When raising money for a startup, choosing the right funding structure is critical. The three most common options are SAFE notes, convertible notes, and equity financing. Each works differently:

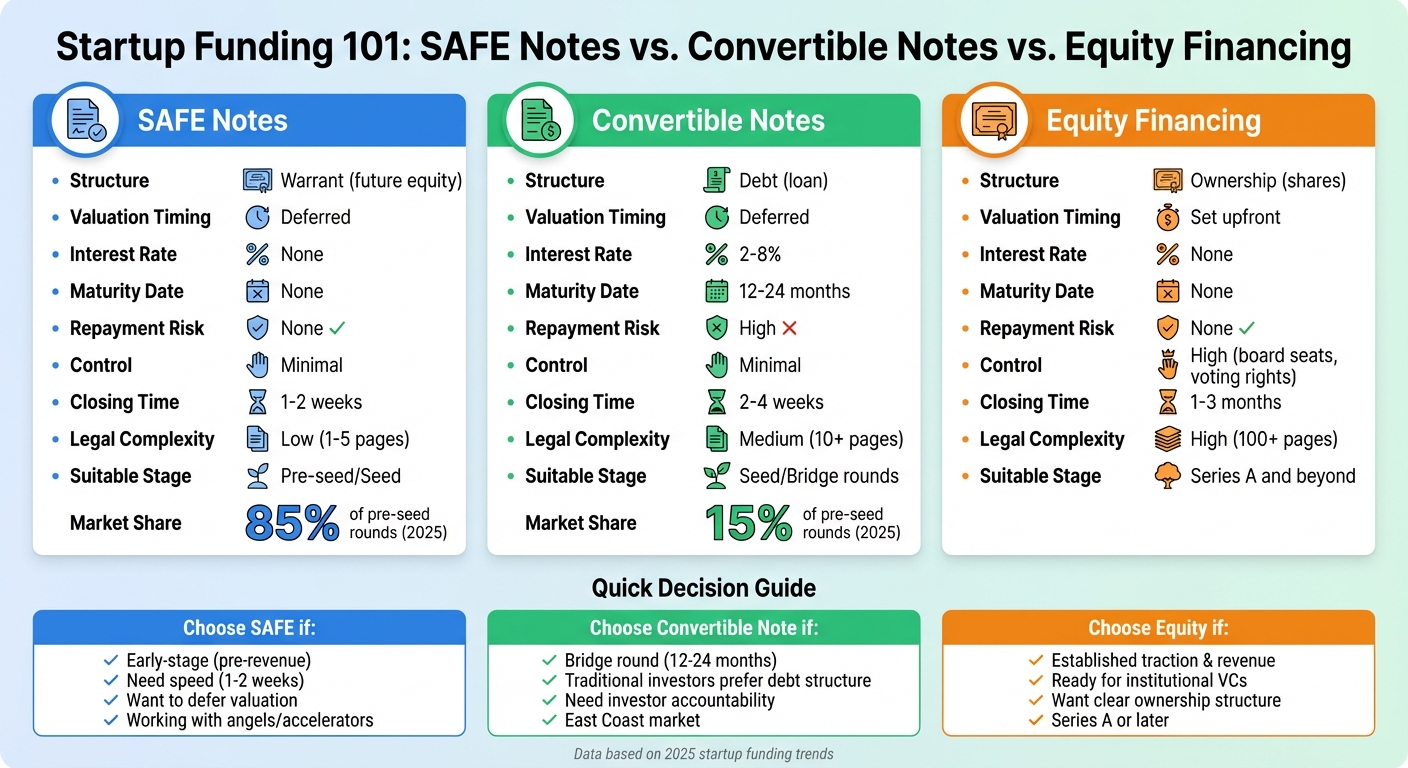

- SAFE Notes: Simple agreements for future equity without debt or immediate ownership. Popular for their speed and simplicity, they dominate early-stage funding (85% of pre-seed rounds in 2025).

- Convertible Notes: Short-term loans that convert to equity later, carrying interest (2%-8%) and a maturity date. Often used in bridge rounds.

- Equity Financing: Selling shares at a set valuation, granting investors ownership and control. Common in later stages like Series A.

