Expanding your business internationally? Tax treaties can save you from paying taxes twice on the same income. These agreements decide whether taxes are applied by your home country or the country where your business operates.

Key points to know:

- Double Taxation Relief: Treaties reduce or eliminate taxes like the U.S.’s standard 30% withholding rate on dividends, interest, and royalties.

- Permanent Establishment (PE): You’re taxed in a foreign country only if you have a significant business presence there (e.g., an office or factory).

- Residency Tie-Breakers: If two countries claim you as a tax resident, treaties use tests (like where you live or work most) to resolve conflicts.

- Forms You’ll Need: Filing the right forms (e.g., W-8BEN, 8833) is mandatory to claim treaty benefits and avoid penalties.

Important Updates:

- The U.S.-Chile tax treaty began in 2024, while the U.S.-Hungary treaty ended the same year.

- Federal treaties don’t apply to state taxes, so you may still owe state income tax.

Understanding and leveraging tax treaties ensures compliance and reduces your tax burden. Always consult a tax professional for guidance.

What Are Tax Treaties?

U.S. Tax Treaty Withholding Rates: Standard vs. Treaty-Reduced Rates

Tax treaties are agreements between two countries that establish rules for taxing income earned across borders. These agreements determine how taxing rights are divided between the country where the income is earned and the taxpayer’s country of residence. The United States, for instance, has tax treaties with over 60 countries.

These treaties clarify which country has the right to tax specific types of income. For example, they might state that business profits are only taxable in your home country unless you maintain a physical office abroad. Similarly, they often reduce the standard 30% U.S. withholding tax on income like dividends, interest, and royalties.

"A U.S. tax treaty (also called a tax convention or double taxation agreement) is a bilateral agreement between the United States and another country that establishes rules for taxing income that crosses borders." – Mike Wallace, CEO, Greenback Expat Tax Services

For international entrepreneurs, these treaties simplify tax planning and encourage cross-border business by creating predictable tax outcomes. IRS data from 2016–2021 highlights this benefit: 62% of Americans filing from abroad reported owing $0 in federal taxes after applying exclusions and credits. Let’s explore how these treaties work to eliminate double taxation.

How Tax Treaties Prevent Double Taxation

Tax treaties eliminate double taxation through two main methods. The Exemption Method allows one country to waive its right to tax specific income, while the Credit Method lets both countries tax the income but provides a credit to avoid exceeding the higher tax rate. For example, if you’re a U.S. resident earning business profits in Germany without a permanent establishment there, Germany would exempt that income from taxation.

Another key feature is the concept of permanent establishment (PE). A country can only tax business profits if you have a fixed place of business there, such as an office or warehouse. Treaties also settle dual residency disputes using tie-breaker rules based on factors like your permanent home, habitual residence, and nationality. These mechanisms form the backbone of treaty provisions that benefit international entrepreneurs.

Key Provisions in U.S. Tax Treaties

U.S. tax treaties include several provisions that are especially relevant for international entrepreneurs. One major provision states that business profits are exempt from U.S. tax unless you have a permanent establishment in the U.S., defined as maintaining a fixed place of business for at least six months.

