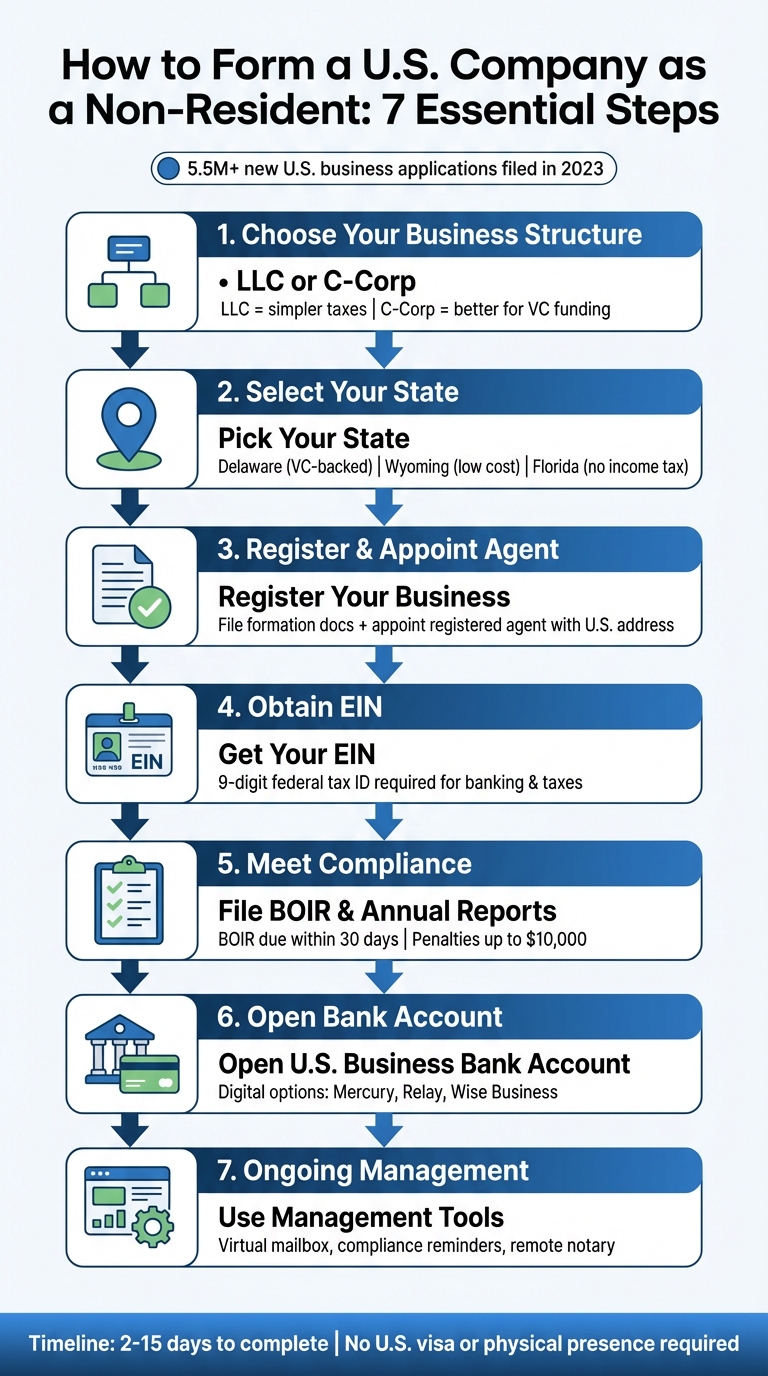

Starting a U.S. company as a non-resident is easier than you might think. You don’t need a visa or physical presence to get started. Here’s a quick breakdown of the process:

- Choose a business structure: LLC (simpler taxes, fewer formalities) or C-Corp (better for raising venture capital).

- Pick a state: Delaware (investor-friendly), Wyoming (low cost, strong privacy), or Florida (no personal income tax).

