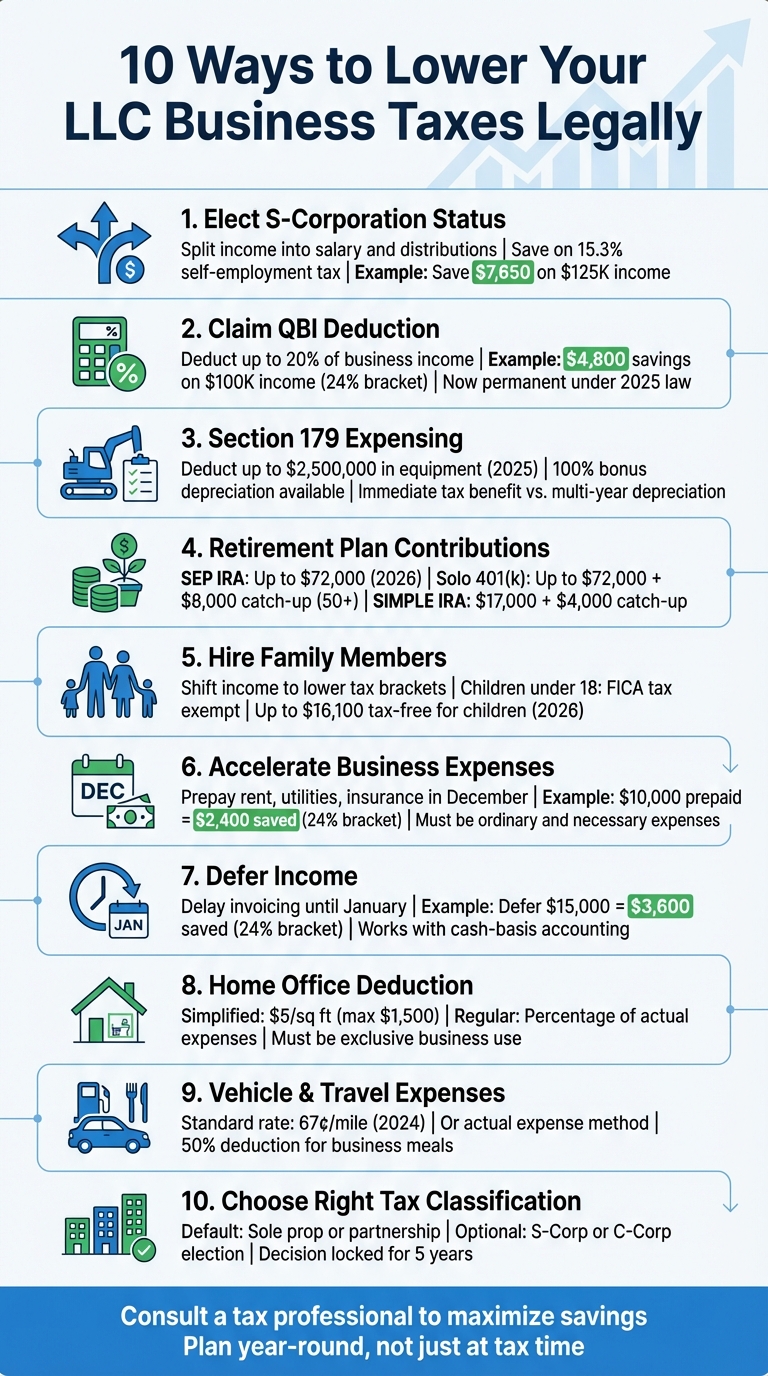

Starting a new LLC? Taxes can feel overwhelming, but with the right strategies, you can save money while staying compliant. Here are 10 proven ways to reduce your tax bill:

- Compare S-Corp vs LLC tax benefits: Split income into salary and distributions to lower self-employment taxes.

- Claim the QBI Deduction: Deduct up to 20% of your business income under Section 199A.

- Use Section 179 Expensing: Deduct the full cost of equipment and software upfront.

- Contribute to Retirement Plans: Lower taxable income by saving for retirement through SEP IRAs or Solo 401(k)s.

- Hire Family Members: Pay family for legitimate work to shift income into lower tax brackets.

- Accelerate Business Expenses: Prepay expenses like rent or supplies to claim deductions sooner.

- Defer Income: Push income to the next year if you expect to be in a lower tax bracket.

- Claim the Home Office Deduction: Deduct expenses for a workspace used exclusively for your business.

- Deduct Vehicle and Travel Costs: Track mileage and travel expenses for business purposes.

- Choose the Right Tax Classification: Select the best IRS classification (e.g., S-Corp) for your LLC to optimize taxes.

These strategies can help you keep more of your earnings while staying compliant with IRS rules. Plan ahead, track expenses, and consult a tax professional to maximize your savings.

10 Tax Strategies to Lower LLC Business Taxes Legally

1. Elect S-Corporation Tax Status

When setting up a new LLC, one of the most effective ways to manage your taxes is by choosing the right tax classification.

