Owning rental property can expose your personal assets – like your home, savings, and car – to legal and financial risks. An LLC (Limited Liability Company) creates a legal barrier between your personal wealth and your rental business, protecting you from lawsuits or debts tied to your property. However, forming an LLC comes with costs, administrative work, and potential financing challenges.

Here’s what you need to know:

- Why an LLC? It protects personal assets from lawsuits and creditor claims related to your rental property.

- Costs: Formation fees range from $100 to $300, with annual fees up to $800 in some states.

- Challenges: LLCs may complicate mortgages and require personal guarantees, which could still expose your assets.

- Who Should Consider It? Landlords with multiple properties, significant personal wealth, or high-risk properties (e.g., short-term rentals).

While an LLC offers strong liability protection, it’s not always the best choice for everyone. Evaluate your financial situation, property portfolio, and state fees when choosing between an LLC vs sole proprietorship before deciding. For landlords with minimal assets or single properties, robust insurance might suffice. Always consult a tax advisor or attorney to make the right call for your circumstances. If you decide to move forward, you’ll need to know how to set up an LLC for real estate properly.

The Risks of Owning Rental Property in Your Personal Name

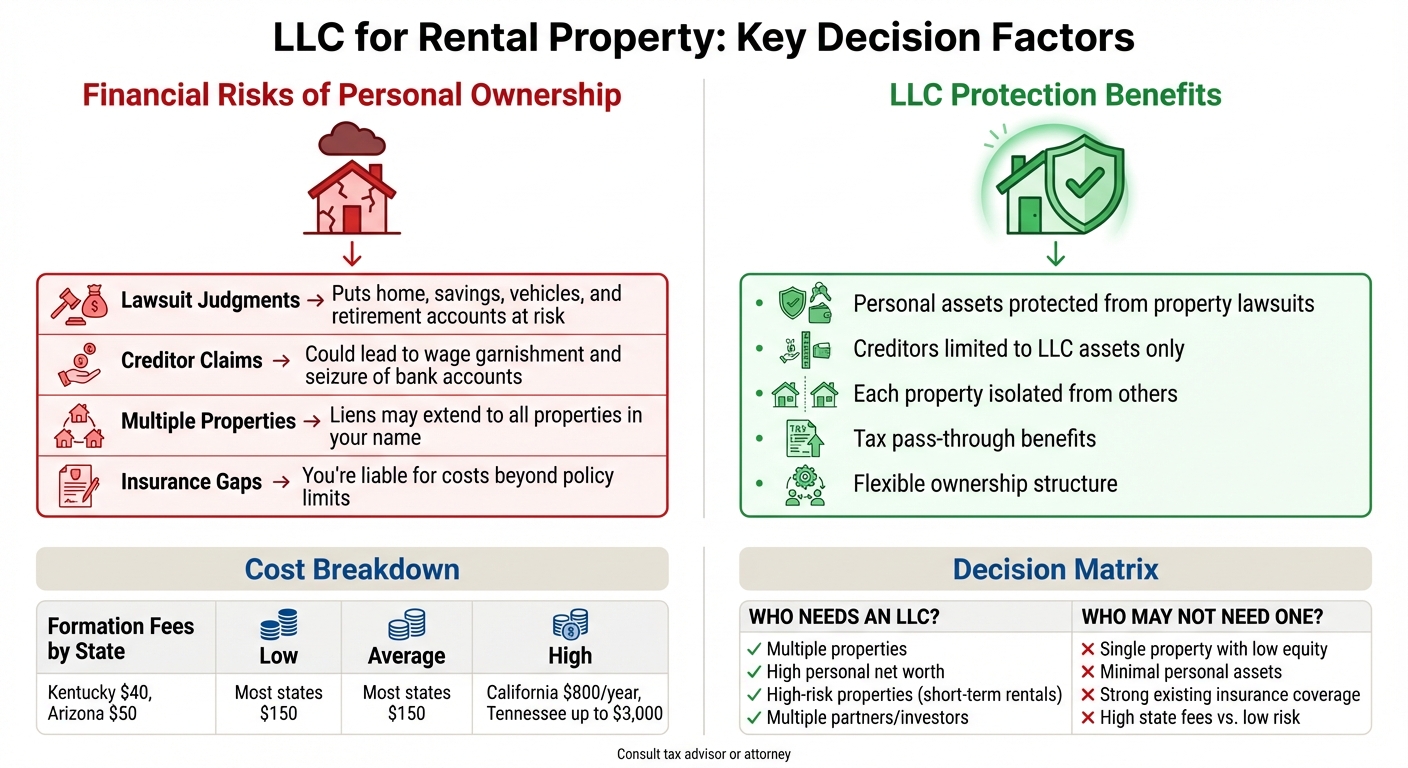

Owning rental property in your personal name puts everything you own – your home, car, bank accounts, and even retirement savings – at risk. If something goes wrong with the property, lawsuits and creditor claims could target your personal assets.

Legal Liability Without an LLC

When you hold property in your name, you’re directly exposed to legal action. Tenant injuries, slip-and-fall accidents, or disputes over security deposits can lead to lawsuits that jeopardize your personal assets.

"If they secured that judgment against you personally in the absence of an LLC, nearly any personal asset could be fair game for them to seize without additional legal defenses." – Daniel Rodriguez, Attorney, Legal Norcal P.C.

It doesn’t stop there. If you handle repairs yourself or hire contractors, you could be held liable for injuries or damages caused by poor workmanship. Additionally, because property ownership is public record, individuals with substantial wealth – such as physicians or attorneys – may become targets for lawsuits based on perceived financial status.