- Register your business: File the necessary documents and appoint a registered agent with a U.S. address.

- Get an EIN: Essential for taxes and opening a U.S. bank account.

- Meet compliance requirements: File the Beneficial Ownership Information Report (BOIR) and annual state filings.

- Open a U.S. bank account: Options include digital banking platforms like Mercury and Wise for remote access.

- Use tools to simplify management: Services like BusinessAnywhere handle registration, compliance, and virtual mailboxes.

This step-by-step approach ensures your business is legally compliant and ready to operate in the U.S. market. Whether you’re launching an online service or aiming to attract U.S. investors, the process is straightforward with the right resources.

Step 1: Choose Your Business Structure (LLC or C-Corp)

Deciding between an LLC and a C-Corp is one of the first big steps when starting your business. Both offer personal liability protection, but they differ when it comes to taxes, investor preferences, and management requirements.

An LLC operates with pass-through taxation, meaning profits are taxed only once on the owners’ personal income tax returns, avoiding corporate-level taxes. This makes it a solid choice if you’re aiming for a straightforward setup without the need for venture capital. It also comes with fewer formalities, keeping things simple.

A C-Corp, on the other hand, is taxed at both the corporate level and again on dividends (double taxation). Despite this, many foreign founders lean toward this structure because it keeps their personal information off direct IRS records. As Richard Hartnig, Tax Advisor and Lawyer at Schwartz International, points out:

"Foreign individuals are very, very hesitant to put their names on the U.S. tax rolls".

If you’re planning to raise venture capital, offer stock options to employees, or reinvest profits into your business, a C-Corp is typically the better fit. It allows for issuing unlimited stock and multiple share classes, which appeals to investors.

Important note: Non-residents cannot be shareholders in an S-Corp, so this structure is off the table for foreign founders.

LLC vs. C-Corp: Key Differences

Here’s a quick comparison to help you decide:

| Feature | LLC | C-Corp |

|---|---|---|

| Taxation | Pass-through taxation (profits taxed on personal returns) | Double taxation (corporate level and dividends) |

| Ownership Rules | No residency requirements for members | No residency requirements for directors/officers |

| Investor Appeal | Limited; not ideal for venture capital | High; preferred by venture capitalists due to stock flexibility |

| Complexity | Simple, with minimal formalities | More complex, requiring a board of directors and regular meetings |

| Annual Costs | Generally lower; depends on the state | Higher due to additional compliance and filings |

| Tax Privacy | Owners report income directly | Corporation files taxes, offering more privacy for owners |

If simplicity and minimal formalities are your priorities, an LLC is a great option. But if you’re aiming to build a venture-backed startup or want to keep your personal details off U.S. tax filings, a C-Corp might be the better route. Either way, consulting a tax professional with expertise in international tax treaties is essential to navigating non-resident taxation.

Once you’ve chosen your structure, your next step is picking the right state for incorporation.

Step 2: Select Your State of Incorporation

The state you choose for incorporation affects fees, taxes, privacy, and how appealing your business is to investors. For international founders, Delaware, Wyoming, and Florida are popular options.

Delaware is the go-to for venture-backed startups. More than 68% of Fortune 500 companies are incorporated here because of its business-friendly legal and tax environment. The state’s Court of Chancery, focused exclusively on business law, ensures clarity and consistency in corporate litigation. If you plan to raise venture capital or issue stock options, investors will likely expect you to incorporate in Delaware.

Wyoming stands out for its strong privacy protections and low costs. There’s no state income tax, the annual fee is just $60, and ownership details don’t need to be publicly disclosed. As Vincenzo Villamena, CPA and CEO of Entity Inc., puts it:

"If you’re a non-US resident launching an online business, Wyoming offers the best balance of cost, privacy, and simplicity."

