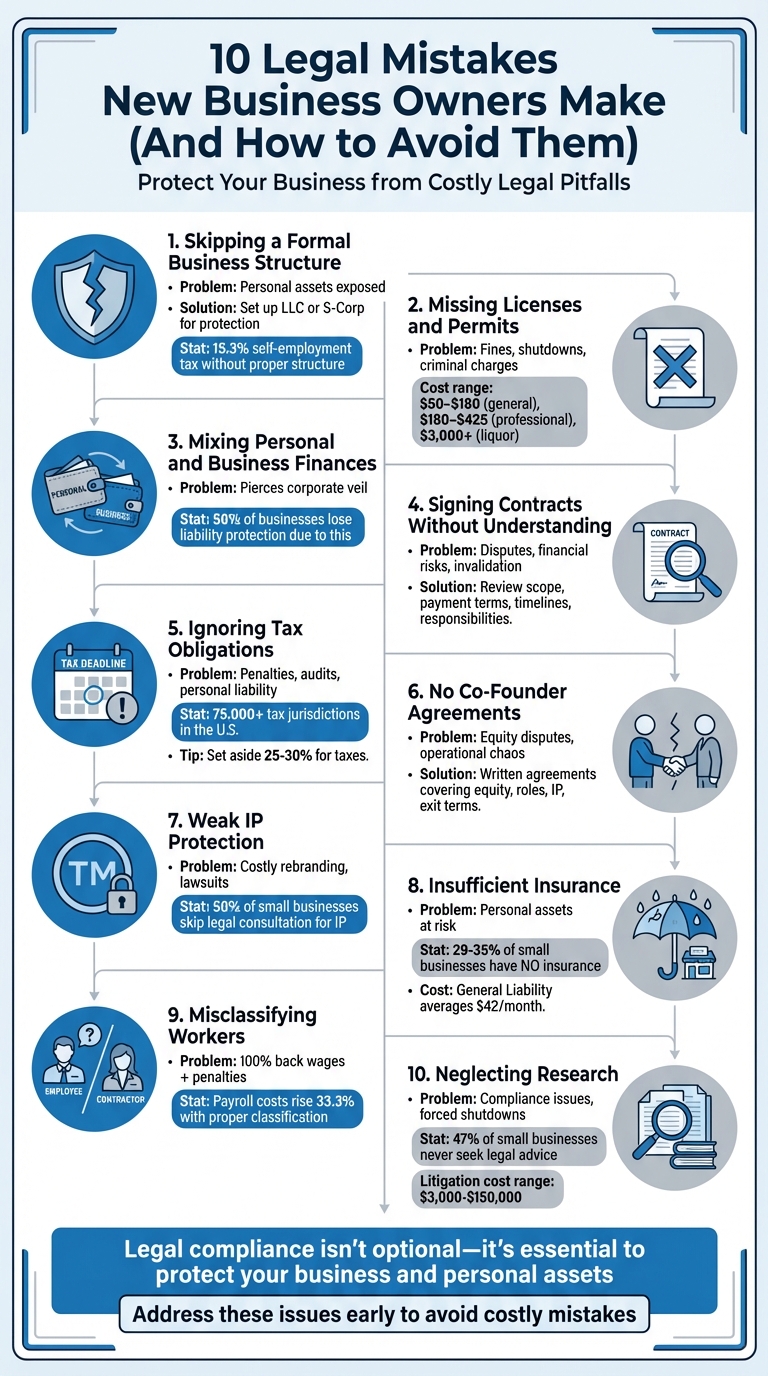

When starting a business, legal missteps can lead to lawsuits, financial losses, or even closure. This guide covers the 10 most common legal mistakes new business owners make and how to avoid them:

- Skipping a formal business structure: Operating as a sole proprietor exposes personal assets. Setting up an LLC or S-Corp protects them and reduces taxes.

- Missing licenses and permits: Failing to comply with federal, state, or local requirements can result in fines or shutdowns.

- Mixing personal and business finances: This can void liability protections and complicate taxes.

- Signing contracts without understanding them: Poorly reviewed contracts can lead to disputes and financial risks.

- Ignoring tax obligations: Missing deadlines or mismanaging payroll taxes can result in penalties or audits.

- No co-founder agreements: Verbal agreements can lead to equity disputes and operational chaos.

- Weak intellectual property (IP) protection: Not securing trademarks or IP rights can result in costly rebranding or lawsuits.

- Insufficient insurance: Lack of coverage leaves businesses vulnerable to lawsuits or disasters.

