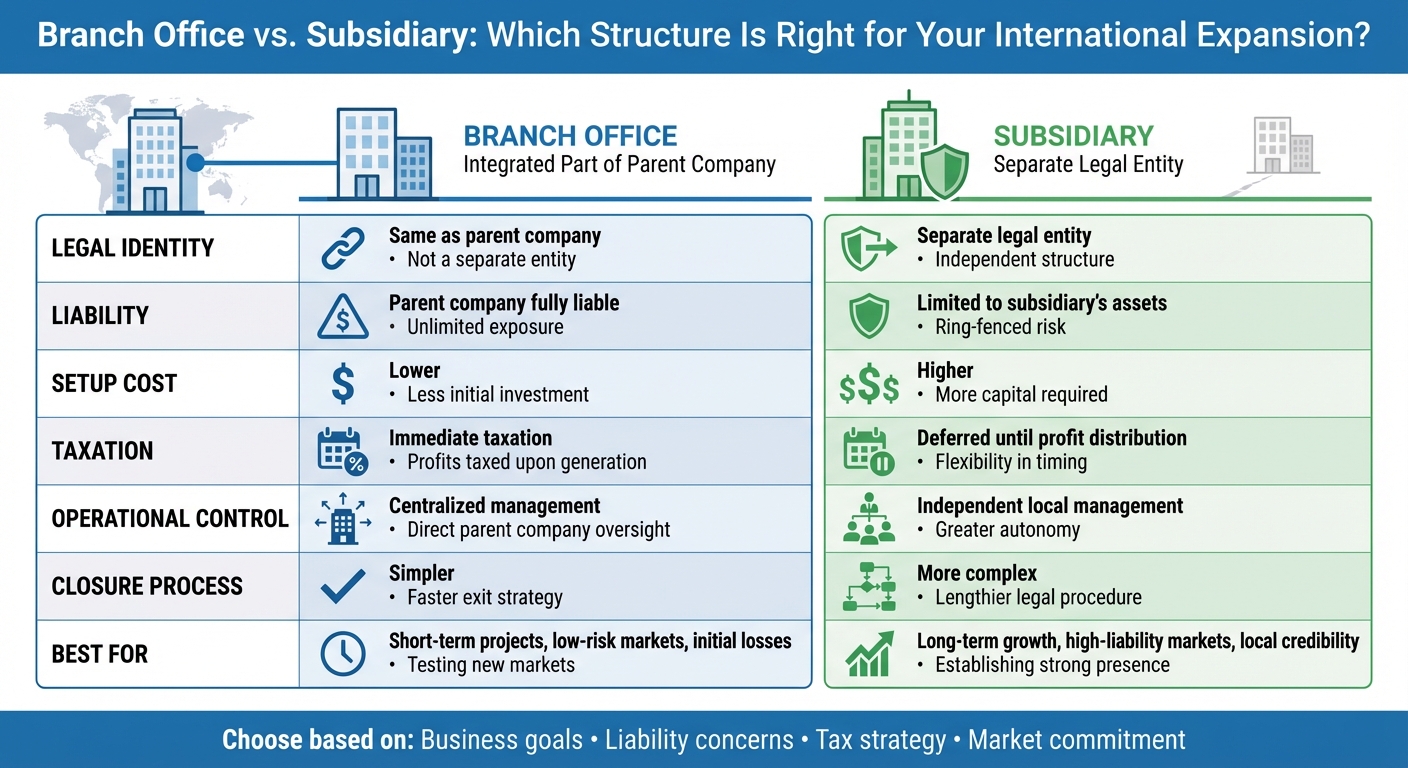

When expanding your business globally, your choice between a branch office and a subsidiary can impact taxes, liability, and operational flexibility. Here’s a quick breakdown:

- Branch Office: An extension of your parent company. Easier to set up, but the parent company is fully liable for debts and legal issues. Profits are taxed immediately.

- Subsidiary: A separate legal entity. Offers liability protection and local credibility but involves higher setup and compliance costs. Profits are taxed only when distributed as dividends.

