Opening a U.S. business bank account as a non-resident founder can be challenging, but fintech platforms like Mercury, Relay, Lili, Airwallex, and Brex make it easier. These platforms let you open accounts remotely, without requiring an SSN or in-person visits, and offer features tailored to international entrepreneurs. Here’s a quick breakdown:

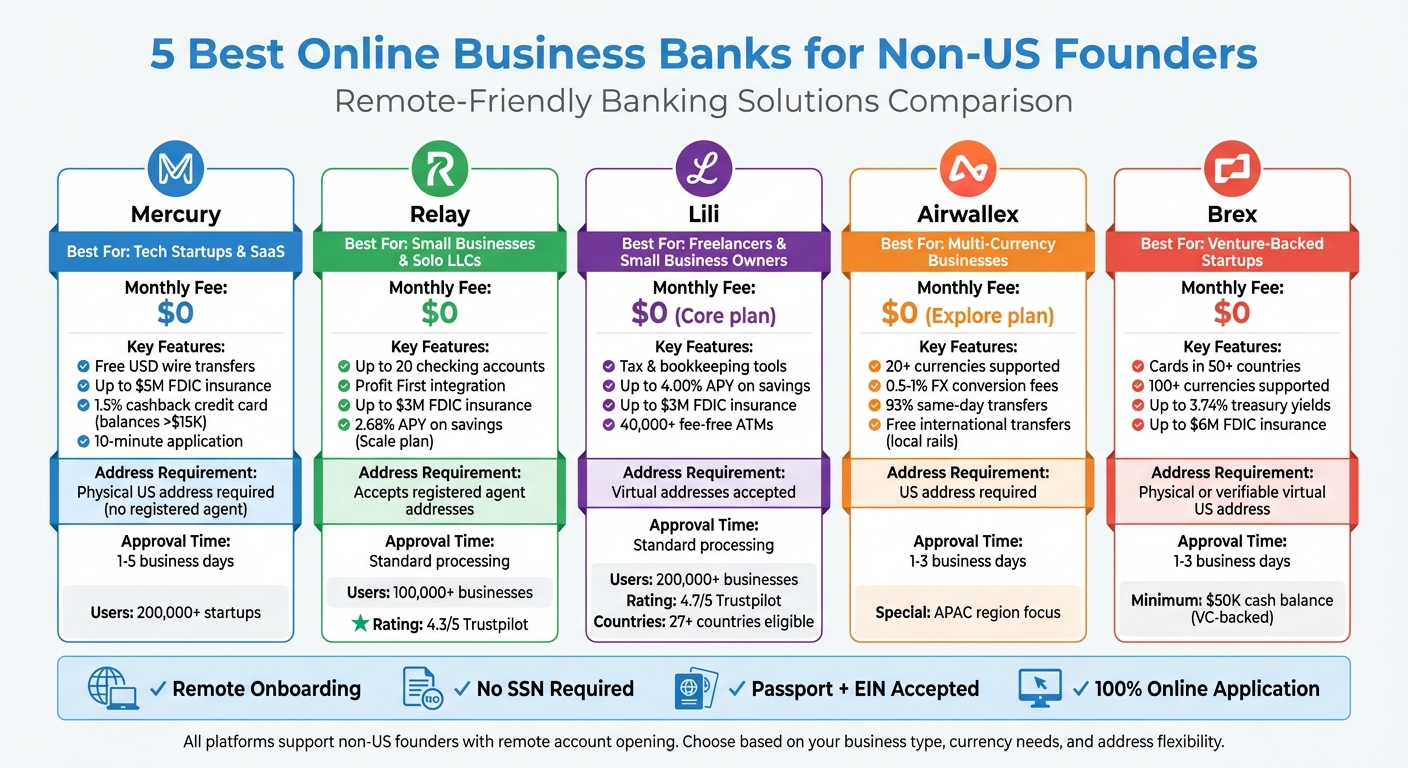

- Mercury: Great for tech startups; no monthly fees, free USD wire transfers, but requires a physical U.S. address.

- Relay: Ideal for small businesses; allows up to 20 checking accounts and accepts registered agent addresses.

- Lili: Best for freelancers; offers tax tools, bookkeeping, and savings accounts with up to 4.00% APY.

- Airwallex: Perfect for multi-currency businesses; low FX fees and fast international transfers.