Even if you have insurance, it won’t cover everything. Once a judgment exceeds your policy’s limits, you’re on the hook for the rest, which can lead to hefty out-of-pocket costs.

Legal claims are only one side of the coin. The financial fallout from such claims can be devastating, putting your entire asset portfolio at risk.

Financial Exposure from Property-Related Claims

The financial risks go beyond lawsuits. If you own multiple properties in your personal name, a judgment or lien against one property could ripple across your entire portfolio. In states like California, creditors can attach liens to all real estate you own, including your primary residence, to recover unpaid debts.

Creditors can also garnish wages from your job or seize money from your personal bank accounts to satisfy judgments. If your rental business accumulates unpaid bills, supplier debts, or defaults on mortgages, you’re personally responsible because there’s no legal barrier between your business and personal finances.

Here’s a quick breakdown of the financial risks tied to owning properties in your personal name:

| Risk Factor | Impact on Personal Finances |

|---|---|

| Lawsuit Judgments | Puts your home, savings, vehicles, and retirement accounts at risk |

| Creditor Claims | Could lead to wage garnishment and seizure of bank accounts |

| Multiple Properties | Liens may extend to all properties in your name |

| Insurance Gaps | You’re liable for costs beyond your policy limits |

"If you’re a normal owner of the property, if the tenant wins the case, he could be compensated from your own personal assets and belongings." – Nasser Mansur, Mashvisor

These risks aren’t just hypothetical. A tenant injury claim that exceeds your insurance coverage could wipe out your savings, leaving everything you’ve worked hard to build vulnerable. This highlights why separating your rental business from your personal assets is critical for protecting your financial future.

How an LLC Protects Your Personal Assets

An LLC serves as a protective shield between your rental business and your personal assets. When set up correctly, any legal claims or debts tied to your rental property are limited to the LLC’s assets, leaving your personal bank accounts, home, and retirement savings untouched.

What is an LLC?

A Limited Liability Company (LLC) is a separate legal entity from its owners, who are referred to as members. Once you form an LLC and transfer your rental property into it, the LLC becomes the official landlord. This means the LLC, not you personally, takes on all the rights, responsibilities, and liabilities tied to the property.