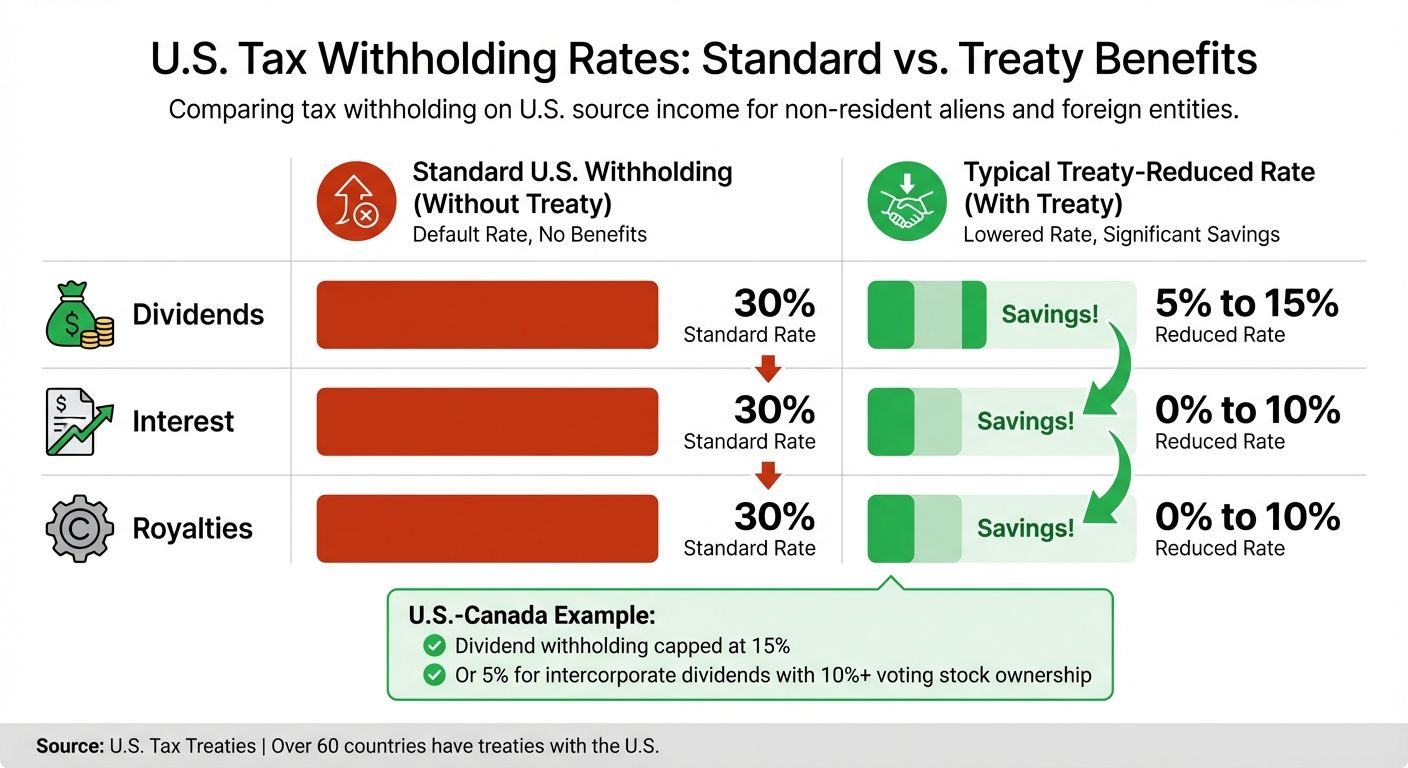

Another important benefit is reduced withholding rates. The table below shows how treaties lower the standard 30% U.S. withholding tax:

| Income Type | Standard U.S. Withholding | Typical Treaty-Reduced Rate |

|---|---|---|

| Dividends | 30% | 5% to 15% |

| Interest | 30% | 0% to 10% |

| Royalties | 30% | 0% to 10% |

For example, under the U.S.-Canada treaty, dividend withholding is capped at 15%, or even 5% for intercorporate dividends when the parent company owns at least 10% of the voting stock.

To prevent treaty shopping – where companies set up in treaty countries solely to benefit from lower tax rates – Limitation on Benefits (LOB) provisions ensure that only qualified residents can claim treaty advantages.

Most U.S. treaties also include a Saving Clause, which allows the U.S. to tax its citizens and residents as if the treaty didn’t exist. However, exceptions apply for specific income types, such as pensions, Social Security benefits, and certain capital gains.

"The Saving Clause reserves (or ‘saves’) the US government’s right to tax you on your worldwide income as if the treaty didn’t exist." – Katelynn Minott, CPA & CEO, Bright!Tax

The definition of permanent establishment varies by country. For instance, Canada has a "Services PE" rule: if you provide services in Canada for 183 days or more within a 12-month period for the same project, or if over 50% of your revenue comes from services performed there, you’re considered to have a PE. On the other hand, countries like Belgium and Germany rely on more traditional definitions, focusing on fixed locations like offices or factories.

Understanding these provisions can help you structure your international business operations to reduce tax obligations. It’s essential to identify which treaty articles apply to your situation and ensure you meet all documentation requirements to take full advantage of these benefits.

Tax Residency and Tie-Breaker Rules

Tax treaties rely on residency tests and tie-breaker rules to ensure benefits are allocated fairly and to avoid conflicts between countries.

How Tax Residency Is Determined

You could end up being a tax resident in two countries at the same time. For instance, spending enough days in France might make you a French tax resident, while holding a U.S. green card automatically qualifies you as a U.S. tax resident, no matter where you live.