- Brex: Designed for venture-backed startups; supports global spending with advanced financial tools.

Quick Tip: You’ll need an EIN, business formation documents, and a U.S. address (virtual or physical) to get started. Platforms like BusinessAnywhere can assist with these requirements.

1. Mercury

Mercury has become a go-to choice for international entrepreneurs, with over 200,000 startups relying on it for U.S. banking needs. The application process is entirely online, taking just about 10 minutes, and approvals are typically completed within 1–5 business days. What’s convenient is that you don’t need a Social Security Number – just your international passport and an IRS-issued Employer Identification Number (EIN). These minimal requirements make Mercury far more accessible than traditional banks.

Mercury offers $0 monthly fees, free domestic and international USD wire transfers, and up to $5 million in FDIC insurance through its partner banks. If you need to send non-USD international wires, there’s a 1% currency exchange fee. Mark Zhang, CEO of Manta Sleep, shared his experience:

"Mercury is so intuitive and saves us so much time. Plus, free international USD transfers save us a ton of money when we pay our suppliers overseas."

To use Mercury, your business must be a U.S.-registered LLC or C-Corp, and you’ll need to provide a physical U.S. address – P.O. boxes and registered agent addresses aren’t allowed. Keep in mind, Mercury doesn’t support businesses in industries like cannabis, internet gambling, adult entertainment, or money services.

The platform integrates seamlessly with accounting tools like QuickBooks, Xero, and NetSuite. As part of the KYC process, you’ll need to complete a selfie verification during the application. Once approved, you’ll receive virtual debit cards immediately, while physical debit cards are shipped within 7–10 business days.

For accounts with balances exceeding $15,000, Mercury offers the IO Mastercard credit card, which provides 1.5% unlimited cashback on all spending. Paid plans, starting at $35 per month, unlock advanced features like mass payments via API and enhanced NetSuite automations.

2. Relay

Relay is designed with international entrepreneurs in mind, offering support to business owners across more than 200 countries, including Canada, the UK, and Australia. The onboarding process is entirely remote – no need for branch visits or a U.S. address. Plus, Relay doesn’t require a Social Security Number, making it accessible for non-U.S. residents. But what truly sets Relay apart are its features that simplify managing your business finances.

One standout feature is Relay’s integration with the Profit First system, allowing you to open up to 20 individual checking accounts. You can assign custom nicknames and automate percentage-based transfers between accounts. Mike Michalowicz, the creator of Profit First, praises the platform:

"Relay is the only banking platform that I know of that supports Profit First right out of the box. It is so easy to set up. I would go to Relay immediately."

Relay also keeps costs low with $0 monthly fees and no minimum balance requirements. Your deposits are insured by the FDIC up to $3 million through its partner, Thread Bank. With a 4.3/5 rating on Trustpilot and trust from over 100,000 small businesses, Relay has built a strong reputation. Savings accounts on the Scale plan offer up to 2.68% APY, and physical Visa debit cards can be shipped internationally within 8–10 business days. Understanding the eligibility requirements can help you get started smoothly.

To qualify, your business must be a U.S.-registered LLC, corporation, general partnership, or sole proprietorship. Relay doesn’t accept Proton Mail addresses, so you’ll need to use Gmail, Outlook, or your business domain email. Additionally, certain industries are excluded, such as cryptocurrency exchanges, firearms, credit repair, and cannabis sales.

Relay further boosts its utility by integrating directly with QuickBooks Online and Xero for accounting, as well as Gusto for payroll management. You’ll also have access to over 55,000 free Allpoint ATMs for cash withdrawals and can deposit checks via its iOS and Android apps.

3. Lili

Lili stands out as a solid option for international entrepreneurs seeking a U.S. business bank account. This platform allows founders from over 27 countries – including Canada, the UK, Germany, Australia, India, and Brazil – to onboard remotely without setting foot in the U.S.. With more than 200,000 businesses served and a 4.7/5 rating on Trustpilot from over 3,900 reviews, Lili has gained recognition, including being named "Best U.S. Digital Bank for SMBs 2025" by the International Investor Awards.

One of Lili’s key advantages is that non-resident founders don’t need a Social Security Number. Instead, an EIN and a valid passport are sufficient. The platform also waives monthly fees for its Core account and offers up to 4.00% APY on business savings balances. Plus, FDIC insurance covers balances up to $3 million through a network of partner banks. Liran Zelkha, Lili’s CTO and Co-Founder, highlights a major pain point for entrepreneurs:

"Transferring funds across borders comes at a steep price – payment gateways can eat up as much as 5% of their revenue, not to mention additional currency exchange fees".

