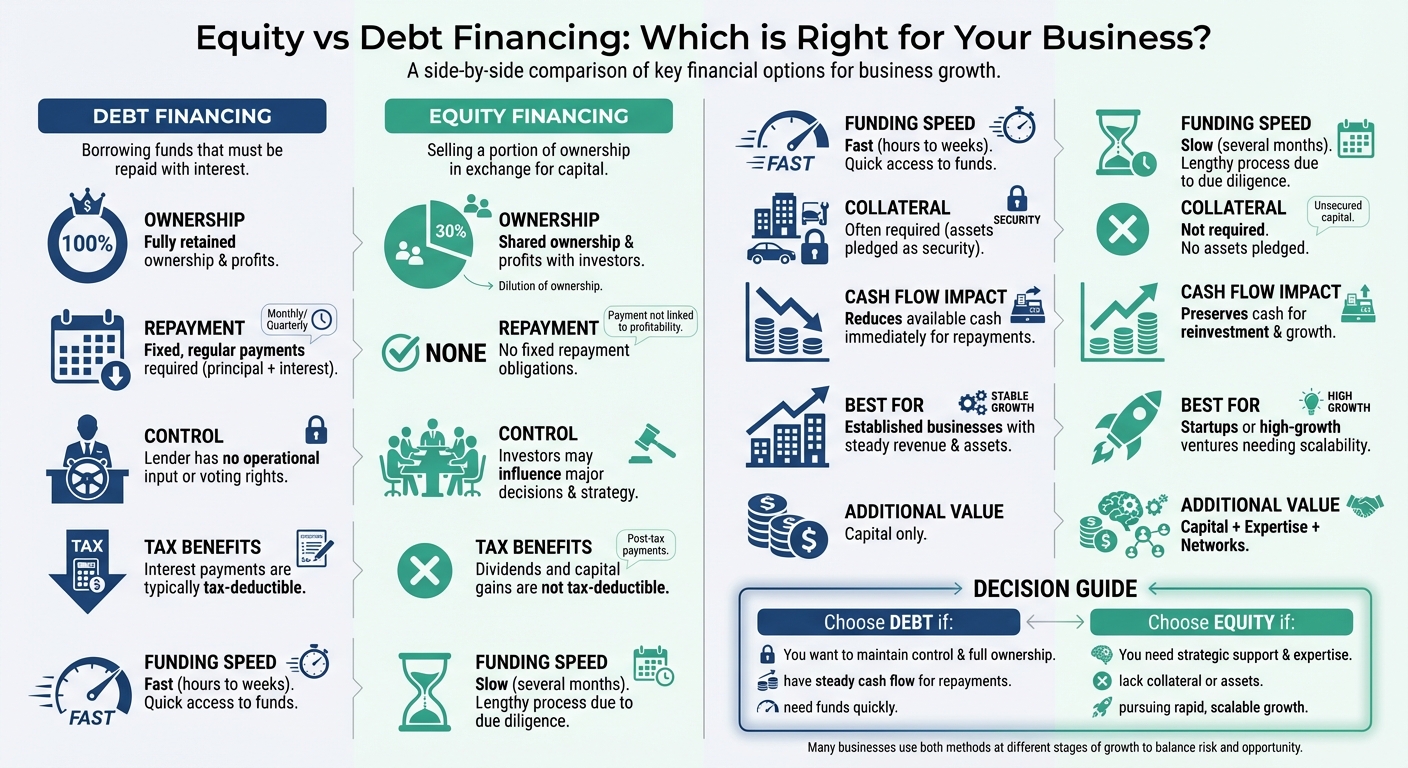

When deciding how to fund your business, the choice often comes down to equity financing (selling ownership for capital) or debt financing (borrowing money to repay with interest). Each option has trade-offs that affect ownership, control, cash flow, and growth potential.

- Debt Financing: You keep full ownership and control but must make regular repayments, even in tough times. Interest payments are tax-deductible, but you may need collateral.

- Equity Financing: No repayments are required, and investors may bring expertise and connections. However, you give up a share of ownership and some decision-making power.

Key Factors to Consider:

- Control: Debt keeps you in charge; equity means sharing decisions.

- Cash Flow: Debt requires fixed payments; equity frees up cash but shares profits.

- Tax Impact: Debt offers interest deductions; equity does not.

- Business Stage: Debt suits stable businesses; equity fits startups or high-growth ventures.

