Thinking about accepting cryptocurrency at your business? Here’s what you need to know:

- Why it matters: Crypto payments offer lower transaction fees (0%-2% vs. 2%-4% for credit cards), eliminate chargeback fraud, and enable instant global transactions.

- Challenges: Volatility, tax complexities, and setup hurdles can complicate adoption.

- How it works: Use payment processors like BitPay or Coinbase Commerce to accept crypto and convert it to dollars instantly, minimizing risks.

- Getting started: Select a processor, set up a wallet, ensure tax compliance, and train your team.

Bottom line: Crypto payments can reduce costs and expand your customer base, but managing volatility and taxes is critical.

| Feature | Cryptocurrency | Credit Cards |

|---|---|---|

| Fees | 0%-2% | 2%-4% |

| Settlement Speed | Minutes | 2-5 business days |

| Chargebacks | None | High |

| Volatility Risk | Yes, unless using stablecoins | No |

| Global Transactions | Instant, no conversion fees | Delays, high fees |

Crypto adoption is growing, with 741 million users globally in 2026. Ready to join the trend? Keep reading for a step-by-step guide.

Cryptocurrency vs Credit Card Payments: Complete Feature Comparison

Benefits of Accepting Cryptocurrency Payments

Reaching Tech-Savvy and Global Customers

Cryptocurrency opens the door to a broader customer base, especially those who may lack access to traditional banking systems. By offering crypto as a payment option, businesses can connect with the massive unbanked population without the need for complex banking infrastructure.

The profile of cryptocurrency users is particularly appealing for growth. These are often younger, tech-savvy individuals with higher disposable incomes. Displaying a "Crypto Accepted Here" badge signals your business embraces modern financial trends, making it attractive to customers who value forward-thinking solutions.

Crypto payments also operate around the clock – 24/7/365. For example, a customer in Tokyo can shop from a U.S.-based store at 3 AM Tokyo time without worrying about bank hours or international payment delays. In regions with unstable currencies, stablecoins pegged to the U.S. dollar provide a dependable way for international customers to participate in global commerce. This enhanced accessibility pairs well with the operational savings from lower transaction fees.