The U.S. taxes its citizens and green card holders on their worldwide income. Meanwhile, many countries use the 183-day rule – spend more than half the year there, and you’re considered a tax resident.

When dual residency occurs, tax treaties use tie-breaker rules to decide which country gets to treat you as a resident for treaty purposes. These rules don’t change domestic tax laws but determine which country’s treaty benefits you can claim.

Settling Dual Residency Disputes

Tie-breaker rules follow a step-by-step process to resolve dual residency conflicts. Here’s the typical order:

| Tie-Breaker Hierarchy | Determination Criteria |

|---|---|

| 1. Permanent Home | The country where you have a dwelling available to you at all times. |

| 2. Center of Vital Interests | The country where your personal and economic ties are stronger. |

| 3. Habitual Abode | The country where you spend more time overall. |

| 4. Nationality | The country where you hold legal citizenship. |

| 5. Mutual Agreement | A decision made by the "competent authorities" of both countries. |

Each test is applied only if the previous one doesn’t resolve the issue.

The permanent home test examines whether you have a home continuously available – not a hotel or short-term rental, but a place you can access anytime. If you have homes in both countries, the focus shifts to your center of vital interests, which looks at factors like where your family lives, where you work, and where your investments are located.

If these factors are evenly balanced, the habitual abode test considers your overall pattern of presence over time, rather than a simple day count for a single year. If the conflict remains unresolved, your nationality determines your residency. For dual nationals, the final step involves a mutual agreement between the countries’ tax authorities.

"The most frequent error I encounter is the assumption that the treaty tie-breaker is a simple hierarchy that ‘automatically’ resolves residency by counting days. In reality, the tests proceed in a specific order, require detailed evidence, and may yield ambiguous outcomes." – Prof. Chad D. Cummings, CPA, Esq., Cummings & Cummings Law

If the tie-breaker rules determine you’re a resident of another country for treaty purposes, you’re generally treated as a nonresident alien for U.S. tax calculations. To claim this, you must file Form 1040-NR and attach Form 8833 (Treaty-Based Return Position Disclosure).

However, be aware that many U.S. states don’t follow federal tax treaties and may still tax you as a resident based on their own rules. Also, the Saving Clause in most U.S. treaties allows the U.S. to tax its citizens as if the treaty didn’t exist, which might limit your relief even after a tie-breaker determination. These tests aim to create consistency when applying treaty benefits.

How to Claim Treaty Benefits

Once you’ve figured out your tax residency and the treaty that applies to you, the next step is to claim your benefits. This involves submitting the right forms to your withholding agent and informing the IRS about your treaty position. Here’s a breakdown of the process to help you navigate it effectively.

Required Forms and Documentation

The forms you need depend on the type of income you’re earning and whether you’re filing as an individual or an entity. These forms must be submitted to the withholding agent – the person or company paying you – before any payments are made. If you don’t provide the proper documentation, the withholding agent is legally required to withhold tax at the full statutory rate, which is normally 30% for most U.S.-sourced income.

To qualify for a reduced withholding rate, you’ll need to provide a Taxpayer Identification Number (TIN) (either U.S. or foreign) and certify that:

- You are a resident of a treaty country.

- You are the beneficial owner of the income.

- You meet any Limitation on Benefits (LOB) provisions.

LOB provisions are safeguards designed to prevent individuals or entities from third-party countries from improperly claiming treaty benefits.

Here’s a quick reference table for the forms you might need:

| Form | Who Uses It | Income Type | When to Submit |

|---|---|---|---|

| W-8BEN | Foreign individuals | Dividends, interest, royalties, rents | Before payment is made |

| W-8BEN-E | Foreign entities (e.g., corporations, partnerships) | Business profits, dividends, interest, royalties | Before payment is made |

| Form 8233 | Foreign individuals | Independent contractor payments, personal services | Before payment is made (valid for one tax year) |

| Form 8833 | Individuals or entities claiming treaty overrides | Residency tie-breakers, real property gains, income source changes | Attached to annual tax return (Form 1040-NR or 1120-F) |

Form 8233 is specifically for independent contractors or service providers. If you’re receiving payments for services, you’ll need to submit this form to each withholding agent individually. It’s only applicable for personal services income.

Form 8833, on the other hand, is used to disclose treaty-based positions that modify or override the Internal Revenue Code. This is required if you’re claiming treaty benefits for things like reduced tax on U.S. real property gains, changes to the source of income, or credits for foreign taxes not typically allowed. If you’re using a tie-breaker rule to determine residency and your income exceeds $100,000, filing Form 8833 is mandatory. Be sure to include detailed facts on Line 14 of the form – vague explanations could lead to rejection by the IRS.

