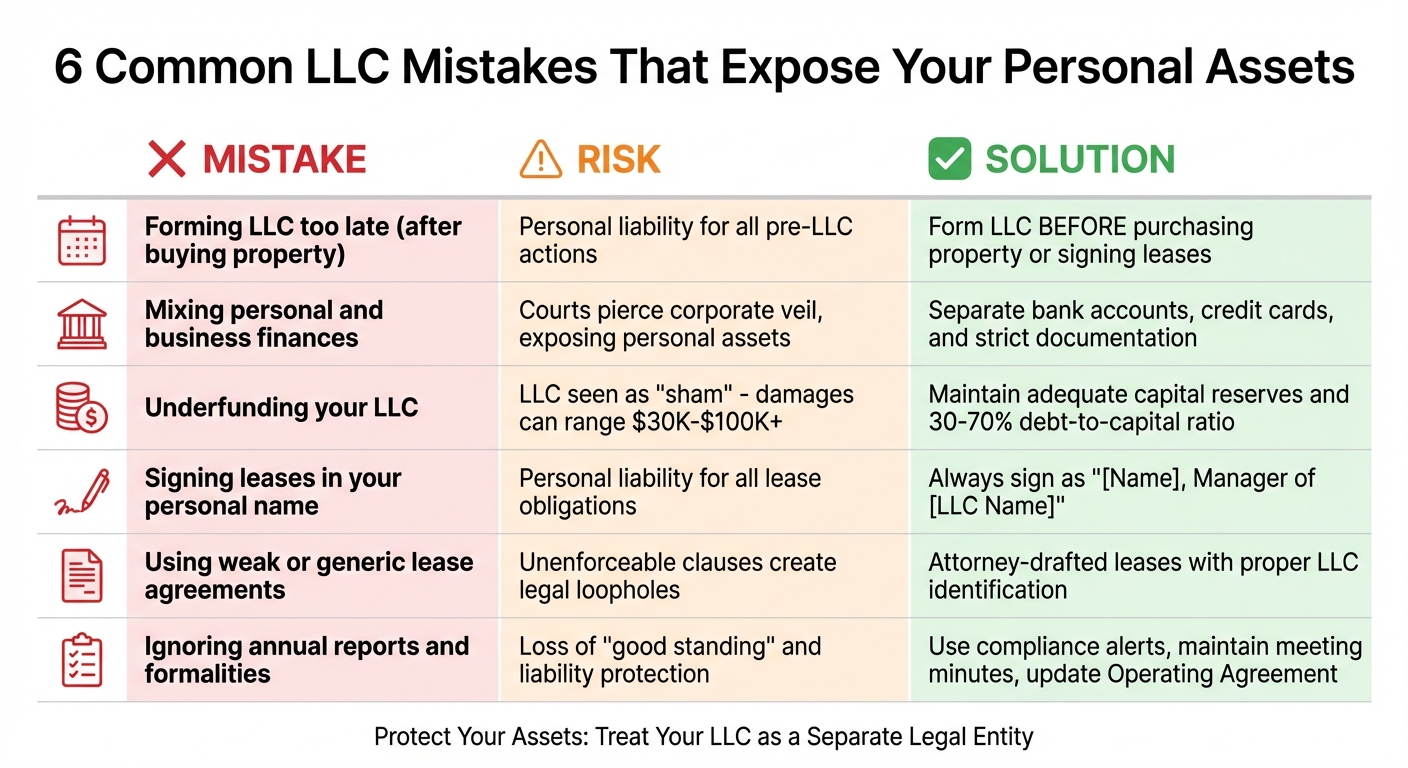

You set up an LLC to protect your personal assets, but it’s not foolproof. Many landlords unknowingly make mistakes that weaken this protection, leaving their savings, home, and other assets vulnerable to lawsuits. The key? Treat your LLC like a separate entity and avoid these six common pitfalls:

- Forming the real estate LLC too late: If you buy property or sign leases in your name before setting up the LLC, you remain personally liable for any issues tied to those actions.

- Mixing personal and business finances: Using the same bank account or paying expenses incorrectly can lead courts to "pierce the corporate veil."

- Underfunding your LLC: An LLC without enough capital may be seen as a sham, exposing your personal assets.

- Signing leases in your personal name: Always sign as the LLC manager to avoid personal liability.

- Using weak lease agreements: Generic or outdated leases can create legal loopholes that leave you exposed.

