How much is your startup worth? That’s the question every founder needs to answer before raising funds. Startup valuation isn’t just about numbers – it’s about showing investors what your company could achieve. Here’s the core idea:

- Pre-money valuation is your company’s worth before investment.

- Post-money valuation adds the investment amount to pre-money valuation, determining equity split.

For early-stage startups, valuation depends on team strength, market potential, and future growth, not past revenue. Too high a valuation can scare investors; too low dilutes your ownership.

Key Methods to Value Startups

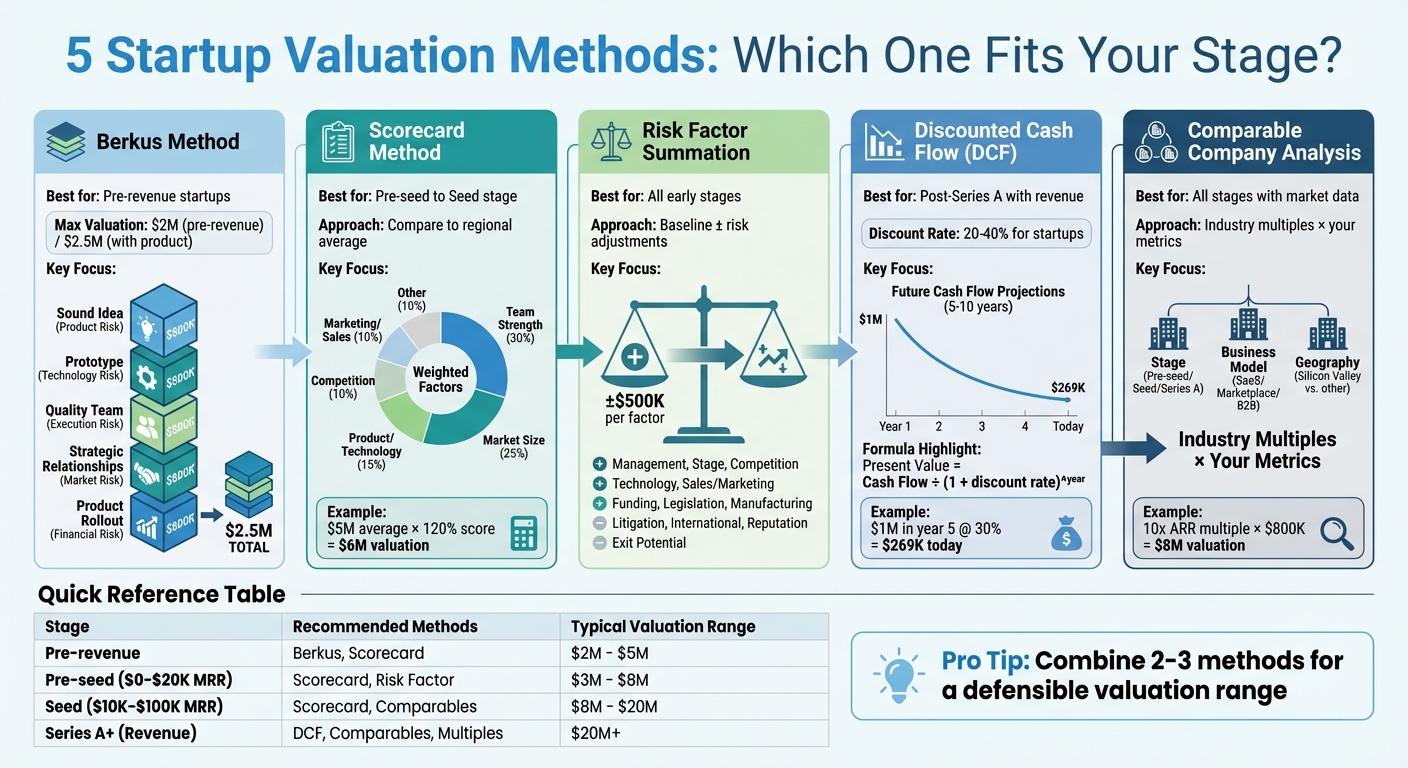

- Berkus Method: Assigns value to factors like team, prototype, and product rollout (max $2.5M for pre-revenue startups).