- Misclassifying workers: Mislabeling employees as contractors can lead to back taxes and penalties.

- Neglecting research: Skipping market and legal research can result in compliance issues or operational hurdles.

Key takeaway: Legal compliance isn’t optional – it’s essential to protect your business and personal assets. By addressing these issues early, you can avoid costly mistakes and focus on growth.

10 Common Legal Mistakes New Business Owners Make and How to Avoid Them

1. Operating Without a Formal Business Structure

Setting up the right business structure is a key step to steering clear of legal risks. Many entrepreneurs start as sole proprietors, but this choice can leave personal assets exposed. Without formal registration, there’s no separation between personal and business finances, putting your personal wealth at risk.

"Selecting the appropriate legal structure for your business is crucial… LLCs and corporations can offer limited liability, protecting personal assets from business debts, whereas sole proprietorships and partnerships offer no such protection." – John McWilliams, McWilliams Law Group

Beyond protecting your assets, a formal business structure can help you avoid unnecessary tax burdens. For instance, without an entity like an LLC or S-Corp, all profits are subject to a 15.3% self-employment tax. Opting for an S-Corp allows you to split income between salary and distributions, saving thousands since distributions aren’t subject to that tax.

Another advantage? Credibility. Investors, especially venture capitalists, often insist on a formal structure like a C-Corporation before committing funds. Without it, you might miss out on critical funding opportunities.

Establishing an LLC or S-Corp not only protects your personal assets but also reduces tax liabilities and boosts your appeal to investors. For example, BusinessAnywhere offers $0 business formation plus state fees, including the first year of registered agent service for free. Even if you’re the sole owner, it’s wise to draft essential agreements and keep business finances separate by opening a dedicated business bank account.

2. Failing to Obtain Required Licenses and Permits

Skipping the licensing process might seem like an easy shortcut, but it’s a mistake that can cost you big time – potentially shutting down your business overnight. Operating without the right licenses can lead to hefty fines, forced closures, or even criminal charges.

Business licenses are required at federal, state, and local levels, and what you need depends on your industry and location. Federal licenses apply to heavily regulated areas like alcohol, firearms, aviation, and broadcasting. On the state level, most businesses need a sales tax permit, and some industries – like medicine, law, or cosmetology – require professional licenses. Locally, you might need a general business license, zoning approval, health department permits for food handling, or fire department clearances. These requirements are non-negotiable if you want your business to operate legally.

"It’s essential that you have the necessary business licenses before opening your doors to the public." – Christine Mathias and Amanda Hayes, Attorneys, Nolo

The costs of compliance vary widely. A general business license typically costs between $50 and $180, while professional licenses can range from $180 to $425. Specialized permits are often much more expensive – liquor licenses can exceed $3,000, and marijuana permits can cost even more. While these fees can feel steep, they’re a fraction of what you might pay in penalties for non-compliance.

Failing to comply with licensing rules can have consequences beyond fines. States can dissolve your business, which means losing liability protection and potentially being held personally responsible for debts. If you fall behind on licensing fees, tax liens could follow – and those aren’t wiped out in bankruptcy. To avoid these risks, double-check zoning rules before signing a lease and make sure all required permits are in place. For guidance, reach out to your local Small Business Development Center or consult your Secretary of State’s website for a tailored list of requirements for your industry.

3. Neglecting to Separate Personal and Business Assets

Mixing personal and business finances can quickly strip away the legal protections your business structure provides. For instance, if you pay personal bills with your business account or use your personal credit card for business expenses, courts and creditors may "pierce the corporate veil", leaving you personally liable for business debts and lawsuits. Shockingly, nearly 50% of businesses that face lawsuits lose their liability protection due to incomplete paperwork or failing to keep finances separate.

The fallout from this mistake goes beyond legal disputes. Your personal assets – like your home, car, savings, and investments – could be at risk if you blur the lines between personal and business finances. Commingling funds also complicates taxes. It becomes difficult to prove which expenses qualify as legitimate business deductions, and auditors may reject write-offs that appear personal. Poor financial separation can also increase your chances of being audited and make it harder to defend your business in investigations.

"By separating your business and personal finances, you can keep track of your expenses, income, and profits more accurately." – TaxAct

To avoid these pitfalls, implement strict financial boundaries. Start by opening a business checking account and credit card using your EIN, which you can get for free through the IRS. If you operate an S-Corp or C-Corp, pay yourself a regular salary. For LLCs, take documented owner draws instead of making random withdrawals. Always sign contracts and checks with your official business title to reinforce the separation of liability.