- Ignoring compliance requirements: Missing annual filings, neglecting your registered agent, or failing to document key decisions can dissolve your LLC’s protections.

Fixing these mistakes involves proper planning, maintaining strict financial separation, and staying compliant with legal requirements. By addressing these issues, your LLC can serve as the legal shield it’s meant to be.

Mistake 1: Forming Your LLC at the Wrong Time

Setting up your LLC after you’ve already bought property or signed leases can leave you exposed to personal liability. Why? Because any agreements, incidents, or legal relationships that happen before your LLC exists are tied directly to you – not your business. This timing misstep can create serious vulnerabilities down the road.

Why Timing Is Crucial

When you purchase property or sign leases under your personal name, you become the legal owner. That also makes you the primary target for any lawsuits. Unfortunately, forming an LLC later won’t protect you from actions taken before the LLC was established.

"If you don’t take care of this [transferring the deed], you personally will still be considered the owner of the property – and would therefore be the defendant in any lawsuit associated with it." – Nellie Akalp, CEO, CorpNet

If the property deed is in your name, you’re legally responsible. Fixing this after the fact involves transferring the deed to your LLC, which comes with tax consequences and extra costs like administrative fees or title transfer taxes. And if there’s a mortgage, you could face even bigger challenges. Moving the property into an LLC might trigger a "due-on-sale" clause, requiring you to pay off the entire loan immediately.

The Fix: Form Your LLC First

To avoid these headaches, plan ahead. Create your LLC before buying property or signing any leases. This ensures the LLC is the legal owner from the start, sparing you from the hassle of transferring deeds, dealing with tax surprises, and, most importantly, protecting your personal assets.

Services like BusinessAnywhere make it easy to get started, offering LLC formation for $0 plus state fees, which range from $50 to $500 depending on your state. They also include a free first year of registered agent service, so you can get your LLC up and running quickly. Once your LLC is formed, it can handle property purchases, lease agreements, and tenant interactions – all while keeping your personal name out of the equation.

sbb-itb-ba0a4be

Mistake 2: Mixing Personal and Business Finances

Using your personal bank account for rental income or property expenses is a quick way to jeopardize your LLC’s legal protection. When personal and business funds are combined, courts may no longer view your LLC as a separate legal entity. This concept, called piercing the corporate veil, can leave your personal assets – like your home, savings, or retirement accounts – vulnerable if your LLC faces legal judgments.

"If you have a single member LLC, it is especially important that you go out of your way to handle the LLC’s assets separately from your personal assets. When it’s just you, it can be easy to use the LLC’s bank account for personal expenditures, and vice versa. You must not blur these lines!"

– Dan McKenzie, Attorney, The McKenzie Law Firm, LLC

Examples of Commingling

Commingling funds is more common than you might think. It can happen when you deposit rent checks into your personal bank account, pay for property repairs with your personal debit card, or use business funds to cover personal expenses like groceries. Even transferring money between accounts without proper documentation counts as commingling. Single-member LLCs are especially at risk since there’s no business partner to help enforce financial boundaries. These mistakes can undermine your LLC’s legal status, making it critical to maintain clear separation between personal and business finances.

Solution: Keep Finances Separate

The best way to protect your LLC is to establish strict financial boundaries. Start by opening a dedicated business bank account using your EIN, and get separate business debit and credit cards. Services like BusinessAnywhere can assist with obtaining an EIN for your LLC to help you set up quickly. Some landlords even go so far as to use different banks – or keep business cards in a separate wallet – to avoid confusion.

When signing leases, contracts, or checks, always do so in your role as an LLC manager or member. For example, use a signature like "Jane Smith, Manager of Sunshine Rentals, LLC", instead of your personal name. If you accidentally use the wrong account, correct the mistake immediately by transferring funds back and documenting the transaction properly. Additionally, pay yourself through scheduled distributions rather than pulling money out whenever needed. This creates a clear audit trail, which is essential for preserving your LLC’s legal protections if legal challenges arise.

Mistake 3: Running an Underfunded LLC

Starting an LLC without enough capital can put your personal assets at serious risk. If your LLC doesn’t have the funds to handle basic repairs, legal claims, or unexpected costs, courts might see it as a “sham” entity – one created to dodge responsibilities rather than operate as a legitimate business. This perception gives tenants’ lawyers an opportunity to pierce the corporate veil, leaving your personal assets vulnerable.