Tax Savings Potential

Opting for S-Corp status allows you to split your income between a salary (subject to the 15.3% self-employment tax) and distributions (which are not taxed for Social Security and Medicare). For example, if a single-member LLC earns $125,000 in profit, allocating $75,000 as salary and $50,000 as distributions could save $7,650 in Social Security and Medicare taxes.

"Setting up an LLC and then electing treatment as an S corporation may just give you the best of both worlds – the ease of administration of the LLC and the tax planning opportunities of the S corporation."

- Laura Schmidt, Senior Customer Service Representative, Wolters Kluwer

Compliance with U.S. Tax Laws

The IRS requires S-Corp owners who are also employees to take a "reasonable salary" that aligns with industry standards. To elect S-Corp status, you’ll need to file Form 2553 within two months and 15 days of the start of your tax year (for most businesses, this means by March 15). Other requirements include:

- Your LLC must be a domestic entity.

- You can have no more than 100 shareholders, all of whom must be U.S. citizens or permanent residents.

- Your LLC can only issue one class of stock.

Once your S-Corp status is approved, you’ll need to file Form 1120-S annually and issue Schedule K-1 forms to each owner.

Applicability to LLC Structures

S-Corp status works best for businesses with profits that exceed the owner’s reasonable salary. If your profits are just enough to cover that salary, the costs of payroll and additional tax preparation might outweigh the savings. For those looking to simplify this process, BusinessAnywhere offers an S-Corp Tax Election service for $147, which handles filing Form 2553 – an appealing option for remote entrepreneurs and digital nomads.

Ease of Implementation for New Business Owners

While S-Corp status offers notable tax advantages, it also comes with added responsibilities. You’ll need to set up a payroll system, withhold FICA taxes, and maintain detailed records. If you miss the March 15 deadline, you might qualify for late relief if you can show reasonable cause. Keep in mind that for 2024, only the first $168,600 of earnings is subject to the Social Security portion of the self-employment tax. Consulting a tax professional can help you determine a reasonable salary and ensure you maximize your savings while staying compliant.

This is just one way to reduce your tax burden. Next, we’ll look at how the Qualified Business Income deduction can help you save even more.

2. Claim the Qualified Business Income (QBI) Deduction

The Qualified Business Income (QBI) deduction – outlined in Section 199A – lets eligible LLC owners deduct 20% of their net business income. This tax-saving opportunity is a key strategy for reducing liabilities, especially for new LLC owners. Initially set to expire after 2025, the deduction became permanent through the One Big Beautiful Bill Act in 2025.

Tax Savings Potential

The QBI deduction can make a noticeable difference in your tax bill. For example, if you earn $100,000 and fall into the 24% tax bracket, this deduction could save you around $4,800. The best part? It applies whether you take the standard deduction or itemize your deductions on Schedule A.

For 2026, you can claim the full 20% deduction if your taxable income is below $203,000 (single filers) or $406,000 (married couples filing jointly). If your income exceeds these thresholds, limitations kick in – especially for owners of Specified Service Trades or Businesses (SSTBs), such as law, healthcare, accounting, or consulting.

Compliance with U.S. Tax Laws

Qualified business income refers to your net profit, excluding things like capital gains, interest income, and reasonable compensation. To claim the deduction, use Form 8995 if your income is under the threshold. If your income exceeds the threshold or you operate an SSTB, you’ll need Form 8995-A.

For those earning above the threshold and not operating an SSTB, the deduction is limited to the greater of:

- 50% of W-2 wages paid by the business, or

- 25% of W-2 wages plus 2.5% of the unadjusted basis of qualified property.

However, SSTB owners face stricter rules: the deduction phases out completely once income surpasses $247,301 for single filers or $494,601 for married couples (2025 tax year).

"Now that the QBI deduction has been made permanent, owners of pass-through entities should model multi-year strategies that coordinate reasonable compensation, depreciation timing, and elective SALT/PTET planning to sustain the full 20% benefit over time."

- Ryan Millan, CPA

Applicability to LLC Structures

The QBI deduction applies to all pass-through LLC structures. Whether you run a single-member LLC (disregarded entity), a multi-member LLC (partnership), or an LLC taxed as an S-corporation, the income flows through to your personal tax return, where you can claim the deduction.

To maximize the deduction, consider contributing to a SEP-IRA or Solo 401(k), as these contributions lower your taxable income. If you’re an S-corp owner with income exceeding the threshold, increasing your W-2 wages could help you optimize the wage-based limitation and claim a larger deduction.

Ease of Implementation for New Business Owners

If your income is below the threshold, claiming the QBI deduction is relatively simple – just complete Form 8995 when filing your 1040. However, if your income exceeds the threshold or you’re dealing with SSTB rules, wage limitations, or property considerations, the process becomes more intricate. In these cases, a tax professional can help integrate the QBI deduction with other strategies, like retirement contributions or depreciation planning.