Reduced Transaction Fees

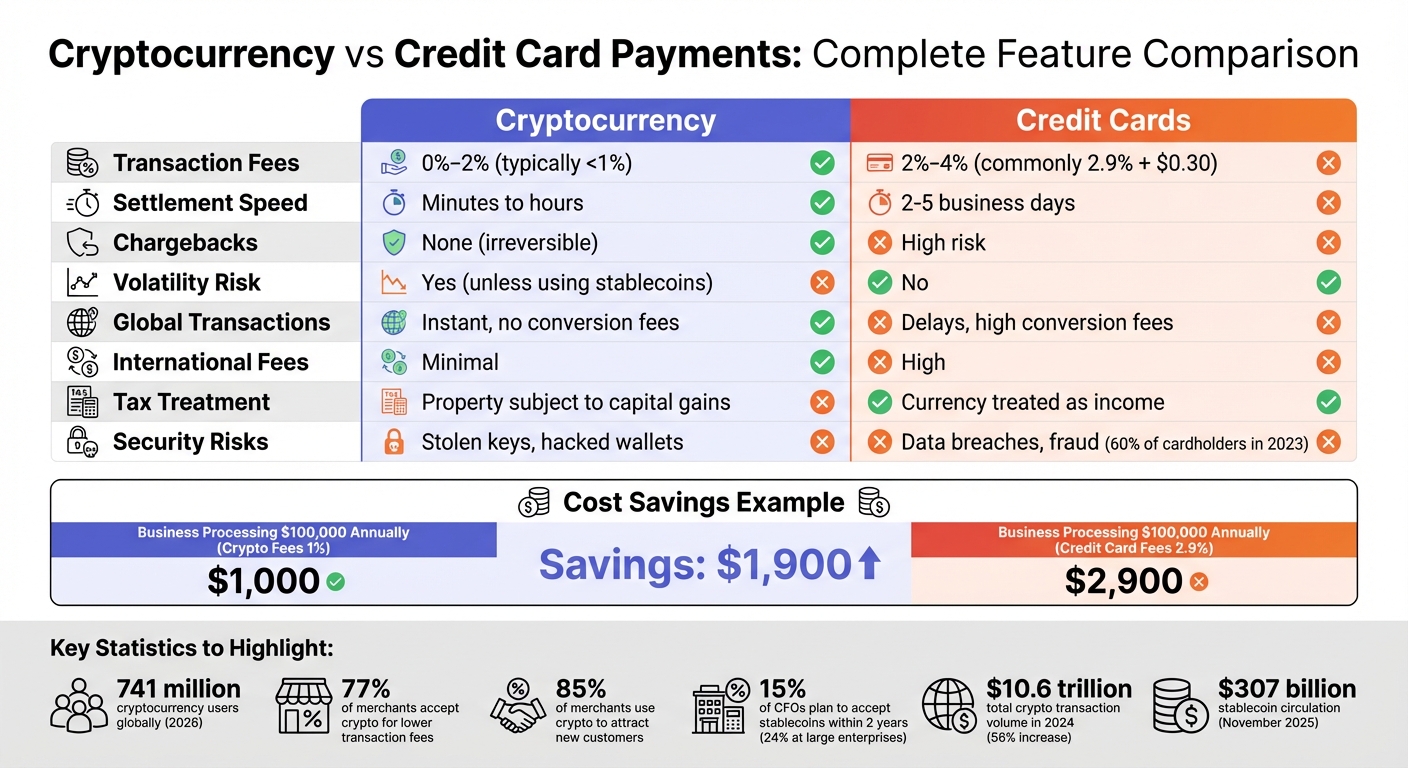

Credit card processing fees typically range from 2% to 4%, with common rates like 2.9% + $0.30 per transaction. In contrast, cryptocurrency fees usually hover around 1% and can even drop to 0%.

The savings add up fast. For instance, a business processing $100,000 annually at a 2.9% rate would pay $2,900 in fees. Switching to crypto at 1% cuts those fees to about $1,000, saving $1,900. As Nikolai Kariuk, Senior Marketing Copywriter at B2BINPAY, notes:

"For a business with tight margins, switching to digital currencies isn’t just tech innovation; it is an immediate 2% raise on your bottom line."

The benefits grow even more with international transactions. Traditional cross-border payments often involve currency conversion fees, wire transfer charges, and multiple intermediaries. With cryptocurrency, international and domestic payments are treated the same, offering a cost-effective alternative for businesses of all sizes.

Protection from Chargebacks and Fraud

Once a cryptocurrency transaction is confirmed, it’s permanent and cannot be reversed. This eliminates chargeback fraud, where customers dispute legitimate charges to get refunds while keeping the product. Unlike credit card payments, which can be revoked as they are "request" payments, cryptocurrency operates on a "push" system – funds are directly transferred to your wallet, and no bank or third party can reverse the transaction.

Additionally, crypto’s decentralized infrastructure reduces the risk of data breaches. Payment details are stored in individual wallets rather than centralized merchant databases, minimizing liability and offering better security for customers’ financial data. This added protection can give your business a competitive edge in today’s digital economy.

International Payments Without Currency Conversion

Handling payments from customers in different countries often means dealing with currency exchange fees, unfavorable rates, and settlement times that can stretch to 3–5 business days. Cryptocurrency eliminates these hurdles, offering near-instant settlement without conversion fees or delays, making global scalability much simpler.

There’s no need to manage multiple currency accounts or navigate the complexities of international wire transfers. For example, a customer in Germany paying with a USDC stablecoin enjoys a seamless transaction, while you receive the funds just as quickly.

Stablecoins, in particular, have become a cornerstone of global commerce. Their circulation more than doubled over an 18-month span beginning in 2024. Additionally, 15% of CFOs – and 24% at large enterprises – plan to accept stablecoins within the next two years. These dollar-pegged cryptocurrencies offer the speed and low costs of blockchain technology while maintaining price stability, making them an appealing choice for businesses looking to embrace crypto without dealing with extreme volatility.

Drawbacks of Accepting Cryptocurrency Payments

While cryptocurrency payments offer some intriguing benefits, they also come with a fair share of challenges.

Price Fluctuations and Financial Risk

Cryptocurrencies are infamous for their volatility. For instance, Bitcoin’s 30-day volatility index reached 10.88% during 2020-2021, compared to the USD/EUR currency pair, which has historically stayed under 1% volatility. Imagine receiving a $1,000 payment in Bitcoin – by the time you convert it, its value might have dropped to $900 or risen to $1,100. This unpredictability can lead to financial losses if businesses hold onto crypto for too long.