Quick Comparison

| Feature | SAFE Note | Convertible Note | Equity Financing |

|---|---|---|---|

| Structure | Warrant (future equity) | Debt (loan) | Ownership (shares) |

| Valuation Timing | Deferred | Deferred | Set upfront |

| Interest Rate | None | 2%-8% | None |

| Maturity Date | None | 12-24 months | None |

| Repayment Risk | None | High | None |

| Control | Minimal | Minimal | High |

| Closing Time | 1-2 weeks | 2-4 weeks | 1-3 months |

Key Takeaways:

- Use SAFEs for early-stage funding when speed and simplicity matter.

- Opt for convertible notes in bridge rounds with clear timelines.

- Choose equity financing when your startup is established and ready for institutional investors.

Each option has trade-offs, so align your choice with your startup’s stage and goals.

What Are SAFE Notes?

A SAFE (Simple Agreement for Future Equity) is a financial agreement that allows investors to exchange their initial investment for equity in a company during a future financing round or a liquidity event. Introduced by Y Combinator in 2013, SAFEs were created to simplify early-stage fundraising by eliminating the complexities associated with debt-based instruments.

With a SAFE, investors provide funds upfront in exchange for the right to convert their investment into shares when the company raises its next "priced round", such as a Series Seed or Series A. Unlike convertible notes, SAFEs are not considered debt. This means there’s no obligation to repay the investment if the company doesn’t raise another round or takes a different approach to fundraising.

SAFEs have become the go-to tool for early-stage funding. As of 2025, 85% of pre-seed rounds use SAFEs, making them a dominant choice, especially in Silicon Valley and fast-moving industries like AI, machine learning, and consumer apps, where speed and simplicity are crucial.

Grasping these fundamentals helps explain why SAFE notes are so appealing to early-stage founders.

Key Features of SAFE Notes

SAFEs are popular for their straightforward and founder-friendly structure. The documents are typically concise, spanning just 1–5 pages, compared to the 10+ pages often required for convertible notes. This simplicity translates into faster funding rounds – startups using SAFEs can close deals about 30% faster than those pursuing traditional equity financing.

Some key features of SAFEs include:

- No debt obligations, interest rates, or maturity dates: There’s no repayment requirement, and conversion happens automatically during the next equity financing round or a liquidity event, such as an acquisition or IPO.

- Valuation cap and discount rate: These terms are designed to protect early investors. The valuation cap sets the maximum company valuation at which the SAFE converts, ensuring investors receive more equity if the company’s valuation exceeds the cap. The discount rate (commonly 15%–25%) offers early investors a reduced share price compared to new investors in the next round.

In 2025, 61% of SAFEs use a "Valuation Cap Only" structure, while 30% combine a "Valuation Cap + Discount".

The "Post-Money SAFE", introduced in 2018, has become the standard, accounting for 85% of all SAFEs issued. This version allows investors to lock in a specific ownership percentage at the time of signing. While this provides clarity for investors, it can lead to higher dilution for founders, especially if multiple SAFEs are issued before the next priced round.

Pros and Cons of SAFE Notes

SAFEs come with both benefits and trade-offs, depending on the needs of the startup and its investors.

Advantages:

- Speed and cost efficiency: SAFEs are quick to execute, often closing within 1–2 weeks, and they typically reduce legal fees by about 15% compared to priced equity rounds.

- No debt classification: Since SAFEs aren’t debt, they don’t appear as liabilities on a company’s balance sheet, which can be helpful for future borrowing or financial ratios.

- Flexibility in valuation: SAFEs allow startups to delay the complex process of determining their valuation until a later stage, when they’ve gained more traction and data.

Challenges:

- Dilution uncertainty: Founders may face unexpected equity loss, especially if multiple SAFEs with varying valuation caps are issued.

- No repayment pressure: For investors, the absence of a maturity date means there’s no obligation for the company to repay the investment if another round isn’t secured.

- Limited control for investors: SAFE holders don’t typically gain voting rights or board seats until their investment converts to equity, reducing their influence in the early stages.