Failing to file Form 8833 can result in hefty penalties: $1,000 for individuals and $10,000 for corporations per failure. However, you usually don’t need to file this form if the income being disclosed totals $10,000 or less.

For entities submitting Form W-8BEN-E, it’s important to confirm that your entity meets the relevant LOB tests under Section 894. Use IRS Treaty Table 4 to identify the appropriate LOB test before filing.

Filing Steps and Common Mistakes

Now that you know the forms you need, here’s how to file them correctly and avoid common pitfalls:

- Get your TIN early. This could be a Social Security Number (SSN), Individual Taxpayer Identification Number (ITIN), or Employer Identification Number (EIN). Keep in mind that ITINs expire if they aren’t used on a tax return for three consecutive years, so ensure yours is active before claiming benefits.

- Submit the right form to every payor. Whether it’s W-8BEN, W-8BEN-E, or Form 8233, make sure you provide the appropriate form to each withholding agent from whom you expect to receive income. For Form 8233, the withholding agent must wait 10 days after mailing the form to the IRS before ceasing tax withholding, but the exemption will apply retroactively.

- File a U.S. tax return. Even if you qualify for a full treaty exemption, you’re still required to file a U.S. tax return (usually Form 1040-NR) with Form 8833 attached to disclose your treaty position.

It’s also important to note that U.S. tax treaties generally only apply to federal taxes. State tax obligations may differ, so check with state tax authorities to understand your responsibilities.

Lastly, be cautious about the U.S. treaty saving clause. This clause allows the U.S. to tax its citizens and residents as if the treaty didn’t exist. However, exceptions may apply for certain groups, such as students, teachers, or researchers. Double-check whether an exception applies to you before assuming the treaty exempts you from all U.S. tax obligations.

sbb-itb-ba0a4be

Tax Treaty Examples and Case Studies

Example: Reducing Taxes Through Treaty Benefits

Here are three real-world scenarios showing how U.S. tax treaties can help reduce international tax burdens:

Jennifer, a Canadian entrepreneur, earns $5,000 in interest income from a U.S. investment. Normally, Canada would withhold 25% ($1,250) of this income. Thanks to Article XI of the U.S.-Canada tax treaty, Canada applies a 0% withholding rate on interest payments. This means Jennifer avoids the $1,250 withholding and only pays taxes in her home country.

Sarah, a French entrepreneur, receives €10,000 in royalties from licensing her software to a U.S. company. Without a treaty, France would withhold 30% (€3,000) of her income. However, the U.S.-France tax treaty significantly reduces this withholding rate, allowing Sarah to retain more of her earnings while avoiding double taxation.

Michael, a UK entrepreneur, collects U.S. Social Security benefits. Under normal circumstances, he would face taxation in both the U.S. and UK. But Article 17 of the U.S.-UK tax treaty exempts these benefits from UK taxation, completely eliminating the double tax issue.

For a quick overview, here’s a table summarizing these examples:

| Entrepreneur | Country | Income Type | Without Treaty | With Treaty | Savings |

|---|---|---|---|---|---|

| Jennifer | Canada | Interest ($5,000) | 25% withheld ($1,250) | 0% withheld | $1,250 |

| Sarah | France | Royalties (€10,000) | 30% withheld (€3,000) | Reduced rate | Keeps more of her earnings |

| Michael | UK | Social Security | Taxed in both countries | UK exemption | Avoids double taxation |

Key Takeaways from Common Situations

These examples highlight the importance of leveraging the correct treaty provisions to reduce or eliminate tax burdens. For passive income – such as interest, dividends, and royalties – treaties often lower withholding rates. Similarly, personal service income may qualify for exemptions under specific treaty conditions.

To benefit, it’s essential to consult IRS tables for applicable rates and ensure the proper forms are submitted to the payor. By understanding and applying the right treaty articles, international entrepreneurs can effectively reduce or avoid double taxation.

Compliance Issues and State Tax Rules

Federal vs. State Tax Treatment

Here’s an important distinction to remember: U.S. tax treaties only apply to federal income taxes, not state taxes. This means you could potentially qualify for treaty benefits that eliminate your federal tax obligations but still owe state income taxes on the same earnings. The U.S. Supreme Court clarified this in Container Corp. of America v. Franchise Tax Board, stating that "the tax treaties into which the United States has entered do not generally cover the taxing activities of subnational governmental units such as States".