Keep in mind, not all states follow federal QBI rules. For example, states like California, New Jersey, and Pennsylvania may not allow this deduction. Understanding how the QBI deduction fits into your overall tax strategy can help you retain more of your hard-earned business income. Up next, learn how expensing equipment upgrades can further enhance your tax planning.

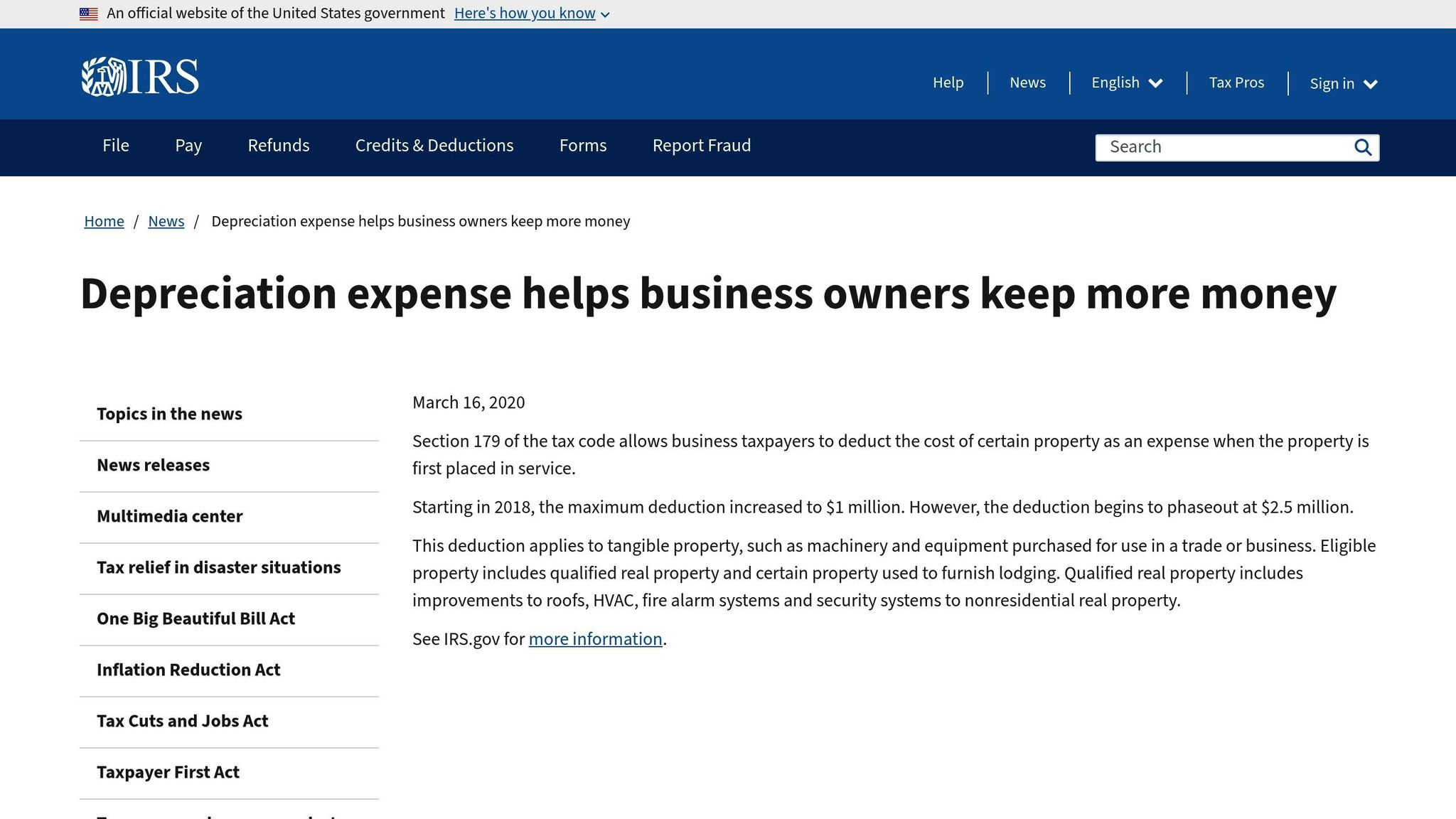

3. Use Section 179 Expensing and Bonus Depreciation

Investing in equipment, software, or vehicles for your business? Section 179 allows you to deduct the full cost of these purchases upfront, offering an immediate tax benefit instead of spreading deductions over years through traditional depreciation.

Tax Savings Potential

For the 2025 tax year, businesses can deduct up to $2,500,000 under Section 179. However, this benefit begins to phase out once total equipment purchases exceed $4,000,000. After reaching the Section 179 limit, you can turn to bonus depreciation, which stands at 100% for qualifying property acquired and placed in service after January 19, 2025. Together, these tools can significantly reduce taxable income.

"Section 179 isn’t just some obscure tax code, it’s a practical tool that can give your business a real financial edge. By letting you deduct the full cost of qualifying purchases right away, it can lower your tax bill and free up cash when you need it most."

