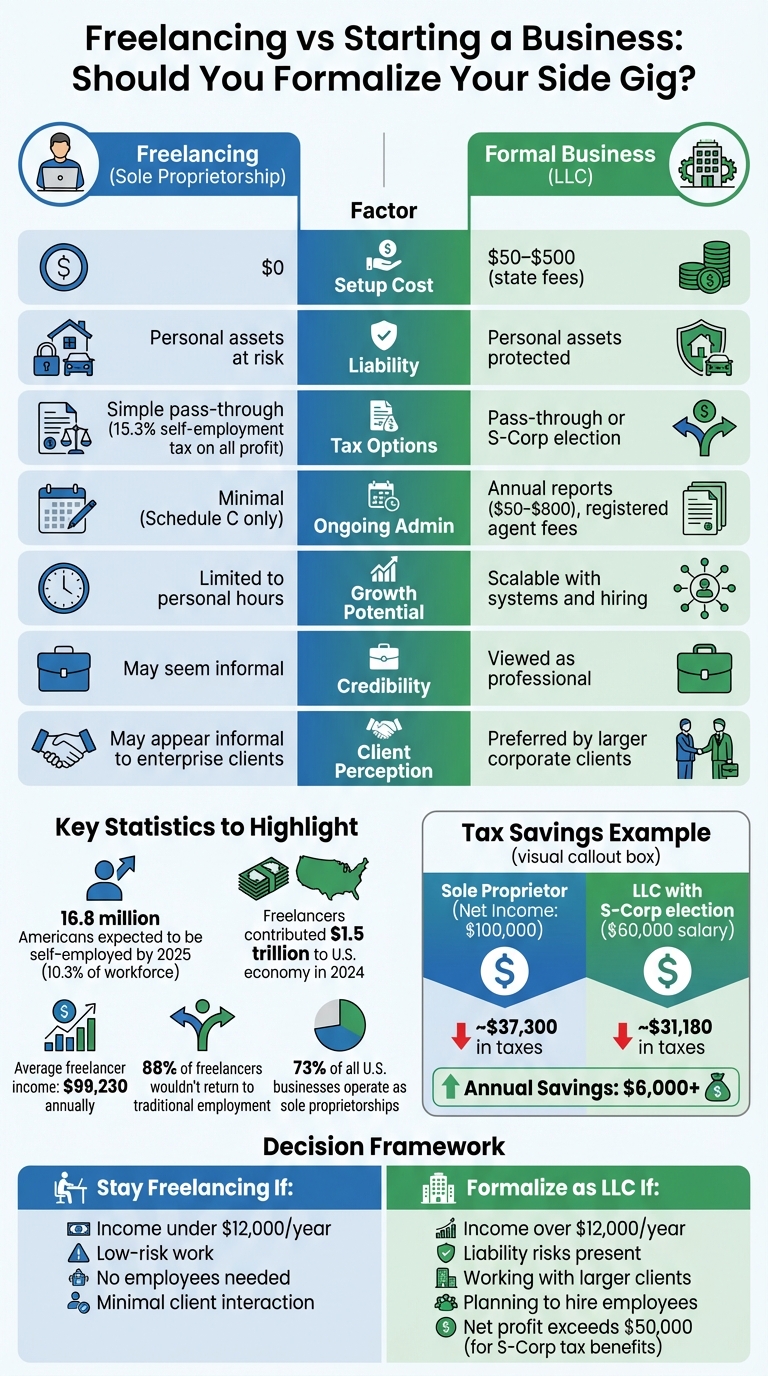

Should you stay a freelancer or register a formal business? The decision depends on your income, risk tolerance, and goals. Freelancing is simple, with no setup costs or paperwork, but leaves you personally liable for any business issues. On the other hand, formalizing as an LLC protects your personal assets, offers tax flexibility, and enhances your credibility – especially with larger clients.

Key Points:

- Freelancing: Easy to start, no upfront costs, but your personal assets are at risk if something goes wrong.

- LLC: Provides legal separation, asset protection, and tax advantages, but requires setup fees ($50–$500) and ongoing administrative tasks.