This structure has become a popular choice among property investors across the U.S. Setting up an LLC typically costs around $150, though fees vary by state. For instance, Kentucky charges just $40, while in Tennessee, fees can climb to $3,000 depending on the number of members.

"If the property is set up as an LLC, only the LLC’s assets (those related to that specific property) would likely be at risk in the lawsuit. The property owner’s personal assets would be protected because the rental property was established as a separate legal entity."

– Nellie Akalp, CEO, CorpNet

How Liability Protection Works

Here’s how this protection plays out: imagine a tenant files a $200,000 lawsuit after an incident on your property. Only the LLC’s assets – like the rental property and its bank account – would be at risk. Your personal home, car, and savings would remain safe. This protection also applies to employee actions. For example, if a maintenance worker accidentally damages a neighbor’s property, any resulting judgment would be satisfied using the LLC’s assets, not your personal wealth.

Similarly, if the LLC falls behind on supplier payments or defaults on expenses, creditors can only go after the LLC’s assets. They can’t touch your personal wages or place liens on your primary residence.

To maintain this legal separation, it’s essential to avoid mixing personal and business finances. Open a dedicated business bank account for the LLC and use it exclusively for business-related expenses. Additionally, drafting a thorough Operating Agreement and updating all leases to name the LLC as the landlord reinforces the distinction between your personal and business finances.

Understanding these mechanisms is key to evaluating different LLC structures for your rental properties.

Single-Property LLC vs. Series LLC

Now that we’ve covered how liability protection works, let’s dive into how different LLC structures can offer even more asset protection. Property owners often choose between a single-property LLC (one LLC per property) and a Series LLC (a single entity with multiple sub-LLCs). The right choice depends on the size of your portfolio and your budget.

| Feature | Single-Property LLC | Series LLC |

|---|---|---|

| Structure | One LLC per property | One "parent" LLC with multiple "series" (sub-LLCs) |

| Liability Protection | Claims against one property don’t affect others in separate LLCs | Each series has independent assets and liabilities, protecting them from claims tied to other series |

| Administrative Work | Higher – separate filings, fees, and registered agents for each LLC | Lower – one filing and one annual report for the entire structure |

| State Availability | Recognized nationwide | Limited to certain states; for example, California does not allow Series LLCs |

| Best For | Investors with a few properties seeking maximum asset separation | Investors with larger portfolios looking for efficiency and lower administrative costs |

A single-property LLC offers maximum protection by isolating risks to just one property. If legal trouble arises, it won’t spill over to other properties. However, the downside is the cost – separate setup fees, annual maintenance, and registered agent fees can quickly add up for multiple properties.

On the other hand, a Series LLC simplifies management by grouping multiple properties under one parent LLC. Each series functions independently, with its own liability protection, while the overall structure requires only one filing fee and annual report. Keep in mind, though, that Series LLCs aren’t available in every state, and their tax treatment can vary.

Benefits of Using an LLC for Rental Properties

Now that you’ve got a handle on how LLCs work and the different structures available, let’s break down why more than 2 million landlords in the U.S. have chosen this legal entity for managing their rental properties. These benefits can help you make smarter decisions about your rental business.

Protection from Personal Liability

One of the biggest perks of forming an LLC is the shield it creates between your personal assets and your rental business. If a tenant, visitor, or even a creditor files a claim against your property, they can typically go after the LLC’s assets – not your personal savings, home, or retirement accounts. For example, if your LLC defaults on a loan or falls behind on vendor payments, creditors usually can’t touch your personal wages or place liens on assets you own individually. This protection also extends to liabilities caused by co-owners or employees.

However, this safety net only works if you keep your business and personal finances completely separate. That means using a dedicated business bank account for all rental income and expenses. Additionally, you’ll need to transfer the property title into the LLC’s name through a deed. Just forming the LLC isn’t enough to activate these protections.