- Jacob Dayan, CEO, Community Tax LLC

Compliance with U.S. Tax Laws

Qualifying purchases include machinery, office furniture, computers, off-the-shelf software, and certain building improvements like HVAC systems, fire alarms, and security systems. Even used equipment qualifies, provided it’s new to your business. To take advantage of these deductions, the asset must be used for business purposes at least 50% of the time and placed in service by December 31 of the tax year.

There are a few key differences between Section 179 and bonus depreciation. Section 179 deductions cannot exceed your taxable income and cannot create a loss. On the other hand, bonus depreciation has no income limit and can even create a net operating loss. To claim these deductions, file Form 4562 with your tax return.

Applicability to LLC Structures

Both Section 179 and bonus depreciation apply to all LLC structures. Single-member LLCs report these deductions on Schedule C of Form 1040, while multi-member LLCs use Form 1065, passing deductions to members via Schedule K-1. To maximize your tax savings, apply Section 179 to specific assets first, then use bonus depreciation for additional costs.

Ease of Implementation for New Business Owners

For new business owners, this strategy is manageable with proper record-keeping. Save invoices and receipts that document purchase dates and business use. Keep an eye on your total equipment spending, as the Section 179 benefit phases out when purchases exceed $4,000,000. For vehicles weighing under 6,000 pounds, bonus depreciation is capped at $8,000 for the first year, with a total first-year limit of $20,200. A tax professional can help you coordinate these deductions with other strategies to maximize your savings. Next, let’s explore additional ways to reduce your tax liability.

4. Contribute to Retirement Plans

Setting up a retirement plan not only helps you save for the future but also reduces your tax burden. Contributions to these accounts are tax-deductible, which lowers your taxable income, and your savings grow tax-deferred until you withdraw them during retirement.

Tax Savings Potential

When you contribute to a retirement plan, it directly decreases your taxable income. For 2026, the contribution limits for various plans are as follows:

- SEP IRA: You can contribute up to $72,000 or 25% of your compensation (20% of modified net profit for unincorporated LLCs).

- Solo 401(k): Allows contributions up to $72,000, with an additional $8,000 for individuals aged 50 or older.

- SIMPLE IRA: Permits salary deferrals of $17,000, with a $4,000 catch-up for those 50+.

Small employers with 1–50 employees may also benefit from a tax credit. This credit can cover 100% of qualified startup costs – up to $5,000 annually for three years. An additional $500 per year is available if the plan includes automatic enrollment [36,37].

Applicability to LLC Structures

The right retirement plan often depends on how your LLC is classified for taxes and needs:

- SEP IRA: A flexible option for businesses of any size, easily set up using IRS Form 5305-SEP. However, you must contribute the same percentage of compensation for all eligible employees as you do for yourself.

- Solo 401(k): Best suited for LLC owners with no employees other than a spouse. This plan allows you to contribute as both the employer and employee, maximizing your savings potential [39,40].

- SIMPLE IRA: A practical choice for LLCs with up to 100 employees, offering straightforward setup and lower administrative costs compared to traditional 401(k) plans [39,41].

These plans align well with other tax strategies by reducing taxable income directly.

Ease of Implementation for New Business Owners

Starting a retirement plan is straightforward. For example, you can establish a SEP IRA or Solo 401(k) as late as your LLC’s tax filing deadline, including extensions, and still deduct contributions for the prior year. If you’re a single-member LLC, contributions are typically based on your net self-employment income. For LLCs taxed as corporations, contributions are calculated using W-2 wages.

If your Solo 401(k) account surpasses $250,000 in assets, you’ll need to file Form 5500-EZ to stay compliant. A tax professional can help ensure your retirement contributions are seamlessly integrated into your broader tax plan.

5. Hire Family Members

Hiring family members can be a smart way to manage taxes while staying within the bounds of IRS regulations. By employing family members, you can shift income into lower tax brackets, reducing your overall tax burden.

Tax Savings Potential

In 2026, a child who earns up to $16,100 will owe no federal income tax, and the wages are deductible for the LLC. For example, if you’re in the 24% tax bracket and pay your child $12,000 for legitimate work, you could save around $3,000 in combined taxes.

The benefits don’t stop at income taxes. If you run a single-member LLC or a partnership where both partners are the child’s parents, wages paid to children under 18 are exempt from Social Security and Medicare (FICA) taxes, and wages to children under 21 avoid Federal Unemployment Tax Act (FUTA) taxes. For instance, in February 2026, John Garcia paid his wife $30,000 and his 16-year-old son $10,000. The LLC deducted these wages while avoiding FUTA taxes on his wife’s income and both FICA and FUTA taxes on his son’s pay. His son’s income was also tax-free under the standard deduction.

| Entity Type | Child Under 18 (FICA) | Child Under 21 (FUTA) | Spouse (FUTA) |

|---|---|---|---|

| Single-Member LLC / Sole Prop | Exempt | Exempt | Exempt |

| S-Corp or C-Corp | Required | Required | Required |

Compliance with U.S. Tax Laws

To stay compliant, family members must perform "ordinary and necessary" tasks for the business. Acceptable jobs include managing social media, filing documents, cleaning the office, or data entry. However, personal chores like babysitting or mowing the lawn don’t qualify.

