If you’re thinking about transferring your rental property to an LLC, here’s the bottom line: it offers advantages and disadvantages for rental properties, but only if you do it the right way. The process involves working closely with your lender and insurer to avoid triggering a due-on-sale clause or voiding your insurance policy. Miss these steps, and you could face loan acceleration, denied claims, or other financial headaches.

Key Steps to Follow:

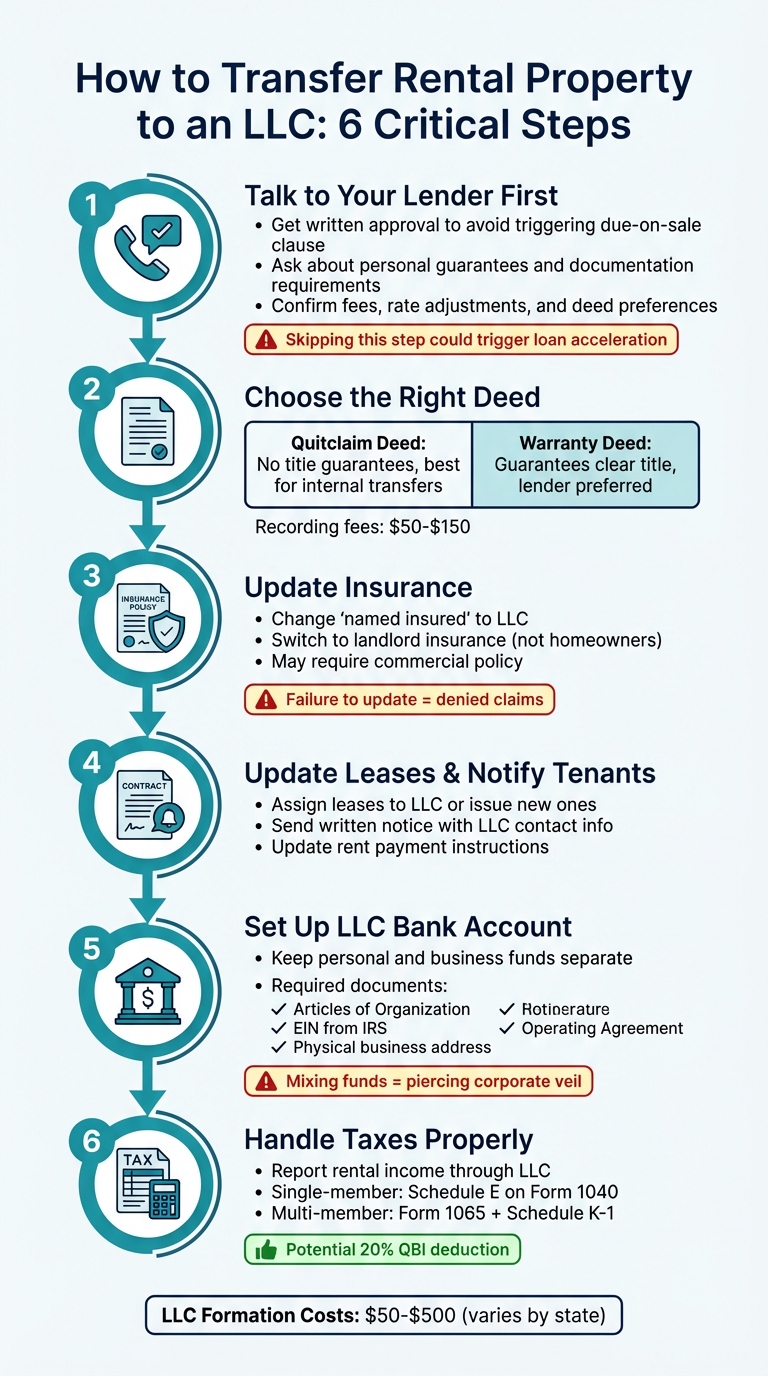

- Talk to Your Lender First: Get written approval to avoid triggering the due-on-sale clause in your mortgage.

- Choose the Right Deed: Use a Quitclaim or Warranty Deed to transfer ownership – but make sure it aligns with your lender’s and insurer’s preferences.

- Update Insurance: Change the "named insured" on your policy to match the LLC. Landlord insurance is a must.

- Update Leases and Notify Tenants: Ensure that all leases and tenant notices reflect the LLC as the new landlord.

- Set Up an LLC Bank Account: Keep personal and business funds separate to maintain liability protection.

- Handle Taxes Properly: Report rental income and expenses through your LLC and take advantage of potential deductions.