- Scorecard Method: Compares your startup to peers, adjusting based on factors like market size and product strength.

- Risk Factor Summation: Adjusts a baseline valuation for 12 risks (e.g., competition, sales, reputation).

- Discounted Cash Flow (DCF): Projects future cash flows, discounted for risk (best for revenue-generating startups).

- Comparable Company Analysis: Uses metrics from similar companies to estimate your valuation.

Tools and Tips

- Use platforms like Equidam or Carta to calculate valuation and manage equity.

- Blend 2–3 methods for a defensible range (e.g., $4M–$5M).

- Prepare a pitch deck with key financials and milestones.

Your valuation isn’t just a number – it’s a story backed by data. Focus on realistic benchmarks, avoid overinflated projections, and align your valuation with your growth stage.

5 Methods for Valuing Startups

5 Startup Valuation Methods Comparison by Stage and Focus

Here are five practical ways to assess your startup’s value. Each method caters to specific stages and types of startups, and combining them can lead to a more comprehensive valuation. These approaches are designed to prepare you for meaningful conversations with potential investors.

The Berkus Method

The Berkus Method is perfect for pre-revenue startups, where financial projections are often unreliable. Instead of speculative forecasts, this approach assigns monetary value to five key factors that help reduce risks.

Each factor can contribute up to $500,000 to your startup’s valuation:

- Sound Idea: Reduces product risk.

- Prototype: Mitigates technology risk.

- Quality Management Team: Addresses execution risk.

- Strategic Relationships: Lowers market risk.

- Product Rollout or Sales: Reduces financial risk.

The total valuation typically caps at $2 million for pre-revenue startups and $2.5 million for those with a product rollout.

| Success Factor | Risk Mitigated | Max Value Added |

|---|---|---|

| Sound Idea | Product Risk | $500,000 |

| Prototype | Technology Risk | $500,000 |

| Quality Management Team | Execution Risk | $500,000 |

| Strategic Relationships | Market/Competitive Risk | $500,000 |

| Product Rollout or Sales | Financial/Production Risk | $500,000 |

This method is tailored for startups aiming to exceed $20 million in revenue by year five. To make a strong case, provide evidence such as letters of intent or detailed resumes of your team.

"Valuation is ultimately about storytelling backed by evidence. The Berkus method gives you both the story structure and the evidence framework to make your case convincingly".

Scorecard Valuation Method

The Scorecard Method starts with the average valuation for startups in your region and stage, adjusting it based on how your startup compares across several factors. These include:

- Team Strength (30%)

- Market Size (25%)

- Product or Technology (15%)

- Competitive Environment (10%)

- Marketing and Sales Channels (10%)

- Need for Additional Investment (5%)

- Other Considerations (5%).

For instance, if the average pre-seed valuation in your area is $5 million and your startup scores 120% compared to peers, your valuation could be $6 million. This method works well for U.S.-based startups, where regional benchmarks are well-documented. The key is being honest about your strengths and weaknesses relative to similar companies.

Risk Factor Summation Method

This approach builds on a baseline valuation, often determined by another method like Berkus or Scorecard, and adjusts it based on 12 specific risk factors. Each factor can increase or decrease the valuation by up to $500,000.

The 12 risk categories include:

- Management

- Stage of the business

- Legislation/political risk

- Manufacturing risk

- Sales and marketing risk

- Funding/capital raising risk

- Competition risk

- Technology risk

- Litigation risk

- International risk

- Reputation risk

- Potential for a lucrative exit

If a risk is lower than average, it adds value; if higher, it subtracts value. This method highlights your startup’s strengths and vulnerabilities, helping you address investor concerns more effectively.

Discounted Cash Flow (DCF) Analysis

DCF focuses on projecting your startup’s future cash flows (typically over 5–10 years) and discounting them to their present value using a rate that reflects your venture’s risk. For startups, this discount rate is usually high – between 20% and 40% – to account for the likelihood of failure.