"SAFEs provide a flexible, efficient, and founder-friendly way for startups to raise early capital without the baggage of traditional debt-based agreements." – Allied Venture Partners

To avoid surprises, founders should use cap table tools to model the potential dilution caused by multiple SAFEs upon conversion. It’s also wise to stick to Y Combinator’s standard templates. If the document doesn’t include the standard YC footer language, a legal review can help identify any modifications. Lastly, avoid setting a valuation cap too low just to close a deal quickly, as this can result in excessive equity loss later on.

sbb-itb-ba0a4be

What Are Convertible Notes?

Convertible notes combine the simplicity of SAFEs with debt-like features that offer additional investor protections. At their core, a convertible note is a short-term loan that converts into equity – typically preferred shares – when a specific event occurs, such as a future priced funding round or the sale of the company.

"Convertible notes are a type of loan that gives investors the right to convert their debt into equity at a predetermined event." – AngelList Team

Before SAFEs gained traction, convertible notes were the go-to fundraising tool for startups. By 2025, they still accounted for about 15% of pre-seed rounds. They’re especially common in bridge rounds, often used in industries like biotech and hardware, and in East Coast markets like New York and Boston, where they appear in roughly 50% and 40% of rounds, respectively.

What sets convertible notes apart from SAFEs is their inclusion of features like interest rates (usually 2%–8% annually), maturity dates (typically 12–24 months), and a repayment obligation if the note doesn’t convert.

"The presence of the maturity date gives convertible note holders more leverage than SAFE holders." – Mark Tyson, Founding Partner, TKN Tyson

For example, Peter Thiel’s $500,000 convertible note in Facebook converted into a 10.2% equity stake after a Series A round valued the company at around $100 million.

These features make convertible notes a unique fundraising option, and it’s worth diving deeper into how they work.

Key Features of Convertible Notes

Convertible notes are built on several key components that aim to balance protections for both investors and founders:

- Principal: The original amount invested, which later converts into equity.

- Interest Rate and Maturity Date: Interest accrues annually (typically 2%–8%) and converts into additional equity rather than being paid out in cash. Maturity dates are generally set 12–24 months from issuance, marking the deadline for conversion or repayment.

- Valuation Cap: A negotiated upper limit (e.g., $5M–$30M) on the company’s valuation for conversion purposes, protecting early investors from excessive dilution.

- Discount Rate: Typically 15%–25%, giving early investors a reduced share price in the next funding round.

- Conversion Trigger: A qualifying event, such as raising $1M or more, that automatically converts the debt into equity.

- Balance Sheet Classification: Until conversion, convertible notes are listed as liabilities, which can influence financial ratios and borrowing capacity.

To avoid unnecessary dilution, founders should set realistic valuation caps that align with expectations for the next funding round.

Pros and Cons of Convertible Notes

Convertible notes come with a mix of benefits and challenges, each influencing how founders and investors approach this fundraising tool.

Advantages:

- Investor Protection: As debt instruments, convertible notes take precedence over SAFEs and equity in liquidation scenarios, ensuring noteholders are paid first in the event of a sale or bankruptcy.

- Interest Accrual: Interest that converts into additional equity boosts the return for early investors.

- Simplified Valuation: By deferring valuation until a later stage, startups can raise funds more quickly and with fewer complications compared to priced equity rounds.

Challenges:

- Maturity Date Pressure: Founders must carefully manage maturity dates to avoid being forced into repayment if a priced round isn’t on the horizon.

- Balance Sheet Impact: Classified as liabilities, convertible notes can affect financial ratios and limit future borrowing options.

- Conversion Risks: If the “qualified financing” threshold is set too high relative to the capital raised, the note may not convert, leaving the startup with outstanding debt.

"Convertible notes are like an IOU – investors give you upfront cash in the form of debt, which accrues interest, and has a maturity date." – Lighter Capital

To sidestep maturity date challenges, founders should closely monitor deadlines and, if needed, negotiate extensions or updated conversion terms well in advance. This proactive approach can help mitigate potential risks and ensure smoother transitions to equity.

What Is Equity Financing?

Equity financing, often referred to as a priced round, involves selling shares of your company to investors at a set price per share, based on an agreed-upon valuation. Unlike SAFEs or convertible notes, this method establishes your startup’s valuation upfront, clearly defining investor ownership from the start. For example, if you raise $5 million on a $20 million pre-money valuation, investor ownership is immediately determined at that moment.

