When offering equity to employees, the structure of your business – LLC or C-Corp – determines how equity is distributed, taxed, and managed. Here’s the key takeaway:

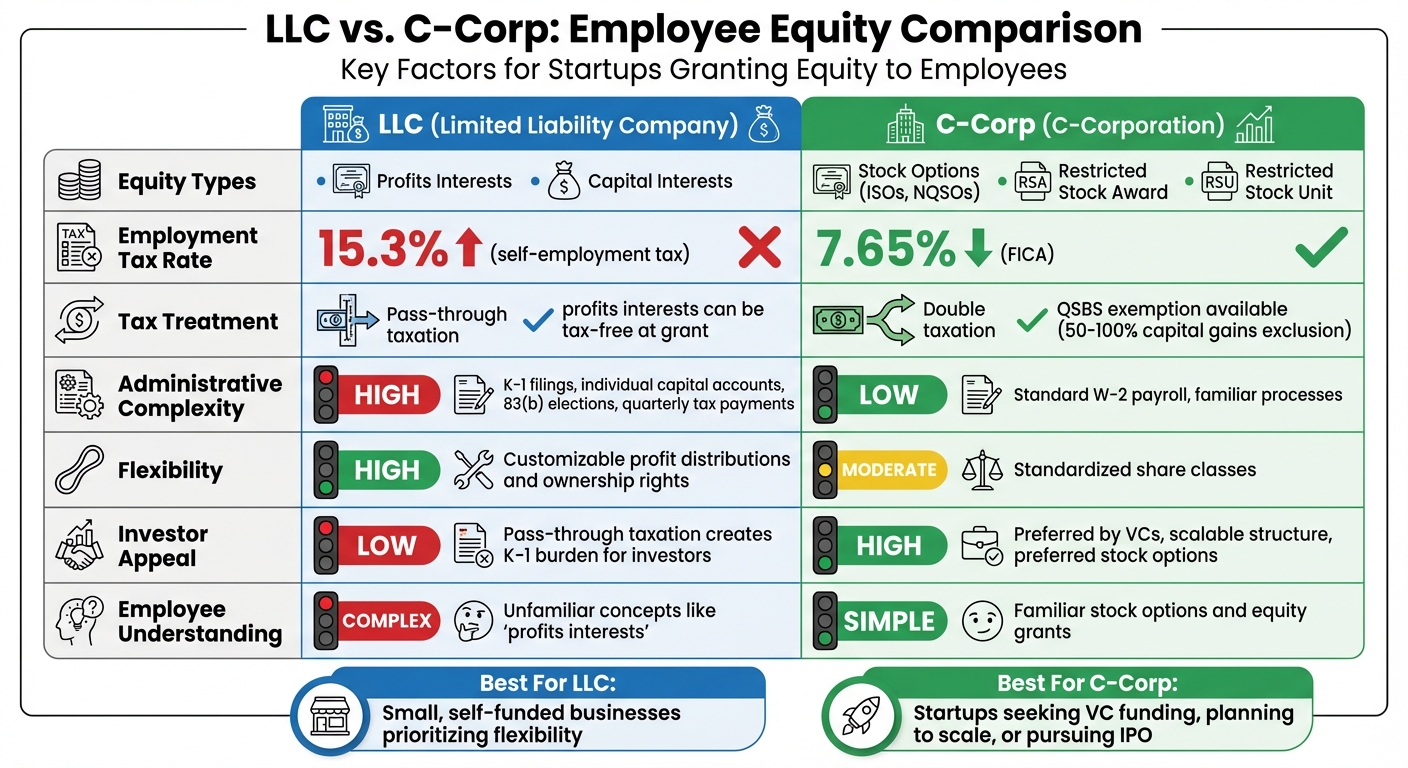

- LLCs often use "profits interests" or "capital interests" to grant equity. These offer flexibility but come with higher self-employment taxes (15.3%) and administrative complexity (e.g., filing Schedule K-1s). They’re less attractive to investors due to pass-through taxation.