To minimize this risk, many businesses use instant conversion services offered by payment processors. These services lock in the exchange rate at the time of the transaction, ensuring you get the exact amount you charged. Another option is to accept stablecoins like USDC or USDT, which are pegged to the U.S. dollar and help avoid price swings.

Tax and Regulatory Requirements

Handling cryptocurrency for payments adds layers of tax and regulatory complexities. The IRS classifies cryptocurrency as property, which means accepting crypto triggers a double-taxation scenario. For example, if you receive $500 worth of cryptocurrency for a sale, you must report that $500 as ordinary income based on its fair market value at the time. Later, if you spend or convert that same cryptocurrency, a second taxable event occurs, resulting in either a capital gain or loss depending on its value at the time.

"The IRS considers cryptocurrency to be ‘property’ for tax purposes".

Businesses are required to track the fair market value of crypto in U.S. dollars at the moment of receipt, keep detailed records for each wallet, and file multiple IRS forms, including Form 8949, Schedule D, and the upcoming Form 1099-DA starting in the 2025 tax year. Additionally, sales tax must still be remitted in dollars, based on the fiat value of the transaction. Beyond taxes, setting up a crypto payment system brings its own hurdles.

Technical Setup and Integration

Accepting cryptocurrency payments isn’t as simple as flipping a switch. Businesses need to integrate compatible payment processors, secure digital wallets, and potentially upgrade hardware, such as QR scanners or NFC terminals, to handle blockchain transactions. One key point to note: blockchain transactions are irreversible. This means processing refunds involves manually initiating them through your payment processor’s dashboard.

Employees also need training to handle common issues like verifying blockchain confirmations and resolving problems such as incorrect blockchain payments, underpayments caused by network fees, or transactions stuck in "pending" status due to network congestion. These technical and operational challenges can make the integration process more demanding than it initially appears.

Pros and Cons Comparison Table

When evaluating whether cryptocurrency payments suit your business, comparing them directly with traditional credit card payments can provide clarity. Below is a side-by-side overview of their key features, highlighting the benefits and challenges of each option.

| Feature | Cryptocurrency Payments | Traditional Credit Cards |

|---|---|---|

| Transaction Fees | Less than 1% | 2% to 4% |

| Settlement Speed | Minutes to hours | 2 to 5 business days |

| Chargeback Risk | None – transactions are irreversible | High – customers can dispute charges |

| International Fees | Minimal | High due to currency conversion |

| Tax Treatment | Property subject to capital gains | Currency treated as income |

| Price Stability | Volatile unless using stablecoins | Stable (USD) |

| Security Risks | Stolen keys, hacked wallets | Data breaches, fraud (60% of cardholders in 2023) |

For example, 77% of merchants accept digital currencies specifically to benefit from lower transaction fees. Additionally, 85% of surveyed merchants see crypto payments as an effective way to attract new customers. The increasing adoption of Bitcoin by U.S. businesses underscores this trend, as multiple surveys reveal growing interest in digital payments.

This comparison highlights key advantages like reduced fees and faster settlements for cryptocurrencies, while also pointing out challenges such as price volatility and regulatory complexities. Use this perspective to determine whether crypto payments align with your business goals.

sbb-itb-ba0a4be

How Cryptocurrency Payments Work

Understanding how cryptocurrency transactions function sheds light on why they stand out compared to traditional payment methods. At the heart of crypto payments lies blockchain technology – a decentralized system that verifies and records transactions without needing banks.

Blockchain Technology Basics

A blockchain is essentially a decentralized ledger maintained by a network of computers, or nodes. Instead of relying on a single institution like a bank, thousands of nodes collaborate to verify and store every transaction. Each payment is secured with cryptography and digital signatures, where your private key acts as proof of ownership and authorizes transfers.

What makes blockchain so secure is its design. Transactions are grouped into "blocks", each linked to the one before it through a cryptographic fingerprint, or hash. If anyone tries to alter a single detail, the entire chain breaks, making fraudulent activity easy to detect. This transparency and built-in security help reduce fees and enhance fraud protection, as previously mentioned.

To ensure agreement among nodes and prevent dishonest behavior, networks use consensus methods like Proof of Work or Proof of Stake. Every transaction is recorded on a public ledger that is time-stamped, traceable, and open for auditing – all without compromising user privacy. By 2024, around 560 million people globally owned cryptocurrency, with the total transaction volume hitting $10.6 trillion – a 56% increase from the previous year.