Invest in professional bookkeeping tools to track every transaction and keep receipts that directly link to business activities. Maintain your operating agreements or bylaws, document major decisions with meeting minutes, and file annual reports on time. These steps demonstrate that your business operates as an independent entity, not an extension of your personal finances.

BusinessAnywhere offers services to help you set up your business correctly from the start. Their business registration services start at $0 plus state fees, and they include a free EIN application so you can open a business bank account with ease. They also provide a registered agent service – free for the first year – to keep your personal address off public records and ensure you receive legal documents promptly. These tools can help you maintain the clear separation needed to protect both your business and personal assets.

4. Signing Contracts Without Understanding Terms

Signing a contract without fully understanding its terms can lead to serious headaches for your business. It’s not uncommon for new business owners to skim contracts or rely on verbal assurances, only to later discover that the written terms don’t align with their expectations. Vague clauses about payment schedules, deliverables, or termination conditions can quickly snowball into costly legal disputes or even contract invalidation.

The consequences of poorly understood contracts can go far beyond simple misunderstandings. Take, for example, a case from March 2022 in the São Paulo Court of Appeals. In Appeal No. 0021687-37.2017.8.26.0196, a contract labeled as a "trademark license" was reclassified as a franchise agreement because the licensor exercised too much control over aspects like store layouts, uniforms, and suppliers. The court declared the contract null, ordered the licensor to reimburse all royalties paid, and even awarded BRL 30,000 in moral damages. This case highlights how poorly drafted agreements can unexpectedly create legal and financial burdens – even when both parties enter with good intentions.

"A well-drafted business contract is crucial for protecting your company’s rights, clarifying obligations, and minimizing risks." – McWilliams Law Group

To avoid these pitfalls, focus on thoroughly reviewing key contract elements. These include:

- Scope of work: Ensure it clearly defines deliverables and expectations.

- Payment terms: Specify amounts, payment schedules, and penalties for late payments.

- Timelines and deadlines: Set clear milestone dates to track progress.

- Responsibilities: Detail what each party is obligated to do.

- Dispute resolution: Include procedures like mediation or arbitration to handle conflicts efficiently.

Additionally, pay close attention to the definitions section in longer contracts. Misunderstandings often arise from how terms like "Company" or "Deliverables" are defined. For example, "shall" indicates a binding obligation, while "may" provides flexibility.

Hiring a business attorney to review contracts is one of the best ways to protect your company. Legal professionals can identify hidden risks, clarify ambiguous terms, and ensure compliance with federal and state laws. While online templates can be a helpful starting point, they should always be tailored to fit your specific business needs. Just as a solid business structure protects your assets, legal oversight ensures your contracts work in your favor.

For added convenience, BusinessAnywhere provides online notary services for $37 per notarization. This service allows you to handle contracts remotely while ensuring your signatures are legally valid across all U.S. states. It’s a simple way to make sure your agreements are authenticated and enforceable from the outset.

5. Overlooking Tax Obligations and Compliance

Taking care of your tax responsibilities is just as important as securing licenses or drafting solid contracts for your business. In the U.S., there are more than 75,000 federal, state, and local tax jurisdictions, each with its own set of rules and requirements. Missing a tax deadline or misunderstanding your obligations can lead to hefty penalties, audits, or even personal liability – especially when it comes to payroll taxes.

To stay on top of things, accurate tax recordkeeping is a must. Start by opening a dedicated business bank account and credit card. This setup not only makes tracking expenses and deductions easier but also protects your personal assets from tax-related liabilities. It’s also smart to set aside 25–30% of your earnings for federal and state taxes. Mixing business and personal accounts complicates recordkeeping and can cause issues when meeting tax deadlines.

"Accidentally failing to comply with tax laws, violating tax codes, or filling out forms incorrectly can leave taxpayers and their businesses open to possible penalties." – Internal Revenue Service

Quarterly estimated tax payments are another common stumbling block. If you expect to owe $1,000 or more when filing your return, you’ll need to make estimated payments on April 15, June 15, September 15, and January 15. Missing these deadlines can result in penalties and interest charges. To avoid this, consider using a compliance calendar or accounting software to help you track and meet these quarterly deadlines.