Quick Comparison:

| Factor | Freelancing (Sole Proprietorship) | Formal Business (LLC) |

|---|---|---|

| Setup Cost | $0 | $50–$500 (state fees) |

| Liability | Personal assets at risk | Personal assets protected |

| Tax Options | Simple pass-through | Pass-through or S-Corp |

| Growth Potential | Limited to personal hours | Scalable with systems |

| Credibility | May seem informal | Seen as more professional |

If your side hustle earns over $12,000 annually, involves liability risks, or you’re working with larger clients, formalizing as an LLC might be the right move. For low-risk, smaller-scale gigs, freelancing keeps things simple.

What Freelancing Looks Like

Defining Freelance Work

Freelancing is all about offering your skills on a project-by-project basis to various clients in exchange for payment. Essentially, you’re selling your expertise directly to those who need it.

When you begin freelancing, you’re operating as a sole proprietor. Legally, there’s no separation between you and your business – you’re one and the same. You don’t need to file any official paperwork or pay registration fees to get started. The moment you earn your first dollar from independent work, congratulations – you’re officially in business.

This simplicity makes freelancing incredibly accessible. As Stephen Fishman, CPA and author, puts it:

"The sole proprietorship exists precisely to lower the barrier to entry for independent work".

Why People Choose Freelancing

It doesn’t require startup costs. Unlike forming an LLC, which typically costs between $50 and $500 in state filing fees, freelancing lets you dive in with zero upfront expenses. You can start earning immediately without dealing with government approvals or legal complexities.

The statistics paint a clear picture. By 2025, 16.8 million Americans are expected to be self-employed, making up 10.3% of the workforce. Freelancers contributed a staggering $1.5 trillion to the U.S. economy in 2024, with an average annual income of $99,230. Even more striking, 88% of freelancers report they wouldn’t return to a traditional 9-to-5 job.

Why such loyalty to freelancing? Steve King, Partner at Emergent Research, explains:

"It really boils down to autonomy, control, and flexibility: the autonomy to work in the way they want to, control over what they do, and the flexibility to work when and where they want".

Freelancing also keeps tax filing straightforward. You report your income on a Schedule C attached to your personal tax return, using your Social Security number instead of a business tax ID. No need to worry about corporate formalities, annual reports, or operating agreements.

However, this informal structure comes with its own set of challenges.

Downsides of Staying Informal

While freelancing offers flexibility and a low barrier to entry, it also leaves you exposed to unlimited personal liability. Since you and your business are legally the same, your personal assets – like your home, car, or savings – are at risk if something goes wrong. A lawsuit or unpaid debt could jeopardize everything you own.

Another hurdle is income unpredictability. Vicki James, a business owner, highlights this reality:

"You end up working a lot more than you think, oftentimes way more than when you were working for someone else".

Financial experts emphasize the need to plan ahead by setting aside 25% to 40% of your gross earnings for self-employment taxes, health insurance, and retirement savings.

Scaling your work is another challenge. Megan Crist, Founder of Range Creative Studio, points out:

"Freelancers get hired for a skill… Business owners, on the other hand, build systems".

As a freelancer, your income is tied to the hours you can personally work. Expanding beyond that – by hiring employees, selling products, or creating scalable systems – can be difficult when you’re working solo.

What Formal Business Registration Involves

How Formal Businesses Differ

Registering your business as an LLC or corporation creates a separate legal entity, setting it apart from you as an individual. This separation is critical because it protects your personal assets – like your home, car, or savings – from business-related debts or legal judgments. Essentially, your business’s financial risks won’t spill over into your personal life.

This structure also opens doors that freelancers typically don’t have access to. For instance, formal businesses can hire employees, attract investors, and establish independent systems for operations. In 2025 alone, 5.1 million new businesses had to decide on the right formation structure to suit their needs.

However, with these benefits come responsibilities. Most states require periodic filings, such as annual reports, and franchise taxes to keep the business in good standing. While this adds administrative work, the advantages often outweigh the effort.

Beyond asset protection, formal registration offers practical perks that can help your business grow.