How Undercapitalization Can Backfire

Courts often look at whether your LLC was properly funded to meet its expected obligations when it was formed. For example, if a tenant sues over unsafe living conditions – like a broken heater or other hazards – and your LLC can’t pay the judgment, a judge may determine that you intentionally underfunded the business to escape liability.

The financial risks here are no joke. Emotional distress claims in tenant disputes can range from $30,000 to $75,000, and in severe cases, they can exceed $100,000. In states with strong tenant protections, landlords displaying egregious behavior might even face treble damages, which means the compensation amount could be tripled. If your LLC only has a few hundred dollars in its account when these judgments hit, you could lose the legal protections that separate your personal assets from the business.

"Deliberately underfunding a business with obvious risks can be seen as a shell game to avoid creditors." – Lerner & Weiss

Undercapitalization not only weakens the legal shield of your LLC but also draws extra scrutiny if you’re making frequent personal withdrawals while leaving the business unable to cover its costs. Courts may view this as treating your LLC like a personal bank account rather than a separate legal entity. Once the corporate veil is pierced, you lose limited liability protection for all business debts – not just the one claim that brought the issue to light. This risk is similar to other behaviors, like mixing personal and business funds, that blur the line between your LLC and personal finances.

Solution: Keep Your LLC Financially Healthy

To avoid these pitfalls, make sure your LLC has enough money to cover repairs, insurance, and potential legal disputes. If you’re running a rental property business with significant monthly expenses, you’ll need a larger cash reserve than a smaller operation might require. Create a capital budget that outlines your expected expenses and revenue for at least the first year.

While borrowing is an option, aim to keep your debt-to-capital ratio between 30% and 70%. Always document capital contributions and distributions in your LLC’s records to clearly separate personal and business finances. As your business grows, reinvesting profits can help you avoid the appearance of underfunding.

Using tools like BusinessAnywhere’s compliance alerts can also help you stay on top of filing deadlines and maintain good standing with your state. Missing annual reports or state fees could lead to the automatic dissolution of your LLC, stripping away your liability protection and exposing your personal assets to business debts. Staying organized with these details is essential to preserving your LLC’s legitimacy and safeguarding your personal wealth.

Mistake 4: Signing Leases in Your Personal Name

When you sign a lease in your personal name, you’re putting your assets – like your home, car, and bank accounts – at risk. This simple mistake can weaken the legal shield your LLC is supposed to provide, leaving you vulnerable to lawsuits and financial liabilities.

The Risks of Personal Signatures

Your LLC is designed to act as a separate legal entity. But if you sign lease agreements as "Jane Smith" instead of "Smith Rentals, LLC, by Jane Smith, Manager", you’re effectively taking on personal responsibility. Courts treat personal signatures as a commitment from you, not your LLC, which can expose your personal wealth to claims against the business.

Attorney Stephen E. Yoch highlights this danger with a real-life example. In one case, a tenant signed a lease on behalf of "XYZ Corp." but used "Tom Jones, Owner" as the signature. Because the corporation wasn’t clearly identified, the court held Jones personally liable for unpaid rent. This judgment left his personal assets on the line.

"The difference between personal financial ruin and just another day at the office can be [how you sign your name]."

– Stephen E. Yoch, Partner, Felhaber, Larson, Fenlon & Vogt, P.A.

Even if your LLC dissolves, signing with your personal name keeps you on the hook. Similarly, if you transfer property to your LLC but fail to update existing leases, you remain the landlord on record, leaving your personal assets exposed to potential claims.

Solution: Always Sign as the LLC Manager

To protect yourself, always sign documents as a representative of your LLC. Your signature block should clearly state the LLC’s name, your printed name, and your title. For example:

"Smith Rentals, LLC, by Jane Smith, Manager."

Make sure the lease explicitly names the LLC as the landlord, not you personally.

If you’re handed a pre-printed lease with only your name, you can manually revise it to include the LLC’s name and your official title before signing. Avoid vague titles like "Owner", which can imply personal liability.

