If your business is solving technical problems, testing new ideas, or improving processes, you might qualify for the R&D Tax Credit. This credit offers a dollar-for-dollar reduction in federal taxes and can even offset payroll taxes for startups.

Key Points:

- Who qualifies? Businesses improving products, processes, or software using hard sciences like engineering or computer science.

- Benefits: Up to $500,000 annually in payroll tax offsets for startups and tax reduction for profitable businesses.

- Eligible Costs: Employee wages, research supplies, contractor expenses (65%), and cloud computing costs.

- Claiming Steps: Identify qualifying activities, keep detailed records, calculate the credit (Form 6765), and file with your tax return.

Even failed projects can qualify if they meet IRS criteria. Don’t miss out – less than 30% of eligible businesses take advantage of this credit.

Qualifying Activities: What Counts as R&D

To qualify for the R&D Tax Credit, your activities must meet specific criteria set by the IRS. These guidelines ensure only genuine research efforts are eligible.

The 4-Part Test for R&D Eligibility

For your research to qualify, it must pass all four of these tests:

- Permitted Purpose (Business Component Test)

Your research should aim to develop or improve a business component, such as a product, process, software, technique, formula, or invention, that your business uses or sells. The improvement must focus on function, performance, reliability, or quality – not just aesthetics or style. - Technological in Nature

The work must rely on principles from hard sciences like engineering, computer science, physical sciences, or biological sciences. For instance, creating advanced software algorithms, enhancing manufacturing equipment, or developing new chemical compounds would typically qualify. - Elimination of Uncertainty (Section 174 Test)

Your project must address uncertainty about capability, method, or design. According to the IRS Audit Techniques Guide, "Uncertainty exists if the information available to the taxpayer does not establish the capability or method for developing or improving the product or the appropriate design of the product". This doesn’t mean your work has to be revolutionary – it just needs to involve uncertainty for your business at the outset. - Process of Experimentation

At least 80% of your research efforts (measured by cost) should involve testing alternatives through trial-and-error, modeling, or simulation. Documenting uncertainties, the options considered, and the testing process is crucial.

For example, if a software company is developing a new feature and resolving performance issues by testing various database architectures, this likely meets all four tests. The project improves a business component, relies on computer science, addresses technical uncertainty, and involves systematic experimentation.

If a project as a whole doesn’t qualify, the IRS allows you to apply the "shrink-back" rule. By breaking the project into smaller components, you might identify specific qualifying elements.

Common Myths About R&D Tax Credit Eligibility

Misconceptions often discourage businesses from claiming the R&D Tax Credit. Here are some of the most common myths:

- Myth: You need a formal R&D department or lab.

This is false. As Barbara C. Neff explains, "You don’t have to meet any requirements as to industry or size; you don’t even need a formal R&D department". Any technical problem-solving effort could qualify. - Myth: Your research must succeed.

Success isn’t required. Even failed projects qualify if they meet the four-part test. The IRS values the process of resolving technical uncertainty, not just the outcome. - Myth: You need a patent.

While a patent can prove that your research is technological in nature, it’s not a requirement. Many qualifying activities don’t result in patents. - Myth: Your work must be "cutting-edge" or "new to the world."

Your research only needs to be new to your business. Even improving an existing product or process using established principles can qualify, regardless of whether others have done something similar.

The bottom line? If your team is tackling technical challenges through experimentation – even if the project doesn’t succeed – you’re likely conducting qualifying R&D.

Next, we’ll explore which activities and expenses count as research expenditures.

sbb-itb-ba0a4be

What Activities and Expenses Qualify

Here’s a closer look at the activities and expenses that meet the criteria for the R&D Tax Credit, building on the eligibility tests we’ve already covered.

R&D Activities That Qualify for Small Businesses

The R&D Tax Credit covers a wide range of technical projects across industries. For example, software developers creating APIs to link third-party systems, developing machine learning algorithms, or enhancing cybersecurity measures are conducting eligible research. Manufacturers can qualify by improving production processes, automating assembly lines, or designing advanced drilling and coating techniques to meet performance benchmarks. In the food and beverage industry, experimenting with new formulations or extending product shelf life through technical testing is also eligible. Similarly, hardware companies working on wearable devices, improving battery efficiency, or solving transmission issues can benefit.

Becca Hoeft, CEO of Morris Hoeft Group, emphasizes the importance of ingenuity for smaller firms: "the small business will have to get creative to conduct worthwhile R&D."

What matters most is whether your team is addressing technical uncertainty through systematic experimentation. You don’t need a formal R&D department or groundbreaking projects to qualify – what counts is the methodical approach to solving technical challenges.

Qualified Research Expenses (QREs)

Four main expense categories contribute to your credit calculation:

- Employee wages: Salaries for employees directly involved in R&D are eligible. If an employee spends at least 80% of their time on research, their entire salary qualifies.