Florida is a practical choice for businesses targeting the U.S. market or with a physical presence in the country. The state offers no personal income tax and access to a large domestic market, making it ideal for businesses that require local infrastructure. However, if you incorporate in one state but operate in another, you may need to register for foreign qualification, which can bring extra fees and compliance requirements.

Here’s a quick comparison of these states:

State Comparison for Non-Residents

| Feature | Delaware | Wyoming | Florida |

|---|---|---|---|

| Initial Filing Fee | $110 | $100 | $125 |

| Annual State Fee | $300 (flat tax) | $60 (minimum) | $138.75 |

| State Income Tax | None (for non-residents) | None | None (personal) |

| Privacy Level | Moderate | High (owners not disclosed) | Moderate |

| Best For | Funded startups, C-Corps | Online businesses, consultants | Businesses with U.S. physical presence |

| Investor Appeal | Very high | Low to moderate | Moderate |

For online businesses or freelancers: Wyoming’s low fees, zero state income tax, and strong privacy protections make it a top contender.

For real estate or physical operations: Incorporating in the state where your property or office is located can save you from extra costs. Nikki Nelson, Customer Service Manager at BizFilings, explains:

"The added costs of fulfilling the ongoing business entity law and taxation requirements imposed by two states… often outweigh the perceived benefits of forming a corporation or LLC outside the state where the business is located."

Take these examples: An entrepreneur from India chose Wyoming for an e-commerce business using Stripe and Amazon to handle U.S. sales, benefiting from the state’s affordability and privacy without needing a physical U.S. address. On the other hand, a founder from Germany incorporated in Delaware to attract U.S. investors, later converting the LLC to a C-Corp to secure venture capital funding.

Once you’ve picked your state, the next step is registering your business and naming a registered agent. Choosing the best registered agent service is critical for maintaining compliance and privacy.

Step 3: Register Your Business and Appoint a Registered Agent

Once you’ve picked your state, the next step is to officially register your business in the U.S. This involves filing the necessary formation documents: Articles of Organization for an LLC or Articles of Incorporation for a C-Corp.

These documents require key details, such as your business name, a U.S. address, the purpose of your business, and the name and physical address of your registered agent. To ensure flexibility as your business evolves, it’s a good idea to use a broad business purpose statement. Before filing, check your state’s online entity search tool to confirm your business name is available – this can save you from unnecessary delays. Once that’s done, you’ll need to appoint a registered agent who complies with state requirements.

What Is a Registered Agent and Why Do You Need One?

Every U.S. business must designate a registered agent. This is a person or company with a physical street address in the state where your business is incorporated. Their job is to receive important documents on your behalf, such as legal notices, tax forms, government correspondence, and lawsuit notifications. The registered agent must be available during standard business hours to accept hand-delivered paperwork. According to the Virginia State Corporation Commission:

"This person or company accepts official paperwork such as service of process (lawsuits) and annual registration fee notices."

For international founders who don’t have a U.S. address, hiring a professional registered agent service is the most practical solution. Many states allow you to file your documents online, though some still accept mail or fax submissions. Filing fees vary widely, ranging from $50 to $500, depending on the state.

How BusinessAnywhere Simplifies Registration

BusinessAnywhere makes the registration process easier by handling the filing of your formation documents at no additional cost – you only pay the state filing fees. They also provide a free first-year registered agent service, assigning an agent with a physical U.S. address to ensure compliance. Through their platform, you can manage compliance tasks effortlessly via a centralized dashboard with automated reminders. After the first year, the registered agent service renews at $147 annually.

Once your business is registered, the next step is obtaining an EIN.

Step 4: Obtain an EIN (Employer Identification Number)

An Employer Identification Number (EIN) is a nine-digit federal tax ID issued by the IRS, essentially serving as a Social Security Number for your business. It’s a must-have for opening a U.S. business bank account, which can be a major hurdle for international founders. Beyond that, it’s essential for hiring employees, filing taxes, and securing business licenses and permits.