Tax Benefits and Pass-Through Taxation

LLCs come with some attractive tax perks. Thanks to pass-through taxation, the LLC’s profits and losses go straight to your personal tax return (Form 1040), which helps you avoid double taxation. Plus, you can deduct typical rental property expenses like mortgage interest, property taxes, insurance, maintenance, repairs, and management fees. On top of that, LLC owners may qualify for the Qualified Business Income (QBI) deduction, which lets you deduct up to 20% of your qualified business income.

If you’re part of a multi-member LLC, you can customize profit-sharing arrangements in the Operating Agreement to optimize tax outcomes for members in various tax brackets. And since rental income is usually considered passive income, it’s not subject to self-employment taxes like Social Security and Medicare, potentially leading to significant savings.

Easier Financial Management

An LLC doesn’t just protect your assets – it also makes managing your rental finances a lot simpler. By keeping a separate business bank account, you create a clear line between personal and business funds. This makes bookkeeping easier, simplifies tax preparation, and ensures you don’t miss out on deductible expenses. Plus, using your LLC’s Employer Identification Number (EIN) allows it to establish its own credit history, which can help you qualify for commercial real estate loans without relying on your personal credit.

Collecting rent and handling payments also becomes more streamlined. Tenants can pay the LLC directly through online platforms or business accounts, which often integrate with property management software for automatic transaction tracking. Just remember to update your lease agreements to list the LLC as the landlord and ensure rent checks are made out to the company.

Flexible Ownership and Estate Planning

LLCs also offer flexibility when it comes to ownership and long-term planning. The Operating Agreement outlines how ownership changes, member adjustments, and succession will be handled. This is particularly helpful for estate planning. For example, you can gradually transfer LLC membership interests to family members, which may reduce estate taxes. You can also place the LLC in a Living Trust to ensure a smooth management transition and avoid probate.

For those in joint ownership arrangements – whether with business partners, family members, or investment groups – the Operating Agreement acts as a guide. It clearly defines everyone’s rights, responsibilities, and profit-sharing arrangements, adding structure and professionalism that informal partnerships often lack.

sbb-itb-ba0a4be

Costs and Drawbacks of Forming an LLC

Setting up an LLC comes with upfront expenses, ongoing fees, and administrative responsibilities that landlords should weigh carefully before moving forward.

Formation and Annual Maintenance Costs

The cost of forming an LLC varies depending on the state. Filing fees can range anywhere from $100 to $300, with the average landing around $150. For example, in Tennessee, fees are calculated at $50 per member, with the total ranging from $300 to $3,000.

Once your LLC is filed, you’ll need to appoint a registered agent – a person or service with a physical address in your state to handle legal documents. Choosing the best registered agent service typically costs between $50 and $300 annually. Additionally, many states require annual or biennial reports, with fees ranging from $0 in states like Missouri and New Mexico to as much as $800 in California. California also imposes a mandatory annual franchise tax of $800 on all LLCs, regardless of profitability. In contrast, states like Virginia charge an initial filing fee of approximately $100 and an annual registration fee of about $50.

These costs represent just the starting point when it comes to the financial commitment of forming an LLC.

Mortgage and Financing Challenges

Owning property through an LLC can complicate financing. Banks often treat LLC-owned properties as commercial loans rather than personal residential mortgages, which usually means higher interest rates. Additionally, most lenders require a personal guarantee, putting your personal assets at risk if the LLC defaults.

"If you’re forming the LLC in order to shield your personal assets, the personal guarantee will destroy that protection, which means you’ll have spent a lot of time and money in pursuit of protection that you won’t have." – Christine Mathias, Attorney, Nolo

If you’re transferring a property you already own into an LLC, you might encounter a "due-on-sale" clause in your existing mortgage. This clause allows the lender to demand full repayment of the loan when the title is transferred, potentially forcing you to refinance under less favorable commercial terms.