- Supplies: Tangible materials used in research, like prototype components, qualify. However, capital equipment is excluded.

- Contract research: Payments to third-party contractors for research services qualify at 65% of the total cost.

- Cloud computing costs: Expenses for server space and hosting directly related to development work are also eligible.

The R&D Tax Credit typically provides a net benefit of 6% to 8% of your annual qualified costs. For tax years 2022–2024, businesses with average gross receipts under $31 million can claim up to $500,000 against payroll taxes. Additionally, unused credits can be carried forward for up to 20 years, ensuring no benefit is lost if you can’t use the full credit immediately.

To substantiate your claim, keep detailed records, including forms W-2, payroll registers, time-tracking logs, supply invoices, design documents, and test results. Next, we’ll cover how to document these expenses effectively.

How to Claim the R&D Tax Credit

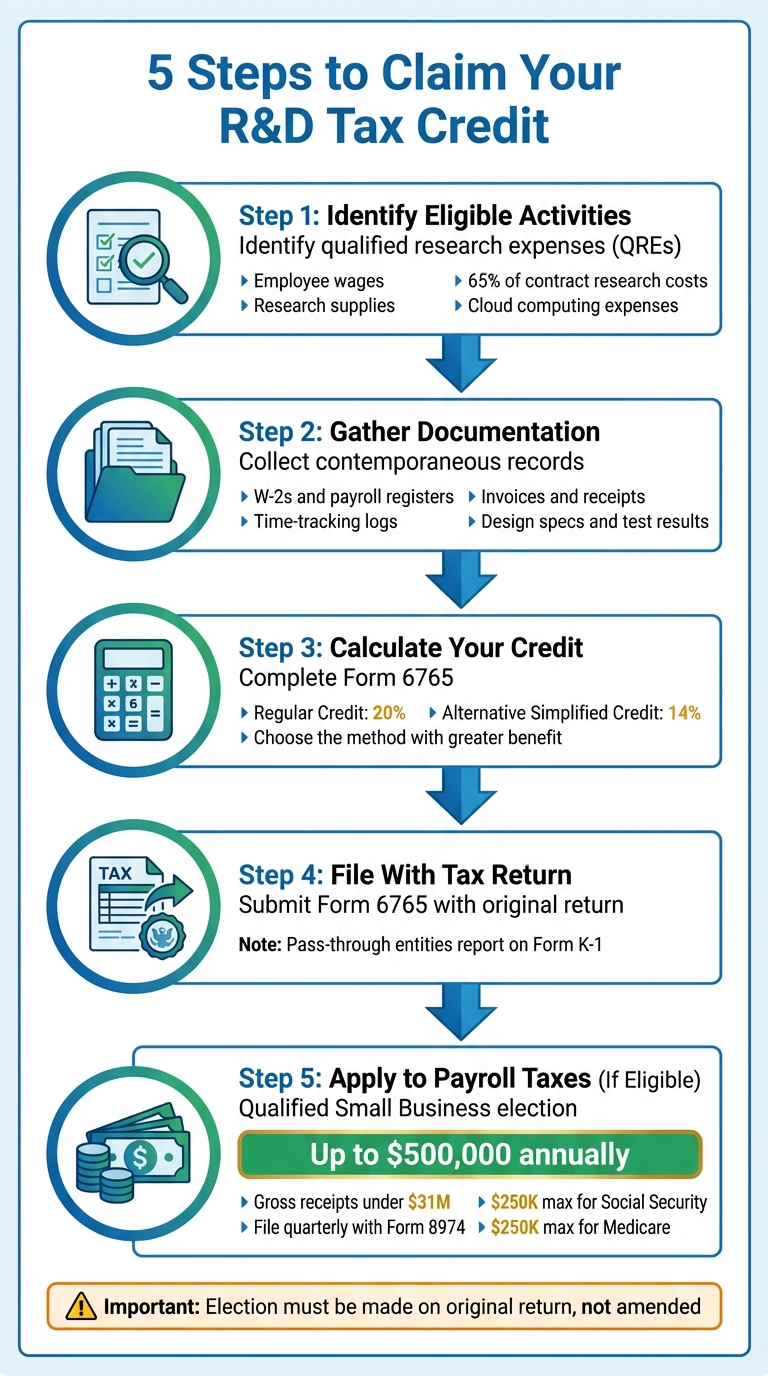

5 Steps to Claim the R&D Tax Credit for Small Businesses

5 Steps to Claim Your R&D Tax Credit

Claiming the R&D Tax Credit involves several key steps. Here’s a breakdown to guide you through the process:

Step 1: Identify eligible activities and qualified research expenses (QREs). These typically include employee wages, supplies used in research, 65% of contract research costs, and cloud computing expenses.