If you’re a non-resident, you’ll also need an EIN to handle tax withholding on payments to non-resident aliens. The good news? The IRS doesn’t charge a fee for issuing an EIN. However, international applicants face a snag: the IRS online application tool isn’t an option if your principal place of business is outside the U.S.. Instead, you’ll need to apply by phone, fax, or mail using IRS Form SS-4.

Here’s how to get it done:

- By phone: Call the IRS at 267-941-1099 (Monday through Friday, 6:00 a.m. to 11:00 p.m. ET) for immediate issuance.

- By fax: Send your completed Form SS-4 with a return fax number, and you’ll typically get a response within four business days.

- By mail: This method takes longer – around four weeks.

Keep in mind, the IRS limits EIN issuance to one per responsible party per day.

Important Tips for EIN Applications

Before applying, make sure your business is registered with the state. The IRS won’t process your EIN application until your business registration is complete. Also, double-check your business name for compliance with IRS-approved characters: stick to A–Z, 0–9, hyphens, and ampersands. If your name includes symbols like "+" or "@", you’ll need to spell them out.

Once your state registration is sorted, securing your EIN is the next step. If you’re feeling overwhelmed, services like BusinessAnywhere can handle the process for you.

EIN Application Through BusinessAnywhere

For $97, BusinessAnywhere offers a hassle-free EIN application service tailored for non-residents. They’ll take care of filing Form SS-4 and coordinating with the IRS, which can save you time and minimize the chances of errors – especially since international applicants can’t use the IRS’s faster online portal.

sbb-itb-ba0a4be

Step 5: Meet Compliance Requirements (BOIR and Annual Filings)

After registering your company and securing your EIN, two essential compliance tasks await: the Beneficial Ownership Information Report (BOIR) and annual state filings. These steps aren’t optional – they’re legal obligations designed to keep your business in good standing and help you avoid hefty penalties.

The BOIR is a federal requirement under the Corporate Transparency Act of 2021. It mandates that you disclose all beneficial owners – individuals who own at least 25% of your company or have significant control. This report must be submitted to the Financial Crimes Enforcement Network (FinCEN), part of the U.S. Department of the Treasury, within 30 days of receiving your formation notice.

Unlike the BOIR, which is typically a one-time filing unless ownership changes, annual state filings are recurring. Most states require you to update details such as your business address and registered agent annually or biennially. These filings often come with an annual franchise tax. Missing these deadlines can result in penalties, losing your "good standing" status, or even administrative dissolution of your business.

The consequences for failing to file the BOIR are severe. Civil penalties can exceed $500 per day, with fines reaching up to $10,000 and potential imprisonment for up to two years. As CPA Thomas J. Bulger explains:

"It is a small business reporting requirement with potential penalties including prison for committing a felony by not reporting".

To complete the BOIR, you’ll need to provide a valid, non-expired passport or driver’s license image for every beneficial owner. Note that P.O. boxes or third-party addresses are not accepted. Staying ahead of these requirements can save you from unnecessary risks.

BusinessAnywhere’s Compliance Support

For only $37, BusinessAnywhere can handle your BOIR filing, managing the paperwork and coordinating with FinCEN. This service is a cost-effective alternative to hiring a CPA, which usually costs around $350 per entity. BusinessAnywhere also offers automated reminders for your annual state filings, ensuring you never miss a deadline. If your ownership details change, you’re required to file an updated BOIR within 30 days – BusinessAnywhere simplifies this process, too.

Step 6: Open a U.S. Business Bank Account

Once you’ve completed the necessary filings and secured your EIN, the next critical step is setting up a U.S. business bank account. This step is essential for managing your company’s finances and maintaining a proper business framework. However, for international founders, this process can be tricky due to strict federal regulations like AML (Anti-Money Laundering) and FATCA (Foreign Account Tax Compliance Act). As Vincenzo Villamena, CPA and CEO of Entity Inc., explains:

"The most frustrating part isn’t forming the company, it’s opening a US business bank account."