Transaction Process Steps

Crypto transactions differ significantly from traditional credit card payments. While credit cards operate on a "pull" system, where merchants request funds, cryptocurrencies use a "push" system. This means the customer actively sends funds from their wallet, eliminating the risk of unauthorized chargebacks once the transaction is confirmed.

Here’s how it typically works:

- The customer selects "Pay with Crypto" at checkout. The payment gateway then generates a unique wallet address or QR code and locks in the exchange rate for 10–15 minutes.

- The customer scans the QR code using their digital wallet and authorizes the payment by signing it with their private key.

- The transaction is broadcast to the network, where nodes verify the sender’s funds and confirm the digital signature.

- Once the transaction is validated and added to a block, the payment processor notifies your e-commerce platform to mark the order as paid.

Many businesses use payment processors that convert cryptocurrency into fiat currency (like USD) instantly, reducing the risk of price volatility. Unlike credit card payments, which can take 1–3 business days to settle, crypto transactions are finalized in minutes or even seconds.

Today, over 15,000 businesses worldwide accept cryptocurrency payments, and stablecoin circulation reached $307 billion by November 2025. This efficient, push-based system makes cryptocurrency an appealing option for businesses looking to streamline their payment processes.

How to Start Accepting Cryptocurrency Payments

Getting started with cryptocurrency payments is easier than you might think. Small businesses can often set things up in just a few hours using third-party platforms. Here’s how you can integrate crypto payments into your operations.

Select a Cryptocurrency Payment Processor

Your first step is to pick a payment processor. For small businesses, third-party services like BitPay or Coinbase Commerce are popular choices because they handle key aspects like security, integration, and converting crypto into fiat currency. When deciding on a processor, consider the following:

- Settlement Options: Choose a service that offers instant conversion to fiat or stablecoins (like USDC) to avoid the risks of price swings.

- Supported Cryptocurrencies: Make sure the platform supports the coins your customers are likely to use. By 2026, stablecoins such as USDT and USDC on low-cost networks like Solana and Tron are dominating digital commerce. Bitcoin is still widely used but may not fit every business due to its higher transaction fees.

- Security Features: Look for providers that store most funds in cold storage and use multi-signature wallets for added protection.

Here’s a quick comparison of some major payment processors:

| Processor | Transaction Fee | Custody Model | Fiat Settlement | Best For |

|---|---|---|---|---|

| BitPay | 1% flat fee | Custodial | Yes (8 currencies) | Hands-off, full-service approach |

| Coinbase Commerce | 1% flat fee | Non-custodial | Yes (USD via bank) | Full control over funds |

| CoinPayments | 0.5% flat fee | Custodial | Yes (via partners) | Wide range of altcoins supported |

Most platforms charge around 1% per transaction, which is far lower than the 2.5% to 3% typically charged by credit card processors. Once you’ve selected a processor, it’s time to set up your wallet infrastructure.

Create a Crypto Wallet and Connect Payment Systems

Your wallet setup will depend on how you sell your products or services:

- E-commerce: Use plugins for platforms like Shopify, WooCommerce, or Magento.

- Custom Websites: Integrate via API to create unique payment addresses or QR codes.

- Brick-and-Mortar Stores: Use point-of-sale (POS) terminals or mobile apps that display QR codes for payments.

For day-to-day transactions, hot wallets are convenient, while cold wallets are better for securely storing larger amounts. If you opt for instant fiat conversion, your funds will be automatically settled in U.S. dollars, shielding you from crypto price volatility.

To enhance security, consider role-based access so only authorized staff can withdraw funds. Multi-signature wallets, which require multiple approvals for large transactions, add another layer of protection.

Meet U.S. Tax and Compliance Requirements

The IRS treats cryptocurrency as property. This means you need to record the fair market value of the crypto you receive at the time of the transaction as gross income. If the value changes before you convert it to fiat, you’ll need to report any capital gains or losses.

To simplify tax reporting, connect your payment gateway to accounting tools like QuickBooks or Xero. These tools can log transactions at their fiat value, helping you maintain accurate records. Be sure to track:

- Timestamps

- Fair market values

- Wallet addresses

- Conversion dates

You’ll also need to comply with Anti-Money Laundering (AML) and Know Your Customer (KYC) rules. This may involve verifying customer identities for larger transactions. State regulations can vary, so make sure your payment processor is authorized to operate in your area.