To open an account, you’ll need a registered U.S. business entity, such as an LLC, C-Corp, or Partnership, as sole proprietorships aren’t eligible for international applicants. Required documents include your EIN confirmation letter, Articles of Organization or Incorporation, and a U.S. business address (virtual addresses are typically accepted). If you don’t already have an EIN, you’ll need to apply by submitting IRS Form SS-4 via fax or mail, which can take several weeks.

Lili also simplifies financial management. Its Core account integrates invoicing, accounting, and tax tools – all without monthly fees. International transfers cost $25 outbound and $15 inbound, supporting over 130 currencies. Debit card purchases have no foreign transaction fees, and users can access over 40,000 MoneyPass ATMs across the U.S. without withdrawal charges. However, note that using a VPN during the application process is prohibited, and VoIP phone numbers aren’t accepted for verification.

Luke Bivens, Founder of QC Growth, shared his thoughts on the platform:

"Lili has been an amazing tool for me in running my business. It was extremely easy to set up and makes it extremely easy for me to manage my company’s spending".

With 83% of customers rating its support team as a 9 or 10 out of 10, Lili combines convenience and dependability, making it a strong choice for international entrepreneurs navigating U.S. banking.

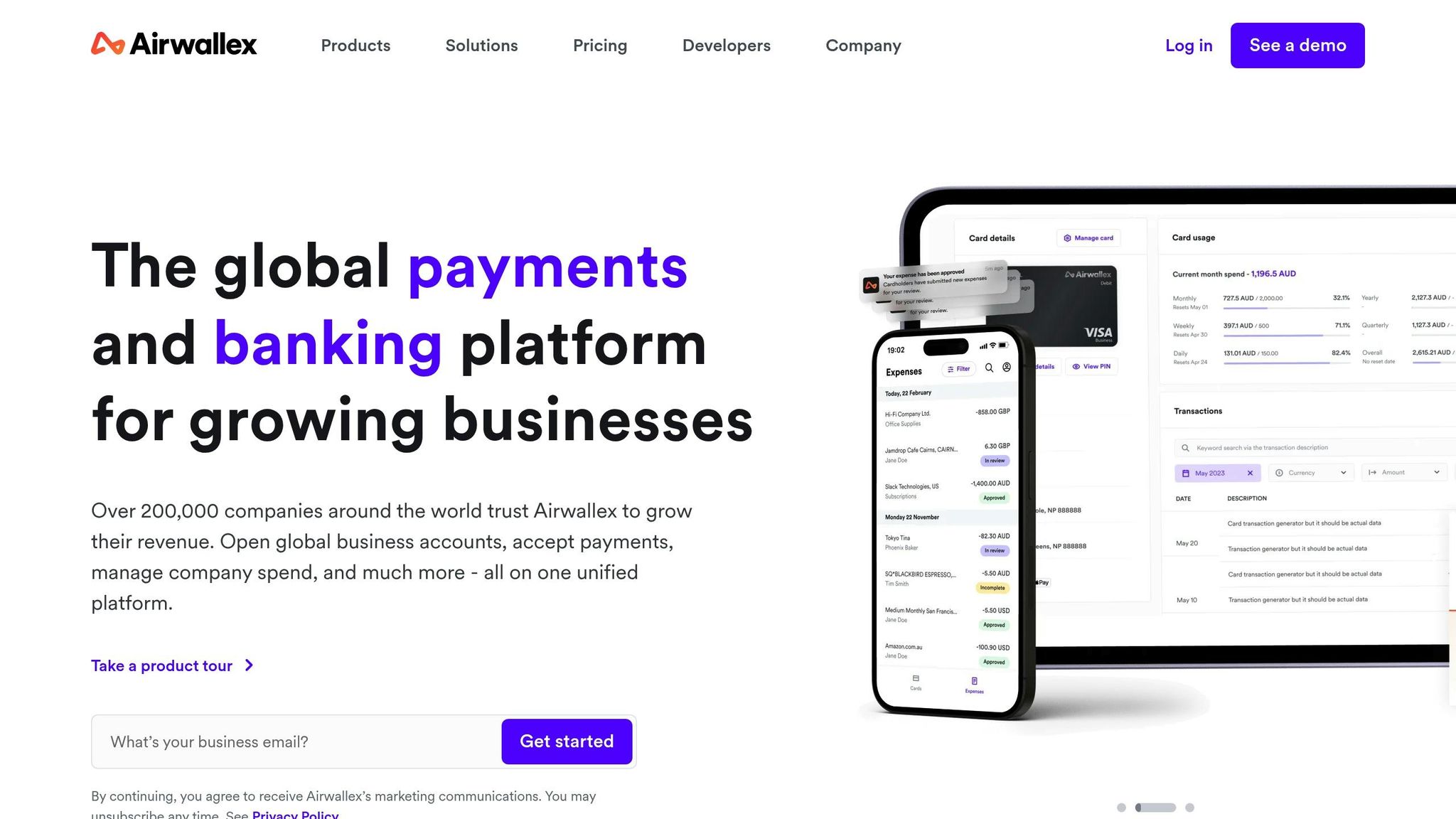

4. Airwallex

Airwallex offers a streamlined way for non-US founders to open a U.S. business bank account entirely online. With approval times ranging from 1 to 3 business days, the platform provides local USD bank details to simplify transactions.

One standout feature is its ability to handle over 20 currencies, with foreign exchange (FX) conversion markups between 0.5% and 1% – a noticeable improvement compared to the 2%–3% typically charged by traditional banks. Additionally, 93% of global transfers through Airwallex reportedly arrive on the same day, making it a reliable option for fast international payments.

To get started, you’ll need to submit a few key documents: your Certificate of Formation (or Incorporation), IRS EIN letter, a government-issued photo ID, and proof of a residential address dated within the last 90 days. If your business primarily operates outside the U.S., you might also need to provide a statement from a U.S. bank.

