Startups often overlook a key financial opportunity: R&D tax credits. These credits can reduce your tax bill dollar-for-dollar or offset payroll taxes – even if you’re not profitable yet. Here’s why they matter and how to claim them:

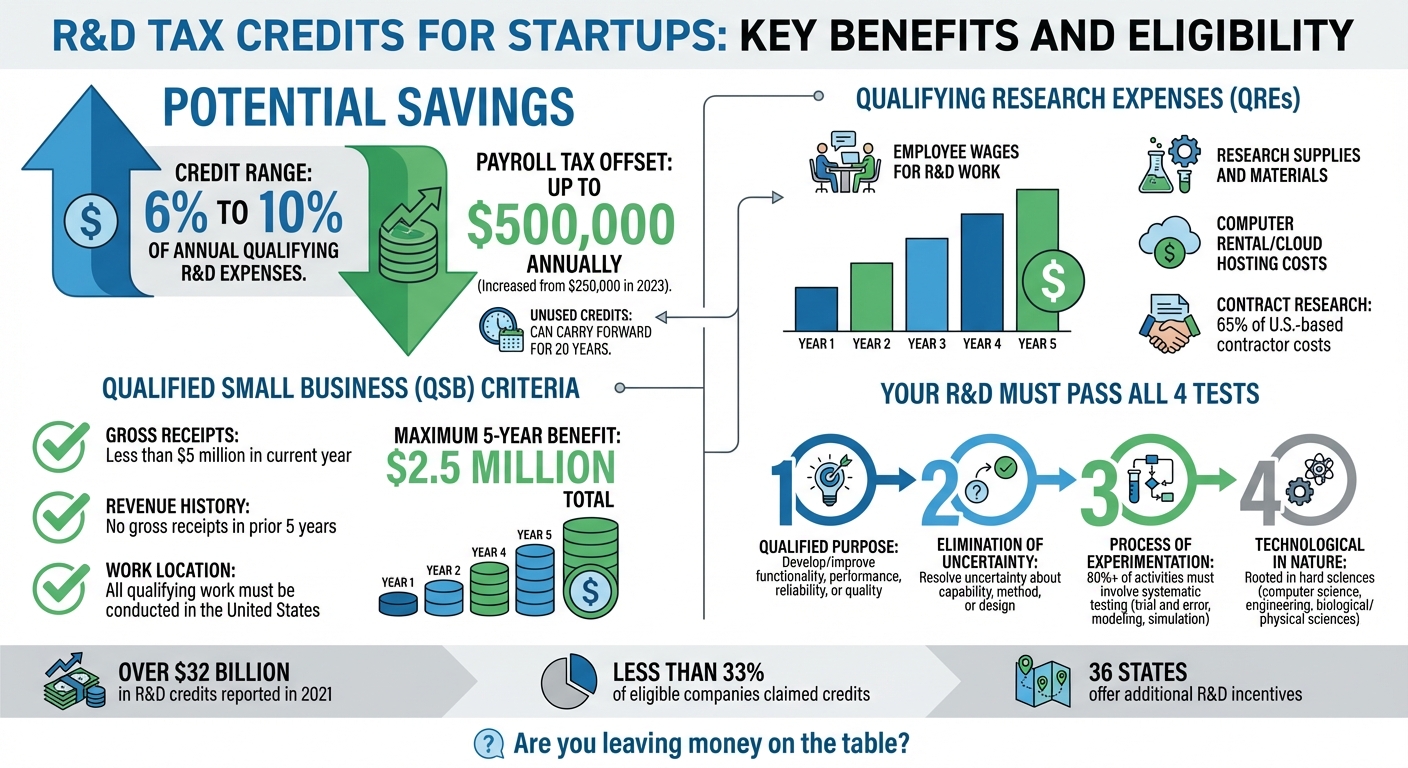

- What it is: A federal tax credit for qualified research activities, offering up to 10% back on eligible expenses like wages, supplies, and contract research.

- Who qualifies: Startups with less than $5M in gross receipts and no revenue in the last 5 years can apply credits to payroll taxes.

- How much you can save: Up to $500,000 annually for payroll taxes, with unused credits carrying forward for 20 years.

- Recent updates: The 2025 tax law changes now allow immediate deductions for R&D expenses, simplifying compliance and improving cash flow.

If you’re building new products, solving technical challenges, or improving processes, you may qualify. Keep detailed records and follow IRS guidelines to ensure your claim is accurate. Start leveraging this benefit today to ease financial strain and fuel your growth.