Why Register a Business

Formal registration boosts your business’s credibility, especially with larger clients. Many corporate and government contracts insist that vendors operate as registered entities. Adding "LLC" or "Inc." to your business name signals professionalism and stability, which can give you a competitive edge.

Tax benefits are another compelling reason to register. While freelancers can deduct standard business expenses, registered entities may qualify for additional deductions, such as health insurance premiums, retirement contributions, and home office expenses. For example, converting an LLC to S-Corp taxation can save business owners between $5,000 and $15,000 annually in self-employment taxes once the business becomes profitable.

Formal registration also makes scaling easier. You can bring on partners, hire employees with proper payroll systems, and even plan for long-term succession. Unlike sole proprietorships, which typically dissolve when the owner steps away or passes on, registered businesses can continue operating.

One of the most significant benefits is personal asset protection. While no structure is immune to risks – such as personal guarantees, negligence, or mixing personal and business finances – proper registration and diligent maintenance create a legal shield that separates your personal and business worlds.

To enjoy these advantages, you’ll need to navigate the registration process.

What Registration Requires

Registering your business involves a few key steps and some associated costs. First, you’ll need to file formation documents with your state’s Secretary of State. These documents are called "Articles of Organization" for LLCs or "Articles of Incorporation" for corporations. Filing fees vary widely – from $35 in Montana to $500 in Massachusetts.

Next, appoint a registered agent. This person or service must have a physical address in your state and will receive legal documents on your behalf. Professional registered agent services typically cost between $50 and $300 annually, though some companies, like BusinessAnywhere, offer the first year for free when you register your business.

You’ll also need an EIN (Employer Identification Number) from the IRS. This number is free and helps protect your personal Social Security number when dealing with business finances.

Another important step is creating internal governance documents. LLCs should prepare an Operating Agreement, while corporations need Bylaws. These documents outline ownership and operational rules, helping to avoid disputes down the line. While not always required by state law, they are highly recommended for smooth business operations.

Finally, check for local licenses and permits. Registering with the state doesn’t exempt you from city or county requirements. General business licenses usually cost between $20 and $200, but depending on your industry, you may also need professional licenses, zoning permits, or other specific approvals to operate legally.

Freelancing vs Starting a Business: Direct Comparison

Deciding between freelancing and formally registering a business involves weighing factors like financial implications, legal protections, and potential for growth. Freelancing, typically under a sole proprietorship, ties your personal and business finances together. This means you report income using Schedule C, but there’s no legal separation between your personal and business assets. If your business faces financial trouble, creditors can go after your personal property – your home, car, or savings are all on the line. On the other hand, registering a formal business, such as an LLC, creates a separate legal entity. This separation, often referred to as the "corporate veil", shields your personal assets from business-related lawsuits and debts. However, this added protection comes with more administrative responsibilities, including filing annual reports, paying state fees, and keeping distinct financial records.

Taxes also differ significantly between these two paths. Both freelancing and LLCs generally use pass-through taxation by default, but LLCs offer additional flexibility. For instance, an LLC can opt for S-Corp status, which can reduce self-employment taxes. To illustrate, if you earn $100,000 in net income, a sole proprietor would pay around $37,300 in taxes. With an LLC electing S-Corp status and paying a $60,000 salary, the total tax drops to approximately $31,180 – a savings of more than $6,000 annually. This tax advantage highlights one of the financial benefits of formalizing your business.

Here’s a breakdown of the main differences to help you decide which route aligns with your goals:

Comparison Table: Key Differences

| Factor | Freelancing (Sole Proprietorship) | Formal Business (LLC) |

|---|---|---|

| Legal Structure | No separation; owner and business are one entity | Separate legal entity independent from owners |

| Personal Liability | Unlimited; personal assets at risk for business debts | Limited; personal assets generally protected |

| Tax Treatment | 15.3% self-employment tax on all net profit | Pass-through by default; can elect S-Corp to split income |

| Setup Cost | $0 (default status) | $50–$500 state filing fee |

| Ongoing Admin | Minimal; Schedule C tax filing only | Annual reports ($50–$800), registered agent fees |

| Client Perception | May appear informal to enterprise clients | Viewed as professional and established |

| Growth Potential | Capped by personal billable hours | Scalable through hiring and systems |

| Raising Capital | Difficult; limited to personal loans | Easier to add members or attract investors |