The calculation for each year’s present value is simple: divide the projected cash flow by (1 + discount rate) raised to the power of the year. For example, $1 million in projected cash flow five years from now, discounted at 30%, is worth around $269,000 today. Additionally, you estimate a "Terminal Value", which represents the company’s worth at the end of the forecast period, often based on exit multiples.

"DCF’s strength lies in its focus on future growth potential and your smart evaluation of future risk".

This method is most effective for post-Series A startups with steady revenue and a clear growth trajectory. For earlier-stage startups, the uncertainty of projections can make DCF less reliable on its own.

Comparable Company Analysis

This method evaluates your startup based on similar companies in the same industry, stage, and region. By identifying valuation multiples – like revenue multiples for SaaS companies or user-based metrics for consumer apps – you can apply these to your own metrics.

Key criteria for finding comparable companies include:

- Stage of Development: Pre-seed, seed, or Series A.

- Business Model: B2B SaaS, marketplace, consumer app, etc.

- Geography: A Silicon Valley startup may have a different valuation than one in a smaller market.

For example, if similar seed-stage SaaS companies are valued at 10x annual recurring revenue and your ARR is $800,000, your valuation would be approximately $8 million. This approach anchors your valuation in real market data, making it easier to justify to investors familiar with your industry.

Each of these methods offers valuable insights into your startup’s worth. Using a combination of approaches can help you build a stronger case for investors.

Tools and Resources for Startup Valuation

Once you’ve chosen your preferred valuation methods, the right tools can simplify the process and strengthen your case with investors. Here’s a breakdown of the most effective options for early-stage startups.

Startup Valuation Calculators

Equidam stands out by offering five valuation methods, including DCF and Venture Capital, to create investor-ready reports in less than an hour. Since its launch in 2013, over 140,000 businesses worldwide have used Equidam, collectively raising more than $5 billion in funding. A survey from the past two years revealed that 94% of investors gave positive feedback on Equidam’s reports.

"Equidam is a fantastic tool. It gave me confidence in my two valuations. It helped us set a solid pre-money, and we actually over-subscribed our round." – Sarah Kitlowski, President & COO, Omeza

Founder Shield‘s Startup Valuation Calculator is another option, offering specific models based on your startup stage. For instance, the Berkus Method suits pre-revenue startups, while Market Comps work better for established sectors. Venture Calculator is a free, browser-based tool that requires no signup, making it ideal for modeling funding rounds, dilution, and cap tables without the risk of sharing sensitive data. Meanwhile, the Eton Venture Services Calculator provides quick estimates using methods like Venture Capital and DCF, with a focus on industries such as SaaS and Fintech.

The trick is to match the tool to your startup’s stage. For idea-stage startups, the Berkus Method is a good fit. Pre-seed or seed-stage companies might benefit from the Scorecard method, while businesses with at least 12 months of steady revenue can leverage DCF. To present a well-rounded valuation, choose tools that combine multiple methodologies rather than relying on a single figure. Beyond calculators, managing equity details is just as important, which brings us to cap table solutions.

Cap Table and Compliance Tools

Managing equity and compliance is critical, and Carta is a go-to platform for this purpose. It handles cap tables, regulatory compliance, and equity management efficiently. For example, Carta can calculate fully diluted shares, including preferred and restricted stock, which is essential for determining ownership percentages and share prices. It also tracks post-money valuations from earlier funding rounds, providing a foundation for current discussions.

Cap table tools also allow for dilution modeling, helping you see how new investments will affect ownership before making decisions. A clear and accurate cap table not only reflects your current status but also signals transparency and preparedness, making investor due diligence smoother. This level of detail strengthens your valuation argument and builds trust with potential investors.

It’s important to distinguish between 409A valuations and fundraising valuations. A 409A valuation is used for tax compliance and typically comes in 10-30% lower than a fundraising valuation. While 409A valuations determine the fair market value for employee stock options, fundraising valuations reflect what investors are willing to pay based on future potential.

