If your small business uses cryptocurrency – whether for payments, trading, or investments – understanding tax rules is crucial. The IRS treats digital assets like property, meaning every transaction (selling, trading, or spending) can result in taxable income. Starting with your 2025 tax return, businesses must answer a mandatory "digital asset" question on federal tax forms, even if no crypto transactions occurred. Misreporting can lead to penalties, especially with the new Form 1099-DA for crypto transaction reporting.

Here’s a quick breakdown of what you need to know:

- Taxable Events: Selling crypto, trading one crypto for another, using crypto for business expenses, or earning it through mining/staking are all taxable.

- Tax Categories: Capital gains (short-term: 10%-37%, long-term: 0%-20%) and ordinary income (10%-37%).

- Required Forms: Use Form 8949 for gains/losses, Schedule D for summaries, and Schedule C for business income.

- Key Deadlines: File by March 15 (partnerships, S-corps) or April 15 (sole proprietors, C-corps).

Accurate record-keeping is essential. Track cost basis, fair market value, and transaction details to ensure compliance. IRS audits are becoming more stringent, so using crypto tax software like CoinLedger or Koinly can simplify tracking and filing. Stay up to date with the latest IRS changes to avoid penalties and ensure smooth tax filing.

What Cryptocurrency Transactions Are Taxable

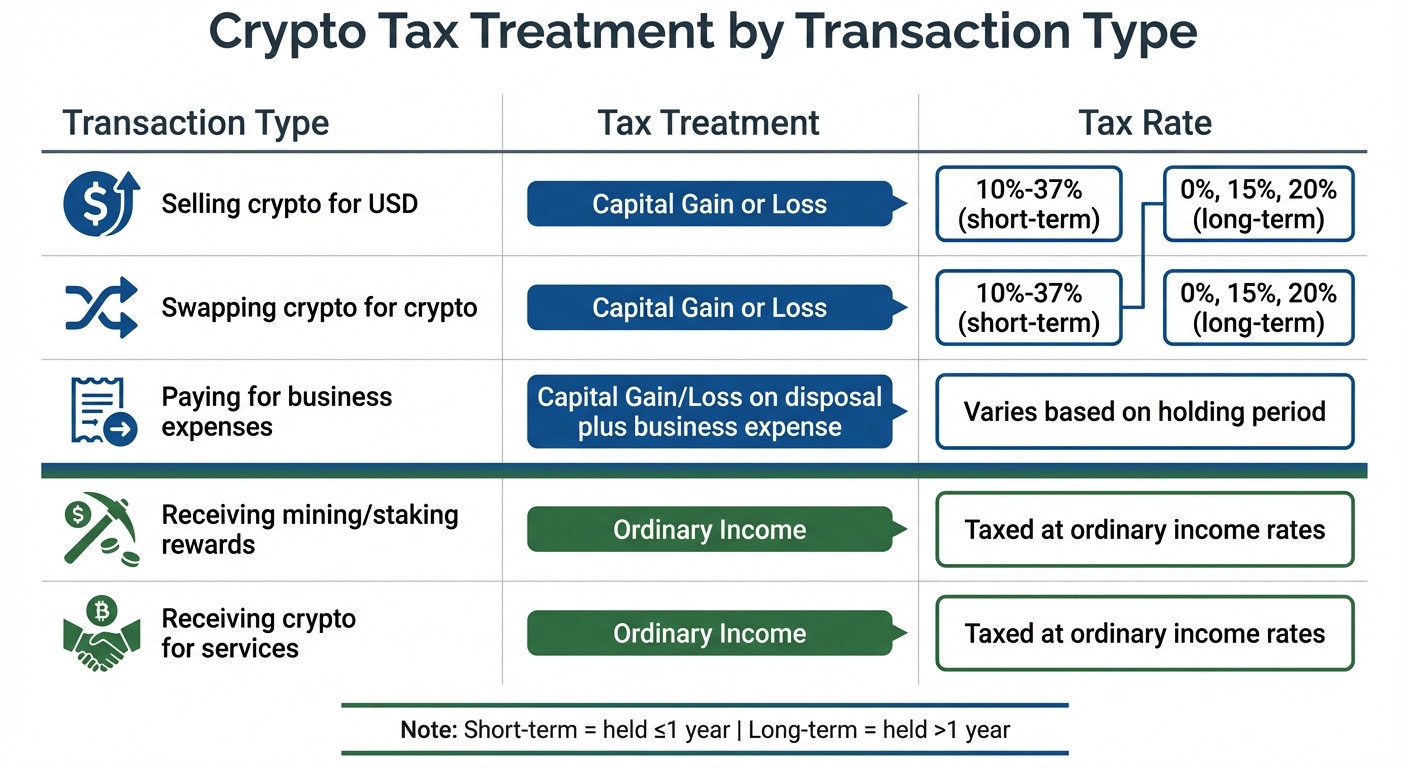

Crypto Tax Treatment by Transaction Type for Small Businesses

The IRS considers cryptocurrency to be property, which means that many activities involving crypto can lead to tax liabilities. Knowing which transactions are taxable is crucial for accurate reporting and avoiding penalties. Below are some common scenarios that may trigger tax obligations.

Selling Cryptocurrency for Cash

Selling cryptocurrency for U.S. dollars or another fiat currency requires you to report a capital gain or loss. This is calculated by subtracting your cost basis (the amount you originally paid) from the sale price.