Challenges of Traditional Banking for Non-Residents

Most traditional banks require you to visit a branch in person to open an account. For non-residents, this isn’t always feasible. To proceed, you’ll need to gather several key documents, including:

- A valid passport

- Proof of business registration (like Articles of Incorporation or Organization)

- EIN confirmation letter

- Your Operating Agreement or Bylaws

Additionally, banks will ask for a physical U.S. address. If you don’t have one, you can use the address of your registered agent (see our registered agent checklist) or a best virtual mailbox services.

Remote Banking Options for International Founders

Fortunately, you don’t have to rely solely on traditional banks. Digital banking platforms like Mercury, Relay, and Wise Business allow non-resident business owners to open accounts remotely. These platforms are designed with international founders in mind and offer streamlined onboarding processes. Here’s what they bring to the table:

- Mercury: No monthly fees, free domestic and international wire transfers.

- Relay: Ideal for solo business owners and LLCs, with zero monthly fees.

- Wise Business: Excellent for managing multiple currencies, supporting over 50 currencies for global transactions.

With these options, you can often set up an account within a few days without needing a Social Security Number.

Getting Your Documents in Order

Before applying, make sure you have everything ready to avoid delays. This includes:

- Your passport

- Business registration documents

- EIN confirmation letter

- Operating Agreement or Bylaws

- A detailed description of your business, including products, services, and expected transaction volumes

Having these documents prepared will help streamline the application process and improve your chances of approval.

Expert Assistance for a Smooth Setup

If navigating the process feels overwhelming, services like BusinessAnywhere can help. They provide bank account setup assistance, connecting you with banks that specialize in working with international founders. This service ensures your application is complete and can save you significant time and effort.

Once your account is open, remember to use it exclusively for business transactions. This practice is essential for maintaining your company’s limited liability status. Plus, standard FDIC insurance protects deposits up to $250,000 per depositor, giving you added financial security as you grow your U.S. business.

Step 7: Use BusinessAnywhere for Ongoing Business Management

Once your business structure, registration, and banking are set up, you’ll need tools to keep everything running smoothly. BusinessAnywhere offers a centralized solution to help you stay compliant and manage operations efficiently – no matter where you are. Designed specifically for non-residents managing U.S. companies, these tools simplify the complexities of running a business remotely.

Virtual Mailbox for Mail Management

Even in today’s digital age, physical mail remains a critical part of business operations. Important documents from the IRS, state agencies, or banks often arrive via postal service, and missing them could lead to compliance issues.

BusinessAnywhere provides a real U.S. street address in states like Florida, Arizona, New Mexico, or Wyoming – not just a P.O. box. This address can be used for business registration, bank applications, and public records. Starting at $20/month, the virtual mailbox service includes unlimited mail scanning and global forwarding, all managed through a user-friendly dashboard.

Beyond convenience, this service protects your privacy by keeping your personal home address off public records.

Remote Online Notary and Additional Tools

For many, notarizing documents has traditionally meant traveling to a notary in person – a major inconvenience for non-residents. BusinessAnywhere’s remote online notary service removes this obstacle, offering notarization for $37 per session and available 24/7, all year round.

Here’s how it works: create a free account on the dashboard, upload your document, and verify your identity using a government-issued photo ID during a video call. A licensed notary will digitally seal your signature in real-time, and the document will be stored in your dashboard for easy access.

The Digital Nomad Kit

For a comprehensive solution, BusinessAnywhere offers the Digital Nomad Kit. This package includes LLC registration, EIN application, registered agent services, a virtual mailbox, compliance tools, and banking support – all for about $3,200. It’s a cost-effective way to bundle essential services compared to purchasing them individually.

With these tools, you’ll have everything you need to manage your U.S. business remotely while staying compliant with federal and state regulations. Whether it’s handling mail, notarizing documents, or simplifying daily operations, BusinessAnywhere ensures you’re covered, no matter where you are.