Key Factors to Consider:

- Liability: Branches expose the parent company; subsidiaries limit risk.

- Taxes: Branches allow loss deductions; subsidiaries may offer tax deferral.

- Control: Branches are centrally managed; subsidiaries operate independently.

- Cost: Branches are cheaper to establish; subsidiaries require more investment.

Quick Comparison:

| Criteria | Branch Office | Subsidiary |

|---|---|---|

| Legal Identity | Same as parent company | Separate legal entity |

| Liability | Parent company fully liable | Limited to subsidiary’s assets |

| Setup Cost | Lower | Higher |

| Taxation | Immediate | Deferred until profit distribution |

| Operational Control | Centralized | Independent |

| Closure Process | Simpler | More complex |

Choose a branch for short-term or low-risk projects. Opt for a subsidiary for long-term growth or high-liability markets. Your decision should align with your business goals, liability concerns, and tax strategy.

Branch Office vs. Subsidiary: Core Differences

The key difference lies in legal identity. A subsidiary operates as an independent legal entity, incorporated under the host country’s laws. In contrast, a branch is an extension of the parent company and typically doesn’t have a separate legal identity in most jurisdictions.

This distinction impacts nearly every aspect of operations. Branches usually carry the same name as the parent company, while subsidiaries can adopt a local name that better suits the market. When it comes to contracts, branches often rely on the parent company to sign agreements, whereas subsidiaries can enter into contracts on their own, offering more operational independence.

"A branch is an unincorporated, direct extension of a parent company that operates business activities on behalf of the parent to the extent the business purposes of the parent permit." – Samuel Pollack and Naoko Watanabe, Associates, Baker McKenzie

Governance is another area where the two structures diverge. Branches are managed directly by the parent company’s headquarters, which allows for centralized control but limits local decision-making. Subsidiaries, on the other hand, have their own management team and board of directors, although the parent company typically retains strategic control through ownership. Transferring a branch involves deregistration and re-registration, while a subsidiary can be transferred through share or stock transactions.

These operational differences are rooted in their distinct legal setups.

Legal Structure and Entity Status

The legal structure defines how the foreign operation connects to the parent company and interacts with local regulations. A branch office is essentially your parent company doing business in another country under the same corporate identity. It doesn’t have its own legal personality, meaning all contracts, liabilities, and legal matters are directly tied to the parent company.

A subsidiary, however, is a separate legal entity with its own assets, liabilities, and corporate identity. It files its own taxes, maintains independent financial records, and operates under the laws of the host country. While the parent company controls the subsidiary through ownership, the subsidiary is legally distinct.

There is an exception to this general rule: in Brazil, branches are recognized as having a separate legal personality, which allows them to enter contracts independently. However, in most countries, branches remain legally inseparable from their parent companies.

Liability and Risk Exposure

Liability is a critical factor when deciding between a branch and a subsidiary. With a branch office, the parent company is fully liable for the branch’s debts, legal claims, and other obligations. If the branch incurs debt, faces a lawsuit, or violates regulations, creditors can pursue the parent company’s assets, regardless of where they are located.

"A permanent branch is a fixed site in a foreign country where you fully or partly carry out your business’s operations. It is not a separate legal entity, which means debts and fines incurred and legal claims or other liabilities brought against the foreign branch extend to the company here in the U.S." – Steven Gallant and Larry Andler, Partners, LGA

Subsidiaries, on the other hand, limit liability to the entity itself. The parent company’s exposure is generally restricted to its investment in the subsidiary. This means that if the subsidiary encounters financial or legal trouble, the parent company’s other assets are typically shielded. This structure is especially advantageous in markets with a high risk of litigation, such as the United States, or in industries prone to liability.

"The primary benefits of forming a separate legal entity include limiting liability arising through US operations at the US subsidiary level (or at least making it more difficult for liabilities to rise to the parent level)…" – Kaoru C. Suzuki, Larry P. Naughton, and Joshua D. Fox, Attorneys, Mintz

That said, liability protection isn’t foolproof. Courts can "pierce the corporate veil" if corporate formalities aren’t followed or if the subsidiary is merely a shell. However, when properly structured, a subsidiary offers far more protection against risk than a branch.