For example, in April 2023, Mary bought 5 Bitcoins for $50,000. By July 2023, she sold them for $52,000, resulting in a $2,000 short-term capital gain. If you hold cryptocurrency for more than a year before selling, you may qualify for lower long-term capital gains rates (0%, 15%, or 20%, based on your income). However, short-term gains – assets held for one year or less – are taxed at ordinary income rates.

Trading One Cryptocurrency for Another

Exchanging one cryptocurrency for another, such as trading Bitcoin for Ethereum or swapping Bitcoin for a stablecoin like USDC, is also a taxable event. The IRS treats this as if you sold the first cryptocurrency at its fair market value and used the proceeds to buy the new one.

For instance, Bill purchased 5 Bitcoins for $50,000 in April 2023. In June 2023, he traded them for another cryptocurrency worth $40,000 at the time. This resulted in a $10,000 short-term capital loss. Even though no cash was involved, Bill must report the loss by comparing the fair market value of the received crypto to his original cost basis.

Paying for Business Expenses with Crypto

If you use cryptocurrency to pay for business expenses, it triggers two tax events: a capital gain or loss on the disposal of the crypto and a business expense deduction based on the asset’s fair market value.

"When a customer or client pays you in crypto, the income you realize is based on the currency’s fair market value at the time of the transaction and will be included in your gross business income."

- Hayden Adams and Jim Ferraioli, Charles Schwab

For example, if you use Bitcoin purchased for $30,000 to settle a $35,000 invoice, you’d recognize a $5,000 capital gain while also recording a $35,000 business expense deduction.

Earning Crypto from Staking, Mining, or Airdrops

Cryptocurrency earned through mining, staking rewards, or airdrops is treated as ordinary income. Its taxable value is determined by the fair market value at the time you receive it. If you’re running a mining operation as a business, this income might also be subject to self-employment tax.

For example, in 2023, Maria held 10 units of Cryptocurrency A. After a hard fork, she received 10 units of a new Cryptocurrency B, valued at $50 when she gained control. She had to report that $50 as taxable income. If mining is part of your business, you can deduct related expenses like equipment, software, and electricity from your income.