- C-Corps provide standardized equity options like stock options (ISOs, NQSOs) and restricted stock (RSAs, RSUs). These are simpler to manage, taxed at lower rates (7.65% FICA), and preferred by venture capitalists for their scalability and potential tax benefits like QSBS exemptions.

For startups seeking funding or planning to scale, C-Corps are often the better choice. LLCs work well for smaller, self-funded businesses prioritizing flexibility over investor appeal.

1. LLC Equity Structures

LLCs offer equity to employees through two primary mechanisms: capital interests and profits interests. Capital interests provide employees with an immediate share in both the company’s current assets and future value. Think of it as similar to restricted stock in a corporation. On the other hand, profits interests grant employees a stake in the company’s future growth starting from the grant date, without giving them any claim to the company’s current liquidation value.

Daniel N. Janich, Of Counsel at Holifield & Janich, PLLC, highlights the appeal of profits interests:

"The nonrecognition of tax on a profits interest presents an attractive compensation vehicle for LLC employees that is not otherwise available to employees of Subchapter S or C corporations."

The tax implications for these structures are distinct. Profits interests, when they meet IRS safe harbor rules, are typically tax-free at the time of grant. In contrast, capital interests are taxed as ordinary income, based on their fair market value at the time they are granted or vested. Once employees receive equity – whether capital or profits interests – they transition to partner status. This means they receive a Schedule K-1 and are subject to a 15.3% self-employment tax, compared to the 7.65% FICA rate for regular employees.

Administrative Challenges

Managing equity in an LLC is no small feat. Companies must maintain individual capital accounts to track ownership accurately. Employees receiving restricted interests must file an 83(b) election within 30 days to secure a lower tax valuation. To offset the higher tax burden, some companies even provide "gross-up" payments. These administrative complexities can make LLC equity structures less appealing, especially when compared to simpler C-Corp mechanisms.

Additionally, the shift to partner status can bring drawbacks for employees. They may lose access to certain tax-deductible benefits, such as health insurance and retirement plans, and are required to make quarterly tax payments. This can create friction, particularly for startups, which often lean toward C-Corp equity structures for simplicity and broader appeal.

Investor Considerations

From an external perspective, LLC equity structures can pose challenges for attracting investors. Greg Miaskiewicz, CEO of Capbase, explains:

"In general, it is vastly more complex to issue equity to employees in an LLC, as compared to a C corporation. This is one of the many reasons that startups choose to incorporate as a C Corporation."

One key issue is the pass-through taxation model of LLCs. Professional investors must report LLC income on their personal tax returns via Schedule K-1s, which adds administrative headaches. For startups aiming to secure venture capital, this complexity can be a major barrier.

Despite these challenges, profits interests can be a strategic tool for compensating new hires without diluting the initial capital invested by founders. Startups often allocate 10% to 20% of total equity for employee compensation pools, and profits interests can help balance this allocation effectively. However, the administrative and tax-related hurdles often lead startups to favor C-Corp structures for their equity plans.

sbb-itb-ba0a4be

2. C-Corp Equity Structures

C-Corporations (C-Corps) offer three main equity tools for compensating employees: Stock Options (including Incentive Stock Options and Nonqualified Stock Options), Restricted Stock Awards (RSAs), and Restricted Stock Units (RSUs). Stock options allow employees to buy shares at a set price in the future, while restricted stock involves actual shares that are subject to vesting requirements.

The tax implications differ depending on the equity instrument. Incentive Stock Options (ISOs) are the most tax-friendly for employees – they aren’t taxed at the time of grant or exercise. Instead, any gains are taxed as long-term capital gains if the shares are held for at least one year after exercise and two years after the grant date. On the other hand, Nonqualified Stock Options (NQSOs) trigger ordinary income tax on the difference between the exercise price and the fair market value at the time of exercise, though companies can claim a tax deduction for this amount. RSAs are taxed as ordinary income when they vest, but employees can opt to file an 83(b) election within 30 days of the grant. This election lets them pay taxes based on the value at the grant date rather than the vesting date, potentially reducing their tax burden. These structured equity options are a key reason why C-Corps are attractive to both employees and investors.

