownership information to FinCEN. This requirement ensures adherence to federal rules and helps prevent potential penalties.

How can I estimate quarterly taxes if my income changes month to month?

When dealing with fluctuating income, estimating quarterly taxes can feel tricky. Start by calculating based on your expected annual income, then divide that total into four equal payments. This aligns with the IRS’s "safe harbor" rule, which helps you avoid penalties as long as you pay enough throughout the year.

If your income shifts during the year, adjust your future payments to reflect those changes. This way, you can stay on track and avoid surprises at tax time. To make things easier, consider automating your payments or recalculating every quarter. These steps can help ensure your payments are accurate and reduce the risk of underpaying.