These examples highlight the key taxable events you may encounter. Below is a quick reference table summarizing how different transactions are taxed:

| Transaction Type | Tax Treatment | Tax Rate |

|---|---|---|

| Selling crypto for USD | Capital Gain or Loss | 10%–37% (short-term) or 0%, 15%, 20% (long-term) |

| Swapping crypto for crypto | Capital Gain or Loss | 10%–37% (short-term) or 0%, 15%, 20% (long-term) |

| Paying for business expenses | Capital Gain/Loss on disposal plus business expense | Varies based on holding period |

| Receiving mining/staking rewards | Ordinary Income | Taxed at ordinary income rates |

| Receiving crypto for services | Ordinary Income | Taxed at ordinary income rates |

IRS Forms You Need to Report Crypto Income

When it comes to reporting cryptocurrency activity, the IRS requires specific forms depending on how you use crypto – whether you’re selling, receiving it as payment, or earning it through mining or staking. Here’s a breakdown of the forms you’ll need and when to use them.

Form 8949 for Capital Gains and Losses

Form 8949 (Sales and Other Dispositions of Capital Assets) is where you detail every crypto transaction involving sales, exchanges, or disposals. This includes selling crypto for U.S. dollars, trading one cryptocurrency for another, or spending crypto on goods or services. For each transaction, you’ll need to provide:

- Asset description

- Dates of acquisition and sale/disposal

- Proceeds from the sale

- Cost basis

Starting in 2025, brokers will report gross proceeds from digital asset transactions on the new Form 1099-DA, and by 2026, they’ll also report cost basis for certain transactions. However, if you’ve moved assets between wallets or exchanges, the reported basis may not be accurate. In such cases, you’ll need to adjust the cost basis in column (g) of Form 8949. Once completed, totals from Form 8949 feed directly into Schedule D for your overall capital gains summary.

Schedule D for Capital Gains Summary

Schedule D (Form 1040) consolidates the totals from Form 8949. After entering all transactions into Form 8949, the short-term (Part I) and long-term (Part II) subtotals are transferred to Schedule D. This form calculates your total net capital gain or loss, which then flows into your Form 1040. If your crypto activities generate business income, these details are reported on Schedule C, while other miscellaneous earnings are filed on Schedule 1.

Schedule C for Business Crypto Income

Schedule C (Profit or Loss From Business) is for individuals or small businesses that receive crypto as payment, earn income from mining or staking operations, or sell digital assets as part of their business. Crypto payments should be reported at their fair market value at the time you receive them.

If you accept crypto for business purposes, report it as ordinary income on Schedule C. Later, if you sell that crypto, any resulting gain or loss is reported on Form 8949. If your net profit from these activities exceeds $400, you’ll also need to file Schedule SE to calculate self-employment taxes for Social Security and Medicare.

Schedule 1 for Other Income Sources

Schedule 1 (Additional Income and Adjustments to Income) is for reporting "other income" that isn’t tied to a regular business. This includes airdrops, hard forks, or staking and mining rewards earned as a hobby rather than a business. The distinction is straightforward: use Schedule C for regular, profit-driven activities and Schedule 1 for occasional or hobbyist earnings.

For example, if you receive crypto from an airdrop or hard fork, report the fair market value as ordinary income on Schedule 1 when you gain full control over the assets. Additionally, businesses paying over $600 in crypto rewards must issue Form 1099-MISC.

Starting in 2025, all business tax returns (including Forms 1065, 1120, 1120-S, and 1040/Schedule C) will require a "Yes" or "No" response to whether the business received, sold, exchanged, or disposed of digital assets during the year.

| IRS Form | Purpose for Crypto Reporting | When to Use |

|---|---|---|

| Form 8949 | Report sales or exchanges of crypto held as capital assets | Selling crypto for USD, trading one crypto for another, or using crypto to buy goods |

| Schedule D | Summarize total capital gains and losses | After completing Form 8949 to calculate net gain or loss |

| Schedule C | Report crypto received as business income or sold as inventory | Receiving crypto for services, professional mining/staking, or selling crypto as part of a business |

| Schedule 1 | Report miscellaneous income (staking, mining, airdrops) | Airdrops, hard forks, or hobbyist rewards not tied to a business |

How to Calculate Gains, Losses, and Cost Basis

To figure out your crypto gains and losses, you start with your cost basis – the purchase price of your crypto plus any fees (like gas fees or exchange commissions). When you sell, trade, or spend cryptocurrency, your gain or loss is calculated by subtracting your cost basis from the net amount (fair market value minus transaction costs) [3,25].