The key difference lies in how federal and state taxation standards operate. Federal treaties rely on the "Permanent Establishment" (PE) concept, which requires a fixed business presence before taxes apply. States, however, use the broader "nexus" standard, which can be triggered by minimal economic activity or even a short-term physical presence. As a result, you might avoid federal taxes under a treaty but still meet the nexus threshold in a state where you conduct business.

There is one notable exception: the nondiscrimination clause, usually found in Article 24 of most treaties. This provision ensures that states cannot tax foreign nationals more heavily than U.S. citizens in similar situations. Beyond this, states are not obligated to provide tax credits for taxes paid to other states. Offering such credits is a matter of policy, not a constitutional requirement.

These complexities highlight the importance of staying on top of compliance, which we’ll explore next.

How to Avoid Compliance Errors

To avoid missteps, always file Form 8833 when taking a treaty-based position to reduce your federal tax liability, such as claiming an exemption or changing the source of income. Even if a treaty exempts you from federal taxes, you’re generally required to file a return to disclose your treaty position.

For state-level compliance, it’s critical to review each state’s nexus rules. Federal exemptions don’t automatically apply to state taxes, so you may need to file state income, franchise, or sales tax returns, depending on your business activities.

Maintain thorough documentation of all transactions, U.S. presence, business operations, and treaty claims. These records are essential in case of an audit. Additionally, obtain a certificate of tax residency (Form 6166) from your home country’s tax authority to confirm your eligibility for treaty benefits. Taking these steps can help you navigate the complexities of both federal and state tax compliance.

Conclusion

Tax treaties offer international entrepreneurs an effective way to minimize or eliminate double taxation, but taking full advantage of them requires careful planning. Treaty benefits don’t apply automatically – you’ll need to actively claim them by filing the right forms, keeping detailed records, and clearly disclosing your treaty positions to the IRS.

It’s also important to note that federal treaty benefits do not extend to state taxes. Each state has its own rules, so make sure to review those to stay compliant. A good starting point is the IRS Treaty Tables at IRS.gov/TreatyTables, where you can find details about which types of income qualify for reduced rates or exemptions under your country’s treaty. For more detailed insights, you can refer to the Treasury Department’s Technical Explanations that accompany each treaty.

Non-compliance can be costly, with penalties of $1,000 for individuals and $10,000 for corporations. Given the complexity of treaty provisions, the frequent changes (such as the recent termination of the Hungary treaty and the suspension of the Russia treaty in 2024), and the interaction between federal and state tax systems, working with a qualified international tax professional is highly recommended.

If you’re setting up a U.S. business presence, platforms like BusinessAnywhere can assist with everything from business registration to virtual mailboxes and compliance support. These tools can help ensure your operations remain in line with U.S. regulations while maximizing treaty benefits.

Stay informed about your residency status, maintain thorough documentation of your treaty claims, and keep up with IRS updates. A little preparation now can save you from paying unnecessary taxes later.

FAQs

Do I still need to file a U.S. return if a treaty makes my U.S. tax $0?

Yes, even if a treaty reduces your U.S. tax liability to $0, you are still required to file a U.S. tax return. In most cases, you must also disclose any treaty-based positions by submitting Form 8833. Your filing responsibilities depend on your individual situation, so make sure to follow U.S. tax regulations carefully.

What business activities create a U.S. permanent establishment (PE) for treaty purposes?

A U.S. permanent establishment (PE) for treaty purposes is generally established when a foreign business operates through a fixed physical location in the U.S., such as an office, factory, or workshop. Alternatively, it can occur if the business has a dependent agent in the U.S. who regularly finalizes contracts on its behalf. However, for a PE to exist under treaty rules, the activities must be more than just preparatory or auxiliary – they need to be substantial in nature.

How do I claim a reduced U.S. withholding rate on dividends, interest, or royalties?

To qualify for a reduced U.S. withholding rate under a tax treaty, you need to file the correct form with the IRS to confirm your eligibility. Common options include Form 8233, which applies to specific types of income, or Form W-8BEN for individuals. Make sure the tax treaty between your country and the U.S. specifically covers your type of income. Once completed, submit the required documentation to the withholding agent. Always follow IRS instructions to meet the conditions for claiming treaty benefits.