Contact Your Lender Before Transferring the Title

Before you officially transfer your rental property to an LLC, it’s essential to reach out to your mortgage lender. Even if the transfer initially goes unnoticed, any later discovery could lead to serious consequences.

To understand how your lender might react, it’s important to familiarize yourself with the due-on-sale clause.

What Is the Due-on-Sale Clause?

The due-on-sale clause, sometimes called an acceleration clause, is a provision in most mortgages that allows the lender to demand full repayment if the ownership of the property changes. Since an LLC is considered a separate legal entity, transferring your property to one is viewed as a change in ownership. If this transfer is done without the lender’s approval, it could trigger the clause, requiring you to pay off the entire loan immediately.

Attorney Amy Loftsgordon explains the potential risk:

"If your mortgage has a due-on-sale clause and [the lender] finds out you transferred the property’s ownership to an LLC, they might call the loan due because you violated this clause."

While the Garn-St. Germain Act provides exceptions for transfers to family members or certain living trusts, these protections don’t apply to business entities like LLCs. Lenders rely on this clause to control unauthorized transfers and to adjust interest rates when necessary.

Questions to Ask Your Lender

When contacting your lender, make sure to get all agreements in writing. Larger banks may sometimes allow LLC transfers, but policies vary. Attorney Nathaniel Gilbert suggests asking these key questions:

- "Will transferring this property to my single-member LLC trigger the due-on-sale clause?"

This is the most important question. Some lenders may allow the transfer under specific conditions, while others may not permit it at all. - "Will I need to sign a personal guarantee, and what documentation do you require?"

If the transfer is approved, most lenders will ask for a personal guarantee and will likely review your LLC’s Articles of Organization, Operating Agreement, and EIN. - "Are there any fees, rate adjustments, or deed type preferences?"

Find out if there are administrative fees, whether your interest rate will change to a commercial rate, and if the lender has a preference for a Warranty Deed or Quitclaim Deed.

Recording fees for a new deed usually range from $50 to $150, while state LLC filing fees can vary between $50 and $500. Asking these questions helps protect both your financing terms and your liability strategy.

Once you have your lender’s approval, it’s time to decide on the type of deed for the transfer.

Quitclaim Deed vs. Warranty Deed

After getting the green light from your lender, you’ll need to select the appropriate type of deed. The two most common options – Quitclaim Deeds and Warranty Deeds – serve different purposes and offer different levels of protection.

- Quitclaim Deed:

This type of deed transfers whatever interest you currently hold in the property without making any guarantees about the title’s quality. It’s often used for simple transfers, such as moving property into your own LLC. However, it doesn’t protect against future title disputes. - Warranty Deed:

A warranty deed ensures a clear title and offers protection against any claims. This type of deed is typically preferred by lenders and title companies because of the security it provides.

| Deed Type | Key Features | Financing Impact | Best Use Case |

|---|---|---|---|

| Quitclaim Deed | No title guarantees | Higher lender risk | Internal transfers |

| Warranty Deed | Guarantees clear title | Lender preferred | Third-party transactions |

Your lender’s preference will likely influence your choice. Warranty deeds generally offer stronger protection for everyone involved, and some title insurance companies may even require a warranty deed to maintain your existing policy. For single-member LLC transfers, however, many lenders are comfortable with quitclaim deeds.

Before recording the deed, check with your title insurance company to see if the transfer will impact your current policy. Some insurers might need specific endorsements or mandate a warranty deed to keep coverage intact.

sbb-itb-ba0a4be

How to Transfer Rental Property to an LLC

Once your lender has given the green light, you can move forward with transferring your rental property to an LLC. This process involves three key steps: setting up your LLC, preparing the necessary deed, and documenting the transfer within your LLC’s records. Here’s how to handle each step.

Form Your LLC and Obtain an EIN

Start by forming your LLC in the state where your property is located. This avoids the hassle and expense of registering as a foreign LLC. Choose a unique name that includes "LLC" or "Limited Liability Company", and appoint a registered agent who has a physical address in the state and is authorized to receive legal documents on your behalf.

Next, file your Articles of Organization with the Secretary of State. Filing fees vary by state and typically range from $50 to $500. If your LLC has multiple members, create an Operating Agreement. This document outlines ownership shares, management responsibilities, and how profits will be divided.

Once your LLC is officially formed, you’ll need an Employer Identification Number (EIN) from the IRS. This number is essential for opening a business bank account and managing your LLC’s taxes. You can apply for an EIN directly on the IRS website. Alternatively, services like BusinessAnywhere can assist with LLC formation, EIN applications, and even provide registered agent services for an additional fee.