For example, if you buy 1 Bitcoin at $30,000 and pay $50 in fees, your cost basis is $30,050. Later, if you sell it for $40,000 but pay $75 in fees, your net proceeds are $39,925. Subtracting your cost basis gives you a $9,875 gain. If you hold the Bitcoin for over a year, you may qualify for lower long-term capital gains tax rates. However, if you sell it within a year, it will be taxed at ordinary income rates. These calculations are essential for accurate reporting on IRS forms.

FIFO, LIFO, and Specific Identification Methods

When selling cryptocurrency, the IRS allows two main methods to determine which units you’ve sold: First-In, First-Out (FIFO) and Specific Identification.

- FIFO is the default method. If you don’t specify which units you’re selling, the IRS assumes you sold the earliest ones you bought. In a rising market, this could mean higher taxable gains because older units are typically cheaper.

- Specific Identification gives you more control. You can select the exact units to sell based on their purchase date, time, and price. This is useful for managing your tax liability – for instance, by selling higher-cost units to reduce gains or by selling at a loss to offset other taxable income. Starting January 1, 2025, the IRS requires that you record the specific units being sold on the same day as the transaction. You won’t be able to change your method after the fact.

While Last-In, First-Out (LIFO) isn’t officially recognized by the IRS, you can achieve a similar result using Specific Identification by selling your most recently purchased units first. This can lower your gains in a rising market, but keep in mind that short-term gains (from assets held under a year) are taxed at higher rates.

"If you do not identify specific units of virtual currency, the units are deemed to have been sold, exchanged, or otherwise disposed of in chronological order beginning with the earliest unit… that is, on a first in, first out (FIFO) basis." – IRS FAQ

Starting in 2025, the IRS will require a "per-wallet" or "per-account" approach. This means you’ll need to track the cost basis for each wallet or account separately. You can’t match a sale on one exchange with a purchase from another. Businesses using custodial brokers can set up standing orders to automate Specific Identification, ensuring compliance with the new rules.

| Method | How It Works | Tax Impact | Best For |

|---|---|---|---|

| FIFO | Oldest units sold first | Higher gains in rising markets | Default; conservative approach |

| LIFO (via Spec-ID) | Newest units sold first | Reduces gains but may trigger higher short-term taxes | Recent purchases in rising markets |

| Specific Identification | Choose exact units to sell | Offers flexibility for tax planning | Businesses wanting precise control |

Deducting Business Expenses Paid in Cryptocurrency

The same cost basis rules apply when you use cryptocurrency to pay for business expenses. The IRS treats this as disposing of an asset, which triggers a capital gain or loss. At the same time, you can deduct the expense based on the fair market value of the goods or services received.

For example, if you pay a contractor $2,000 worth of Ethereum for services, and your cost basis for that Ethereum was $1,500, you’d report a $500 capital gain. Meanwhile, you can deduct the full $2,000 as a business expense. To do this correctly, you need to determine the fair market value of the crypto at the exact time of the transaction. Use either exchange data or a blockchain explorer for peer-to-peer transactions.

Always factor in transaction costs. Add them to your cost basis when purchasing crypto and subtract them from the net proceeds when selling or using it. Keep detailed records of every transaction, including the date, time, number of units, cost basis, and fair market value in U.S. dollars. While the IRS recommends keeping these records for at least three years, holding them for six years provides extra security in case of an audit.

Accurate calculations and record-keeping are essential for correctly reporting crypto transactions on your business tax returns.

Software and Tools for Tracking Crypto Transactions

When it comes to managing crypto transactions, having the right tools can make all the difference. Modern software simplifies the process by syncing data from exchanges and wallets, calculating fair market values (FMV) for transactions, and even generating IRS forms. Keeping accurate records is not just helpful – it’s essential.

