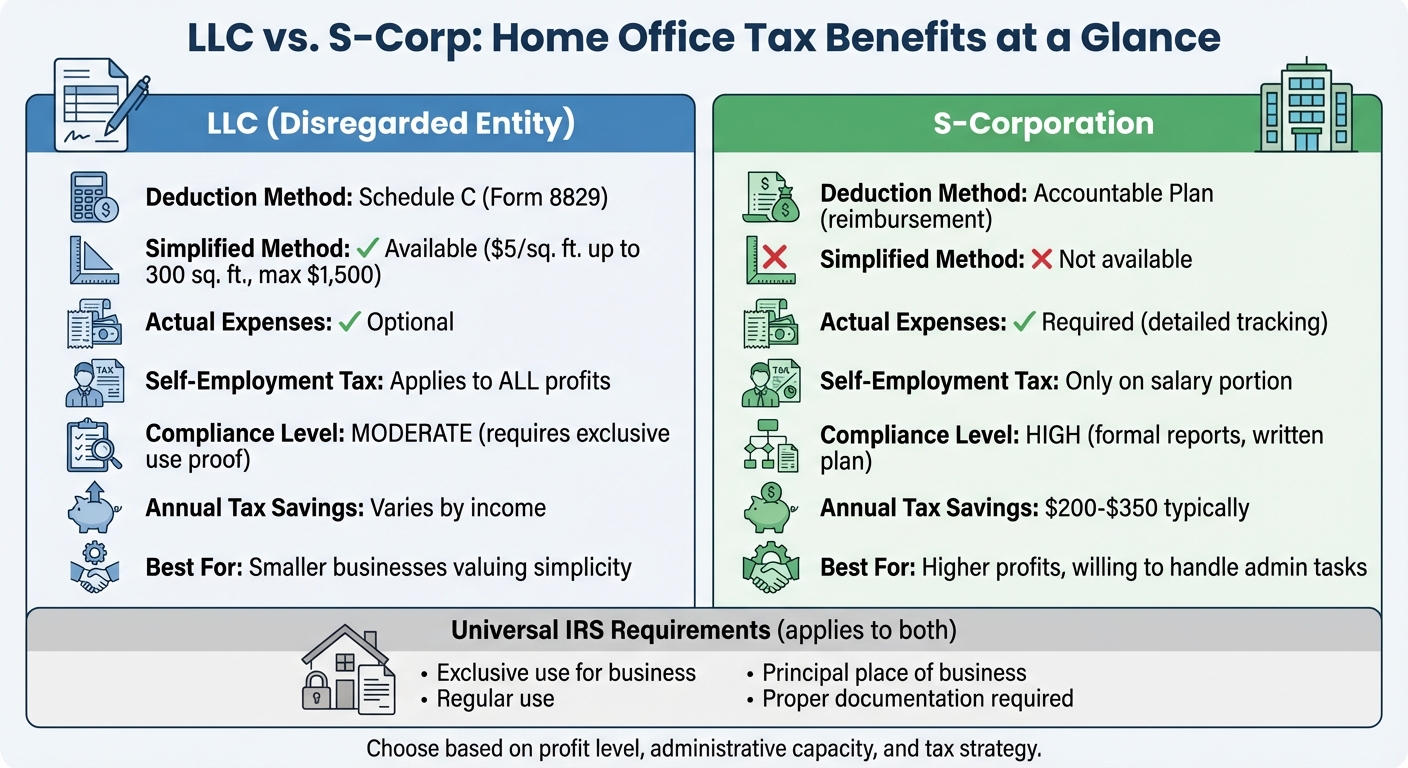

When deciding between an LLC and an S-Corp for your home-based business, the key differences lie in how taxes and home office deductions are handled. Here’s a quick breakdown:

- LLC Owners: Deduct home office expenses directly on their personal tax returns. You can choose between the simplified method ($5/sq. ft. up to 300 sq. ft.) or actual expenses (a percentage of home costs like utilities and mortgage interest). Easier to manage but may result in higher self-employment taxes.

- S-Corp Owners: Use an "accountable plan" to get reimbursed tax-free for home office expenses. This requires detailed records, monthly reports, and formal documentation. While more complex, it can reduce self-employment taxes by treating part of the income as dividends.

Both options require the home office to meet IRS rules: the space must be used exclusively for business and serve as your principal place of business. Choosing the right structure depends on your income level, willingness to handle administrative tasks, and tax strategy.