Prepare and Record the Deed

The deed is the official document that transfers ownership of the property to your LLC. Begin by listing yourself as the "grantor" (current owner) and your LLC as the "grantee" (new owner). Be sure to use the exact legal description of the property as it appears in your county records.

When deciding on the type of deed, refer to the earlier discussion on Warranty and Quitclaim Deeds. A Warranty Deed ensures a clear title and is often preferred unless your lender advises otherwise.

Once the deed is prepared, have it notarized and submit it to your county recorder’s office to finalize the transfer. This step makes the transfer public and legally binding. Keep in mind that some states, such as California, require additional forms like the Preliminary Change of Ownership Report (PCOR) or Form BOE-502-A.

After the deed is recorded, make sure to document the transfer within your LLC’s internal records to maintain the liability protections associated with your LLC.

Draft an LLC Member Resolution

Even if you’re the sole member of your LLC, it’s important to formally document that your LLC has accepted the property. This is done through an LLC member resolution, which records the transfer as a capital contribution. This step not only supports the liability protections of your LLC but also creates a clear paper trail for tax purposes, including future depreciation.

Once signed, file the resolution with your LLC’s official records alongside your Articles of Organization and EIN confirmation. Don’t forget to update your Operating Agreement’s "Schedule of Assets" to reflect the property’s legal description and market value. This ensures your LLC’s documentation remains complete and accurate.

Update Leases, Tenant Notices, and Insurance

When transferring your rental property to an LLC, it’s crucial to update all related contracts and insurance records. Since your LLC is now the legal landlord, you must revise leases, tenant notices, and insurance policies to reflect this change. Neglecting these updates could leave your personal assets vulnerable, as an umbrella policy won’t fully protect your investments on its own, even if the title transfer was handled correctly.

Assign Leases to the LLC

Your existing tenant leases likely still list you as the landlord, but the LLC now legally owns the property. You have two ways to address this: either issue new leases naming the LLC as the "landlord" or "lessor", or assign the current leases to the LLC. Whichever route you choose, make sure the LLC is clearly listed on all documents.

"Once the property is transferred to the LLC, you’re no longer the landlord. The LLC is." – Realized

If you’re in the middle of a lease term, assigning the lease is often the easier option. Draft a short assignment agreement that transfers all rights and responsibilities under the lease from you to your LLC. Both you (as the original landlord) and the LLC should sign this document, and it should be filed with your LLC records.

Once the lease updates are complete, the next step is to notify your tenants.

Notify Tenants of the Ownership Change

Send written notice to your tenants about the ownership change. This notice should include the LLC’s updated contact information and details for rent payments.

Make sure all rent payments go directly to the LLC’s business bank account. Mixing personal and business funds can weaken your liability protection. The name on checks or digital payment platforms should match your LLC’s legal name exactly.

After notifying tenants, don’t forget to update your property insurance.

Update Your Property Insurance

After transferring the property title, contact your insurance agent to update the "named insured" on the policy from your name to the LLC. For rental properties, you’ll need landlord insurance (also known as dwelling fire insurance).

"You need landlord insurance, not homeowners insurance, to protect your asset when it’s being used as a rental." – Ramsey Solutions

Depending on the insurer, you may need to switch to a commercial policy, which is common for properties owned by an LLC. Be aware that landlord insurance premiums may be higher. Additionally, update any utility accounts and service contracts to the LLC’s name to keep everything aligned with corporate formalities.

Tax and Banking Requirements for LLC-Owned Properties

Once your rental property is under your LLC’s name, two essential steps come next: setting up a dedicated bank account and handling tax obligations. These tasks are crucial for maintaining liability protection and staying on the right side of IRS regulations.

Open a Separate LLC Bank Account

A separate bank account for your LLC is non-negotiable. Mixing personal and business funds could jeopardize your liability protection by "piercing the corporate veil", leaving your personal assets exposed.

"The court will respect your LLC as much as you do. Treat it like a business, and it will protect you like one." – Toby Mathis, Founder, Anderson Business Advisors

To open an LLC bank account, you’ll need the following:

- Articles of Organization for your LLC

- Employer Identification Number (EIN) from the IRS

- Physical business address (banks will not accept a PO Box or virtual mailbox)

- Operating Agreement (required by many banks)

- Valid photo IDs for all LLC members

Providing a valid physical address is critical. Banks may suspend your account if this requirement isn’t met.