Ongoing Administrative Requirements

Beyond the initial setup, maintaining an LLC requires consistent administrative work. To preserve the LLC’s legal protections, you’ll need to handle tasks like filing annual or biennial reports with your state, keeping a dedicated business bank account, and maintaining detailed records to clearly separate the LLC’s finances from your own.

For multi-member LLCs, additional tax filings are necessary. This includes submitting IRS Form 1065 and providing Schedule K-1s to each member annually, which often requires the expertise of a CPA.

When transferring property into an LLC, you’ll also need to update the deed, adjust insurance policies, revise lease agreements to name the LLC as the landlord, and potentially secure new business licenses. Some municipalities may even impose deed transfer taxes based on a percentage of the property’s value. These ongoing requirements can add both time and cost to managing property under an LLC.

When Should You Form an LLC for Your Rental Property?

Deciding whether to form an LLC for your rental property depends on your specific circumstances. Factors like the size of your property portfolio, your personal financial situation, and your exposure to potential risks all play a role. Below are some scenarios where forming an LLC could be a smart move.

Situations Where an LLC Makes Sense

LLCs provide legal and financial protections that become increasingly valuable as your rental property portfolio and personal assets grow. If you own multiple properties, setting up separate LLCs for each property can help isolate liability. This means that if one property faces legal issues, the equity in your other properties remains shielded. This setup is especially useful for landlords with substantial personal wealth, such as a primary residence, savings, or investments, who want to safeguard these assets from claims tied to their rental properties.

Properties with higher risks – such as older buildings or short-term rentals with frequent tenant turnover – are particularly well-suited for LLC protection. Additionally, if you’re working with multiple partners or investors, an LLC provides a formal structure. Through an Operating Agreement, you can clearly define roles, responsibilities, and even customize how profits are distributed, which doesn’t necessarily have to align with ownership percentages.

"The larger the rental business, and the lower your tolerance for risk, the more you should consider forming an LLC." – Christine Mathias, Attorney, Nolo

Timing also plays a crucial role. Forming an LLC before purchasing a property can help you avoid complications like triggering due-on-sale clauses in existing mortgages, paying title transfer taxes, or renegotiating lease agreements. However, in states like California, where the annual franchise tax is $800, or if your property has minimal equity and you already have strong landlord insurance, the costs of forming an LLC might outweigh the benefits.

| Factor | Recommended | Not Needed |

|---|---|---|

| Portfolio Size | Multiple properties or commercial units | Single property |

| Personal Assets | High net worth and significant savings | Minimal personal assets |

| Ownership | Multiple partners or investors | Sole owner |

| Financing | New purchase or lender-approved transfer | Existing mortgage with due-on-sale clause |

| State Fees | Low annual fees (e.g., AZ, MO) | High annual taxes (e.g., CA’s $800 minimum) |

How to Form an LLC with BusinessAnywhere

If you’ve decided that forming an LLC is the right choice for your rental property, BusinessAnywhere makes the process simple. They offer LLC formation with $0 service fees, requiring you to pay only the state filing costs, which typically range from $50 to $500 depending on your state. Plus, they include a free first-year registered agent service (a $147 value), giving you a legal address for receiving official documents and compliance reminders.

For an additional $97, BusinessAnywhere can also handle your EIN application, which is essential for opening a business bank account and filing taxes. The entire process is managed through a 24/7 online dashboard, making it especially convenient for remote property owners or digital nomads.

After your LLC is formed, BusinessAnywhere can help you stay compliant with ongoing requirements like filing annual reports and adhering to the Beneficial Ownership Information reporting mandate from FinCEN, which will apply to all LLCs starting in 2024. If you operate in states like Texas, Delaware, or Nevada, you might also consider a Series LLC. This option allows you to manage multiple properties under a single umbrella filing, potentially reducing administrative costs and paperwork.

Conclusion

Deciding whether to form an LLC for your rental property hinges on factors like the size of your portfolio, your net worth, risk tolerance, and the fees in your state. An LLC provides a legal barrier between your personal assets and the liabilities tied to your property. However, this protection only works if you keep your business and personal finances completely separate.