Pay wages that align with what you’d offer a non-family employee for the same work. For example, paying $100 per hour for basic filing would likely catch the IRS’s attention. Maintain a clear paper trail by paying through business checks or direct deposit, keeping detailed timesheets, and issuing W-2 forms at the end of the year. You’ll also need to complete Form I-9 and W-4 for each family member you hire, just as you would for any other employee.

Applicability to LLC Structures

The tax perks depend on whether you choose an LLC vs S Corp for your business classification. Single-member LLCs treated as disregarded entities receive the most benefits, including full FICA and FUTA exemptions for qualifying children. On the other hand, if your LLC is taxed as an S-Corp or C-Corp, you lose these payroll tax exemptions, though wages remain deductible as a business expense.

Employing your spouse can also be advantageous for sole proprietors. Through a Health Reimbursement Arrangement (HRA) or Section 105 plan, you can deduct family medical expenses that wouldn’t otherwise be fully deductible for self-employed individuals. While your spouse’s wages are subject to FICA taxes, they’re exempt from FUTA taxes, saving you 6% on the first $7,000 of wages.

Ease of Implementation for New Business Owners

Getting started is straightforward. Assign tasks that are age-appropriate – children as young as seven can organize files or clean – and document their responsibilities in a written job description and employment agreement. Payroll software like Gusto or QuickBooks can simplify tax filings and generate W-2 forms.

Family members’ earned income can also be used to fund a Roth IRA (up to $7,500 in 2026), helping them build long-term, tax-free savings while staying fully compliant with IRS rules. From here, you can look into ways to accelerate business expenses for even more tax benefits.

6. Accelerate Business Expenses

If you use cash-basis accounting, you can deduct expenses when you pay them, not when they’re incurred. This gives you some control over the timing of your deductions. For instance, paying for January’s rent, utilities, or insurance premiums in December allows you to claim those deductions in the current tax year, reducing your taxable income.

Tax Savings Potential

The numbers can add up fast. Say you’re in the 24% tax bracket and prepay $10,000 in expenses before year-end – things like office supplies, advertising, or professional fees. This could save you around $2,400 in taxes. And if you’re subject to the 15.3% self-employment tax, the savings could be even higher.

For larger purchases, consider using Section 179. This allows you to deduct the full cost of qualifying equipment in the year it’s purchased, which can significantly lower your taxable income.

Compliance with U.S. Tax Laws

Not all expenses qualify for acceleration. The IRS requires that any accelerated expense must be both "ordinary and necessary" for your business. According to the IRS:

"Ordinary means it’s common and accepted in your industry. Necessary means it’s helpful and appropriate for running your business."

Personal expenses – like groceries or a vacation – don’t qualify. Additionally, the 12-month rule governs prepaid expenses. For example, prepaying three months of rent is fine, but prepaying an entire year might force you to spread the deduction over multiple years.

Keep detailed receipts and invoices, and use a business bank account or credit card to create a clear paper trail. This documentation is crucial if the IRS ever audits you. Staying organized not only saves headaches but also aligns with tax strategies that maximize your benefits.

Applicability to LLC Structures

Accelerating expenses is especially useful for LLCs, which are typically pass-through entities. This means deductions directly reduce your personal adjusted gross income (AGI). Whether you’re a single-member LLC, a partnership, or an S-Corp, this strategy can provide timely tax relief. However, if you’re an S-Corp owner, be extra careful to keep business and personal finances separate to avoid complications.

| Expense Type | Method | Tax Impact |

|---|---|---|

| Office Supplies | Bulk purchase in December | Deduct the total cost immediately |

| Rent/Utilities | Prepay upcoming bills | Lowers taxable income for the current year |

| Insurance | Pay annual premium in full | Deduct the full amount in the same year |

| Equipment | Use Section 179 expensing | Deduct full purchase price (up to $1,310,000 limit) |

Ease of Implementation for New Business Owners

As the year wraps up, take stock of your business needs for the first quarter of the next year. Things like office supplies, software subscriptions, or marketing materials can often be prepaid. Planning to upgrade equipment? Make sure to buy and start using it before December 31 to benefit from Section 179 expensing.

Accounting software can simplify tracking and categorizing these expenses. You might also want to look into deferring income as part of your broader tax strategy. Always consult a CPA to confirm which expenses qualify and avoid potential audit issues. By timing your expenses wisely, you can lower your taxable income now while setting yourself up for further tax advantages in the future.

sbb-itb-ba0a4be

7. Defer Income to Later Tax Years

Deferring income is a smart way to delay reporting revenue, helping to reduce your tax burden in the current year. This approach works particularly well if you expect to drop into a lower tax bracket next year or if you’re trying to avoid bumping into a higher bracket after a year of high earnings. Essentially, it’s about timing your income to align with your overall tax strategy for your LLC.