Conclusion

Starting a U.S. company as a non-resident is entirely achievable if you follow a clear set of steps. First, decide between forming an LLC or a C-Corp, then pick the best state for incorporation. From there, you’ll need to register your business with a registered agent, obtain an EIN, fulfill compliance requirements like BOIR filing, and set up a U.S. business bank account. Each step lays the groundwork for a strong and legally compliant business.

For international founders, the real challenge often lies in handling these tasks remotely, especially without a U.S. address or Social Security Number. That’s where expert assistance becomes invaluable. Services like BusinessAnywhere simplify the process by offering solutions such as $0 company formation (state fees range from $50 to $500) and ongoing compliance management, including deadline reminders.

The numbers speak volumes about the opportunities in the U.S. business ecosystem. In 2023 alone, over 5.5 million new business applications were filed, highlighting the momentum of entrepreneurship. Tools like the Digital Nomad Kit, which bundles essential services – business registration, EIN application, registered agent, virtual mailbox, and compliance tools – can streamline the process for around $3,200.

You don’t need a physical presence in the U.S. to operate successfully. With the right resources, you can manage everything remotely while adhering to federal and state regulations. Whether your goal is to access U.S. payment processors, establish credibility with American clients, or ensure personal asset protection through limited liability, the groundwork you lay now will support your business for years to come.

The process is faster than you might think. In as little as 2 to 15 days, you could have your EIN, business bank account, and virtual mailbox ready to go. Take the first step today and start your U.S. business journey – no matter where you are in the world.

FAQs

Can a non-resident start a business in the U.S. without a visa?

Yes, non-residents can legally start and own a company in the U.S. without needing a visa. You can run your business remotely from outside the country. However, if you plan to physically work or manage your business within the U.S., you’ll need a visa.

Starting a U.S. company as a non-resident involves several steps. First, you’ll need to decide on a business structure, such as an LLC or C-Corp. Then, you’ll register your company and obtain an EIN (Employer Identification Number). While being physically present isn’t required, it’s crucial to familiarize yourself with the legal and financial obligations to ensure everything goes smoothly.

What’s the difference between an LLC and a C-Corp for international founders?

When deciding between an LLC and a C-Corp, international founders should consider factors like ownership rules, taxation, and growth opportunities.

A C-Corp is often the go-to option for businesses aiming to raise capital. It allows unlimited shareholders, including foreign investors, and can issue multiple classes of stock – making it appealing to venture capitalists and other investors. Additionally, a C-Corp is taxed as a separate entity from its owners, which can simplify international tax compliance.

An LLC, on the other hand, operates as a pass-through entity. This means the profits and losses are reported directly on the owners’ personal tax returns. LLCs are generally easier and less costly to establish and maintain. However, some states impose restrictions on foreign ownership, and LLCs are usually less attractive to investors compared to C-Corps.

Ultimately, the choice depends on your specific goals. If your focus is on scaling and attracting investors, a C-Corp might be the better fit. For businesses prioritizing simplicity and lower regulatory hurdles, an LLC could be the way to go.

Can non-residents open a U.S. business bank account remotely?

Yes, non-residents can set up a U.S. business bank account remotely, but it takes some planning and preparation. Banks typically require key documents, including Articles of Incorporation or Formation, a valid passport for the authorized signer, and an Employer Identification Number (EIN). Depending on the bank, there may be additional requirements based on their internal policies.

While the exact process differs by institution, many banks now offer remote account setup if you submit all the necessary paperwork electronically. One thing to note: obtaining an EIN can take 4–6 weeks, so it’s important to account for that timeline. To make the process easier, you might want to work with financial institutions or services that specialize in helping international entrepreneurs open accounts remotely. With the right approach, securing a U.S. business bank account from abroad is absolutely achievable.