Up next, we’ll explore the financial implications of these two structures.

sbb-itb-ba0a4be

Tax and Financial Considerations

A branch’s income is taxed in the U.S. as it is earned, while a subsidiary’s profits are taxed in the U.S. only when dividends are distributed. However, anti-avoidance rules like Subpart F and Global Intangible Low-Taxed Income (GILTI) can lead to taxation even if no dividends are distributed.

This difference in timing has a big impact on cash flow. For branches, funds can be accessed easily through accounting entries or notices. In contrast, subsidiaries require board approval and must comply with local reserve rules before declaring dividends. Asset transfers between a branch and its parent company are tax-neutral, but transactions involving subsidiaries must adhere to detailed transfer pricing rules, which require "arm’s-length" pricing for goods, services, and loans.

Tax Filing and Reporting Requirements

Branches report their income as part of the parent company’s tax return, with the Foreign Tax Credit (FTC) helping to offset double taxation. Subsidiaries, on the other hand, file separate tax returns, including Form 5471, and may face local withholding taxes on dividend distributions. Additionally, subsidiaries must maintain annual transfer pricing documentation, with compliance thresholds varying by country – for example, approximately $123,000 in India versus around $720,000 in Mexico.

"Even if a U.S. parent company wholly owns a foreign subsidiary, the profits are not subject to U.S taxation until the subsidiary distributes the dividend to the U.S. corporation." – Steven Gallant and Larry Andler, Partners, LGA

One notable benefit of subsidiaries is the potential for a 100% deduction on dividends received by a U.S. corporation that owns more than 10% of the foreign entity. However, this deduction is subject to limitations imposed by GILTI and other rules. For branches owned by U.S. C Corporations, the Foreign-Derived Intangible Income (FDII) deduction introduced under the 2017 Tax Cuts & Jobs Act may apply. Furthermore, operating as a branch can help avoid the Base Erosion Anti-Abuse Tax (BEAT), which might be triggered by payments made to foreign subsidiaries.

These tax differences highlight the financial and operational incentives tied to each structure.

Cost Efficiency and Tax Incentives

Branches can offset a parent company’s taxable income during periods of early losses, while subsidiaries may offer tax deferral and access to local incentives once they become profitable.

"A U.S. corporation is better served operating its foreign business through a branch for the period that the foreign business generates net deductions and operating through a foreign corporation for the period that the foreign business generates net income." – Samuel Pollack and Naoko Watanabe, Associates, Baker McKenzie

In some cases, branches may face additional costs, such as branch profits taxes, which can make them less cost-effective than subsidiaries over time. Tax treaties also play a critical role. For example, countries with low dividend withholding rates might make subsidiaries more appealing, while strong FTC provisions could favor branches. In Germany, if a parent corporation owns at least 10% of a subsidiary, only 5% of the dividend distribution is taxable under Section 8b of the German Corporate Tax Act.

Next, we’ll look at how these structures affect operational control and management.

Operational Control and Management

A branch office operates under the direct oversight of its headquarters, while a subsidiary is led by independent local management. This difference allows subsidiaries to make faster decisions and adapt more effectively to local market conditions.

Governance and Decision-Making Authority

Branch offices follow a centralized control model, which works well when maintaining uniform global policies is a priority. In this setup, major decisions are made by the parent company, and the branch carries them out. However, this structure can slow things down when local teams need to act quickly in response to market demands.

Subsidiaries, on the other hand, operate autonomously. As separate legal entities, they manage their own boards of directors and maintain independent financial records. For instance, the UK-based fintech company Revolut set up a subsidiary in Lithuania to obtain a banking license and comply with local regulations – something a branch office would not have been able to achieve.

"Local managers [in a subsidiary] have the power to make more decisions, reducing the bottlenecks that arise from long approval chains." – Jemima Owen-Jones, Author, Deel

Unlike a branch office, which cannot independently sign legal agreements, a subsidiary can enter contracts and form partnerships on its own. This ability is particularly useful when bidding for government contracts or working with local suppliers who prefer dealing with domestic entities.