- Speed: Debt is faster to secure; equity takes longer but may offer more than just funding.

| Feature | Debt Financing | Equity Financing |

|---|---|---|

| Ownership | Fully retained | Shared with investors |

| Repayment | Fixed payments required | No repayment obligations |

| Tax Benefits | Interest is tax-deductible | Dividends are not tax-deductible |

| Funding Speed | Fast (hours to weeks) | Slow (months) |

| Best For | Established businesses | Startups or high-growth ventures |

Takeaway: Debt works for businesses with steady cash flow and a desire to retain control. Equity is better for businesses needing significant capital and strategic support. Many businesses use both approaches at different stages.

Equity vs Debt Financing Comparison Chart for Small Businesses

Equity Financing vs Debt Financing: The Basics

Before diving into the pros and cons, it’s essential to grasp what these two funding approaches entail and how they differ. Let’s break them down to see how they impact businesses in distinct ways.

What is Debt Financing?

Debt financing involves borrowing money that you’re required to repay on a set schedule, typically with interest. Think of options like small business loans or credit lines. The standout feature? You keep 100% ownership of your business. The lender has no say in how you operate, but there’s a catch: if you fail to meet repayment terms, they could claim collateral or pursue legal action.

What is Equity Financing?

Equity financing, on the other hand, means selling a stake in your business in exchange for funding. Instead of taking on debt, you offer shares to investors like venture capitalists, angel investors, or even close connections. The upside? No mandatory repayments. The downside? You’re giving up a slice of your company – and possibly some influence over key decisions.

A great example of equity financing in action is Trade Republic, a fintech company based in Berlin. In May 2021, they raised $900 million in a Series C round led by Sequoia Capital and TCV, reaching a valuation of $5.3 billion. This funding allowed them to expand rapidly across Europe – growth that would’ve been hard to achieve with traditional debt financing.

Now that we’ve covered the basics, let’s explore the key differences that shape ownership, repayment, and tax considerations.

Main Differences Between Equity and Debt

The primary distinction lies in ownership versus obligation. Debt financing allows you to keep full control of your business but requires regular repayments, regardless of how well your business is performing. Equity financing, on the other hand, trades some ownership – and potentially decision-making power – for funding without the burden of repayment schedules.

Tax treatment is another factor. Interest payments on debt can reduce your taxable income, making loans more cost-effective. Dividends paid to equity investors, however, come out of after-tax profits, offering no such benefit.

For instance, Dutch hosting company Cloud86 opted for debt financing, securing €1.2 million from re:cap to fund marketing and customer acquisition. This decision ensured they maintained complete control and avoided diluting ownership. It’s a clear example of how debt can help businesses grow while preserving autonomy.

| Feature | Debt Financing | Equity Financing |

|---|---|---|

| Ownership | Fully retained | Shared with investors |

| Repayment | Fixed payments required | No repayment obligations |

| Control | Lender has no operational input | Investors may influence decisions |

| Tax Impact | Interest is tax-deductible | Dividends are not tax-deductible |

| Collateral | Often required | Not required |

Understanding these distinctions is crucial for determining which funding route aligns best with your business’s goals, cash flow, and growth trajectory.

sbb-itb-ba0a4be

How Each Method Affects Ownership and Control

Choosing how to fund your business isn’t just about money – it’s about deciding how much control you’re willing to give up. The path you choose shapes your financial structure and who gets to make the big decisions: you or your investors.

Debt Financing Keeps You in Charge

Debt financing lets you keep full ownership of your business. The lender doesn’t take a stake in your company or a slice of your profits. Their only concern is getting their money back with interest. As Investopedia explains:

"The lender has no control over your business. Once you pay the loan back, your relationship with the financier ends."

This means you can make decisions – like launching a new product or hiring key staff – without anyone else weighing in. Kelly Hillock from QuickBridge highlights this advantage:

"When you take debt financing over equity, you stay in control of the decisions and can keep decision-making processes shorter and less complicated."

Take Cloud86 as an example: they used debt financing to grow while holding onto full ownership. But it’s worth noting that some loans come with strings attached, like covenants that can restrict how you spend or limit additional borrowing.

Equity financing, however, comes with a different set of trade-offs.

Equity Financing Means Sharing the Power

With equity financing, you’re selling a piece of your company in exchange for funding. This means you’re not just gaining capital – you’re also gaining partners. Those investors may want a say in how the business is run, often through decision-making rights or board seats.

Unlike debt, which you can pay off and move on from, equity investors stick around. They remain part-owners unless you buy them out. And if things go south, they might get more involved to protect their investment.

High-growth startups often go this route, even if it means giving up some control. As Entrepreneur warns:

"You’ll have to consult with investors, and you might disagree over the direction of your company. You might even be forced to cash out and abandon your own business."