Quick Comparison:

| Feature | LLC (Disregarded Entity) | S-Corp |

|---|---|---|

| Deduction Method | Schedule C (Form 8829) | Accountable Plan |

| Simplified Method | Available ($5/sq. ft.) | Not available |

| Actual Expenses | Optional | Required |

| Self-Employment Tax | Applies to all profits | Only on salary |

| Compliance | Moderate | High (formal reports) |

| Tax Savings | Varies | $200–$350 annually |

For smaller businesses valuing simplicity, LLCs may be better. For higher profits and tax savings, S-Corps are often worth the extra effort.

IRS Home Office Rules That Apply to All Business Owners

Before diving into how LLCs and S-Corps handle home office benefits, let’s cover the IRS rules that apply to everyone. These guidelines are the starting point for understanding how home office deductions work across different business structures.

Who Qualifies for Home Office Deductions

The IRS sets clear criteria for home office deductions: the space must be used exclusively and regularly for business and must serve as your principal place of business. The exclusive use rule means a specific area of your home must be dedicated solely to business activities. For instance, if your den doubles as a family hangout, it won’t qualify. However, exceptions exist for certain situations, like storage areas or licensed daycare facilities, especially when no other fixed location is available.

Your home office qualifies as your principal place of business if it’s where you handle essential administrative tasks – like billing or bookkeeping – and you don’t have another fixed location for these activities. This rule can benefit professionals who perform their services elsewhere. For example, a plumber who meets clients at their homes but handles all paperwork in a home office would still qualify.

The IRS takes a broad view of what constitutes a "home." It includes houses, apartments, condos, mobile homes, boats, and even separate structures like unattached garages.

2 IRS Calculation Methods: Simplified vs. Actual Expenses

Once you confirm your home office qualifies, you’ll need to choose between two IRS-approved methods to calculate your deduction.

- Simplified Method: This option offers a flat rate of $5 per square foot for the portion of your home used for business, up to 300 square feet. The maximum deduction is $1,500. It’s straightforward, requires minimal recordkeeping, and doesn’t involve depreciation, so you avoid depreciation recapture when selling your home.

- Actual Expenses Method: This approach uses the percentage of your home dedicated to business (office square footage divided by total square footage) and applies that percentage to actual home expenses. Eligible expenses include mortgage interest, property taxes, utilities, insurance, HOA dues, and repairs. Direct expenses, like fixing something in the office itself, are fully deductible, while indirect expenses are prorated. Although this method often results in a larger deduction, it requires detailed records and incorporates depreciation, which lowers your home’s cost basis when sold.

"If you use the simplified option… This option will save you time because it simplifies how you figure and claim the deduction. It will also make it easier for you to keep records." – IRS

One more perk: a qualifying home office can turn commuting miles into deductible business miles. Travel from your home office to another business location is considered business travel, not commuting, which can further reduce your tax burden.

How LLC Owners Claim Home Office Deductions

LLC owners can claim home office deductions directly on their personal tax returns, skipping the need for reimbursement plans. However, the process varies depending on whether you run a single-member or multi-member LLC.

Claiming Deductions as an LLC Owner

If you operate a single-member LLC, the IRS treats it as a disregarded entity. This means your business income flows directly to your personal tax return. You’ll report your home office deduction on Schedule C (Form 1040). If you choose the actual expenses method, you’ll also need to complete Form 8829 (Expenses for Business Use of Your Home) to calculate the deduction.

For multi-member LLCs, which are typically taxed as partnerships, things work a bit differently. Partners usually report home office expenses as unreimbursed partnership expenses on Schedule E (Form 1040). To deduct these expenses, the partnership agreement must specify that you’re responsible for covering them out of pocket without reimbursement.

Regardless of the LLC type, the way you calculate the deduction remains the same. Direct expenses – like painting or repairs exclusively for your home office – are fully deductible. Indirect expenses – such as utilities, mortgage interest, insurance, and property taxes – are deductible based on the percentage of your home used for business. For instance, if your home office takes up 200 square feet of a 2,000-square-foot home, you can deduct 10% of your indirect expenses.

Using the actual expenses method requires additional steps, like calculating depreciation over 39 years. Be aware that selling your home may trigger a recapture tax on the depreciation, even if you didn’t claim it on your return.

Next, let’s dive into the records you’ll need to keep for these deductions.

Recordkeeping Requirements for LLC Owners

The type of records you’ll need depends on the method you choose. If you use the simplified method, you only need to document your office’s square footage and show that it’s regularly used for business. However, the actual expenses method demands more detailed records, such as receipts for utilities, insurance, HOA dues, repairs, and other home-related costs.

It’s also a good idea to keep a log of how you use the space for business. Photos or diagrams that confirm the size and exclusive use of your office can provide additional clarity.