Tax Savings Potential

Here’s an example to illustrate: if you’re in the 24% federal tax bracket and decide to defer $15,000 in income from December to January, you could save around $3,600 in federal taxes for the current year. Add the 15.3% self-employment tax to that, and your total savings could approach $6,000. That extra cash could be reinvested into your business or used elsewhere.

Timing is everything when it comes to deferring income. If your LLC uses cash-basis accounting – common for small businesses with annual gross receipts under $25 million – you only report income when it’s actually received in your bank account. For instance, sending invoices late in December instead of earlier can push payments into January, effectively deferring the tax obligation tied to that income.

Compliance with U.S. Tax Laws

The IRS has strict guidelines on when income becomes taxable. The "constructive receipt" rule is key here: you can’t simply hold onto a check received in December and claim it as January income. As tax expert Lana Dolyna, EA, CTC explains:

"The federal tax system doesn’t let LLC owners simply ‘skip’ paying taxes for a year, but it does offer structured ways to delay when income is recognized."

For example, if you receive payment in December – via check, wire transfer, or credit card – it counts as taxable income for that month, even if you don’t deposit it right away. For larger transactions, installment sales under Section 453 allow you to spread the tax impact over several years, reporting only a portion of the gain as payments come in. This makes income deferral a flexible tool for managing your overall taxable income.

Applicability to LLC Structures

Most LLCs operate as pass-through entities, meaning that deferring income at the business level also delays the personal income tax you’ll owe on those profits. Whether you’re a single-member LLC or part of a multi-member partnership, this strategy can be effective.

For LLCs taxed as S-corporations or multi-member partnerships, there’s an additional option: electing a fiscal year under Section 444. This allows you to close your tax year up to three months before December 31 – say, on September 30. Late-year income is then reported on the following calendar year’s return. However, this election often requires a deposit payment to the IRS under Section 7519, which serves as a non-interest-bearing offset for the tax benefit.

Ease of Implementation for New Business Owners

If you’re new to this, start by reviewing your invoicing schedule for November and December. Delaying non-urgent invoices until January 1 can shift taxable income into the next year. It’s a simple yet effective adjustment.

Another way to defer income is by maximizing your retirement contributions. For example, contributing to a SEP-IRA or Solo 401(k) not only reduces your current taxable income but also defers taxes on that income until you withdraw it during retirement. For 2024 and 2025, the contribution limit is up to $69,000.

Keep in mind that state rules may differ from federal ones. Some states require income to be reported on a calendar-year basis, even if you’ve elected a fiscal year at the federal level. As Lana Dolyna advises:

"Deferring income tax works best when both federal and state line up, so plan in consultation with a tax advisor who knows your state’s rules."

Pair income deferral with other strategies, like tax deductions and write-offs, to optimize your tax position and keep more money in your pocket.

8. Claim the Home Office Deduction

Running your LLC from home? The home office deduction can help cut down your tax bill. It allows you to deduct part of your housing costs – whether you rent or own – based on the area you use solely for business purposes. The key here is exclusivity: the space must be used only for work-related activities.

Tax Savings Potential

There are two ways to calculate this deduction: the simplified method or the regular method.

- The simplified method is straightforward: multiply your office’s square footage by $5 (capped at 300 square feet for a maximum deduction of $1,500). It’s easy and doesn’t require extensive recordkeeping – just measure your office space and do the math.

- The regular method can provide greater savings if your home expenses are high. Here, you calculate the percentage of your home used for business and apply that percentage to costs like mortgage interest, property taxes, utilities, insurance, and repairs. For example, if your home office occupies 15% of a 2,000-square-foot home, you can deduct 15% of eligible expenses. Plus, direct expenses like painting your office are fully deductible.

| Feature | Simplified Method | Regular Method |

|---|---|---|

| Calculation | $5 per sq. ft. (max 300 sq. ft.) | Percentage of actual home expenses |

| Max Deduction | $1,500 | Unlimited (subject to business income) |

| Recordkeeping | Minimal; no receipts needed | Extensive; requires receipts |

| Depreciation | Not allowed | Required and must be calculated |

| Carryover | No carryover of excess expenses | Excess expenses can carry forward |

One thing to note: your total home office deduction can’t exceed your LLC’s gross income. If your eligible expenses surpass your income, you can carry the excess forward to future tax years under the regular method.

Compliance with U.S. Tax Laws

The IRS has clear guidelines for what qualifies as a home office. It must be your principal place of business, meaning it’s where you handle your most critical tasks or spend the majority of your business hours. For instance, even if you meet clients at various locations, you can still qualify if you handle all your administrative duties – like billing, scheduling, or bookkeeping – from home.