Why Investors Prefer C-Corps

C-Corps are particularly appealing to investors, especially venture capitalists, for several reasons. Unlike LLCs, C-Corps don’t require investors to report phantom income on personal tax returns via K-1 statements, which simplifies tax filings. The standard corporate governance structure – complete with a board of directors, officers, and legally mandated bylaws – provides investors with greater oversight and a sense of security. Additionally, C-Corps can issue preferred stock, giving institutional investors priority over dividends and distributions during liquidity events.

Another major draw for investors is the Qualified Small Business Stock (QSBS) exemption under Section 1202. This provision allows individuals who hold C-Corp shares for more than five years to exclude 50% to 100% of their capital gains from federal taxes. When combined with the ability to offer ISOs – an option unavailable to LLCs – C-Corps become the go-to choice for companies looking to attract venture capital. It’s worth noting that stock option grants require formal Board approval, which must specify the recipient, the number of shares, the vesting schedule, and an exercise price at or above the fair market value. This process ensures compliance and avoids penalties under Section 409A.

Pros and Cons

When deciding between LLCs and C-Corps, it often boils down to a trade-off between the flexibility offered by LLCs and the streamlined structure of C-Corps. LLCs provide the ability to customize profit distributions, which don’t have to align with ownership percentages. They can also grant profits interests that, if structured to meet IRS safe harbor rules, may be tax-free at the time of grant. This flexibility, however, comes with its own set of challenges, especially when it comes to taxes and administration.

One of the key hurdles LLCs face is their tax structure. LLC members are subject to a 15.3% self-employment tax on their entire share of income, compared to the 7.65% FICA tax that W-2 employees pay in a C-Corp. Additionally, LLC equity holders receive Schedule K-1 forms and often need to file estimated quarterly taxes, sometimes in multiple states where the LLC operates. They also miss out on certain tax-deductible benefits. These complexities can make it harder for LLCs to attract both investors and top talent.

On the other hand, C-Corps are more appealing to investors and easier for employees to understand. They offer standardized equity instruments like ISOs, NQSOs, RSAs, and RSUs, which are favored by venture capitalists and avoid the pass-through tax issues faced by LLCs. C-Corp stock may also qualify for the QSBS exemption, which can allow employees to exclude 50%–100% of gains from federal taxes if they hold the shares for more than five years.

"For both C corporations and LLCs taxed as partnerships, there is a tension between the employer and employee regarding the tax character of equity grants: Employers prefer to grant equity taxed as ordinary income, which would result in a deduction… while employees prefer to receive equity that will provide long-term capital gains treatment",

explains Frost Brown Todd.

Here’s a side-by-side comparison of key factors for LLCs and C-Corps:

| Factor | LLC (Partnership) | C-Corporation |

|---|---|---|

| Flexibility | High – customizable distributions and rights | Moderate – standardized share classes |

| Tax Treatment | Pass-through; profits interests can be tax-free | Double taxation; QSBS eligibility |

| Employment Taxes | 15.3% self-employment tax (paid by member) | 7.65% FICA (paid by employee) |

| Administrative Complexity | High – K-1 filings and detailed capital accounts | Low – standard W-2 payroll |

| Investor Preference | Less appealing to venture capitalists | Preferred for scalability |

| Employee Understanding | Complex (e.g., "profits interests") | Familiar stock options and equity grants |

For LLCs looking to simplify employee compensation, alternative approaches like phantom equity or Unit Appreciation Rights (UARs) can be effective. These options allow employees to remain W-2 earners while receiving cash bonuses tied to increases in the company’s value. While these methods sacrifice some tax benefits, they offer a simpler structure. Ultimately, the decision between an LLC and a C-Corp depends on whether flexibility or scalability aligns better with the company’s long-term equity and growth goals.