Step 2: Gather contemporaneous documentation. This means collecting records created during the research process, such as W-2s, payroll registers, time-tracking logs, invoices, design specifications, prototypes, and test results. The IRS emphasizes the importance of these records being generated during the research, not recreated afterward.

Step 3: Calculate your credit using Form 6765. You’ll need to compute the credit under both the Regular Credit method (20%, which requires extensive historical data) and the Alternative Simplified Credit method (14%, which only needs three years of QRE data). Choose the method that provides the greater benefit.

Step 4: File Form 6765 along with your original federal income tax return. For pass-through entities, the credit is reported on Form K-1 for partners or shareholders.

Step 5: If you’re a Qualified Small Business (gross receipts under $5 million), you can elect to apply the credit toward payroll taxes. This involves making the election on your original return and then claiming the credit quarterly using Form 8974 attached to Form 941. This can offset up to $500,000 annually – split into $250,000 each for Social Security and Medicare taxes.

"The payroll tax credit is elected by completing the appropriate portion of Form 6765 and attaching the completed form to the QSB’s timely filed (including extensions) income tax return… An election cannot be made with an amended return." – IRS

Accurate and thorough documentation is essential to support your claim and protect against potential IRS audits.

Documentation and Record-Keeping Requirements

To substantiate your claim, you need detailed records that demonstrate how each project tackled technical uncertainties. Examples include design iterations, CAD files, test reports, and relevant communication.

For payroll expenses, maintain timesheets that clearly show how employees allocate their time between qualified and non-qualified activities. If an employee spends at least 80% of their time on R&D, their entire salary may qualify. For contractor expenses, ensure agreements specify that your business retains substantial rights to the research and assumes the economic risk of failure.

Looking ahead, starting with tax years beginning in 2025, new Section G reporting requirements will take effect in 2026. These require a higher level of detail at the project level. You’ll need to identify your top 50 business components, describe the research activities performed, list the individuals involved, and explain what information you aimed to discover. To simplify this process, consider using separate cost codes in your accounting system to track research-related expenses throughout the year.

"R&D benefits are often only as valuable as the documentation available to support them." – BDO

Keep all records for five to seven years. While the standard statute of limitations is three years, certain situations may require longer retention. Additionally, businesses can typically claim the credit retroactively by amending returns for up to three prior years. Any unused credits can be carried forward for up to 20 years.

Getting the Most from Your R&D Tax Credit

Choosing Between Credit Calculation Methods

When deciding how to calculate your R&D tax credit, you have two options: the 20% Regular Credit (which relies on long-term historical data) and the 14% Alternative Simplified Credit (ASC) (which uses expenses from the prior three years). While the Regular Credit offers a higher rate, it doesn’t always result in a larger refund because the calculation of the "base amount" differs.

"The RC’s higher rate does not mean that a particular taxpayer’s RC will always be higher than its ASC rate… because the ‘base amounts’ are calculated differently." – BDO

To maximize your benefit, it’s a good idea to calculate both methods. However, keep in mind that if you choose the ASC on Form 6765, you generally can’t switch back to the Regular Credit for that same year on an amended return. Despite the availability of this credit, fewer than 30% of eligible small businesses take advantage of it, even though businesses reported over $32 billion in R&D credits in 2021.

| Feature | Regular Research Credit | Alternative Simplified Credit |

|---|---|---|

| Rate | 20% | 14% |

| Required Historical Data | May require records from the 1980s | Only the last 3 years of expenses |

| Best For | Established businesses with consistent R&D spending | Newer businesses or those without extensive historical data |

| Election Required | No | Yes, on Form 6765 |

Once you’ve chosen your credit calculation method, consider how federal and state credits can work together to increase your savings.

Stacking Federal and State R&D Tax Credits

You can claim both federal and state R&D credits for the same qualifying expenses, and 38 states currently offer their own R&D credit programs with rates ranging from 3% to 20%. By combining these credits, you could see a benefit exceeding 10% of each qualifying dollar spent.

The federal credit typically provides a return of 5–10% of qualifying expenses. Adding state credits can significantly boost your savings, especially in states like Arizona, Connecticut, Delaware, and Iowa, which offer refundable credits. Refundable credits are particularly advantageous because they provide cash back even if you have no tax liability. This further underscores the importance of accurate documentation and expense tracking.

However, be aware of state-specific rules. For example, California has its own rules and does not align with federal treatment, while other states adopt federal changes automatically through "rolling conformity". Timing also matters – Florida’s application window, for instance, is typically just one week in March.

The One Big Beautiful Bill Act of 2025 brought a significant change: the gross receipts threshold for the payroll tax offset rose from $5 million to $31 million. This change allows more small businesses to apply up to $500,000 of their federal credit annually against Social Security and Medicare taxes.