The platform’s free Explore plan is appealing, with no monthly fees, no minimum deposits, and no balance requirements. International transfers to over 120 countries are free when using local payment rails, though SWIFT transfers come with fees ranging from $15 to $25. Airwallex also integrates with popular tools like Xero, QuickBooks, Shopify, and Amazon, making it a flexible choice for various business needs.

For smoother account setup, use a high-resolution scanner instead of a phone camera when submitting documents. Ensure that your business name matches exactly across all documents, including your EIN letter and formation papers, to avoid delays. If you need advanced features like NetSuite or HR integrations, you can upgrade to the Grow plan for $99 per month.

5. Brex

Brex is a strong option for non-US founders managing US-based businesses worldwide. The entire application process is online and uses your passport for identity verification. It typically takes 15 to 30 minutes to complete, with approval decisions arriving in 1 to 3 business days.

Brex provides extensive global capabilities: you can issue both physical and virtual cards in over 50 countries and monitor spending in more than 100 currencies from a single dashboard. Mike Duffy, Director and Assistant Controller at Lemonade, highlights the benefits:

"Consolidating onto Brex’s global cards for our teams around the world allows us to see and analyze spend across our entities in one dashboard – all while operating in local currencies".

The platform’s multi-entity feature also makes managing expenses across subsidiaries straightforward.

To qualify, your business must have a US EIN, be incorporated as a C-corp, S-corp, LLC, or LLP, and maintain a physical or verifiable virtual US address. Venture-backed startups need a minimum cash balance of $50,000 (lower if referred), while commercial businesses must generate at least $1 million annually.

Brex accounts come with several perks: no monthly maintenance fees, unlimited free same-day ACH payments, and free domestic and international wire transfers. Additionally, Brex offers a treasury product with yields up to 3.74% and up to $6 million in FDIC coverage through a network of 24 partner banks. However, keep in mind that international payments may include a markup for currency conversions.