Business Anywhere Services

In addition to financial tools, ensuring your business structure complies with regulations is essential. Business Anywhere offers services to simplify setup and operations, particularly for digital nomads and early-stage founders.

- Business registration: Starting at $0 plus state fees, this service covers LLC, Corporation, or PLLC formation and includes a free first-year registered agent.

- Registered agent services: Available for $147/year after the first year, these services ensure compliance and help maintain good standing with regulatory agencies.

- Virtual mailbox services: Starting at $20/month, this service provides a professional U.S. address and unlimited mail scanning, which can enhance your operational credibility during investor due diligence.

For those working remotely, the Digital Nomad Kit is a comprehensive solution. It bundles LLC registration, EIN application, registered agent services, a virtual mailbox, compliance tools, and banking setup. This package ensures your U.S.-based business is ready to attract investors while allowing you to work from anywhere.

sbb-itb-ba0a4be

How to Prepare for Investor Discussions

Once you’ve nailed down your valuation methods, it’s time to focus on how to effectively communicate with investors.

Combining Valuation Methods

Investors often rely on several valuation methods to cross-check their estimates. To stand your ground, approach your valuation by blending 2–3 methods before stepping into any meeting. This strategy not only strengthens your position but also shows you’ve done your homework.

Take Woosung Chun, CFO of DualEntry, as an example. In 2024, he raised funds by combining the Berkus method (focused on team and product traction) with market comparables. On top of that, he used a "milestone" analysis to reverse-engineer a valuation aligned with the capital needed to achieve product-market fit. This calculated approach reassured investors that his numbers were well thought out, not random.

Make sure to stress-test your assumptions. If a small change – say, 10% – completely throws off your valuation, investors will see it as a red flag. Instead, present a range with a 20% bandwidth, such as $4M to $5M, instead of a rigid single figure. Also, align your methods with your startup’s growth stage. Early-stage companies might lean on qualitative methods like the Berkus or Scorecard approach, while more established startups can use data-driven methods like discounted cash flow (DCF) or revenue multiples.

Here’s a quick breakdown of how different methods align with growth stages:

| Method Category | Best Stage | Key Focus |

|---|---|---|

| Qualitative (Berkus, Scorecard) | Pre-Seed / Seed | Team, idea, and milestones |

| Market-Based (Comparables) | All Stages | Similar companies’ raises/exits |

| Quantitative (DCF, Multiples) | Series A / B+ | Cash flows and revenue multiples |

Using a mix of these approaches ensures your valuation feels grounded and credible, setting the stage for a strong pitch.

Creating a Strong Pitch Deck

Your pitch deck is where numbers meet storytelling. Investors want to see hard evidence backing your valuation. Highlight key elements like your management team’s track record (which can influence up to 30% of a scorecard valuation), your Total Addressable Market (TAM), and essential financial metrics, such as Monthly Recurring Revenue (MRR), Customer Acquisition Cost (CAC), and gross margins.

Anchor your valuation as a range – for example, $3M to $5M – and connect it to specific milestones, like reaching $1M in Annual Recurring Revenue (ARR) or acquiring 100,000 users. This strategy keeps you credible while leaving room for negotiation. For reference, in 2024–2025, pre-seed startups with $0–$20K MRR typically see valuations between $3M and $8M. Seed-stage companies with $10K–$100K MRR often land in the $8M to $20M range.

Also, include a clear roadmap showing how the funds will fuel growth. Investors want to see that you’ve calculated the "survival math" – the capital needed to hit the next fundable milestone while only giving up 15–25% equity.

"The founders who survive don’t pick the highest number; they pick the number that keeps them alive long enough to hit their next milestone." – Tim Worstell, Startup Advisor

With your valuation strategy and pitch deck in place, the next step is to strengthen your position with professional support.

Getting Professional Support

External validation can make a big difference, especially for more complex situations like Series A rounds or cap table restructuring. Hiring a fractional CFO or valuation consultant can provide a third-party perspective that investors are less likely to challenge.