If you own multiple rental properties under separate LLCs, it’s wise to create individual accounts for each LLC. This approach keeps liabilities and finances separate, making bookkeeping easier. All rent payments should go into the LLC’s account, and any property-related expenses – like mortgage payments, repairs, and insurance – should be paid from the same account.

Once your banking is set up, focus on getting your taxes in order.

File Your LLC Taxes Correctly

Rental LLCs are considered pass-through entities, meaning the income and losses are reported on your personal tax return. How you file depends on your LLC’s structure:

- Single-member LLCs report rental income on Form 1040, Schedule E, Part I.

- Multi-member LLCs file as partnerships using Form 1065 and issue a Schedule K-1 to each member.

You might also qualify for the Qualified Business Income (QBI) deduction, which allows eligible LLC owners to deduct up to 20% of their qualified business income. To support any deductions in case of an audit, keep detailed records of all income and expenses, including receipts, canceled checks, and bills.

It’s important to note that repairs are fully deductible in the year they’re paid, while property improvements must be depreciated over several years using Form 4562.

Lastly, be aware of state-specific fees. Some states charge annual fees or franchise taxes simply for operating an LLC. For instance, California imposes an $800 annual fee, regardless of whether your LLC is profitable.

Conclusion: How to Title Rental Properties in an LLC Without Problems

Transferring a rental property to an LLC can be a smooth process if you approach it step by step. The first and most important action is to contact your lender. Why? Because skipping this step could activate the due-on-sale clause, potentially jeopardizing your financing. Getting written approval from your lender ensures you’re clear to move forward.

Once you’ve secured your lender’s approval, the next steps are straightforward: forming an LLC for rental property, apply for an EIN, and record the deed under the LLC’s name. Don’t forget to update your insurance policy to reflect the LLC as the new owner. Ignoring this could lead to denied claims, even if your premiums are fully paid. Also, make sure to reassign any existing leases to the LLC to avoid legal complications.

Finally, open a separate bank account for your LLC. Keeping personal and business funds separate is critical to maintaining your limited liability status. Mixing funds could lead to "piercing the corporate veil", which puts your personal assets at risk. By following these steps, you can transfer your rental property to an LLC without unnecessary problems.

FAQs

What is a due-on-sale clause, and how could it impact my mortgage when transferring a property to an LLC?

A due-on-sale clause is a provision found in most mortgage agreements that gives the lender the right to demand full repayment of the loan if the property is sold or its ownership changes. This includes situations like transferring the title to an LLC, which could activate the clause.

If the lender enforces this clause, they can require the remaining loan balance to be paid immediately, which might create financial challenges. That said, there are exceptions to this rule – such as transfers resulting from inheritance or divorce. To steer clear of any surprises, it’s crucial to carefully review your mortgage terms and seek advice from a legal or financial professional before moving property into an LLC.

How can I keep my insurance policy valid after transferring my rental property to an LLC?

If you’re transferring a rental property to an LLC, it’s crucial to update your insurance to reflect the new ownership. Inform your insurer about the change as soon as possible. Ask for an endorsement to update the policy’s named insured to the LLC, and if your lender requires it, ensure you or the LLC’s manager is listed as an additional insured. This ensures your current coverage – like limits, deductibles, and discounts – stays intact.

Also, make sure the lender’s interest is correctly documented. Update the mortgagee clause to name the lender as a loss-payable entity under the LLC. To avoid any errors, provide your insurer with a copy of the recorded deed or assignment. Lastly, always get written confirmation from your insurer that your policy is active and valid under the LLC’s ownership. This step is essential to avoid unexpected gaps in coverage.

What tax considerations should I know before transferring a rental property to an LLC?

Transferring a rental property to an LLC is generally considered a non-taxable event if the LLC is a single-member entity owned solely by you. In this situation, the property’s tax basis and depreciation history remain unchanged, and you’ll continue reporting rental income and expenses on your personal tax return as usual. However, if the LLC has multiple members, the transfer might be classified as a sale, which could result in taxable gains.

Since LLCs are treated as pass-through entities by default, any rental income, expenses, and deductions – like mortgage interest or property taxes – flow directly to the owners’ personal tax returns. While this type of transfer doesn’t introduce new federal tax benefits, there may be state-level costs to consider, such as deed transfer taxes or recording fees. Additionally, transferring the property could trigger a "due-on-sale" clause in your mortgage agreement. To avoid potential issues, it’s essential to discuss your plans with both your lender and a tax professional before moving forward.