Conclusion

Choose a C-Corp if your plans include raising venture capital, rapid scaling, or pursuing an IPO. Investors often prefer its standardized structure, stock options, and the potential tax advantages provided by the QSBS exemption, which can lead to significant long-term savings. These benefits highlight the importance of aligning your entity choice with your company’s long-term growth and funding strategy.

For entrepreneurs bootstrapping or running smaller operations, an LLC’s pass-through structure can offer flexibility. However, converting equity into partner status comes with added tax and administrative considerations. In many cases, simpler options might better suit LLC owners. Regardless of the structure, careful planning is crucial to ensure your entity type supports your future growth plans.

If you anticipate institutional funding but start as an LLC, consider converting to a C-Corp early – ideally before your first major funding round. This timing can help you sidestep potential valuation and tax hurdles. Facebook’s well-documented transition from an LLC to a C-Corp as it scaled demonstrates that such changes are not only common but also manageable when approached strategically.

Ultimately, your choice should reflect your funding needs, growth ambitions, and compensation strategy. C-Corps simplify equity distribution and appeal to investors, while LLCs provide flexibility and tax advantages for smaller, self-funded ventures. There’s no one-size-fits-all solution – what matters most is selecting the structure that aligns with your specific business goals and the equity narrative you want to share with future employees.

FAQs

What are the key tax differences for employees receiving equity in an LLC versus a C-Corp?

The key tax difference between LLC and C-Corp equity for employees lies in how and when taxes are applied to compensation.

For LLCs, equity compensation – like profits interests – is usually taxed based on the increase in value, often at the time of vesting or sale. While proper structuring can sometimes lead to more favorable tax outcomes, the rules governing LLC equity are more intricate compared to C-Corps, making them a bit harder to navigate.

With C-Corps, equity options such as Incentive Stock Options (ISOs) and Non-Qualified Stock Options (NSOs) follow different tax rules. ISOs can offer potential tax benefits since they aren’t taxed at the time of exercise, and taxation only occurs upon sale if specific conditions are met. On the other hand, NSOs are taxed as ordinary income when exercised, based on the difference between the option’s exercise price and the stock’s fair market value.

In summary, LLC equity often involves deferred or more complex tax scenarios, while C-Corp equity typically triggers taxes at exercise or vesting. Deciding between these structures requires careful consideration of tax implications to match your business goals and employee incentive strategies.

Why do investors often prefer C-Corporations over LLCs for offering equity to employees?

Investors often lean toward C-Corporations rather than LLCs when it comes to equity distribution, largely because of the clear and standardized structure C-Corps offer. They can issue stock options or restricted shares with defined vesting schedules, making it easier for investors to evaluate and value their equity. This level of transparency is particularly attractive to venture capitalists and institutional investors who prioritize predictability.

On the other hand, LLCs use membership or profits interests, which tend to be more complex and unfamiliar to many investors. Moreover, the tax treatment of equity in C-Corps is generally simpler and aligns better with activities like raising capital or planning for liquidity events down the line. For these reasons, C-Corps are typically the go-to choice for equity distribution.

What’s the difference between LLC profits interests and C-Corp stock options for employees?

LLC profits interests and C-Corp stock options offer two distinct ways to provide equity incentives to employees, each with its own advantages and considerations.

LLC profits interests give employees a share in the company’s future profits or value growth, rather than direct ownership. These are often seen as a tax-friendly option for employees and allow for flexible incentive structures. However, because they don’t come with actual ownership rights, they may not provide the same level of long-term motivation for some employees.

C-Corp stock options allow employees to purchase company shares at a predetermined price, giving them a real ownership stake. They’re popular and relatively straightforward in concept, but they come with more intricate tax and compliance obligations, especially when employees decide to exercise or sell their options.

The choice between these two depends on your company’s legal structure, growth strategy, and the kind of incentives you want to offer your team.