"To accept crypto payments, you must have your own crypto account, which, by default, makes you an investor. This means you are expected to comply with the cryptocurrency regulations for your state." – FitSmallBusiness

Working with an accountant familiar with cryptocurrency can help you navigate these requirements. Specialized tracking tools, which typically cost $100 to $1,000 annually, can also make compliance easier.

Test Your Crypto Payment System

Before launching, test your payment system in sandbox mode. This lets you verify that everything – from generating invoices to displaying QR codes – works as expected without using real funds.

Run a full-cycle test: create a test order, complete a payment, and confirm that the order status and accounting records update correctly. Most systems lock exchange rates for 10–15 minutes, so ensure this feature works as intended.

Since blockchain transactions can’t be reversed, it’s crucial to test your refund process. Refunds are usually handled off-chain by returning the original fiat value through traditional methods or store credit. Clearly outline your refund policy and train your staff on how to manage these situations.

Once you’re confident your system is running smoothly, you’re ready to start accepting real payments.

Track Transactions and Manage Price Risk

After launching, keep a close eye on transactions and exchange rates. To minimize price risk, set a policy that locks exchange rates for a short window – typically around 15 minutes – so customers aren’t affected by sudden market changes.

If you decide not to convert crypto into fiat immediately, establish clear rules for when to make conversions. This helps you avoid making hasty decisions during volatile periods. Regularly review transaction reports to spot trends, address any issues, and reconcile your records.

With an estimated 741 million cryptocurrency users worldwide as of February 2026 and 15% of CFOs planning to accept stablecoins within two years, adopting crypto payments can give your business a competitive edge. By focusing on the right tools, compliance, and risk management, you’ll be well-positioned to succeed in this growing market.

Conclusion

Accepting cryptocurrency payments can bring in new customers and reduce transaction costs, but it requires thoughtful preparation. The potential benefits are clear: lower fees, protection from chargeback fraud, and access to a global customer base. Recent trends also show that crypto adoption is gaining traction.

However, these perks come with challenges that need careful management. Cryptocurrency’s price volatility can impact revenue unless you use tools like instant fiat conversion or stablecoins. Additionally, the IRS classifies crypto as property, so you’ll need to document every transaction at its fair market value for tax purposes. Businesses should also focus on staff training, strong security measures, and updated accounting processes to handle these new payment methods effectively.

Start small. Use a trusted payment processor that simplifies compliance, consider stablecoins like USDC to avoid price fluctuations, and collaborate with an accountant to set up accurate tracking systems. Locking in exchange rates at checkout can also help protect against sudden changes in value. These steps can reduce risks and make the transition smoother.

Assess whether your customer base is tech-savvy or international, if your team can handle the extra workload, and if this aligns with your business’s risk tolerance. Striking the right balance between opportunity and caution is key to navigating this space successfully.

Incorporating cryptocurrency payments could be a forward-thinking move that helps position your business for what’s ahead.

FAQs

Should I accept stablecoins or Bitcoin?

Deciding between stablecoins and Bitcoin comes down to your business goals and how much risk you’re willing to take on.

Stablecoins are pegged to assets like the US dollar, which means their value stays steady. This makes them a solid option for businesses that need predictable pricing for transactions. On the other hand, Bitcoin is known for its price swings. While this volatility can be risky, it might appeal to tech-savvy customers and could offer long-term value growth.

Ultimately, your choice should align with your financial strategy, what your customers prefer, and your ability to handle the ups and downs of cryptocurrency prices.

What happens if crypto’s price drops after a sale?

If cryptocurrency prices fall after a transaction, businesses could experience losses due to the unpredictable nature of the market. To minimize this risk, you might want to convert crypto payments into fiat currency right away. Another option is to use stablecoins, which are designed to maintain a steady value. Both approaches can help safeguard your revenue from unexpected market swings.

What records do I need for IRS taxes?

To comply with IRS tax rules for cryptocurrency, it’s important to maintain thorough records of every transaction involving digital assets. Document key details like the date of the transaction, the fair market value at the time, the type of asset involved, and the reason for the transaction (such as a sale, exchange, or receipt). These records are vital for reporting income, calculating gains or losses, and staying within the guidelines when filing taxes. Since the IRS classifies digital assets as property, having precise documentation is a must.