The IRS advises holding onto these records for at least three years from the date you file your tax return. If you’re using the actual expenses method, you’ll also need to track depreciation each year to avoid surprises when calculating recapture tax if you sell your home.

Tools like BusinessAnywhere can make this process easier. Their dashboard helps LLC owners stay on top of recordkeeping and tax documentation throughout the year.

How S-Corp Owners Claim Home Office Deductions

If you’re an S-Corp owner, the rules for claiming home office deductions are a bit different than those for LLC owners. Since you’re technically considered an employee of your corporation, you can’t directly deduct home office expenses on Schedule C like a sole proprietor would. Instead, you need to set up something called an accountable plan to get reimbursed for those costs. This approach comes with its own set of documentation and calculations specific to S-Corp structures.

Accountable plan reimbursements offer tax-free distributions. This approach is generally more tax-efficient than having your S-Corp pay you rent, which would require reporting that rent as taxable income on Schedule E.

Using an Accountable Plan for Reimbursements

An accountable plan is essentially an agreement where your S-Corp reimburses you for business-related home office expenses. These reimbursements are tax-free for you as a shareholder-employee, and the corporation gets to deduct them as business expenses.

To qualify, your home office must meet the IRS requirements for business use. Eligible expenses often include a portion of your mortgage interest, property taxes, homeowners insurance, utilities, internet, and even home repairs.

Unlike other taxpayers who might use the simplified $5-per-square-foot method, S-Corp owners must calculate actual expenses. While this requires more detailed recordkeeping, it often results in tax savings, typically ranging between $200 and $350 annually. Another benefit: if you meet the home office criteria, the miles you drive from your home office to client sites or other business locations can be treated as deductible business miles.

Documentation Requirements for S-Corp Owners

To comply with IRS guidelines, your S-Corp must have a written accountable plan that defines which expenses are eligible and how reimbursements are handled. You’ll need to submit monthly or quarterly reports that include receipts, calculations of the business-use percentage (based on office square footage versus total home square footage), and the total reimbursement amount.

Although S-Corps don’t file Form 8829, many CPAs use it as a worksheet to calculate reimbursable expenses. Be sure to keep copies of reimbursement checks from your corporate account and maintain evidence – like photos or floor plans – showing that your home office is exclusively used for business.

If your S-Corp reimburses you for mortgage interest or property taxes, you’ll need to adjust the amounts you claim as itemized deductions on your personal Schedule A to avoid claiming the same expense twice. Also, be mindful of depreciation. Even if you don’t explicitly claim it, the IRS requires depreciation to be recaptured as taxable income (up to 25%) when you sell your home. Following these steps ensures your deductions align with tax regulations and help optimize your overall tax strategy.

For help staying on top of these detailed requirements, services like BusinessAnywhere provide bookkeeping and accounting solutions tailored to S-Corp owners.

sbb-itb-ba0a4be

LLC vs. S-Corp: Side-by-Side Comparison

Main Differences Between LLC and S-Corp Home Office Benefits

When it comes to home office benefits, the key difference lies in how tax advantages are handled. LLC owners deduct home office expenses directly on their personal tax returns using Form 8829 and Schedule C. On the other hand, S-Corp owners receive tax-free reimbursements through an accountable plan.

LLC owners have the flexibility to choose between two methods for deductions: the simplified method, which allows $5 per square foot for up to 300 square feet (capping at $1,500), or tracking their actual expenses. S-Corp owners, however, must calculate their actual expenses as the simplified method isn’t an option for them.

Compliance requirements also differ significantly. S-Corps must maintain a formal written accountable plan and require employees to submit regular expense reports. LLC owners, by contrast, need to prove that the home office meets the "exclusive and regular use" standard and keep accurate records for Form 8829. These differences highlight the operational and compliance factors to weigh when choosing between these business structures.

Comparison Table: LLC vs. S-Corp

Here’s a quick look at how LLCs and S-Corps compare when it comes to home office benefits:

| Feature | LLC (Disregarded Entity) | S-Corporation |

|---|---|---|

| Primary Mechanism | Direct tax deduction (Form 8829) | Accountable Plan reimbursement |

| Simplified Method | Available ($5/sq. ft. up to 300 sq. ft.) | Not available |

| Actual Expenses | Deductions prorated by office square footage | Required for reimbursement |

| Self-Employment Tax | Reduces income and self-employment taxes | Reduces pass-through income tax only |

| Reporting | Schedule C | Corporate expense reporting |

| Compliance Level | Moderate; requires "exclusive use" proof | High; formal documentation required |

| Annual Tax Savings | Varies | Typically $200 to $350 |

| Depreciation | Claimed on Form 8829 | Reimbursed by the corporation; tracked for recapture |

Which Structure Is Right for Your Home-Based Business?