Once the fundraising documents are signed, the investors officially become part-owners of your company, with specific rights tied to their shares. Equity financing is generally used in later-stage funding rounds – such as Series A and beyond – when a startup has shown clear growth and traction. By 2025, while SAFEs dominated early-stage funding (accounting for 85% of pre-seed rounds), equity financing had become the standard for startups seeking institutional investment. However, this approach is more involved, often taking months to finalize and requiring significant legal fees due to the detailed due diligence process.

"A traditional equity financing forces a company to set a valuation at the worst possible time… [it] punts the valuation down the line to the time of a traditional equity financing – when the company is likely to have a resilient basis upon which to establish a positive valuation." – Louis Lehot, Attorney, Foley & Lardner LLP

Equity financing provides a clear ownership structure, which is essential for startups preparing to secure institutional backing.

Key Features of Equity Financing

In equity financing, new shares are issued immediately, which reduces the ownership percentages of existing shareholders. These rounds typically involve a lead investor who plays a central role in negotiating terms and overseeing due diligence. Lead investors often gain voting rights and board representation, giving them influence over major decisions.

Before pursuing equity financing, startups need to ensure their capitalization table and financial records are in order. The process includes creating detailed term sheets that define governance structures, liquidation preferences, and protective provisions. Additionally, priced rounds usually trigger the conversion of any existing SAFEs or convertible notes into equity.

These elements highlight both the opportunities and challenges that come with equity financing.

Pros and Cons of Equity Financing

Advantages:

- Defined Ownership Structure: Investors know exactly how much of the company they own from the outset, avoiding the ambiguity of convertible instruments.

- No Debt or Interest Payments: Unlike loans, equity financing doesn’t require repayment, and investors often bring strategic guidance and industry connections.

- Investor Engagement: Voting rights and board representation ensure investors are aligned with the company’s long-term success.

Challenges:

- Cost and Complexity: The process can be lengthy and expensive due to the extensive legal and financial requirements.

- Ownership Dilution: Issuing new shares reduces the percentage of ownership held by current shareholders.

- Loss of Control: Granting voting rights and board seats gives investors a voice in decision-making.

- Valuation Risks: Establishing an upfront valuation can be tricky, especially for companies without a proven track record, potentially leading to less favorable terms.

To minimize dilution, it’s crucial to plan how existing SAFEs or convertible notes will convert during the priced round. Additionally, adjusting your employee option pool to match near-term hiring needs can help preserve founder equity.

SAFE Notes vs. Convertible Notes vs. Equity: Side-by-Side Comparison

To help you navigate the differences between these funding options, here’s a straightforward side-by-side comparison.

Feature Comparison Table

The table below highlights key distinctions across SAFE notes, convertible notes, and equity financing:

| Feature | SAFE Note | Convertible Note | Equity Financing |

|---|---|---|---|

| Legal Structure | Warrant (Right to Equity) | Debt (Loan) | Ownership (Shares) |

| Valuation Timing | Deferred to future round | Deferred to future round | Set upfront |

| Interest Rate | None | 2-8% | None |

| Maturity Date | None | 18-24 months | None |

| Repayment Risk | None | High (debt repayment required) | None |

| Control/Governance | Minimal (No board seats) | Minimal (No board seats) | High (Board seats, voting rights) |

| Dilution Timing | At next priced round | At next priced round | Immediate |

| Legal Complexity | Low (1-5 pages) | Medium (10+ pages) | High (100+ pages) |

| Closing Time | 1-2 weeks | 2-4 weeks | 1-3 months |

| Suitable Stage | Pre-seed / Seed | Seed / Bridge rounds | Series A and beyond |

As seen above, SAFE notes are quick and simple, often closing in just weeks. Convertible notes take a bit longer, while equity financing requires significantly more time and legal work.