Additionally, after transferring property to your LLC, update all active leases to reflect the change. Direct tenants to make rent payments to your LLC’s business bank account. Services like BusinessAnywhere can help by providing a professional business address for legal notices, keeping your home address private.

| Lease Element | Personal Ownership (Incorrect) | LLC Ownership (Correct) |

|---|---|---|

| Landlord Name | Individual’s Name (e.g., Jane Smith) | LLC Name (e.g., Smith Rentals, LLC) |

| Signature Line | Jane Smith | Smith Rentals, LLC, by Jane Smith, Manager |

| Rent Payment | Paid to Jane Smith | Paid to Smith Rentals, LLC |

| Notices | Sent to Home Address | Sent to Registered Agent or Business Address |

Mistake 5: Using Weak or Outdated Lease Agreements

A poorly constructed lease agreement can leave your LLC vulnerable. Even if your LLC is set up and maintained correctly, a weak lease can create loopholes for tenants’ lawyers to bypass your liability protection and target your personal assets.

What Makes a Lease Agreement Weak

To safeguard your LLC, your lease agreement needs to be airtight. It’s not just about having a lease – it’s about having one that’s legally sound and tailored to your state’s landlord-tenant laws.

One common pitfall is using vague or incomplete language. Generic templates downloaded online often fail to comply with state-specific regulations, which can make certain clauses unenforceable.

"Attorney Janet Portman warns that generic form leases may include unenforceable clauses that undermine your legal protection."

Here are some key mistakes that could jeopardize your LLC:

- Incorrect landlord identification: If the lease lists you personally as the landlord instead of your LLC, you’ve essentially invited lawsuits to target your personal assets.

- No renter’s insurance requirement: Without a clause requiring tenants to carry renter’s insurance, your LLC could be left exposed to claims for damaged tenant belongings. Landlord-tenant laws typically don’t hold landlords liable for tenant property unless negligence is proven, so requiring insurance shifts the responsibility appropriately.

- Poorly defined maintenance responsibilities: Failing to outline "tenant-like" duties – such as unclogging sinks or changing light bulbs – can lead to disputes where you’re unfairly blamed for minor issues.

- Illegal liability waivers: Some outdated lease templates attempt to waive all landlord liability for negligence, which is prohibited in states like Wisconsin.

"According to Wisconsin Administrative Code ATCP 134.08: ‘No rental agreement may relieve, or purport to relieve the landlord from liability for property damage or personal injury caused by negligent acts or omissions of the landlord’".

Including such clauses can backfire, as courts may not only invalidate them but also penalize you for their presence.

Solution: Invest in Attorney-Drafted Leases

The best way to protect your LLC is by using a lease agreement drafted or reviewed by a qualified real estate attorney familiar with your state’s laws. While this might cost a few hundred dollars upfront, it’s a small price compared to the potential financial fallout of a lawsuit.

A strong lease should:

- Clearly name your LLC as the landlord.

- Require tenants to maintain renter’s insurance.

- Define specific maintenance responsibilities for tenants.

- Include proper notice requirements for landlord entry (typically 24 to 48 hours, depending on your state).

- Set reasonable late fees that reflect actual damages rather than punitive amounts.

If your current leases list you personally as the landlord, replace them immediately with agreements that name your LLC. Also, ensure all rent payments go directly to your LLC’s business bank account, not your personal account.

Regularly reviewing and updating your leases is another essential step. Laws evolve, and what worked a couple of years ago might not be compliant today. Set an annual reminder to consult your attorney for updates. Tools like BusinessAnywhere can help you stay on top of compliance requirements, including Beneficial Ownership Information (BOI) reporting.

Taking these precautions ensures your lease agreements align with your overall strategy for protecting your assets.

| Lease Element | Weak Agreement | Strong Agreement |

|---|---|---|

| Landlord Name | Lists individual owner’s name | Uses the full legal name of the LLC |

| Signature Line | Signed personally by owner | Signed as "[Name], Manager of [LLC]" |

| Insurance | No mention of renter’s insurance | Requires mandatory renter’s insurance |

| Maintenance | Vague repair responsibilities | Clearly defines tenant duties |

| Liability | Waives all negligence liability | Complies with state-specific laws |

Mistake 6: Ignoring LLC Formalities and Compliance

Keeping up with your LLC’s formalities is not just a good habit – it’s a must for protecting your personal assets. The liability protection your LLC offers depends on following specific rules. If you skip important filings or fail to document major decisions, courts might decide your LLC isn’t a separate entity and hold you personally responsible.

Common Compliance Missteps

Most states require LLCs to file annual or biennial reports with the Secretary of State to maintain "good standing." Missing these filings can weaken your LLC’s legal status or, worse, lead to administrative dissolution. Without this protection, your personal assets could be at risk.