There are exceptions, too. If your home is the only fixed location for your wholesale or retail business, you can deduct inventory storage costs without meeting the exclusive-use rule. Similarly, licensed daycare facilities can also benefit from this deduction. As always, keeping accurate records is essential to make the most of this opportunity.

Applicability to LLC Structures

The process for claiming this deduction depends on your LLC’s tax structure:

- Single-member LLCs taxed as sole proprietorships use Form 8829 for the regular method or report the square footage on Schedule C for the simplified method.

- Multi-member LLCs taxed as partnerships report unreimbursed home office expenses on Schedule E.

- LLC owners electing S-corporation status and receiving a W-2 cannot claim the home office deduction on their personal tax return. This is something to weigh when deciding on your tax classification.

Getting Started

To begin, measure your home office space and calculate its percentage of your total home square footage. Compare the simplified and regular methods to see which gives you a better deduction. For the regular method, make sure to track all home-related expenses throughout the year.

Even if your office is in a separate structure, like a detached garage or studio, it’s still eligible for the deduction as long as it’s used exclusively for business – even if it’s not your primary workspace. Paying attention to these details can help you maximize your tax savings.

9. Deduct Vehicle and Travel Expenses

Keeping a close eye on your vehicle and travel expenses can significantly lower your tax bill. If you use your car for business purposes – like meeting clients, attending conferences, or visiting job sites – you can deduct those costs. The IRS offers two ways to claim these deductions: the standard mileage rate or the actual expense method. For 2024, the standard mileage rate is 67 cents per mile. This rate includes costs like gas, oil, insurance, and depreciation, so you don’t need to save every receipt. On the other hand, the actual expense method allows you to deduct the business-use portion of all your vehicle expenses – such as repairs, tires, registration fees, and lease payments – but it requires detailed records.

Tax Savings Potential

The best method for you depends on your situation. The standard mileage rate works well for frequent drivers with average costs, while the actual expense method is better suited for those with high repair bills or pricier vehicles. Don’t forget: parking fees and tolls for business trips are deductible, too.

Travel expenses extend beyond just your car. If you travel away from your "tax home" – the area where your main business operates – for an overnight stay or longer, you can deduct costs like airfare, train tickets, rideshare fares, lodging, and 50% of meal expenses. Other deductible items include dry cleaning, laundry, and business-related phone calls during your trip. However, commuting between your home and regular workplace is considered personal and isn’t deductible. By carefully tracking these expenses, you can ensure you’re capturing all eligible deductions.

Compliance with U.S. Tax Laws

To qualify for deductions, expenses must be considered both "ordinary and necessary" for your business and not overly extravagant. Accurate records are critical. For vehicle deductions, keep a mileage log that notes the date, destination, business purpose, and miles driven. If you choose the actual expense method, save all receipts and invoices for costs like gas, repairs, and insurance.

"The law requires that you substantiate your expenses by adequate records or by sufficient evidence to support your own statement."

– Internal Revenue Service

If you opt for the standard mileage rate, you must make that choice in the first year the vehicle is used for business. While you can switch to the actual expense method in later years, you can’t go back to the mileage rate afterward. Inflated vehicle expense claims are a common issue leading to unpaid taxes, so precise documentation is essential.

Ease of Implementation for New Business Owners

Tracking mileage has never been easier, thanks to apps like MileIQ or Everlance, which can automatically log trips and store receipts digitally. These tools help you separate business and personal travel effortlessly. If you use your vehicle for both purposes, you’ll need to calculate expenses based on the percentage of business miles driven. For tax filing, single-member LLCs report these deductions on Schedule C, while multi-member LLCs use Form 1065. Staying organized from the start will save you a lot of stress when tax season rolls around.

10. Select the Right Tax Classification When You Form Your LLC

Picking the right tax classification is a crucial step in setting up your LLC. This decision impacts your tax planning strategies, like S-Corp election and expense acceleration, and lays the groundwork for long-term benefits. Since your initial classification with the IRS is locked in for 60 months (five years), it’s important to make the right choice from the start.

Applicability to LLC Structures

The IRS doesn’t treat all LLCs the same. By default, single-member LLCs are classified as "disregarded entities", meaning they’re taxed like sole proprietorships. In this case, you report business income and expenses on your personal tax return using Schedule C. For multi-member LLCs, the default classification is as a partnership, where each member reports their share of profits on their personal tax returns.

However, you’re not stuck with the default. You can choose to be taxed as an S Corporation by filing Form 2553 or as a C Corporation by filing Form 8832. Each option has its own tax rules, administrative requirements, and ownership restrictions.

"Think of your LLC as a legal container for your business operations; its tax classification determines how its income is taxed." – Allied Tax Advisors

For example, S Corporations are limited to 100 shareholders, all of whom must be U.S. citizens or residents. C Corporations, on the other hand, face double taxation – profits are taxed at a 21% corporate rate and again when distributed as dividends. For many new LLC owners, the choice often boils down to sticking with the default pass-through structure or electing S Corporation status to reduce self-employment taxes. This decision ties into other tax strategies to maximize savings.