These professionals can help you avoid common mistakes, such as "founder optimism", which often leads to overvaluation and risky down rounds. They also ensure you’re benchmarking against the right companies – seed-stage startups shouldn’t compare themselves to unicorns or public companies. For instance, Mikey Moran, CEO of Private Label Extensions, worked with a founder who initially pitched an inflated valuation without solid data. By switching to the Scorecard method and using recent transactions in their niche, the founder attracted more investor interest because the numbers made sense.

"Focus less on a lofty valuation and more on proof points that justify it." – Mikey Moran, CEO, Private Label Extensions

Finally, ensure your business structure is investor-ready. Services like Business Anywhere can simplify compliance tasks, such as registered agent services ($147/year after the first year) or virtual mailbox solutions (starting at $20/month). If you’re a digital nomad or remote founder, the Digital Nomad Kit bundles everything from LLC registration to banking setup, ensuring your U.S.-based business is ready for investor scrutiny.

Conclusion

Key Takeaways

Startup valuation is far from a one-size-fits-all process – it’s a mix of data-driven analysis and persuasive storytelling. The approach you take should align with where your company stands. For pre-revenue startups, methods like the Berkus or Scorecard models focus on qualitative factors. On the other hand, revenue-generating companies can rely on more quantitative approaches, such as discounted cash flow (DCF) or revenue multiples.

Rather than aiming for a single number, use 3–5 valuation methods to test your assumptions and establish a defensible range. Investors generally anticipate dilution of 15% to 25% per funding round, so your valuation should ensure you have enough runway to hit your next milestone – not just aim for the highest possible figure.

"At the earliest stages, you’re not selling future cash flows – you’re selling the credibility of your trajectory." – Woosung Chun, CFO, DualEntry

Stay clear of pitfalls like overly ambitious projections or unrealistic comparisons. Base your valuation on real traction, whether that’s monthly recurring revenue (MRR), user growth, or intellectual property protection. Present your valuation as a range with about 20% bandwidth to show flexibility and realism.

With these principles, you’re ready to turn your valuation strategy into a compelling pitch for investors.

Next Steps for Entrepreneurs

Now that you’ve mastered valuation basics and investor preparation, it’s crucial to ensure your business is ready for scrutiny. Business Anywhere simplifies compliance and administrative tasks, helping you build a strong foundation that reinforces your valuation. Whether it’s registered agent services ($147/year after the first year), a virtual mailbox (starting at $20/month), or the Digital Nomad Kit tailored for remote founders, having a U.S.-based business structure signals operational reliability during due diligence.

Cut through administrative obstacles to keep your fundraising efforts on track. Nail down your valuation, refine your pitch, and ensure your business infrastructure is ready to impress potential investors.

FAQs

What valuation range should I target for my stage?

For startups in their early stages, valuations often fall between $1 million and $10 million. This range depends on factors such as the industry you’re in, the traction you’ve achieved, and how investors perceive your potential. At the seed stage, key metrics like revenue, key performance indicators (KPIs), and the size of your market opportunity play a big role in shaping your valuation. To pinpoint a reasonable valuation range for your startup’s stage and sector, it’s helpful to use a mix of approaches, such as comparing similar companies or applying qualitative evaluations.

How do I pick the best valuation methods for my startup?

Choosing the best valuation method for your startup depends on its stage, the data you have, and the goal of the valuation. If you’re in the early stages, qualitative methods such as the Berkus approach or the Venture Capital method are often more suitable. For startups with established revenue streams or tangible assets, quantitative methods like discounted cash flow (DCF) or comparable company analysis tend to be more effective. In some cases, blending multiple methods can provide a more reliable estimate that reflects where your business currently stands.

How much equity should I give up in a funding round?

When raising funds, the equity you part with hinges on your company’s valuation and the size of the investment. To calculate investor ownership, divide the investment amount by the post-money valuation. For instance, if your company has a $10 million pre-money valuation and you raise $2 million, the post-money valuation becomes $12 million. In this case, investors would own approximately 16.67% of the company.

Founders often work to reduce dilution by negotiating a valuation that reflects both the company’s growth potential and comparable metrics from similar businesses in the market.