These differences in decision-making authority also influence staffing and compliance responsibilities.

Employee Hiring and Sponsorship

Subsidiaries act as the legal employer in the host country, managing payroll, benefits, and compliance with local labor laws. In contrast, branch offices hire employees under the parent company’s name, which assumes full liability for employment-related matters.

Visa sponsorship is another key distinction. In the United States and many other countries, subsidiaries – recognized as local entities – can sponsor work visas for foreign employees. Branch offices, however, are typically ineligible for such sponsorships because they are not considered independent domestic companies.

Local regulations also play a crucial role in staffing decisions. For example, Singapore often requires at least one director, manager, or partner to be a permanent resident. Similarly, in the UAE, some subsidiary structures mandate a local partner to hold a 51% ownership stake. These regulatory nuances can significantly influence whether a branch office or a subsidiary is the better choice for your international expansion strategy.

Setup and Maintenance Costs

When planning for international expansion, it’s essential to consider the costs tied to setup, maintenance, and eventual exit. These expenses often go well beyond the initial registration phase.

Initial Setup Costs

Establishing a branch office is usually less expensive than creating a subsidiary because it doesn’t involve forming a new corporate entity. You can skip steps like drafting incorporation documents, forming a board of directors, or negotiating ownership structures. But don’t assume branches are always the easier route.

For instance, in the United Kingdom, registering a branch requires submitting certified copies of the parent company’s documents, often with English translations. This adds translation and certification fees to the process.

"It is a common misconception that branches are easier to establish. It may be just as cumbersome as opening a subsidiary, and may require extensive disclosure of the parent entity information."

– Samuel Pollack and Naoko Watanabe, Associates, Baker McKenzie

Subsidiaries, on the other hand, come with higher upfront costs since they are fully independent legal entities. Costs include incorporation filings, drafting corporate bylaws, and setting up a management structure. In some countries, subsidiaries face additional hurdles like minimum capital requirements. For example, in the UAE, certain business activities require a local partner to hold 51% ownership in a subsidiary, increasing both legal and financial complexities.

Timing also varies between branches and subsidiaries. In Japan, setting up a branch can take about one month, while a subsidiary may require two months. In the U.S., both structures need an Employer Identification Number (EIN) and state-level registration, but the process differs – branches use Foreign Qualification, while subsidiaries go through incorporation.

These initial cost differences are tied to broader issues like liability and operational control.

Ongoing Compliance and Administrative Costs

Maintaining a branch is generally less costly since it operates as an extension of the parent company. Ongoing expenses typically include payroll, rent, and other operational costs, while the parent company’s existing governance structures remain in place.

Subsidiaries, however, require more formal governance, which increases administrative expenses. They must establish a separate board of directors, hold regular meetings, keep detailed minutes, and maintain independent bylaws. Financial reporting is more demanding, as subsidiaries require separate audits and distinct financial records.

Tax compliance adds another layer of complexity. For example, U.S. branches of foreign corporations must file Form 1120-F annually and pay a 30% branch profits tax on earnings not reinvested in the U.S., though tax treaties may lower this rate. Subsidiaries face more intricate reporting requirements, including compliance with Subpart F and GILTI rules.

Both branches and subsidiaries are responsible for federal payroll taxes like Social Security, Medicare, and FUTA, as outlined by the IRS. Payroll administration costs can add roughly 30% to your budget, and late deposits may result in escalating penalties.

Transferring assets also differs. Branches can do this through simple accounting entries, while subsidiaries must follow formal procedures like board approvals and legal thresholds.

Exit Costs and Closure Process

Closing a branch is usually simpler and less costly than shutting down a subsidiary. Since branches aren’t separate legal entities, the process mainly involves deregistration in the local jurisdiction. Asset repatriation is straightforward, often handled through basic accounting entries.

"Permanent branches are generally simpler to close down. There are more legal and financial negotiations involved in closing a subsidiary as well."