What to Consider When Choosing

Start by assessing your profit level. If your business brings in a modest income and you prefer simplicity, an LLC might be the better choice. With an LLC, you can use the simplified method to claim up to $1,500 without tracking every single utility bill. On the other hand, S-Corps come with more paperwork and only make sense when your profits are high enough to outweigh the administrative workload.

Your ability to handle administrative tasks is another key factor. S-Corps demand detailed documentation, including formal Accountable Plans, while LLCs offer a more relaxed approach to recordkeeping. For example, LLC owners using the simplified method can avoid the hassle of complex depreciation calculations. Additionally, your home office setup plays a role. Establishing a dedicated home office can turn non-deductible commuting miles into deductible business expenses.

Don’t forget to think about your long-term tax goals. While S-Corp reimbursements can save between $200 and $350 annually, the added compliance work may not be worth it for smaller operations. Carefully balancing these factors will help you choose the structure that fits your business needs.

How BusinessAnywhere Simplifies LLC and S-Corp Management

Managing the complexities of LLCs and S-Corps can be much easier with the right tools. BusinessAnywhere offers integrated support to tackle administrative and compliance challenges. For instance, they handle S-Corp election filings for $97, ensuring everything stays on track with IRS requirements. Their registered agent service also helps maintain state compliance while keeping your home address private – especially useful if your home doubles as your business headquarters.

With features like compliance alerts and annual filing support, all accessible through a single dashboard, BusinessAnywhere helps streamline the documentation process. This can be particularly valuable for S-Corp owners who face more demanding recordkeeping requirements compared to LLCs.

FAQs

What are the tax advantages of choosing an S-Corp instead of an LLC for a home-based business?

Opting for an S-Corp for your home-based business can open up several tax benefits that may not be available with an LLC. Here’s how:

- Tax-Free Home Office Reimbursements: With an S-Corp, you can set up an accountable plan to reimburse yourself for a portion of your home expenses, like mortgage interest, utilities, and maintenance. These reimbursements are completely tax-free and also reduce the taxable income of your S-Corp.

- Lower Self-Employment Taxes: As an S-Corp owner, you only pay Social Security and Medicare taxes on your salary, not on the entire profit of the business. The remaining profits can be distributed as dividends, which aren’t subject to self-employment tax. This structure can significantly reduce your overall tax liability compared to an LLC.

- Flexible Expense Allocation: S-Corps offer more options for handling home-office expenses. You can either get reimbursed for these costs or have the S-Corp pay you rent for using your home as an office. This flexibility can result in greater tax savings compared to the standard home-office deduction typically used by LLCs.

By leveraging these benefits, S-Corp owners can fine-tune their tax strategies while adhering to IRS rules for home-office deductions.

What are the IRS requirements for a home office to qualify for tax deductions?

To claim a home office deduction, the IRS has two main requirements your workspace must meet:

- Regular and exclusive use: The space must be used only for business purposes and on a regular basis. For instance, if you occasionally work from a guest bedroom, it wouldn’t qualify because the space serves multiple functions.

- Principal place of business: Your home office should be the primary location where you handle administrative or management tasks for your business. This applies even if you perform other work or meet clients at different locations.

If your home office meets these criteria, you can calculate the deduction using one of two methods: the simplified method or the actual expense method. Make sure to consult the IRS guidelines for details on how to calculate and report these deductions, including which forms to use, such as Schedule C or those specific to S-Corps.

What records do LLC and S-Corp owners need to keep for home office tax deductions?

To qualify for a home office tax deduction, owners of LLCs and S-Corps need to keep detailed records that demonstrate the space is used exclusively and regularly for business purposes. Here’s what you’ll need to document:

- Square footage breakdown: Record the total size of your home and the portion used specifically for your office.

- Receipts and bills: Keep proof of deductible expenses such as rent, mortgage interest, utilities, insurance, property taxes, and any repairs related to the space.

- Usage logs or calendars: Track the days and hours you use the space for business activities.

- Depreciation schedules: If you own your home, include depreciation schedules and any carryover amounts from previous years.

For S-Corp owners, there’s an extra layer of paperwork. You’ll need to maintain records for accountable-plan reimbursements, which include expense reports, receipts, and evidence of reimbursement payments. Staying organized with these documents not only helps you comply with IRS regulations but also makes filing your business tax returns much smoother.