Another frequent mistake is neglecting your registered agent. If your LLC doesn’t have an active registered agent, you might miss critical legal or tax notices. This could result in default judgments if you fail to respond to lawsuits or summons.

Courts also expect LLCs to document significant actions, like acquiring property or changing management, through written minutes or resolutions. Without this paper trail, it becomes easier for someone to argue that your LLC is just an extension of your personal finances.

"Ignoring these steps can give plaintiffs grounds to argue the LLC is not a true legal entity, which makes it easier to pierce the corporate veil." – Clint Coons, Attorney and Asset Protection Specialist

Additionally, failing to amend your LLC Operating Agreement when membership or profit-sharing arrangements change can undermine your LLC’s legitimacy.

Addressing these compliance gaps is crucial to maintaining the legal separation between your personal and business affairs.

Solution: Stay Organized with Compliance Alerts

To avoid these pitfalls, create a system to track compliance deadlines. Set calendar reminders or use a professional registered agent service to ensure you never miss important filings or legal notices.

Make it a point to review your Operating Agreement annually. If your LLC has added new members, changed profit-sharing arrangements, or adjusted management roles, update the agreement right away to reflect these changes.

Document major business decisions. For example, if your LLC buys a new rental property or undertakes significant repairs, record the decision with a written resolution. This step helps demonstrate that your LLC operates as a separate legal entity.

Finally, periodically request a Certificate of Good Standing from your Secretary of State. This document confirms that your LLC has met all filing and fee requirements, which can be especially useful when applying for loans or entering into major contracts.

| Compliance Requirement | Purpose | Risk of Neglect |

|---|---|---|

| Annual Reports | Maintains "Good Standing" with the state | Loss of liability protection; administrative dissolution |

| Meeting Minutes/Resolutions | Documents business as a separate entity | Easier for courts to pierce the corporate veil |

| Operating Agreement Updates | Reflects current ownership and governance | Challenges to LLC legitimacy in court |

| Registered Agent | Ensures receipt of legal and tax notices | Missed deadlines and potential default judgments |

How to Protect Your Rental Properties

Safeguarding your rental properties requires a thoughtful approach. By setting up the right LLC structures, adhering to operational best practices, and ensuring compliance, you can effectively shield your personal assets.

Multiple Layers of Asset Protection

The key to strong protection lies in separating risks. Instead of grouping multiple properties under one LLC, consider placing each property in its own LLC. This approach ensures that if a tenant sues over an incident at one property, your other properties remain unaffected.

For added security, you can use a Wyoming holding company to own each property LLC. This setup keeps your name off public records, making it harder for attorneys to target you as a high-net-worth individual. Wyoming is especially appealing because it offers privacy protections and avoids the annual franchise taxes required in states like California, where the minimum is $800.

"A big part of succeeding in Real Estate is just assembling the right team around you." – Clint Coons, Attorney and Real Estate Investor

Beyond structuring your entities, consider layering your protection with comprehensive insurance. Combine landlord insurance with an umbrella policy to cover catastrophic claims. While an LLC limits liability, insurance addresses potential damages.

BusinessAnywhere’s Digital Nomad Kit offers a one-stop solution for LLC formation, registered agent services, virtual mailboxes, EIN applications, and compliance alerts. Pricing starts at approximately $3,070 for U.S. citizens.

To optimize taxes, elect S-Corp status to reduce self-employment taxes and unlock corporate deductions. BusinessAnywhere provides Form 2553 filing for $97.

Additionally, using a professional registered agent service protects your privacy and ensures you receive important legal notices. BusinessAnywhere offers this service for $147 annually after the first free year.

By combining these measures, you can create a robust asset protection strategy.

Comparison Table: Mistakes vs. Solutions

Here’s a quick breakdown of common mistakes and their solutions to help you strengthen your asset protection plan.

| Mistake | Risk | Solution | Cost | Protection Level |

|---|---|---|---|---|

| Commingling Funds | Personal assets could be at risk if corporate veil is pierced | Keep separate bank accounts and credit cards for each LLC | $0 (Free) | High |

| Personal Signatures | Personal liability for lease or contract breaches | Always sign as "Manager" or "Member" of the LLC | $0 (Free) | High |

| Single LLC for All Properties | One lawsuit could jeopardize your entire portfolio | Use separate LLCs for each property or opt for a Series LLC structure | $50–$500 per LLC | Maximum |

| Self-Managing Repairs | Personal liability for tenant injuries | Hire licensed, insured contractors for all repairs | Variable | High |

| Underfunding the LLC | Courts may deem the LLC a "sham" or "alter ego" | Ensure adequate operating capital in business accounts | Variable | Essential |

| Not Transferring Deed | LLC doesn’t legally own the property, leaving you liable | Record the deed transfer with the county immediately after formation | Low (Recording fees) | Critical |

| Missing Annual Reports | Loss of "good standing" and liability protection | Use compliance alerts or hire a professional registered agent | $147/year | High |