If you have employees, managing employment taxes is critical. You’re required to withhold federal income tax, Social Security, and Medicare taxes from employee wages, along with paying the employer’s share through electronic fund transfers. Neglecting to deposit these "trust fund taxes" can make you personally liable – even if your business is an LLC or corporation. For LLCs taxed as S-Corporations, owners must also pay themselves a "reasonable wage." If the IRS finds you’re underpaying yourself to dodge payroll taxes, you could face an audit. Services like BusinessAnywhere offer tools to help, including EIN applications for $97 and S-Corp tax election filing for $147, ensuring you start with the right tax setup.

Don’t forget about state and local tax obligations either. Depending on your location, you might need to register for sales tax permits, pay franchise taxes, or contribute to state unemployment insurance (SUTA). For example, California imposes a minimum $800 annual fee for LLCs, while in Florida, failing to file an annual report by the third Friday in September can result in a $400 late fee or even dissolution of your LLC. Partnering with a certified public accountant (CPA) or an enrolled agent can help you navigate these requirements and maximize deductions, like the $5,000 start-up expense deduction.

6. Failing to Establish Clear Co-Founder Agreements

Starting a business with just a handshake agreement might seem simple, but it’s a risky move that can lead to costly legal battles. Without a written agreement, disputes over equity, roles, or exit terms can quickly spiral out of control, potentially halting your business entirely. Verbal agreements are often unenforceable, leaving startups vulnerable to conflicts they can’t afford.

A well-thought-out co-founder agreement is essential. It should cover key aspects like equity splits and vesting schedules, capital contributions, and clearly defined roles (e.g., CEO, CTO). It must also assign intellectual property rights to the company and outline decision-making processes for both day-to-day operations and significant strategic moves. Additionally, provisions for what happens if a founder resigns, retires, or faces unforeseen circumstances like disability or death are crucial. These should include buy-sell terms that allow the company to repurchase shares. Including a dispute resolution clause – favoring confidential arbitration or mediation – can save time, money, and public scrutiny.

"Discussing and addressing these issues at the beginning can avoid problems and conflicts later on, and it can help ensure that all parties are in alignment about how the business will be operated." – Richard Harroch, Senior Advisor and Venture Capitalist

While you might be tempted to use an online template, startup attorney Richard Harroch advises against it: "You can’t just get a ‘template form’ online and plug in names. You have to write it with your specific situation in mind, with the help of a startup lawyer or credible online legal assistance service".

One practical suggestion is to steer clear of 50-50 equity splits. Instead, consider a 51-49 structure to ensure one partner has the final say during deadlocks. Also, make it a priority to have all founders, employees, and contractors sign a Confidentiality and Invention Assignment Agreement from the very beginning.

A solid co-founder agreement lays the groundwork for smooth internal governance. Services like BusinessAnywhere can assist in creating legally sound agreements as part of their business registration support. Just as external contracts protect your business dealings, a clear co-founder agreement ensures your internal operations are built on a strong legal foundation.

sbb-itb-ba0a4be

7. Inadequate Intellectual Property Protection

When it comes to intellectual property (IP), ownership doesn’t automatically transfer to your business unless you have a written assignment agreement in place. For example, even a freelance designer retains rights to the logo they create for you unless they formally assign those rights to your company. This oversight can cause major headaches, especially during fundraising or acquisition talks, when investors realize your business doesn’t legally own its key assets. Protecting your IP is just as critical as separating personal and business finances – it shields you from legal and financial pitfalls.

Using a trademarked name can lead to costly rebranding efforts, wiping out your brand equity and confusing your customers. Similarly, using unlicensed images from the internet could result in copyright infringement lawsuits, with settlements often running into thousands of dollars. And if you publicly disclose an invention before filing for a patent, you risk losing your patent rights entirely in most countries – though the U.S. offers a one-year grace period as an exception.

"Mistakes related to IP can be fatal to a startup." – Entrepreneur

To avoid these risks, start with a thorough clearance search before committing to a brand name. Use tools like the USPTO’s Trademark Electronic Search System (TESS), Google, domain registrars, and social media platforms to confirm the name is legally available. This step can save you from expensive rebranding down the road. Once cleared, register your trademark and secure matching domain names and social handles to lock in your brand identity.

Formal agreements are essential for safeguarding your creative assets. Every founder, employee, and contractor should sign an IP assignment agreement that transfers all rights to your business. Without this, ownership disputes can arise, leaving your business exposed. Trade secrets, on the other hand, require confidentiality rather than registration. Clearly mark proprietary documents as confidential and ensure anyone with access signs a non-disclosure agreement (NDA).