R&D Tax Credits for Startups: Key Benefits and Eligibility Requirements

What Are R&D Tax Credits and Why They Matter

R&D Tax Credits Explained

The federal R&D tax credit, introduced in 1981 and made permanent in 2015 under the PATH Act, offers a dollar-for-dollar reduction in your federal tax liability for qualified research activities. For example, if your startup owes $50,000 in taxes and you claim a $20,000 R&D credit, your tax bill drops to $30,000.

For startups that aren’t yet profitable, the credit can be applied to payroll taxes instead – specifically, the employer’s Social Security and Medicare contributions. This provides an immediate financial benefit.

To qualify for the payroll tax offset, your business must meet the Qualified Small Business (QSB) criteria. This means having less than $5 million in gross receipts for the current year and no gross receipts during any of the prior five years.

These features translate into real cash flow advantages for startups, which can make a huge difference during early growth stages.

Benefits for Startups

The credit covers a range of costs, including wages for engineers, research supplies, and 65% of U.S.-based contract research expenses. Startups can typically recover 6% to 10% of their annual qualifying R&D expenses.

One of the standout benefits is the ability to apply the credit against payroll taxes for up to five years. This can significantly boost cash flow when startups need it most. Additionally, any unused credits can be carried forward for up to 20 years, giving businesses the flexibility to offset future tax liabilities as they grow.

"The expanded R&D credit payroll tax offset will provide startup businesses with increased cash savings by maximizing total R&D credit utilization prior to sustaining sufficient taxable income." – BDO

Inflation Reduction Act Changes

Recent updates under the Inflation Reduction Act, effective January 1, 2023, have made these benefits even more attractive. The annual payroll tax offset limit increased from $250,000 to $500,000, split between the employer’s Social Security tax (6.2%) and Medicare tax (1.45%).

Eligible startups can now claim this offset for up to five taxable years, potentially saving $2.5 million over that period. This change is a game-changer for startups working with tight budgets, as it provides a significant cash flow boost. For instance, if you file your income tax return with the R&D credit election by March 31, you can begin reducing your payroll taxes as early as the second quarter.

"Expanding this tax cut will help more small businesses and startups advance their current efforts and create the technology of the future." – U.S. Senator Maggie Hassan

It’s important to note that all qualifying work must be conducted within the United States. Research performed by offshore teams or foreign contractors does not count toward the credit.

Eligibility Requirements for Startups

Startup Qualification Criteria

To use the R&D credit to offset payroll taxes, your startup must meet the Qualified Small Business (QSB) criteria. This requires your gross receipts to be under $5 million for the current taxable year. Additionally, you cannot have had any gross receipts during the five years leading up to the current taxable year.

This setup allows startups to claim credits even before generating profits. If your business is still in its early years and remains under the $5 million gross receipts threshold, you may be eligible to start reducing payroll taxes right away. The next step is ensuring your R&D activities align with the IRS’s specific requirements.

The IRS Four-Part Test

Beyond meeting the gross receipt limits, your R&D activities must pass the IRS’s four-part test. Each business component – whether it’s a product feature, process, or software module – needs to be evaluated individually.

1. Qualified Purpose: Your research should aim to develop or improve a business component in terms of functionality, performance, reliability, or quality. The improvement doesn’t have to be groundbreaking. As Capstan Tax Strategies explains, “The research activity doesn’t have to be groundbreaking – it might just be the next small step in an evolution, and that still satisfies Part #1”.

2. Elimination of Uncertainty: You need to show that your efforts focused on resolving uncertainty about the capability, method, or design of your component. Essentially, you must prove that you didn’t know from the start whether your approach would succeed or how to achieve your goal.

3. Process of Experimentation: At least 80% of your research activities must involve a systematic process, such as trial and error, modeling, simulation, or hypothesis testing. This "substantially all" rule is critical – vague claims won’t qualify.

4. Technological in Nature: Your research must be rooted in hard sciences like computer science, engineering, biological sciences, or physical sciences. Fields like psychology or sociology don’t meet the criteria.

A real-world example highlights the importance of meeting these standards. In March 2023, the U.S. Court of Appeals denied Little Sandy Coal Company, Inc. R&D credits for designing 11 first-in-class vessels. The court ruled against them because they couldn’t prove that "substantially all" of their activities involved a process of experimentation. The ruling made it clear that generalized claims of uncertainty, novelty, or arbitrary time estimates don’t meet the requirements.

If your entire project doesn’t meet the test, you can apply the "shrink-back" rule by breaking the project into smaller components to find qualifying elements. For example, while a complete software platform might not qualify, a specific algorithm or security feature within it might.