Before applying, gather PDFs of your Articles of Incorporation, EIN letter, and valid passports for all owners with 25% or more ownership. If using a virtual address, you’ll also need a recent utility bill, lease, or bank statement. Don’t forget to check the Brex Restricted Activities List to ensure compliance. This overview of Brex’s features and requirements sets the stage for the upcoming platform comparison table.

sbb-itb-ba0a4be

Comparison Table

Here’s a snapshot of the key features of five online business banks tailored for non-US founders:

| Bank | Remote Onboarding | SSN Required | Monthly Fees | Primary Use Case | Non-US Founder Eligibility |

|---|---|---|---|---|---|

| Mercury | Yes | No | $0 | Tech startups, SaaS, Stripe-based businesses | Yes – but requires a physical US address (Registered Agent addresses not accepted) |

| Relay | Yes | No | $0 | Solo owners, single-member LLCs, cash management | Yes (accepts Registered Agent addresses) |

| Lili | Yes | No | $0 (Core plan) | Freelancers needing tax and bookkeeping tools | Yes (available for founders from Canada, UK, Germany, India, Australia, Brazil) |

| Airwallex | Yes | No | Varies | Multi-currency businesses, APAC region operations | Yes |

| Brex | Yes | No | $0 | Venture-backed startups, multi-entity businesses | Yes |

Looking at the table, you’ll notice some important distinctions. Mercury and Relay both allow passport and EIN documentation, eliminating the need for an SSN or ITIN, which is a big plus for international entrepreneurs. However, there’s a key difference in address requirements: Mercury insists on a physical US address and does not accept Registered Agent addresses, while Relay offers more flexibility by accepting them.

Lili, on the other hand, limits eligibility to founders from six specific countries but compensates with features like integrated tax and bookkeeping tools. Airwallex caters to businesses dealing with multiple currencies, especially those with a focus on the Asia-Pacific region. Brex, meanwhile, is geared toward growth-stage companies with significant capital needs, offering advanced features like multi-entity management and treasury products with yields of up to 3.74%.

All five platforms skip the traditional in-person setup and do not require an SSN, making them accessible options. The right choice depends on your business structure, funding stage, and where your operations are based.

How BusinessAnywhere Assists with Bank Account Setup

Opening a U.S. business bank account from abroad can feel like navigating a maze of paperwork and compliance challenges. BusinessAnywhere simplifies this process by managing the critical steps for you.

At the heart of the process is the EIN (Employer Identification Number) – essential for both tax and banking purposes. For non-residents without a Social Security Number, obtaining an EIN involves submitting IRS Form SS-4 via fax or mail, marking "Foreign" in the SSN field. This typically takes weeks, but BusinessAnywhere’s EIN Application Service ($97 one-time fee) ensures accurate and timely filing. You can learn more about this service here.

Another key requirement is your formation documents, such as Articles of Organization or Incorporation. BusinessAnywhere takes care of this through its $0 Business Registration service. You only pay state fees, while the platform handles the preparation and filing of all necessary documents with the state. This ensures you have everything banks require to proceed. More details can be found here.

One common hurdle for international entrepreneurs is the U.S. address requirement. BusinessAnywhere solves this with its Virtual Mailbox service, starting at $20/month. This service provides a physical U.S. address in states like Florida, Arizona, New Mexico, or Wyoming, where you can receive mail and access unlimited scans. Banks often mandate this, and BusinessAnywhere even includes the first year of service free ($147/year after that) with its Registered Agent Service. Check out the service here.

For those looking for an all-in-one solution, the Digital Nomad Kit is a comprehensive package. It includes LLC registration, EIN processing, registered agent service, a virtual mailbox, compliance tools, and banking setup support – all tailored for non-U.S. persons. Priced at approximately $3,200, this package eliminates the need to juggle multiple providers and ensures all documents meet bank compliance standards, including the Beneficial Ownership Information Reporting Rule, which requires identity verification for anyone owning 25% or more of the business. Learn more about the kit here.

Required Documents and Eligibility Tips

Opening a U.S. business bank account from abroad involves meeting strict documentation requirements to comply with federal laws. Under the USA PATRIOT Act, banks are obligated to verify both your identity and the legitimacy of your business to prevent money laundering and terrorism funding. Knowing what to prepare in advance can save you weeks of delays or even rejection. Here’s what you’ll need to streamline the process.

First, gather your business formation documents, such as the Articles of Incorporation or Organization filed with your state, which confirm your company’s legal existence. You’ll also need your EIN confirmation letter (Form CP-575 or 147C) from the IRS, which serves as your federal tax ID. For personal identification, a valid passport is required for all authorized signers and any individual owning 25% or more of the company. If you don’t have a Social Security Number, you may need an Individual Taxpayer Identification Number (ITIN), but keep in mind that obtaining an ITIN can take 6 to 12 weeks.