"SAFEs provide speed and simplicity, appealing to founders seeking minimal complexity. Convertible notes offer stronger investor protections but introduce debt-related risks." – Tyler Seals, Partner, Smith Pauley LLP

Pros and Cons Comparison Table

Here’s a breakdown of the advantages and drawbacks of each instrument to help you decide which one aligns with your goals:

| Instrument | Pros | Cons |

|---|---|---|

| SAFE Note | Quick to close (1-2 weeks), low legal costs, no debt obligations, no maturity deadlines | Lacks investor protections, potential for unexpected dilution in later rounds |

| Convertible Note | Familiar to many investors, offers interest as a reward for early risk, maturity date encourages next funding round | Risk of repayment at maturity, interest adds to dilution, creates debt on the balance sheet |

| Equity | Establishes clear valuation, attracts institutional investors, no debt or interest obligations | Expensive legal fees, lengthy process, immediate dilution, and potential loss of control through board representation |

Each option serves a different purpose depending on your startup’s stage. Consider your current needs and future goals to determine the best fit. Avoid treating these instruments as interchangeable – they each come with distinct trade-offs.

When to Use Each Funding Option

Selecting the right funding option depends on where your startup stands, how quickly you need capital, and the type of investors you’re working with. Each option is tailored for different situations, and using the wrong one could lead to unnecessary costs, delays, or loss of ownership.

SAFE Notes for Early-Stage Funding

SAFEs are ideal when your startup is still in its infancy – pre-revenue or just beginning to gain traction. If you’re not ready to set a formal valuation, SAFEs allow you to postpone that decision until you have solid metrics to back it up. In fact, by 2025, 85% of pre-seed rounds used SAFEs, making them the go-to choice for early-stage fundraising.

One of the biggest advantages of SAFEs is their speed. They typically close in just 1–2 weeks, letting founders quickly shift their focus back to building their product. Joshua Ismin, Co-founder & CEO of Psylo, shared his experience:

"I was surprised at how quickly a round came together using SAFEs… it just made the process templated, quick, and seamless."

SAFEs are especially suited for angel investors or accelerators who value simplicity over complex creditor protections. Over 85% of startups raising less than $1 million choose SAFEs instead of priced equity rounds. Unlike convertible notes, SAFEs don’t come with interest rates, maturity dates, or repayment obligations, which reduces financial strain during your startup’s most fragile phase. However, dilution can become a concern – multiple SAFE rounds with varying caps can significantly impact ownership. Using a cap table simulator is a smart way to model these scenarios.

Next, let’s look at convertible notes, a flexible option for startups aiming to hit specific milestones before a major funding round.

Convertible Notes for Bridge Rounds

Convertible notes are designed for short-term funding between major investment rounds. If your startup needs a 12–24 month runway to reach key milestones before a Series A, convertible notes offer a clear timeline for conversion. These notes typically mature in 18–24 months and carry annual interest rates of 2–8%.

For startups seeking interim capital, convertible notes fit seamlessly into a growth strategy. They are particularly appealing to traditional investors, especially on the East Coast, where familiarity with debt-like protections is common. For instance, in New York, the funding split is about 50% SAFEs and 50% convertible notes, while in Silicon Valley, SAFEs dominate with over 95% usage. If your investors are less comfortable with SAFEs, convertible notes provide a structure they’re more likely to understand.

However, this option comes with a trade-off: debt obligations. If your startup doesn’t reach a conversion event before the note matures, you may face repayment pressure or have to renegotiate terms. Louis Lehot, Partner at Foley & Lardner LLP, explains:

"A SAFE has an infinite duration, so they convert only when there is an opportunity to do so… At some point, convertible notes have to be dealt with, so that founders are accountable to investors".

This accountability can be a double-edged sword – it can push you to hit milestones but can also become a burden if your timeline extends unexpectedly.

When your startup achieves predictable revenue and traction, equity financing becomes the logical next step.

Equity Financing for Established Startups

Once your startup has established traction and a steady revenue stream, equity financing becomes the best fit. This option is typically used at Series A and beyond, when institutional venture capital firms step in. These firms expect formal valuations, board seats, and voting rights in exchange for their investment, making equity financing a structured and strategic choice.

The process, however, is more time-consuming, often taking 2–6 months to close, and involves significant legal costs. But the payoff is clarity. Both founders and investors know exactly what they own, and you gain long-term partners who can offer strategic guidance alongside their capital. As Fidelity Private Shares notes:

"The priced round, however, is highly-structured and provides startups with true investment partners".