Keep detailed records of your process, including the initial technical uncertainties, the alternatives you considered, and the systematic methods you used. These records will be essential if the IRS reviews your claim.

How to Document R&D Activities and Expenses

Required Documentation

Keeping detailed records of your R&D activities and expenses is essential to back up your claims, ensuring accuracy and readiness for any audits. You need to demonstrate both the technical work performed and the costs directly tied to it. This involves two main types of documentation: activity-based records, which explain what you did and how you conducted your experiments, and cost-based records, which track the money spent on qualifying activities.

For personnel costs, gather W-2 forms, payroll registers, timesheets, and job descriptions. If an employee spends 80% or more of their time on qualifying research, their entire wages may qualify under the "substantially all" rule. For contractors, keep signed contracts (dated before the research starts), 1099 forms, and invoices, remembering that typically only 65% of contractor costs are eligible.

When it comes to supply expenses, hold onto receipts and invoices for materials used directly in research, like prototyping materials or testing supplies. Be aware that expenses like travel, meals, and administrative costs are not eligible. For the technical side, retain project plans, design specs, testing logs, meeting notes, and records of failures or adjustments. As Specialty Tax Group points out, "If documentation feels overly generic, it raises concerns quickly."

Starting with the 2026 tax year, you’ll need to report each business component on Form 6765, Section G. This means keeping detailed records for each product feature, process, or software module you claim. According to Brown Plus, "making the connection between the cost and the QRA [Qualifying Research Activity] is critical for meeting IRS requirements."

By following these steps, you’ll create a strong foundation for accurate and defensible credit claims.

Record-Keeping Best Practices

Keeping records in real time is crucial to avoid potential audit issues. The IRS has made it clear: "The Service does not have to accept estimates of qualified research expenses if documentation exists to verify the actual amount of such expenses."

Set up a dedicated folder for each project, including both technical records (highlighting uncertainties and testing) and financial records (tracking labor and material costs). Use time-tracking software to assign employee hours to specific R&D tasks, rather than relying on broad estimates. Keep your records for five to seven years, even though the standard statute of limitations is three years, to cover any credits carried forward. For contractors, ensure agreements clearly define their work and the associated risks.

Finally, make sure your technical narratives align with your financial records. This consistency not only strengthens your claim but also simplifies the audit process if questions arise later on.

sbb-itb-ba0a4be

Calculating and Filing Your R&D Tax Credit Claim

How to Calculate Your Credit

The R&D tax credit typically falls between 6% and 10% of your qualifying research expenses (QREs). To determine your credit, you’ll need to calculate it using two methods: the Regular Research Credit and the Alternative Simplified Credit (ASC).

- Regular Research Credit: This equals 20% of your current-year QREs that exceed a base amount, which is calculated using your historical gross receipts.

- Alternative Simplified Credit (ASC): This equals 14% of your current-year QREs that exceed 50% of your average QREs from the prior three years. If you’re a startup without prior-year QREs, the ASC provides a flat 6% credit on current-year expenses.

Your QREs can include various expenses, such as wages for R&D employees and supervisors, supplies directly used in research, computer rental or cloud hosting costs, and 65% of contract research expenses (contractor costs are capped at 65%).

To avoid increasing your taxable income, make a Section 280C election on Form 6765. If you qualify as a Qualified Small Business (gross receipts under $31 million and no revenue for more than five years), you can apply up to $500,000 annually toward payroll taxes – this is split equally between Social Security and Medicare taxes.

Once you’ve calculated your credit, you’ll need to follow the appropriate filing process.

Forms and Filing Process

After determining your credit, you’ll need to file the correct forms. Use Form 6765 alongside your original income tax return (e.g., Form 1120 for C-Corporations, Form 1120-S for S-Corporations, or Form 1065 for partnerships). This form calculates your credit and lets you choose whether to apply it against income tax or payroll tax. Note: You must elect the payroll tax offset on your original return – it cannot be added later via an amended filing.

If you’re claiming the payroll tax offset, submit Form 8974 quarterly with your employment tax return, usually Form 941. Keep in mind that you can only start using the payroll credit in the first quarter after filing your income tax return with the Form 6765 election.

"Importantly, there is no lump sum payment option available… This is only able to be refunded in the form of credits for the payroll tax that the QSBs pay".

Starting with the 2025 tax year, you’ll need to complete Section G of Form 6765 to break down QREs by business component – unless you’re a Qualified Small Business or your total QREs are $1.5 million or less with gross receipts at or below $50 million. If you’re running short on time to gather your documentation, filing a tax extension can help. Missing the filing deadline could mean losing the credit for that year entirely.