– Steven Gallant, CPA, and Larry Andler, CPA, LGA

Subsidiaries, being independent legal entities, face a more complex closure process. This includes formal board approval, written shareholder consent, and registering these actions with local regulators. Before distributing assets to the parent company, the subsidiary must meet specific financial thresholds and demonstrate sufficient distributable reserves.

Another key distinction lies in transferability. Branches cannot be transferred to a new owner; instead, the parent company must deregister, and the new owner must go through the registration process from scratch. Subsidiaries, however, can be sold or transferred as standalone entities, offering more flexibility if exiting through a sale rather than closure.

Matching Structure to Business Goals

Choosing between a branch or a subsidiary depends largely on how your business goals align with the legal, tax, and operational differences of each structure. Let’s break it down based on specific objectives.

Short-Term Market Entry

If you’re testing the waters in a new market or working on a short-term project, a branch is often the easier and more cost-effective option. Since it operates under your existing legal entity, setting up is quicker and less expensive. Plus, if your foreign operations initially incur losses, a branch allows those losses to flow through to your U.S. tax return, offering immediate tax relief.

"A U.S. corporation is better served operating its foreign business through a branch for the period that the foreign business generates net deductions and operating through a foreign corporation for the period that the foreign business generates net income." – Samuel Pollack and Naoko Watanabe, Associates, Baker McKenzie

If the market test doesn’t pan out, winding down a branch is far simpler than closing a subsidiary, sparing you the complexities of deregistration and other closure processes.

Long-Term Market Development

For businesses aiming to establish a lasting presence, a subsidiary is the better choice. A subsidiary demonstrates your commitment to the local market, which can build trust with customers, banks, and partners. It also offers greater operational flexibility – you can issue stocks or bonds, transfer shares to local employees, and explore other business opportunities within the region.

Take the United Kingdom, for instance. You can incorporate a subsidiary in about 24 hours, but opening a business bank account may take up to three months. While the initial costs of setting up a subsidiary are higher than those of a branch, the stability and credibility it provides are invaluable for long-term growth.

Risk Mitigation and Liability Protection

If reducing liability is a priority, a subsidiary is the safer bet. As a separate legal entity, it isolates debts, lawsuits, and operational risks, protecting the parent company from direct exposure.

"A subsidiary is a separate legal entity… providing a layer of liability protection for the parent company. This shields the parent company from direct risks associated with the subsidiary’s operations." – Shane George, Co-Founder, GEOS

Branches, on the other hand, don’t offer this protection. Since they are extensions of the parent company, any legal claims, fines, or debts fall directly on the parent. This lack of separation can be especially risky in highly regulated industries or volatile markets. By aligning your business structure with your goals, you can balance risk management with market agility effectively.

How to Decide: A Step-by-Step Framework

After reviewing the legal, financial, and operational differences, you can use this framework to decide which structure best suits your international expansion goals. These targeted questions will help you evaluate your needs and make an informed choice.

Key Questions

Consider these important questions to align your expansion structure with your objectives:

Will you incur initial operating losses?

If the answer is yes, setting up a branch could be beneficial. Losses from a branch can offset your domestic taxable income, offering potential tax advantages.

Is liability protection for the parent company a priority?

In markets like the U.S., where lawsuits are common, or in high-risk industries like manufacturing, a subsidiary can protect your parent company’s assets from foreign liabilities, such as debts or legal claims.

Will you need to recruit a large local workforce and provide competitive benefits?

Subsidiaries often simplify hiring and managing benefits for local employees, avoiding the extra administrative challenges that branches might face.

Does the local jurisdiction require majority local ownership for subsidiaries?

Some regions, such as the UAE, mandate that a local partner holds 51% ownership in a subsidiary. If maintaining full control is crucial, a branch might be a better fit.

Are you planning to sell the regional business in the future?

Subsidiaries are typically easier to sell through share transfers, whereas closing a branch can involve more complicated de-registration processes.

Does your industry require a specific structure for licensing?

Certain regulated industries, like banking or insurance, may require a subsidiary to meet legal operating requirements.