Legal and Tax Considerations When Formalizing

How Taxes Change

When freelancing as a sole proprietor, your business income is reported on Schedule C, attached to your personal Form 1040. You’ll face a 15.3% self-employment tax – 12.4% for Social Security (up to $184,500 in net earnings for 2026) and 2.9% for Medicare. The good news? You can deduct half of this tax from your adjusted gross income.

If you decide to register as an LLC, your tax filing doesn’t automatically change. A single-member LLC is considered a "disregarded entity", so you’ll still use Schedule C. However, you can file IRS Form 2553 to elect S-Corp status, which allows you to split your income between a "reasonable salary" and distributions. This move can reduce self-employment taxes, especially when your net income consistently exceeds $50,000–$80,000. Keep in mind, though, that payroll processing and related compliance can cost $600–$1,500 annually, so this strategy is most beneficial at higher income levels.

Another tax break to be aware of is the Qualified Business Income (QBI) deduction, which allows eligible businesses to deduct up to 20% of their qualified income. This deduction is available through 2026 and beyond. If you anticipate owing $1,000 or more in taxes, you’ll also need to pay quarterly estimated taxes (due April 15, June 15, September 15, and January 15) to avoid underpayment penalties, which can reach about 8% annualized.

Formalizing your business also comes with state-specific filing and compliance requirements.

Registration Requirements by State

To formalize your business, you’ll need to file Articles of Organization (or a Certificate of Organization) with your state’s Secretary of State. Formation fees vary widely depending on the state. You’ll also need to obtain a free EIN from the IRS, which helps protect your personal Social Security number when opening business bank accounts or hiring employees.

Most states require you to have a registered agent to receive legal and tax documents. This service usually costs $100–$300 annually. For example, BusinessAnywhere includes the first year free with business registration and charges $147 annually after that. If you’re operating under a name other than your legal business name, you may also need to file a DBA (Doing Business As) registration with your local government.

Federal compliance now includes filing a Beneficial Ownership Information Report (BOIR) with FinCEN to disclose ownership details and avoid penalties. On the state level, you may need to submit annual or biennial reports, which can cost anywhere from $50 to $800. Some states also impose franchise taxes; for instance, California requires LLCs to pay a minimum $800 annual franchise tax. If you sell physical products, you’ll likely need a state sales tax permit, although the tax itself is collected from customers.

Following these legal and tax requirements not only keeps you compliant but also strengthens the separation between your personal and business finances – a major advantage of formalizing your business.

Tools That Simplify Compliance

Keeping up with these regulatory demands can be overwhelming, but tools like BusinessAnywhere simplify the process. Their platform provides a full suite of services, all accessible through a 24/7 online dashboard. Here’s what they offer:

- LLC Formation: $0 plus state fees, with the first year of registered agent service included.

- EIN Applications: $97.

- S-Corp Tax Election Filings: $97.

- BOIR Submission: $37.

They also send compliance alerts to remind you about upcoming deadlines for annual reports or state-specific requirements. Their registered agent service ensures you never miss critical legal documents, while their virtual mailbox service (starting at $20 per month) provides a professional U.S. address with unlimited mail scanning and global forwarding. By managing these tasks in one place, you can focus on growing your business instead of drowning in paperwork – one of the many perks of formalizing your side hustle.

sbb-itb-ba0a4be

When to Formalize Your Side Gig

Factors to Consider

Deciding when to formalize your side gig depends on factors like income, risk, and client expectations. Legally, the IRS requires you to file taxes if your net earnings exceed $400. However, many experts recommend formalizing as an LLC once your monthly income reaches $1,000 (or $12,000 annually). At that stage, the benefits of liability protection and added credibility often outweigh the setup costs.