Tips for Startup Founders

Writing Clear Activity Descriptions

When documenting your projects, aim for concise, straightforward narratives that explain the technical challenges you faced and the experiments you conducted. The IRS isn’t looking for technical jargon – they want to understand your process in plain English.

To ensure your work aligns with the four-part test, focus on these key areas: describe the technical problem you tackled, highlight why the solution wasn’t obvious, explain the alternatives you considered, and detail why you chose your final approach. For instance, instead of vaguely stating, "performed engineering work on the platform", you could say, "developed a caching layer to reduce database query time by 70%, testing three algorithms before selecting Redis with custom TTL logic." This level of detail not only strengthens your claim but also complements your broader record-keeping efforts.

Stick to activities that clearly meet the four-part test – routine bug fixes or cosmetic updates won’t qualify. It’s better to submit a focused, well-supported claim than to include standard feature updates that could raise audit flags. For example, a seed-stage SaaS startup documented three qualifying projects by linking sprint notes and ticket histories. This approach helped them identify $480,000 in qualified research expenses and secure a $52,000 tax credit.

If the thought of detailed documentation feels overwhelming, consider seeking professional help to ensure no qualifying expenses slip through the cracks.

Working with Tax Professionals

If you’re struggling to manage documentation on your own, a tax professional can simplify the process. They can identify overlooked qualifying expenses – like cloud computing or contractor costs – and help ensure your claim stands up to IRS scrutiny.

When selecting a specialist, prioritize those with relevant industry experience. Many offer a free scoping session to estimate your potential credit before you commit. Additionally, confirm they provide audit defense and will stand by their documentation if your claim is reviewed by the IRS. Modern consultants often integrate tools like Jira or GitHub into their platforms, automating much of the data collection process. This makes documentation a byproduct of your workflow rather than an extra task.

Despite over $32 billion in R&D credits being reported in 2021, fewer than 33% of eligible companies actually claimed them. By working with a professional, you can ensure you capture all eligible expenses while staying focused on building your business.

Conclusion

R&D tax credits offer a powerful way for startups to support innovation while improving cash flow. Surprisingly, fewer than 30% of eligible small businesses take advantage of this opportunity. If your company is creating new products, refining processes, or tackling technical challenges, you could be leaving significant savings on the table.

Start by applying the IRS Four-Part Test to identify qualifying activities, and make it a habit to document expenses as they occur. Linking costs directly to specific projects, as outlined earlier, is key to maximizing your claim.

Federal credits can refund 6% to 14% of every dollar spent on qualified research, creating a meaningful financial boost. With 36 states offering additional incentives, the potential savings multiply even further. And don’t worry if your startup isn’t profitable yet – unused credits can be carried forward for up to 20 years, ensuring they remain valuable as your business grows.

Think of this as an ongoing effort rather than a one-time task. As Greg O’Brien, CPA at Anomaly CPA, explains:

"R&D tax credits for startups work best when they are treated as a year-round process tied to how you build, not a one-time form at tax time”.

If your qualified research expenses exceed $100,000, consider consulting a specialist to ensure your claim is both accurate and optimized for the full benefit.

These credits are designed to reward innovation – don’t miss the chance to claim what you’ve earned.

FAQs

Do I qualify if I already have some revenue?

Yes, your startup can qualify for R&D tax credits even if it’s generating revenue. The key factor is whether your business is involved in qualified research activities – not whether you’re pre-revenue. If your company is working on innovation that fits the required criteria, you could still be eligible to claim these credits.

What startup activities don’t count as R&D?

Activities that fall outside the scope of R&D are those that lack a focus on technological progress or scientific challenges. Examples include tasks like land development, routine data collection, market research, quality control, and administrative work. Similarly, activities that don’t involve experimentation are not considered R&D. Additionally, projects financed through grants or classified as "funded research" may be excluded, especially if they don’t aim to achieve technological progress.

What documents should I keep in case of an IRS audit?

When filing for an R&D tax credit, detailed documentation is key. Essential records include:

- Project Descriptions: Clearly outline the research activities and objectives.

- Time Tracking Records: Log hours spent on qualifying research activities.

- Invoices and Expense Reports: Keep receipts and financial records related to eligible expenses.

These documents aren’t just helpful – they’re critical if the IRS audits your claim. Staying organized and maintaining thorough records ensures you’re compliant and prepared to substantiate your credit.