Decision Tree for Structure Selection

Here’s a simplified approach to help you decide:

- Is liability protection critical?

- If yes, go with a subsidiary.

- If no, move to the next question.

- Will you incur initial operating losses that could offset domestic taxes?

- If yes, a branch might be more advantageous.

- If no, proceed to the next question.

- Do you need to hire a large local team and offer comprehensive benefits?

- If yes, a subsidiary offers the operational flexibility you’ll need.

- If no, a branch might suffice for smaller-scale operations.

This framework helps you align your business structure with your goals, considering factors like risk, tax strategies, operational needs, and future plans. Remember, the best choice isn’t about following what worked for another company – it’s about what fits your unique situation.

Conclusion

Deciding between a branch office and a subsidiary is a critical step in shaping your company’s international growth. Picking the wrong structure could lead to unexpected liabilities, tax challenges, or administrative hurdles that might slow your progress.

Here’s the trade-off: Branch offices are quicker and cheaper to set up but leave your parent company more exposed to risks. On the other hand, subsidiaries provide liability protection and enhance local credibility, though they come with higher costs and added complexity. This aligns with the detailed breakdown of legal, tax, and operational factors we discussed earlier.

When making your decision, take a holistic view. Think about your tax strategy, potential liabilities, regulatory demands, and how long you plan to operate in the market. Use the step-by-step framework outlined earlier to guide your choice. For businesses planning long-term operations, hiring extensively, or entering high-risk industries, a subsidiary often proves to be the better option.

FAQs

What are the tax differences between setting up a branch office and a subsidiary for international expansion?

When deciding between a branch office and a subsidiary, understanding the tax impact is crucial.

A branch office functions as an extension of the parent company, not a separate legal entity. This means its income is directly linked to the parent and taxed in the U.S. immediately. Additionally, profits sent back to the parent company may face a branch profits tax, which can increase the overall tax burden.

In contrast, a subsidiary operates as its own legal entity and is typically taxed independently of the parent company. This structure can provide more flexibility in tax planning and allow businesses to utilize local tax laws. However, it comes with added responsibilities, such as filing separate tax returns, and may involve higher compliance and operational costs.

Choosing between these options requires careful consideration of factors like tax efficiency, legal liability, compliance obligations, and your business’s long-term objectives.

What are the liability and risk differences between a branch office and a subsidiary when expanding internationally?

When entering international markets, deciding between a branch office and a subsidiary can heavily influence your company’s exposure to liability and risk.

A branch office operates as an extension of the parent company. This means the parent company is fully responsible for the branch’s debts, legal obligations, and other risks. Essentially, any issues or liabilities faced by the branch directly impact the parent company, increasing financial and legal exposure.

In contrast, a subsidiary is a separate legal entity. This distinction helps shield the parent company from the subsidiary’s liabilities. If the subsidiary accrues debts or encounters legal problems, these remain confined to the subsidiary itself, offering the parent company a layer of protection. This structure is often favored in regions where the legal or economic climate is less predictable.

The choice between the two largely hinges on your company’s risk appetite, the legal framework of the target market, and your broader business objectives.

What should I consider when choosing between a branch office and a subsidiary for international business expansion?

When expanding internationally, choosing between a branch office and a subsidiary depends on several key factors: legal structure, liability, tax considerations, operational control, and ease of setup.

A branch office operates as an extension of the parent company, making it simpler to manage. However, this simplicity comes with a trade-off – greater liability for the parent company. On the other hand, a subsidiary is a separate legal entity. This setup provides liability protection and can offer tax advantages, but it involves a more intricate setup process.

Taxes play a major role in this decision. Subsidiaries often benefit from independent tax regimes and can raise their own funding. In contrast, branches are typically taxed as part of the parent company, which might limit flexibility. Another consideration is operational independence. Branch offices remain tightly controlled by the parent company, while subsidiaries have more autonomy, which can make it easier to comply with local regulations and adapt to market conditions.

The decision ultimately hinges on your business objectives, how much risk you’re willing to take, and the regulatory environment in the country you’re targeting.