"The first big sign your side hustle has turned into a legitimate business is when revenue starts to look less like ‘extra’ money and more like a paycheck." – DBI Agency

Liability is another critical consideration. If your work involves visiting client locations, offering professional advice, or using costly equipment, it’s wise to formalize immediately – regardless of income. Operating as a sole proprietor leaves your personal savings vulnerable to lawsuits. Additionally, larger clients often require a registered business for credibility and insurance purposes.

Payment platforms like PayPal and Stripe issue Form 1099-K once your transactions exceed $20,000 in gross payments and 200 transactions. This reporting creates a clear financial trail, and with the IRS increasingly using AI to cross-reference digital payment data, operating informally carries significant risk.

As your side gig grows, planning for its future becomes even more important.

Planning for Growth

Growth brings new challenges, making formalization essential as your side hustle transitions into a full-fledged business. If you plan to hire employees, bring on a partner, or apply for business loans, establishing a formal business structure is critical. For example, hiring staff as a sole proprietor increases your personal liability, whereas an LLC provides stronger protections. Banks and lenders also typically require a registered business entity to create a business credit profile, which can lead to future funding opportunities.

Revenue growth impacts your tax obligations as well. Once your side income hits $40,000 or more annually, formalizing becomes crucial for efficient tax management. At that point, electing S-Corp status may help reduce self-employment taxes by allowing you to split income between salary and distributions. Planning ahead ensures you’re ready to seize growth opportunities without scrambling to formalize at the last minute.

"Most side hustles don’t cross into ‘business’ territory with a dramatic moment. The shift happens quietly, as revenue stabilizes, customer expectations rise, and money starts flowing back into operations." – Yuliya Pearson, Director of Product, InCorp Services Inc.

Services That Speed Up Formation

Services like BusinessAnywhere make the transition to a formal business structure seamless. Their $0 LLC formation option (plus state fees) includes a free first year of registered agent service, saving you the typical $100–$300 annual fee. After filing your LLC, you can add an EIN application for $97 to protect your Social Security number and open a business bank account. They also offer S-Corp tax election filing for $97 and handle BOIR submissions for $37.

For added convenience, their virtual mailbox service ($20/month) provides a professional U.S. address with unlimited scanning and global forwarding. With these tools, you can formalize and manage your business entirely online.

Sole Proprietorship vs LLC: Which Structure Fits

When deciding how to structure your side gig, two popular options often come into play: sole proprietorships and LLCs. Here’s a breakdown of these structures to help you figure out which one suits your needs.

Sole Proprietorship: Simple but Risky

A sole proprietorship forms automatically as soon as you start earning income. There’s no need for state filing, making it a straightforward option. In fact, about 73% of all businesses in the United States operate as sole proprietorships. You’ll report your earnings on Schedule C of your personal tax return.

But here’s the catch: there’s no liability protection. Your personal and business finances are legally the same. If your business faces a lawsuit or racks up debt, your personal assets – like your home, car, or savings – are fair game. As Stephen Fishman, CPA, puts it:

"The sole proprietorship exists precisely to lower the barrier to entry for independent work".

This structure works well for testing low-risk ideas, but it leaves you financially vulnerable if anything goes wrong.

If you want to operate under a name other than your own, you’ll need to file a DBA (Doing Business As). This step typically costs between $25 and $100, depending on your location, but keep in mind – it’s just a naming formality and doesn’t offer legal protection.

LLC: A Safer Option with Growth Potential

An LLC (Limited Liability Company) provides a legal separation between you and your business. This means that if your LLC faces lawsuits or debt, your personal assets are generally protected. Because of this, many side hustlers transition to an LLC when their income grows or when they have personal assets they want to safeguard.

Beyond asset protection, an LLC offers tax flexibility. By default, it’s taxed as a pass-through entity, similar to a sole proprietorship. However, once your net profit exceeds $50,000–$60,000, you can elect S-Corp status to save on taxes. For instance, an LLC with $120,000 in net profit could save around $7,776 annually in self-employment taxes with S-Corp treatment.