Common Mistakes to Avoid

Once you’ve selected your credit calculation method and explored federal and state options, it’s crucial to avoid common missteps that could jeopardize your claim.

The most frequent mistake? Insufficient documentation. Starting June 18, 2024, claims must include detailed information such as business components, descriptions of research activities, and a breakdown of qualified expenses (e.g., wages, supplies, and contract research). Documenting objectives, technical challenges, and employee time as the work happens – not at year-end – can save you headaches later.

A widespread misconception is that the R&D credit is only for high-tech companies or labs. In reality, industries like manufacturing, construction, and food/beverage also qualify if they conduct experiments to solve technical challenges.

"Poor documentation remains the biggest problem when claiming these credits." – k38consulting

Another pitfall is treating R&D expensing and credits as separate items. Mismanaging Section 174, Section 41, and Section 280C can lead to errors, double benefits, or even audits with penalties up to 20%. Instead, develop a unified financial model that integrates these elements.

Additional errors to avoid include:

- Using round numbers for expense allocations

- Claiming 100% of an employee’s time without detailed records

- Forgetting that only 65% of contract research costs are eligible

- Mixing business and personal expenses – use separate accounts or credit cards to maintain a clear audit trail

Lastly, don’t miss key deadlines. For example, if you qualify for retroactive relief under the 2025 OBBBA, you need to amend returns for tax years 2022–2024 by July 6, 2026. For claims under IRS review, you have until January 10, 2027, to perfect your documentation. Staying on top of these dates can make all the difference in securing your credit.

Conclusion

The R&D Tax Credit isn’t just for cutting-edge research labs – it’s a practical tax incentive that small businesses can use to lower their tax bills and drive growth. If your business tackles technical problems through experimentation, chances are you qualify. This credit directly reduces federal income tax liabilities dollar-for-dollar, and for small businesses with less than $31 million in gross receipts, it can offset up to $500,000 annually against payroll taxes.

Surprisingly, fewer than 30% of eligible small businesses take advantage of this credit. To make the most of it, understanding the four-part test is crucial. Detailed documentation is a must – the IRS requires specific project information, accurate time tracking, and a breakdown of expenses to support your claim.

You can also combine federal and state credits to maximize savings, and any unused credits can be carried forward for up to 20 years. If you’ve overlooked this credit in the past, you can file amended returns for the last three tax years to reclaim those savings.

If your qualified expenses exceed $100,000 annually, consulting an R&D tax specialist is a smart move to avoid mistakes.

"Generalist CPAs may not always identify all qualifying activities or optimize the credit."

– Greg O’Brien, CPA, Co-CEO of Anomaly.

A specialist can ensure you’re maximizing your savings while helping you steer clear of the 20% IRS penalty for disallowed credits.

FAQs

How can my small business claim the R&D Tax Credit?

Claiming the R&D Tax Credit for your small business boils down to three main steps: checking if you qualify, keeping track of eligible expenses, and filing the necessary forms with your tax return.

Start by verifying that your activities align with the IRS guidelines for research and development. Qualifying activities generally involve creating or improving products, processes, or software through experimentation and technological advancements. Routine tasks or work that doesn’t involve innovation typically won’t make the cut.

Next, focus on documenting all qualifying expenses. These may include employee wages for those directly involved in R&D, costs for supplies, and payments to contractors conducting research. Keeping detailed and accurate records is crucial to back up your claim.

When it’s time to file, complete IRS Form 6765 to calculate and claim the credit, and include it with your tax return. Double-check that everything is filled out correctly to avoid delays or potential penalties. By following these steps, you can make the most of this tax credit while staying on the right side of IRS rules.

Do unsuccessful R&D projects still qualify for the tax credit?

Yes, even if your R&D project doesn’t pan out as planned, it may still qualify for the tax credit – as long as the activities align with the criteria for qualified research and experimentation. The credit is based on what you did, not whether the project succeeded.

In other words, your business can claim the credit for trying to develop or improve products, processes, or software, even if the results fell short. The important part is ensuring your activities meet the IRS guidelines for qualified research.

How can my small business save more by using both federal and state R&D tax credits?

Combining federal and state R&D tax credits can be a smart way for small businesses to reduce costs while fueling innovation. The federal R&D tax credit offers a dollar-for-dollar reduction in tax liability based on qualified research expenses. For businesses that meet the IRS’s definition of a small business, this credit can even be applied to offset payroll taxes – a valuable benefit for startups and growing companies.

On top of that, many states offer their own R&D tax credits, which can often be paired with the federal credit. To qualify, your research activities must meet the requirements set by both federal and state guidelines. Proper documentation of all eligible research activities and expenses is key to taking full advantage of these credits.

Working with a tax professional can simplify the process, ensuring accurate filing and compliance. This way, you can lower your tax burden and redirect those savings into advancing your business’s innovative efforts.