Deciding What Matters Most

The choice between debt and equity comes down to your priorities: how much control do you want to keep, and what kind of support does your business need?

Debt financing is ideal if maintaining autonomy is your top concern. This is especially true for family-run businesses, local operations, or companies where the founder’s vision is non-negotiable. If your cash flow is steady and you can handle regular payments, debt lets you grow without giving up control.

Equity financing, on the other hand, offers more than just money. It’s often a better fit for startups aiming for rapid growth, as investors can bring industry connections, strategic advice, and credibility. A good example is heycater!, a Berlin-based company. They initially raised venture capital to develop their product but later switched to debt funding from re:cap to scale up without further diluting ownership.

Before making a decision, consider these questions: Can you live with consulting partners on major decisions? Are you okay with sharing future profits? Do you value strategic mentorship, or is cash alone enough? Your answers will guide you to the right choice.

Financial Impact: Cash Flow, Repayments, and Taxes

Your choice of financing doesn’t just influence ownership and control – it also has a direct impact on your monthly budget, cash flow, and tax obligations. Getting a clear picture of these financial effects is crucial for planning ahead.

Debt Financing Requires Regular Payments

Debt financing comes with fixed monthly payments that include both principal and interest, no matter how well or poorly your business performs. These payments usually start as soon as the loan is disbursed, which can tighten your cash flow. For instance, even if your revenue drops by 30% during a slow period, the monthly payment remains unchanged, potentially putting strain on your operations. This is why it’s important to stress-test your budget to ensure you can handle repayments, even during downturns. Debt is best suited for investments that promise clear and immediate returns, like purchasing equipment to increase production, rather than speculative projects.

On the other hand, equity financing doesn’t come with this kind of repayment pressure.

Equity Financing Has No Repayment Schedule

Equity financing operates differently: there’s no monthly repayment to worry about. This flexibility in cash flow allows you to reinvest in your business, hire new staff, or weather slower periods without the added stress of meeting fixed payments. However, the trade-off is that you’ll need to share future profits with your investors once your business becomes profitable.

Tax Differences Between the Two Methods

One advantage of debt financing lies in its tax benefits: the interest you pay on loans is tax-deductible, effectively lowering the cost of borrowing. As explained by FindLaw:

"Interest on the debt can be deducted on the company’s tax return, lowering the actual cost of the loan to the company."

This tax deduction can make debt financing more cost-effective compared to equity financing, where profit distributions to investors come out of after-tax earnings and offer no tax relief.

To maximize these benefits, consult an accounting professional to see how interest deductions align with your broader tax strategy. Also, if you’re carrying debt, keeping an eye on interest rates and refinancing when they drop can help reduce your monthly payments and improve your financial flexibility.

| Financial Aspect | Debt Financing | Equity Financing |

|---|---|---|

| Repayment Schedule | Fixed monthly installments (principal + interest) | No fixed repayment schedule |

| Cash Flow Impact | Reduces available cash immediately and over time | Preserves cash for reinvestment and growth |

| Tax Impact | Interest payments are tax-deductible | Dividends/profits are paid after-tax |

| Profit Retention | Owner keeps 100% of profits after debt is repaid | Profits are shared with investors |

| Downturn Risk | High; payments required even during revenue dips | Lower; no mandatory payments during losses |

Getting Funded: Speed and Requirements

When deciding between debt and equity financing, the time it takes to access funds and the qualifications required can make all the difference. These factors often determine which option aligns best with your business stage and immediate needs.

Debt Financing: Quick Access, Collateral Often Required

Debt financing is known for its speed. Online lenders can process and approve loans in mere hours, while traditional banks may take a few days to weeks. According to one expert:

"If you need cash as soon as possible, then debt financing is the way to go. You can get business loans incredibly fast – in a matter of hours even, if you apply to the right lenders." – Entrepreneur

However, speed comes with specific conditions. Most lenders require at least two years of financial history and a minimum credit score of 550. Additionally, you’ll need to show consistent cash flow and often provide collateral or a personal guarantee. For established businesses, this can be a practical route, as they can leverage their assets and revenue while retaining full ownership. These requirements make debt financing more suitable for businesses with a proven track record.

Equity Financing: Slower Process, Fewer Barriers

Equity financing, on the other hand, is a longer journey. It often takes months to move from the initial pitch to receiving funds. This process involves presenting your business plan, negotiating terms, and undergoing thorough due diligence – a common scenario for fintech startups.