An LLC also boosts your credibility with clients and banks, making it easier to secure contracts or loans. The cost of forming an LLC varies by state, ranging from $35 in Montana to $500 in Massachusetts. Services like BusinessAnywhere even offer $0 LLC formation (plus state fees), which includes a year of free registered agent service – saving you the usual $100–$300 annual fee. You can also add an EIN application for $97, which helps protect your Social Security number and allows you to open a business bank account.

"An LLC isn’t a magic shield, but it creates a meaningful legal barrier between your business obligations and your personal wealth."

– Slava Akulov, Founder, Jupid

Comparison Table: Structure Options

Here’s a quick side-by-side look at the key features of each structure:

| Feature | Sole Proprietorship | LLC |

|---|---|---|

| Setup Process | Automatic; no state filing required | File Articles of Organization with the state |

| Liability Protection | None; personal assets are at risk | Limited; personal assets generally protected |

| Startup Costs | $0 (excluding local licenses) | $50–$500 state filing fees |

| Ongoing Maintenance | Minimal | Annual reports, fees, and operating agreements |

| Tax Options | Pass-through (Schedule C) | Pass-through; optional S-Corp election |

| Ownership | One person only | One or more members |

Your choice between a sole proprietorship and an LLC comes down to your specific needs. If your side gig earns under $20,000 annually and involves minimal risk, a sole proprietorship offers simplicity. But if you want to protect personal assets or plan to scale your income beyond $50,000, an LLC might be the better option.

Conclusion: Choosing What Works for You

Your business structure plays a big role in shaping both your protection and growth opportunities. Whether you’re aiming for simplicity or planning for long-term expansion, the choice should align with your current needs and future aspirations.

For those running a low-risk side gig with modest income, freelancing keeps things simple with no upfront costs. On the other hand, if you’re signing larger contracts, handling sensitive information, or want to shield personal assets like your home or savings, forming an LLC can provide a critical layer of protection. The formation fee, which ranges from $50 to $500, often pays for itself in peace of mind.

When your net profits climb above $50,000, the tax flexibility of an LLC, particularly with an S-Corp election, can lead to noticeable savings. And if you’re thinking about scaling beyond trading time for money, a formal structure allows you to build systems, hire a team, and create equity that isn’t tied directly to your personal effort.

As one expert puts it:

"Choose the structure that protects your life, not your ego. You can always change it later."

Remember, you’re not locked into your initial choice. Many entrepreneurs start as sole proprietors and transition to an LLC as their business evolves. The key is to evaluate your income, liability risks, and long-term goals to determine the structure that supports your next step.

If you’re ready to take the leap, services like BusinessAnywhere make the process easy with $0 LLC formation (plus state fees) and a free year of registered agent service. Take the next step with confidence and set your business up for success.

FAQs

When should I switch from freelancer to LLC?

When your side hustle starts gaining traction, taking on more risk, or requiring a more structured approach, it might be time to think about forming an LLC. Why? An LLC can shield your personal assets, keep your personal and business finances separate, and even boost your professional image.

This move becomes especially useful when your income grows substantially, you’re considering hiring employees, or you anticipate needing business loans. Many entrepreneurs begin as sole proprietors and transition to an LLC as their business expands and evolves.

Do I still need business insurance if I form an LLC?

Yes, forming an LLC often means you’ll need business insurance to protect your company from potential risks and liabilities. While an LLC helps shield your personal assets, business insurance adds another layer of protection, covering claims or damages that may arise from your business activities.

What changes do I need to make after forming an LLC?

After setting up your LLC, there are a few key steps to ensure everything runs smoothly and stays compliant. First, make sure you obtain any necessary business licenses and permits specific to your industry or location. It’s also a good idea to create an operating agreement, even if your state doesn’t require one – it helps outline how your LLC will be managed.

Next, open a dedicated business bank account. This keeps your personal and business finances separate, which is crucial for legal and tax purposes. If you plan to operate under a name different from your LLC’s registered name, consider registering a DBA (Doing Business As) name.

Finally, stay on top of ongoing requirements like filing annual reports and paying state taxes. These steps are essential to keeping your LLC in good standing and avoiding unnecessary penalties.