Address verification is another common stumbling block. Banks require proof of a physical U.S. business address – a lease agreement or utility bill will work, but PO boxes or mail forwarding services won’t be accepted. Additionally, you’ll need your LLC Operating Agreement or corporate bylaws to confirm who has the authority to open an account. Be prepared to provide beneficial ownership information, including names, dates of birth, and residential addresses for individuals owning 25% or more of the business.

Consistency is key. Ensure that your business name appears exactly the same across all documents – formation papers, EIN letter, and bank application. Even small inconsistencies, like using a DBA instead of your legal name, can lead to rejection. Double-check that addresses and names match everywhere. Having a U.S. phone number, even via a VoIP service, can also help your application pass fraud-prevention checks.

For non-residents, verification can take anywhere from a few business days to up to four weeks. Traditional banks often require you to visit a U.S. branch in person for identity verification – a significant challenge if you’re unable to travel. However, digital banking platforms tailored for remote entrepreneurs offer a convenient alternative. These platforms allow for 100% online applications using passport uploads and digital document verification, making them a practical option for founders based overseas.

Conclusion

Our review highlights how fintech platforms are reshaping the landscape for international founders, offering tailored solutions to meet diverse business needs. Choosing the right platform depends on aligning its features with your operational priorities. For tech startups and SaaS founders, Mercury stands out with its no-fee structure and smooth integrations with major payment processors. Relay is ideal for solo entrepreneurs and single-member LLCs, offering up to 20 sub-accounts to help streamline financial organization. Lili caters to freelancers and small business owners, combining tax automation and bookkeeping with savings rates of up to 4.00% APY on qualifying balances. If your business involves high-volume, multi-currency transactions, Airwallex is a strong contender, especially for operations in the APAC region. Meanwhile, Brex appeals to venture-backed startups with its remote-friendly onboarding process.

Each platform simplifies remote account opening, allowing international founders to set up accounts entirely online. You’ll need a passport, EIN, and formation documents to get started, and most applications are processed within 1–5 days for non-residents. Having a U.S. phone number, even a VoIP line, can further enhance fraud prevention measures. For global e-commerce businesses, Airwallex’s local bank details in 11+ countries can help cut down on FX fees, while Relay’s sub-account system is a practical tool for consultants juggling multiple income streams.

Before diving in, check the key requirements and country eligibility and ensure that your business name is consistent across all documents. If you’re unsure about the setup process, BusinessAnywhere provides support for bank account opening as part of its broader services for international entrepreneurs.

FAQs

What do non-US founders need to open a business bank account in the United States?

To set up a business bank account in the United States as a non-US founder, you’ll need a few key items. First, a registered US business entity, like an LLC or C-Corp, is crucial. This establishes your business’s legal standing. You’ll also need an Employer Identification Number (EIN) from the IRS, which serves as your business’s tax ID.

In addition, banks typically ask for valid identification, such as a passport, to verify your identity. Some banks might require a US address or phone number, but many fintech platforms now allow remote account setup using digital verification tools, eliminating the need for a physical US presence.

Although the process might feel a bit daunting, these steps are in place to ensure compliance with US laws and make banking smoother for international business owners.

What are the key differences between Mercury and Relay for international entrepreneurs?

Mercury and Relay both cater to international entrepreneurs looking for efficient online business banking, but they shine in different ways.

Mercury offers a completely digital account setup, making it easier for non-U.S. founders to open a U.S. business bank account remotely. Its accounts are FDIC-insured, come with free domestic wires in USD, and provide financial management tools. This makes Mercury an appealing choice for startups seeking a straightforward banking solution.

Relay, on the other hand, also enables remote account opening but focuses on features like multi-user access, sub-accounts, and smooth accounting integrations. These features make it a solid option for businesses that need detailed financial organization or collaborative management.

While both platforms aim to simplify banking for non-U.S. residents, Mercury is often preferred for its ease of use, whereas Relay stands out for businesses that require more advanced financial tools.

Can non-US residents use a virtual address to open a US business bank account?

Yes, non-US residents can usually use a virtual address to open a US business bank account. Many online banks and fintech platforms allow you to set up accounts remotely, even if you don’t have a physical US address. Some of these institutions are also open to accepting virtual or foreign addresses during the application process.

However, requirements can differ from one bank to another, so it’s important to check their specific policies before applying. This option makes it easier for international entrepreneurs to manage their US business operations without needing to be in the country.