Tax Savings Potential

Your tax classification can have a big impact on your bottom line. Under the default pass-through structure, you’ll pay 15.3% in self-employment taxes on all net profits. This rate includes 12.4% for Social Security (applicable to the first $160,200 of earnings in 2024) and 2.9% for Medicare. By electing S Corporation status, you can limit self-employment taxes to only your "reasonable salary", while the rest of your profits (taken as distributions) avoid these taxes. S Corporation status typically becomes advantageous once your net income exceeds $60,000 consistently.

Pass-through owners also benefit from the Qualified Business Income (QBI) deduction, which allows you to deduct up to 20% of your net business income. This deduction was made permanent under the One Big Beautiful Bill Act, signed on July 4, 2025. For higher earners, the deduction may be limited by the W-2 wages paid. Electing S Corporation status can help here, as paying yourself a salary generates the necessary W-2 wages. In this way, the right tax classification complements other strategies like the QBI deduction and income deferral.

Ease of Implementation for New Business Owners

While selecting your tax classification is straightforward, timing is critical. To elect S Corporation status for the current tax year, you must file Form 2553 within two months and 15 days of the start of your tax year or the date your LLC was formed. If you miss this window, you’ll need to either wait until the next tax year or request late election relief by providing a reasonable cause for the delay.

Keep in mind that opting for corporate status comes with added administrative responsibilities. You’ll need to set up formal payroll, file separate tax returns (like Form 1120-S for S Corporations), and maintain stricter records. Additionally, not all states automatically recognize federal tax elections. For example, California imposes an $800 annual franchise tax on LLCs and S Corporations, regardless of their federal status. Before making any changes, consult a tax professional to ensure the tax savings outweigh the extra administrative workload.

If you’re forming your LLC through BusinessAnywhere, you can add S-Corp Tax Election filing for $147 as part of your setup. This ensures Form 2553 is submitted accurately and on time.

Conclusion

You’ve now walked through 10 practical strategies to help lower your business taxes. But here’s the thing – effective tax planning isn’t just a once-a-year task. It’s something that requires attention throughout the year. Many of these strategies, like setting up retirement plans or making an S-Corporation election, come with strict deadlines that often hit well before tax season. For example, ensuring retirement plans are in place by year-end is crucial to maximizing your deductions.

When you take a proactive approach to tax planning, it doesn’t just reduce your tax liability – it can fuel your business’s growth. The difference between scrambling during tax season and planning ahead can be huge. In fact, year-round planning has been shown to save small business clients an average of $47,000 annually. As SDO CPA wisely points out:

"Tax planning happens in October, not April. Year-end scrambles leave money on the table".

This kind of forward-thinking transforms taxes from a dreaded obligation into a tool for boosting profitability and improving cash flow.

Working with a qualified tax professional can make a world of difference. While tax planning services typically cost between $1,500 and $5,000 depending on complexity, the potential savings often far outweigh the expense. A professional can help you navigate tricky areas like entity classifications, model financial scenarios, and ensure compliance with new regulations, such as the Beneficial Ownership Information Report under the Corporate Transparency Act. Missteps – like misclassifying employees, claiming incorrect deductions, or missing key elections – can lead to audits or penalties that cost far more than professional fees.

To get the most out of these strategies, review your business’s tax classification to see if an S-Corporation election makes sense. Use accounting software to meticulously track expenses, and keep your records well-organized all year. Schedule a tax planning session with your CPA or advisor by October to implement strategies like Section 179 equipment purchases, retirement contributions, or income deferral. Redirect the money you save into growing your business and building long-term financial security.

Keep in mind that tax laws are always changing. For instance, the One Big Beautiful Bill Act introduced major updates, such as permanently reinstating 100% bonus depreciation and raising the Section 179 limit to $2.5 million for 2025 and 2026. Staying consistent with these strategies will help secure lasting financial benefits for your LLC.

FAQs

When should I elect S-corp status for my LLC?

If electing S-corp status for your LLC helps lower your tax burden, it might be the right move. This is often beneficial if you can pay yourself a reasonable salary and reliably take at least $20,000 in annual distributions, particularly when your net earnings reach $60,000 or more. Always consult with a tax professional to make sure this decision fits your business goals and meets IRS requirements.

Will my state allow the QBI deduction and bonus depreciation?

Your state’s tax laws might not match federal rules when it comes to the QBI deduction or bonus depreciation. Since state conformity can differ, it’s crucial to check your state’s specific regulations. When in doubt, reaching out to a tax professional can help clarify your eligibility.

What records do I need to prove deductions if I’m audited?

To support your deductions during an audit, make sure to maintain detailed records of every business transaction and expense. This means holding onto receipts, invoices, bank statements, credit card statements, and any other relevant documents. Keeping these records organized is key to demonstrating that your expenses are both ordinary and necessary for your business operations.