Business-focused wallets like BitPay and Copay allow users to export transaction histories as CSV files, making it easy to work with tools like Excel or Google Sheets. For peer-to-peer transactions, blockchain explorers can help determine the FMV at the time of the transaction. Additionally, BitPay’s merchant dashboards provide CSV settlement ledgers, and businesses processing over $20,000 annually receive a 1099-K form.

For a more automated approach, crypto tax software like CoinLedger, CoinTracker, and Koinly can be game-changers. These platforms import transaction histories via API keys, classify transactions (e.g., capital gains, business income, staking rewards), and calculate cost basis using methods like FIFO or LIFO (Specific Identification). For instance:

- CoinLedger serves over 700,000 users and offers tools like "Missing Cost Basis" troubleshooting.

- CoinTracker supports more than 3 million users and integrates with over 10,000 crypto assets.

- Koinly is praised for its fast syncing and easy tax form generation, earning a 4.6/5 rating on Trustpilot.

Looking ahead, Form 1099-DA will become mandatory for custodial brokers and hosted wallet providers starting with the 2025 tax year. This form will report gross proceeds and, eventually, cost basis. Tools like Summ can reconcile these forms with on-chain data to catch any discrepancies. However, don’t assume broker-provided forms are flawless – always double-check using third-party tracking software.

For compliance, keep detailed records of transaction dates, times, unit counts, and FMV in U.S. dollars for at least three years. While tracking software automates much of this, it’s wise to keep original records as backups. Look for tools that support per-wallet tracking and Specific Identification to help minimize tax liability. Many platforms also offer alerts for tax-loss harvesting, helping you identify positions that are currently at a loss.

sbb-itb-ba0a4be

How to File Your Crypto Taxes: Step-by-Step

Filing crypto taxes doesn’t have to feel overwhelming. By breaking it down into manageable steps, even businesses handling a high volume of transactions can navigate the process with confidence.

Step 1: Collect All Transaction Records

Start by gathering all your crypto transaction data for the tax year. You’ll need details like the type of asset, exact date and time, amount in units, fair market value (FMV) in U.S. dollars, and cost basis. For peer-to-peer transactions outside of exchanges, use a blockchain explorer to pinpoint the FMV at the exact time of the transaction.

Step 2: Classify Transactions as Income or Capital Gains

Once your records are in order, classify each transaction as either ordinary income or capital gains/losses. For example:

- Crypto received as payment for goods or services – or earned through mining or staking – counts as ordinary income.

- Selling crypto for cash, trading one cryptocurrency for another, or using crypto to pay for business expenses typically results in a capital gain or loss.

Here’s a quick breakdown for reference:

| Transaction Type | Tax Classification | Reporting Form |

|---|---|---|

| Receiving crypto for services/goods | Ordinary Income | Schedule C or Form 1040 |

| Mining or staking rewards | Ordinary Income | Schedule 1 or Schedule C |

| Selling crypto for U.S. Dollars | Capital Gain/Loss | Form 8949 & Schedule D |

| Exchanging one crypto for another | Capital Gain/Loss | Form 8949 & Schedule D |

| Paying business expenses with crypto | Capital Gain/Loss | Form 8949 & Schedule D |

Keep in mind, the holding period for crypto matters. Assets held for one year or less are considered short-term, while those held longer than a year are classified as long-term.

Step 3: Calculate Fair Market Value at Transaction Time

For every transaction, determine its FMV in U.S. dollars at the time it occurred. If the transaction went through a major exchange, use the USD value provided. For peer-to-peer transactions, the IRS allows values from blockchain explorers that aggregate global indices to calculate the cryptocurrency’s value at the exact date and time. If you receive a new token without a published value, base the FMV on the value of the services you provided.

Step 4: Fill Out IRS Forms and Schedules

Next, consolidate your crypto data into the appropriate IRS forms. Use Form 8949 to report individual capital transactions and summarize totals on Schedule D. Report any crypto income on Schedule C (or Schedule 1 if it’s not business-related).