The advantage of equity financing lies in its focus on your business’s future potential rather than its current financial standing. You don’t need collateral, a spotless credit score, or years of financial data. Emily Heaslip from the U.S. Chamber of Commerce explains:

"Equity financing may be necessary if you can’t qualify for a startup business loan and want to avoid more expensive options like credit cards." – Emily Heaslip, U.S. Chamber of Commerce

This makes equity financing particularly appealing to pre-revenue startups with strong growth projections. For these businesses, the lack of immediate revenue or assets is less of a hurdle, as investors are more interested in the vision and potential for future success.

Matching Financing to Your Business Stage

Your business’s maturity level plays a key role in choosing the right funding path. Established companies with steady revenue and tangible assets are well-positioned for debt financing. This option offers fast access to capital for needs like purchasing equipment, managing seasonal inventory, or handling unexpected expenses – all without giving up ownership.

For early-stage startups without predictable revenue or significant assets, equity financing might be the only realistic choice. Investors are often willing to take a chance on a promising idea and growth potential rather than focusing on past financials. For example, the catering platform heycater! combined both approaches: initially raising venture capital to develop its product and enter the market, and later using debt financing from re:cap to scale operations without further diluting ownership. This example highlights how funding speed and requirements shape growth strategies.

| Feature | Debt Financing | Equity Financing |

|---|---|---|

| Funding Speed | Fast (hours to weeks) | Slow (several months) |

| Credit Requirements | Strong credit score and 2+ years of financials | Focus on growth potential; credit history not required |

| Collateral Needed | Often required (assets or personal guarantee) | Not required |

| Best Business Stage | Established with predictable cash flow | Early-stage or high-growth ventures |

While speed and requirements are crucial, equity financing often comes with additional benefits beyond just the funding itself.

What Equity Investors Bring Beyond Capital

Equity investors do more than just write checks. They become partners in your journey, sharing your ambition because their success depends on your business thriving. This alignment of goals can make them invaluable contributors to your growth.

While funding is a big part of what they bring, equity investors also provide strategic advantages.

Investors Offer Experience and Guidance

Equity investors often come with a wealth of industry knowledge. Many have built and scaled businesses themselves, meaning they’ve already tackled challenges that might lie ahead for you. Their insights can prove invaluable in areas like product development, market positioning, and assembling a strong team.

Joe DiSanto, Fractional CFO and Founder of Play Louder, puts it this way:

"These partners may contribute not only financial resources but also their network, expertise and vested interest in the success of your business." – Joe DiSanto, Fractional CFO and Founder, Play Louder

Many investors take active roles in the companies they back, such as joining the board or participating in strategic planning. This hands-on involvement gives you access to seasoned advisors who can help you navigate challenges as they arise. As PNC Insights points out, equity investors often stay engaged with businesses for years, offering continued support as the company grows.

Access to Networks and Business Connections

One of the biggest perks of equity investors is their ability to open doors. Through their networks, they can connect you with potential customers, suppliers, and strategic partners. They’re also instrumental in recruiting top talent and facilitating partnerships that drive growth. In some cases, they can even help you handle regulatory hurdles.

"With the right investors, you can get great experience, wisdom, industry connections and much more." – Entrepreneur

To put this into perspective, in 2015, venture capital investments in the United States totaled nearly $60 billion. While the capital was essential, the strategic support and connections that accompanied it were often just as critical.

Debt Financing Provides Capital Only

Debt financing takes a very different approach. Lenders are focused solely on being repaid, with interest. They don’t offer advice, connections, or help with decision-making.

This transactional nature can be appealing if you want to maintain complete control and keep all future profits. But it also means you’re on your own when it comes to solving problems, finding customers, or navigating market shifts. You get the funds you need, but that’s where the relationship ends.

| Feature | Debt Financing | Equity Financing |

|---|---|---|

| Primary Offering | Capital only | Capital + expertise + networks |

| Relationship Type | Transactional (ends after repayment) | Long-term partnership |

| Strategic Support | None | Mentorship and guidance |

| Network Access | Not provided | Introductions to customers, partners, talent |

| Involvement | No say in operations | May take board seat or advisory role |

Ultimately, the choice between debt and equity financing depends on what your business needs most – just the money, or the money plus the expertise and connections to make it work harder for you.

How to Choose the Right Financing Method

Deciding between equity and debt financing is all about identifying what aligns best with your business’s current situation and future goals. The choice depends on where your business stands today, where you want to take it, and what you’re prepared to exchange to get there.

Questions to Ask Before Deciding

To make an informed choice, consider these five key factors:

- How quickly do you need the funds? Debt financing, like business loans, can often be arranged within days, while equity financing usually requires months of pitching and legal processes.