Surprisingly, nearly half of small businesses skip consulting a legal professional for IP protection. Relying on generic online templates can backfire. As attorney Mark P. Kesslen explains:

"It is often the intellectual property issues that slow down the deals, because the proper steps were not considered and/or implemented early in the project life cycle".

To simplify the process, services like BusinessAnywhere offer trademark filing solutions to help protect your assets. With your IP secured, you can turn your attention to other critical areas, like ensuring your business has proper insurance coverage.

8. Insufficient Business Insurance Coverage

Running a business without proper insurance can leave you exposed to serious financial risks. Shockingly, between 29% and 35% of small business owners with 1 to 50 employees operate with no business insurance at all. Even more concerning, about half of businesses that face lawsuits lack protection against "piercing the veil" legal claims. This means creditors or plaintiffs could go after personal assets – like your home, car, or savings – to settle business debts. A single lawsuit or disaster could be enough to shut your business down if you’re not insured.

At the federal level, businesses with employees are required to carry Workers’ Compensation, Unemployment, and Disability insurance. Beyond these requirements, General Liability Insurance is a must for most businesses. This coverage, which averages $42 per month, helps protect against common accidents like slip-and-fall incidents that could lead to costly lawsuits. For service-based businesses, Professional Liability Insurance is essential. At an average cost of $61 per month, it covers claims of negligence, ensuring you’re protected if a client alleges your work caused them harm.

"General liability insurance is perhaps the most important type of insurance coverage any business can have, as it keeps you safe from generic claims of wrongdoing and will ensure you can keep the lights on should you be sued." – Entrepreneur

Another smart option for small businesses is a Business Owner’s Policy (BOP). This combines General Liability, Commercial Property, and Business Interruption coverage into one package for about $57 per month. It’s a cost-effective way to get comprehensive protection.

As your business grows, it’s critical to reassess your insurance needs every year. Adding new equipment, hiring employees, or expanding your operations can introduce new risks that require updated coverage. The U.S. Small Business Administration advises: "You should insure against things you wouldn’t be able to pay for on your own". And while you’re reviewing your policies, take the opportunity to ensure workers are properly classified – this step can further protect your business from potential legal and financial headaches.

9. Misclassifying Employees and Independent Contractors

Getting worker classification wrong can lead to steep financial consequences. If you misclassify an employee as an independent contractor, you could be on the hook for 100% of back wages, an equal amount in liquidated damages, unpaid Social Security and Medicare taxes, unemployment insurance, penalties, and even attorney’s fees. Considering that employee payroll costs typically rise by over one-third (33.3%) when you include taxes and benefits, this mistake can be both a legal and financial nightmare, potentially jeopardizing the survival of a small business.

To determine whether a worker is genuinely an independent contractor or an employee, the federal government applies an "economic reality" test. As of March 11, 2024, the Department of Labor (DOL) uses a six-factor analysis that evaluates the overall circumstances. However, by February 26, 2026, the DOL has proposed shifting to a simpler "core factors" approach, focusing on control over the work and the worker’s opportunity for profit or loss. The public comment period for this proposed rule ends on April 28, 2026. This evolving regulatory framework highlights the complexities new business owners must navigate.

Key questions to ask: Does the worker set their own schedule, invest in their own equipment, and market their services independently? Or do you provide the tools, dictate the hours, and control the work details? If you’re calling the shots on schedules, equipment, and tasks, that person is likely an employee. Remember, a signed "Independent Contractor Agreement" or issuing a 1099 form doesn’t override the reality of the working relationship.

"The rule we are proposing today… is aimed at ensuring that workers and employers know how to apply those principles predictably." – Andrew Rogers, Wage and Hour Division Administrator

Federal guidelines also emphasize the importance of accurate classification. In addition to the DOL’s economic reality test, the IRS uses its own criteria, focusing on behavioral and financial control, as well as the nature of the relationship between the worker and employer. State-specific tests, like California’s ABC test, further stress that actual control over work defines employment status.

If you discover you’ve made a classification error, the IRS Voluntary Classification Settlement Program (VCSP) allows eligible businesses to reclassify workers for future tax periods with reduced federal employment tax liability. To avoid these pitfalls, conduct regular audits of your worker classifications. Proper classification is critical to protecting your business from legal and financial risks.

10. Failing to Conduct Adequate Market and Legal Research

Skipping thorough research before launching a business can leave you vulnerable to serious setbacks. Shockingly, about 47% of small businesses have never sought legal advice. This lack of preparation can lead to regulatory violations, forced shutdowns, or steep financial losses, with litigation costs ranging anywhere from $3,000 to $150,000.