Step 5: Include Crypto on Your Business Tax Return

Make sure to include all crypto-related transactions on your main business tax return. For instance, income reported on Schedule C flows into Form 1040, while capital gains from Schedule D are filed alongside it. If you’re self-employed, remember that crypto income is subject to a 15.3% self-employment tax on net income, which covers Social Security (up to $176,100 in 2025) and Medicare.

Accurate documentation is key. The IRS requires taxpayers to maintain records that fully support the positions they take on their returns. Keep all documentation related to acquisitions, sales, and transfers for at least three years.

Step 6: File and Pay by the Deadline

Finally, ensure you file and pay any owed taxes on time. Filing deadlines vary by business type: partnerships and S-corporations typically file by March 15, while sole proprietors and C-corporations have until April 15. Missing these deadlines can lead to penalties and interest, so plan ahead.

If taxes are owed, pay by the deadline to avoid additional charges. Note that the IRS can audit returns for up to six years if you overstate your cost basis by 25% or more. If you need more time to file, you can request an extension – but remember, an extension only applies to filing, not to paying taxes owed.

Recent IRS Changes and Compliance Updates for 2025-2026

The IRS has rolled out new cryptocurrency reporting rules that will reshape how small businesses handle and report digital asset transactions. Starting January 1, 2025, brokers and payment processors will need to use Form 1099-DA to report crypto transactions. This replaces the previous mix of reporting methods, aiming for a more uniform system. These updates also reinforce the importance of accurate unit identification when calculating gains and losses.

The new reporting rules will be introduced in phases. For transactions in 2025, brokers are required to report gross proceeds on Form 1099-DA, though reporting the cost basis remains optional at this stage. By 2026, both gross proceeds and cost basis must be reported for digital assets held in custodial accounts. Additionally, real estate professionals acting as brokers will need to report the fair market value of any digital assets used in property purchases for closings starting January 1, 2026.

The IRS has also expanded the definition of "broker" to include processors of digital asset payments (PDAPs). This means that small businesses accepting cryptocurrency through these payment processors will see their transactions automatically reported. To ease the transition, Revenue Procedure 2024-28 allows businesses to allocate unused cost basis to digital assets held as of January 1, 2025.

There’s some flexibility for businesses during the rollout. For transactions in 2025, penalties for failing to file Form 1099-DA will not be enforced if brokers can demonstrate a "good faith effort" to comply. However, certain complex transactions – like staking, lending, short sales, and wrapping – are temporarily excluded from Form 1099-DA reporting under Notice 2024-57. Even though these are exempt from the new form, they are still taxable, so businesses must track and report them separately.

Another key update involves identifying crypto units sold. Starting January 1, 2026, taxpayers will need to specify the units sold using either broker-assigned identifiers or a pre-set standing order. To manage your tax outcomes, it’s crucial to set your preferred lot ordering method before the year ends.

Common Mistakes and How to Avoid Penalties

Small businesses often make critical errors when reporting cryptocurrency income, which can lead to penalties from the IRS. One common misconception is that cryptocurrency transactions are anonymous. While many believe digital assets are untraceable, the IRS actively uses blockchain analytics and subpoenas to track taxpayers. For example, in June 2023, a court required Kraken to provide the IRS with U.S. user lists and transaction histories.

Another frequent mistake involves failing to report crypto-to-crypto transactions. Swapping Bitcoin for Ethereum or converting to stablecoins counts as a taxable event. Businesses filing Form 1065, Form 1120, or Form 1120-S must answer a "Yes/No" question about digital asset transactions. Marking "No" when crypto was received for services is a serious violation that could trigger an audit. Keeping detailed records is essential to avoid further complications.