- What does your cash flow look like? If your revenue is steady and predictable, managing regular loan payments might be straightforward. But if your income is seasonal or uncertain, debt repayments could become a strain.

- Are you willing to give up ownership or control? Debt financing allows you to retain full ownership, while equity financing means sharing a portion of your business – and possibly a seat at the decision-making table.

- Do you need more than just money? Equity investors often bring valuable industry connections, mentorship, and strategic advice, something lenders typically don’t offer.

- What’s your ultimate growth vision? If you aim to scale aggressively or expand globally, equity financing might be the only way to secure the large sums of capital required.

Before committing to any financing option, stress-test your financial plan. For example, ask yourself: if your revenue dropped by 30%, could you still meet your obligations? As re:cap cautions:

"The trap isn’t taking debt. The trap is taking debt on shaky assumptions".

When Debt Financing Makes Sense

Debt financing is a solid choice when your business has predictable revenue, collateral to offer, and a clear plan to generate returns. It’s particularly effective for funding projects with measurable short-term ROI, such as purchasing equipment, stocking inventory, or scaling up an already successful marketing strategy.

Take Cloud86, for example. This Dutch company secured €1.2 million in debt funding to invest in customer acquisition and marketing. By focusing on ROI-driven growth, the founders retained full ownership and control of the business. Another advantage of debt is that interest payments are typically tax-deductible, which can lower the overall cost of borrowing.

Debt financing works best for entrepreneurs who want to maintain control, have the cash flow to meet repayment schedules, and don’t need strategic guidance beyond the capital itself.

When Equity Financing Makes Sense

Equity financing is ideal for businesses that are high-risk, pre-revenue, or aiming for rapid growth – especially if you lack collateral or a proven track record.

A good example is Trade Republic, which raised over $1.25 billion from investors like Sequoia Capital and Accel. This included a $900 million Series C round that valued the company at $5.3 billion. The founders traded some ownership for the capital and strategic support necessary to scale at a massive level.

For early-stage businesses, equity investors often provide $300,000 or more, sometimes in exchange for as much as 50% equity.

Many companies take a hybrid approach: they start with equity to fund product development, then shift to debt financing once revenue stabilizes. For instance, heycater! followed this strategy, using equity to build their foundation and later leveraging debt to scale profitably without further diluting ownership.

Conclusion

Choose the financing option that aligns best with your business goals and circumstances. Debt financing allows you to maintain ownership but requires fixed payments and may need collateral. On the other hand, equity financing eliminates repayment stress but involves giving up a share of ownership and potentially some decision-making power.

Your decision should reflect your financial position, growth plans, and willingness to make trade-offs. For businesses with steady cash flow and a desire to retain full control, debt financing might be the way to go. However, if you’re in a fast-growth phase, lack collateral, or could benefit from investor expertise, equity financing might make more sense.

Many successful businesses use a combination of both – starting with equity to establish a solid foundation, then leveraging debt later to scale without significant ownership dilution.

Before deciding, test your assumptions: Could your business handle debt payments if revenue dropped by 30%? Or, does giving up equity now set you up for greater gains down the road?

Your financing choice impacts control, growth, and the future of your business. Take the time to weigh your options carefully, as today’s decision will shape your path forward.

FAQs

How do I choose between debt and equity for my business?

Choosing between debt financing and equity financing comes down to your business’s financial health, growth ambitions, and comfort with risk. With debt financing, you borrow money while keeping 100% ownership of your company. The interest you pay is often tax-deductible, but this option comes with added financial pressure, especially if cash flow is tight. On the other hand, equity financing means selling shares of your business. This lowers your personal financial risk but also reduces your ownership stake. To make the right choice, weigh factors like your cash flow, the level of control you want to retain, and your long-term business goals.

What are the biggest red flags before taking on business debt?

Borrowing against future earnings can be risky, especially if it leads to over-leveraging – taking on more debt than you can realistically handle. This can make it tough to cover day-to-day expenses and meet repayment obligations. On top of that, high-interest rates and unfavorable loan terms can quickly escalate costs, while missed payments can damage your credit score. Add unpredictable cash flow into the mix, and repayment struggles could jeopardize your financial stability. It’s crucial to take a hard look at your ability to manage debt before moving forward.

How much equity should I give up to raise enough capital?

When deciding how much equity to part with, it all comes down to your funding requirements and the valuation you agree on with investors. The goal is to give up just enough equity to secure the capital you need while still keeping control and safeguarding your business’s ability to grow in the future.