For landlords with multiple properties or significant personal wealth to shield, setting up an LLC often makes sense. While formation and maintenance fees vary by state, they are usually far less than the potential costs of a lawsuit that exceeds your insurance coverage. On the other hand, if you own just one property with minimal equity or live in a state with high fees, such as California, the expenses might not justify the benefits – especially if you already have strong landlord and umbrella insurance policies in place.

"The liability protection, tax flexibility, and estate planning advantages offered by an LLC can be significant… However, lender consent, ongoing costs, and the critical need to maintain corporate formalities should not be overlooked." – Summit Law Group

As Summit Law Group points out, while the benefits of an LLC – like liability protection, tax flexibility, and estate planning – are notable, you must also account for lender approval, ongoing costs, and the need to adhere to corporate formalities. At its core, the main goal of forming an LLC is to safeguard your personal assets. Balancing these pros and cons is essential before making a decision.

Before moving forward, consult with a CPA, tax advisor, or attorney familiar with your state’s laws. They can help you weigh the legal protections against potential challenges like administrative responsibilities, financing hurdles, and compliance requirements, including the Beneficial Ownership Information reporting to FinCEN.

Once you’ve evaluated your options, consider using a service that simplifies the process. If an LLC aligns with your goals, companies like BusinessAnywhere can assist with formation, offering $0 service fees and a free first-year registered agent. Make sure your choice supports your overall investment strategy and protects what matters most.

FAQs

What are the key advantages of setting up an LLC for rental properties?

Forming an LLC for your rental property can provide protection for your personal assets by keeping your personal finances separate from the business. If any legal claims or debts arise related to the property, only the LLC’s assets are at stake. This means your personal savings, home, and other investments remain secure.

An LLC also streamlines tax management. Being treated as a pass-through entity, the LLC allows you to report profits and losses directly on your personal tax return. This setup makes it easier to claim deductions for expenses like depreciation, repairs, and mortgage interest – without dealing with corporate taxes. Plus, if you’re managing joint ownership, an LLC’s operating agreement lets you customize profit-sharing and ownership percentages to suit your needs.

If you own multiple properties, creating a separate LLC for each one can add another layer of protection by isolating liabilities. Beyond the legal and tax advantages, operating under an LLC can also boost your credibility with lenders and tenants, potentially opening doors to better financing options and smoother lease negotiations.

How does forming an LLC protect my personal assets when owning rental property?

Forming a Limited Liability Company (LLC) for your rental property establishes a legal barrier between your personal assets and the property itself. Essentially, if your property encounters a lawsuit, debt, or other financial obligations, only the LLC’s assets are at stake – your personal belongings like your home, savings, or investments stay protected.

By holding your rental property under an LLC, you limit your personal financial risk while retaining flexibility in how you operate your business. That said, it’s crucial to manage the LLC appropriately and comply with all legal requirements to maintain this layer of protection.

What challenges should I consider before setting up an LLC for my rental property?

Setting up an LLC for your rental property can provide a layer of legal protection, but it’s not without its hurdles. One of the main challenges is managing costs and administrative responsibilities. Between state filing fees, annual reports, and the need to maintain separate bank accounts and records, the expenses can quickly add up – especially if you opt to create a separate LLC for each property.

Financing is another area that can get tricky. Lenders often view properties owned by an LLC as riskier investments. This perception might lead to stricter loan terms, higher interest rates, or even requirements for personal guarantees, which could undermine the liability protection you’re aiming for. On top of that, rental income earned through an LLC may, in some cases, be subject to self-employment tax, potentially affecting your overall cash flow.

It’s also important to remember that an LLC doesn’t offer foolproof protection. If you fail to follow proper business practices – like keeping personal and business finances separate or staying current with required filings – a court could still hold you personally liable. Taking a close look at these factors will help you determine whether forming an LLC aligns with your rental property goals.