Conclusion

An LLC’s strength lies in the discipline of its management. Courts are quick to pierce the corporate veil when owners blur the lines between personal and business finances or fail to sign agreements under the LLC’s name. If this happens, personal savings, vehicles, and even your home could be at risk from legal claims.

The six common mistakes – like commingling funds, signing leases personally, or missing compliance deadlines – can weaken your LLC’s protective barrier. The good news? These pitfalls are entirely preventable. Keep your finances strictly separate, always sign as the LLC manager, transfer property titles to the LLC early, and stay on top of state compliance requirements. These steps, as outlined in this article, are essential for safeguarding your personal assets.

"Noncompliance pokes a hole through your LLC’s protective shield and makes your personal assets vulnerable." – Nellie Akalp, CEO, CorpNet

Tackling these issues now can strengthen your LLC’s defenses. Services like BusinessAnywhere simplify this process with tools like compliance alerts, registered agent services for $147 annually, and support for filing Form 2553 for S-Corp elections. Their Digital Nomad Kit, priced at around $3,070 for U.S. citizens, includes LLC formation, EIN applications, a virtual mailbox, and compliance tools – all accessible through a single dashboard.

Take the time to review your setup, correct any errors, and create a solid defense for your assets.

FAQs

How can I properly fund my LLC to protect my personal assets?

To protect your personal assets, it’s crucial to treat your LLC as an entirely separate and properly funded business entity right from the beginning. Start by making a clear capital contribution to cover property expenses, repairs, insurance, and other operational costs. Record this contribution in the LLC’s financial records and deposit the funds into a dedicated LLC bank account in the company’s name. This proves the LLC operates independently and isn’t just a cover for personal transactions.

Make sure to keep personal and business finances separate. Use the LLC’s bank account to handle all rental-related expenses, like mortgage payments, utilities, and repairs. Avoid using personal accounts or credit cards for LLC expenses. If you need to withdraw funds for personal use, document these as member distributions in line with your operating agreement.

Lastly, ensure you maintain detailed and formal records. Keep your operating agreement updated, file any required reports, and store receipts, bank statements, and other documentation that show the LLC functions as a distinct entity. These practices strengthen the legal protections that shield your personal assets from liabilities connected to the LLC.

How can I keep my personal and LLC finances separate to protect my assets?

Maintaining a clear boundary between your personal finances and those of your LLC is essential to safeguard your personal assets and uphold the corporate veil. The first step? Open a business bank account and, if necessary, a business credit card in your LLC’s legal name using its EIN. Make sure all income and expenses tied to the business go through these accounts. If you need to withdraw money, record it as an official member draw or salary – don’t treat it like a personal expense.

To keep everything organized, use accounting software or a dedicated ledger solely for LLC transactions. Clearly label invoices, receipts, and checks with your LLC’s name, and always keep documentation for every expense. Avoid mixing funds by steering clear of personal accounts or credit cards for LLC-related bills. If you ever need to add personal funds to the LLC, document it properly as either a capital contribution or a loan.

By sticking to these habits, you show that your LLC functions as a separate legal entity. This can go a long way in protecting you from personal liability during legal disputes.

Why should I update my lease agreements to reflect LLC ownership?

Updating your lease agreements to name your LLC as the landlord is a crucial step in safeguarding your personal assets. If the lease lists you personally rather than the LLC, courts might view your rental activity as a personal business. This could leave your personal assets vulnerable in the event of a lawsuit. Clearly stating the LLC as the landlord helps draw a firm line between your personal and business liabilities.

Using outdated or generic lease agreements that don’t reflect LLC ownership can also lead to legal complications. Tenants’ lawyers might argue that failing to update the lease demonstrates poor business practices, which could increase the risk of personal liability. By regularly revising your leases to include the LLC’s name and other pertinent details, you ensure compliance with state laws and maintain the liability protection that your LLC was designed to provide.