Neglecting research could mean operating without necessary licenses, unintentionally infringing on trademarks, or failing to meet tax obligations. For example, choosing the wrong business structure – like staying a sole proprietorship when you need the liability protection of an LLC – might put your personal assets at risk. Online businesses face additional risks if they ignore data privacy laws. For instance, the California Consumer Privacy Act requires businesses to notify individuals within 72 hours of a data breach, and non-compliance can result in hefty penalties.

Once you’ve done your research, seeking legal advice is the next critical step.

"Good legal counsel is essential and can certainly be a competitive advantage for business owners who have to manage both opportunities and potential risks." – Charley Moore, Founder and Executive Chairman, Rocket Lawyer

Start by conducting a detailed name search through your state’s Secretary of State office and the U.S. Patent and Trademark Office (USPTO) to avoid the expense and hassle of rebranding later. Check for required permits and regulatory compliance specific to your industry. Determine whether you need an Employer Identification Number (EIN) and familiarize yourself with your state’s tax laws.

A solid foundation also includes staying organized. Keep a compliance calendar for license renewals, filings, and tax deadlines. Draft internal governance documents early to avoid defaulting to state-imposed rules. If you plan to hire, research the legal differences between employees and independent contractors to prevent misclassification penalties. For online businesses, ensure your website includes Privacy Policies and Terms of Service that align with state data protection laws.

In-depth market and legal research not only helps you avoid costly mistakes but also sets the stage for long-term success. By combining research with the right legal frameworks and agreements, you create a strong, reliable foundation for your business to thrive.

Conclusion

Starting a business is an exciting journey, but it comes with legal challenges that can quickly derail even the most promising ventures. Throughout this guide, we’ve highlighted key mistakes that could jeopardize your business – like neglecting a formal structure, skipping essential contracts, overlooking tax compliance, or failing to protect intellectual property. These missteps can lead to personal liability, expensive lawsuits, or even shutting down your business. The upside? Every one of these mistakes is avoidable with timely attention to legal compliance.

"The smartest founders understand that investing in a proper legal setup is the highest-return investment they can make. It’s the cost of admission to building something that lasts." – InCorp Services

Being proactive beats scrambling to fix issues later. By formalizing your business structure, separating personal and business finances, securing written agreements, and staying on top of corporate formalities, you create a strong legal foundation. This not only protects your personal assets but also sets your company up for long-term success.

Don’t go it alone – consult a CPA about tax elections like S-Corp status, and have an attorney review contracts before any issues arise. Tools like BusinessAnywhere make compliance more manageable, offering services like $0 business formation, registered agent support, compliance alerts, virtual mailboxes, and annual report filings. With features like automated monitoring and expert guidance, you can stay focused on growing your business while keeping your legal foundation secure.

Legal compliance isn’t just a box to check – it’s the backbone of a resilient business. By addressing these issues early, you’ll save yourself from unnecessary stress, financial losses, and sleepless nights in the future. Start today, and build a business that stands the test of time.

FAQs

Do I need an LLC right away?

Forming an LLC isn’t something you have to do right away, but it’s definitely worth considering sooner rather than later. Setting up an LLC helps shield your personal assets and gives your business a solid legal framework to operate within. The timing really depends on what you’re aiming to achieve with your business and how you want to handle taxes. That said, getting your LLC in place early can help you steer clear of potential legal or financial headaches down the road. It’s always a smart move to talk to a legal expert to figure out the best approach for your specific situation.

What licenses or permits does my business need?

The licenses and permits your business needs will vary based on what you do, where you’re located, and your industry. Generally, small businesses need to secure permits at the federal, state, and local levels. Federal licenses are typically required for regulated activities like alcohol distribution or transportation. On the other hand, state and local permits might include general business licenses, seller’s permits, or permits specific to your industry. It’s essential to check with local authorities and regulatory agencies to ensure everything is in order before launching your business.

When should I hire a lawyer or CPA?

Hiring a lawyer or a CPA early in your business journey is a smart move – ideally before or during the registration process. A lawyer can guide you in selecting the best legal structure for your business, draft essential contracts, and ensure you’re meeting all state regulations. On the other hand, a CPA plays a key role in setting up your financial systems, navigating taxes, and keeping your business compliant with financial laws.

Getting these professionals involved from the start can help you avoid expensive mistakes and establish a strong foundation for your business.