"The Internal Revenue Code and regulations require taxpayers to maintain sufficient records to establish the positions taken on federal income tax returns." – IRS

Missing cost basis documentation is another major issue. Without proof of the original purchase price for an asset, the IRS might treat the entire sale amount as taxable gain, significantly increasing tax liabilities. To avoid this, regularly download and securely store transaction records. Since platforms may become inaccessible over time, saving records promptly is crucial. While the IRS generally recommends keeping records for three years, holding them for seven years provides more robust audit protection.

Misclassifying income is another area that often leads to audits. For example, reporting staking rewards or mining proceeds as capital gains instead of ordinary income can raise red flags. Additionally, losses on frozen accounts or assets tied up in bankruptcies, such as Celsius or FTX, cannot be claimed until there is a "closed and completed transaction", like a final settlement. It’s worth noting that capital losses can only offset up to $3,000 of ordinary income per year, with any remaining losses carried forward indefinitely.

Relying too heavily on tax software without manual review is another pitfall. Automated tools may miss transactions from specific blockchains (like Solana), misclassify wallet-to-wallet transfers as taxable sales, or fail to recognize internal transfers between your own wallets. To avoid these errors, manually review software-generated reports and ensure internal transfers are correctly labeled as non-taxable. Additionally, converting a portion of earned cryptocurrency to cash immediately can help cover tax liabilities, as crypto is taxed at its fair market value upon receipt – even if its value decreases later. By following these practices, businesses can ensure accurate reporting and steer clear of costly penalties.

Conclusion

Managing crypto taxes becomes simpler when you understand that the IRS views digital assets as property. This means every sale, trade, or payment involving cryptocurrency has tax consequences. Whether you’re selling Bitcoin for cash, swapping one cryptocurrency for another, or using crypto to pay a vendor, keeping detailed and accurate records is a must.

With the IRS introducing Form 1099-DA for increased transparency, it’s crucial to cross-check your records with broker statements to avoid discrepancies that could lead to audits. Document each transaction with the date, amount, and its U.S. dollar value at the time it occurred, and hold onto these records for at least three years. Use specific identification methods to track your cost basis and distinguish between capital assets and business income to ensure you’re filing the right forms.

To protect your business from penalties, focus on compliance and stay organized. Answer the digital asset question truthfully on all tax forms, classify your income correctly, and avoid waiting until the last minute to sort your records. Following these practices not only simplifies compliance but also reduces the risk of audits.

Stay up to date with IRS regulations and consider using specialized crypto tracking software to automate transaction tracking. This approach helps minimize errors and ensures your business remains on steady financial footing. By leveraging reliable software, you can reconcile records efficiently and reduce the stress of managing crypto taxes.

FAQs

How do I report crypto payments my business receives?

When it comes to cryptocurrency payments, the IRS has clear guidelines you need to follow. If you receive digital currency as payment for goods or services, you must report it as income on your tax return. Be sure to record the fair market value of the cryptocurrency at the time you received it. This value should also be documented on your business tax forms, like Schedule C.

Additionally, if your business receives more than $10,000 in digital assets, you may need to file Form 8300 within 15 days to meet federal reporting requirements.

Do wallet-to-wallet transfers create taxable events?

Wallet-to-wallet transfers are generally not taxable unless they involve a sale, exchange, or some other form of disposing of cryptocurrency. If that’s the case, the transaction could trigger tax obligations. It’s important to carefully evaluate the purpose and context of your transfer to determine whether it qualifies as a taxable event.

What records should I keep to prove crypto cost basis?

To properly document your crypto cost basis, it’s crucial to maintain detailed records for every virtual currency transaction. Here’s what you should keep track of:

- Date and time of acquisition: When you purchased or received the cryptocurrency.

- Purchase price: The amount you paid for each unit, also known as the cost basis.

- Date and time of sale, exchange, or disposal: When you sold, traded, or otherwise got rid of the cryptocurrency.

- Fair market value: The value of the cryptocurrency at the time you acquired it and when you disposed of it.

- Proceeds from the transaction: The total amount you received from selling, exchanging, or disposing of the cryptocurrency.

Keeping these records organized and accurate is key to meeting IRS requirements and avoiding potential issues down the line.