Don’t rush into equity financing too early. Setting a valuation before you have meaningful data can backfire, locking you into a price that may lead to a down round later. Waiting until you have solid metrics allows you to negotiate from a stronger position.

Conclusion

Deciding on the right funding structure is a pivotal choice for any founder. SAFEs stand out for their speed and simplicity, often closing within 1–2 weeks without adding debt to your balance sheet. It’s no wonder they’re used in 85% of pre-seed rounds as of 2025. Convertible notes, on the other hand, come with interest rates typically between 2% and 8%, along with maturity dates ranging from 18 to 24 months, making them a solid option for bridge rounds. Equity financing, though more time-intensive and complex, provides clarity and sets the stage for long-term partnerships once your startup has shown traction and revenue.

Choosing the wrong structure can lead to unnecessary pressure and ownership dilution. For instance, convertible notes include a "ticking clock", requiring you to raise capital or face repayment. Similarly, entering a priced equity round too early – before establishing strong metrics – can lock in a lower valuation, potentially leading to higher dilution later. Tyler Seals, Partner at Smith Pauley LLP, explains:

"SAFEs provide speed and simplicity, appealing to founders seeking minimal complexity. Convertible notes offer stronger investor protections but introduce debt-related risks."

A solid legal foundation is key to being investment-ready. This includes having a properly registered entity, compliant records, and organized documentation. Services like BusinessAnywhere can help simplify this process, offering U.S. business registration starting at $0 (plus state fees), along with registered agent services, automated compliance tools, and a virtual mailbox with unlimited scanning. These tools allow you to manage your business professionally from anywhere.

Ultimately, your funding structure should match your startup’s stage, timeline, and investor expectations. SAFEs work best when quick closings are essential and revenue is still in its early stages. Convertible notes are ideal for bridging rounds until you hit critical milestones. Equity financing, meanwhile, is suited for startups with strong traction that can support a higher valuation.

FAQs

What’s the difference between SAFE notes and convertible notes for startup funding?

SAFE notes and convertible notes serve similar purposes but differ in structure, offering distinct advantages to founders and investors.

SAFE notes (Simple Agreements for Future Equity) are exactly what they sound like – simple. They grant investors the right to receive equity in the company at a future date, typically during a subsequent funding round. Unlike traditional loans, SAFEs don’t accrue interest, lack a maturity date, and don’t require repayment. This simplicity makes them a go-to option for startups that need quick funding without the added stress of repayment terms or deadlines.

Convertible notes, however, operate more like a loan that can convert into equity. They usually come with an interest rate (commonly 5–8%) and a maturity date, often set within 12–24 months. If the note doesn’t convert by that maturity date, the startup might need to repay the investor. While this structure offers investors added protection, it introduces more complexity for founders, particularly if repayment becomes an issue.

To sum it up, SAFEs are quicker and easier for founders, while convertible notes provide more safeguards for investors. Choosing between the two depends on your startup’s current stage, funding goals, and what your investors are looking for.

When should a startup consider equity financing?

When a startup reaches a point where its valuation can be clearly established – often during a priced round – it’s time to consider equity financing. This stage typically comes after hitting major milestones like consistent revenue generation, building a loyal customer base, or showcasing strong growth potential.

Equity financing works well when a company is ready to exchange ownership shares for capital. It’s a solid option for startups aiming to secure significant funding and bring on board long-term investors who share the company’s vision and growth goals.

How can startup founders minimize dilution when raising multiple SAFE rounds?

To reduce dilution during multiple SAFE rounds, founders can adopt a few smart strategies. Start by negotiating valuation caps and discount rates carefully for each round. This ensures that early investors don’t end up owning a disproportionately large share of the company when their SAFEs convert. Opting for post-money SAFEs can also be a game-changer, as they clearly outline the exact ownership percentage that will be diluted upon conversion.

Another approach is to space out SAFE rounds or set firm limits on the total amount raised through SAFEs. This helps avoid excessive dilution before transitioning to a priced equity round. Keeping an up-to-date cap table is equally important – it allows you to track ownership changes and make well-informed decisions during fundraising. Lastly, open communication with investors and meticulous planning around conversion terms are essential for striking a balance between raising capital and protecting ownership stakes.