State tax audits can be stressful, but preparation and organization can make the process smoother. Here’s what you need to know to navigate them effectively:

- What is a State Tax Audit? It’s a review of your business’s financial records to ensure taxes are collected, reported, and paid correctly. Audits often focus on sales tax, corporate income tax, franchise tax, and withholding tax.

- Why You Could Be Audited: Common triggers include nexus issues (e.g., operating in multiple states), unreported income, misclassified workers, or discrepancies in tax filings.

- How to Prepare:

- Confirm where your business has nexus (taxable presence).

- Keep detailed, organized records like sales invoices, bank statements, and tax returns.

- Respond promptly to audit notices and consider appointing a representative.

- Key Documentation to Have:

- Ownership documents (e.g., Articles of Incorporation).

- Financial records (e.g., general ledgers, bank statements).

- Sales and tax records (e.g., invoices, exemption certificates).

Pro Tip: Regularly review your records and track compliance across states to avoid surprises. Staying organized and maintaining clear documentation can save you time, money, and stress during an audit.

Pre-Audit Risk Assessment: Identifying Your Exposure

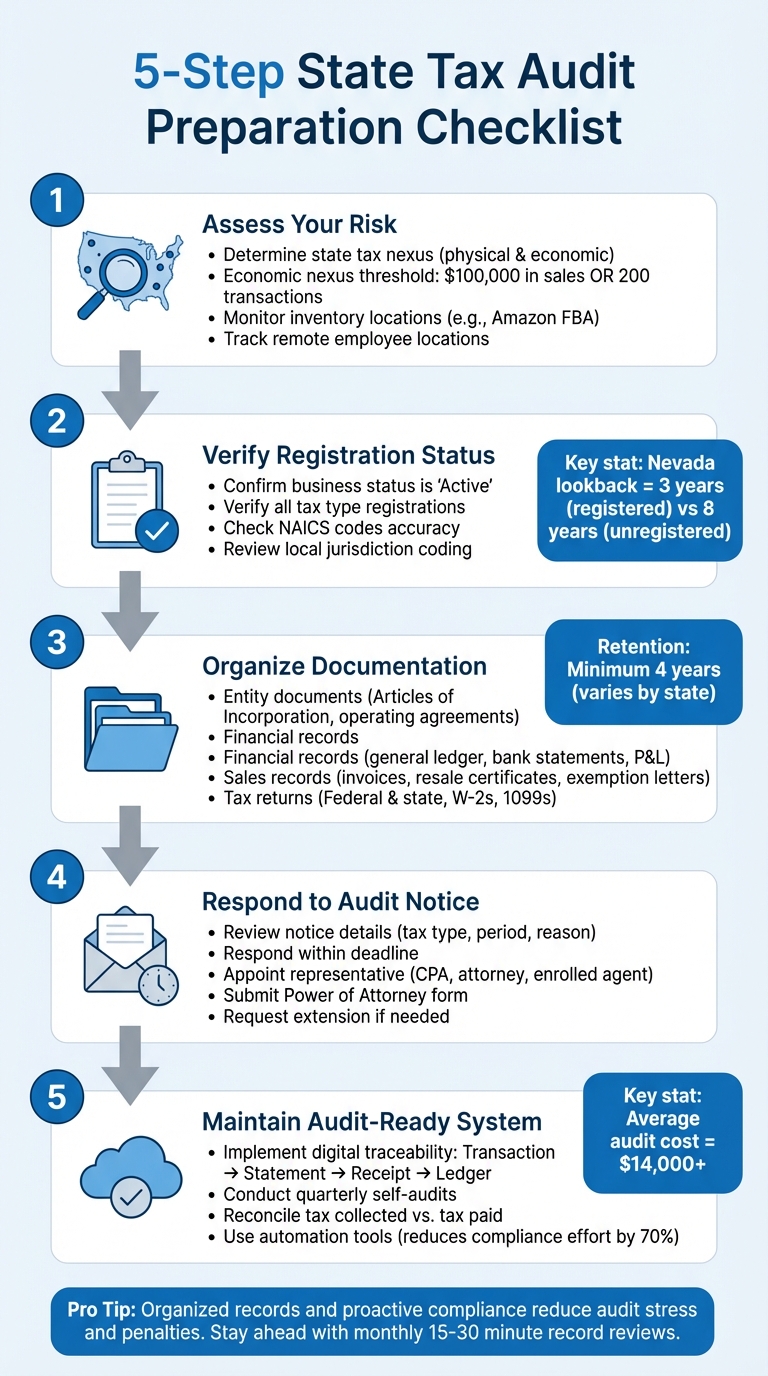

Determine Your State Tax Nexus

Nexus refers to the connection between your business and a state that allows the state to impose tax obligations on you. Understanding where your business has nexus is crucial for gauging your audit risk. Physical nexus is established when your business has a tangible presence in a state – like offices, warehouses, sales locations, or even stored inventory. If you use fulfillment services like Amazon FBA, nexus might be created in states where your inventory is stored, even if you didn’t actively choose those locations.

The 2018 South Dakota v. Wayfair, Inc. ruling introduced economic nexus rules, requiring businesses to register for tax collection if their annual sales exceed $100,000 or involve 200 transactions in a state. Every state with sales tax has adopted these rules. Moreover, if you have employees working remotely in a state, this could trigger corporate nexus and bring additional tax responsibilities.

"The state will take the position that because the inventory was moved into the state by the fulfillment service provider, nexus existed from the moment the inventory was first present."

– David J. Brennan Jr., Esq., Senior Attorney, Moffa, Sutton, and Donnini PA

To stay ahead, monitor your revenue and transaction counts regularly to ensure compliance with these thresholds. Additionally, track where your inventory is stored, as states might use this data to assert nexus from the moment your products entered their borders. A clear understanding of your nexus obligations is a key step in identifying potential audit risks.

Recognize Common Audit Triggers

States employ various methods to flag businesses for audits. Crossing economic nexus thresholds is one obvious trigger, but there are others that often catch businesses off guard. For instance, registering for a tax account after years of operating can lead to a review of whether your business should have been paying taxes all along. Other red flags include inconsistencies in reported gross sales, deductions, or taxable purchases, as well as mismatches between state tax returns and federal income tax filings.

Receiving a nexus inquiry letter is another common starting point. Ignoring such letters or providing incomplete information can result in the state issuing an estimated tax assessment. States also collaborate with federal agencies and other departments to identify businesses operating without proper registration.

"A question with a ‘yes/no’ answer may not tell a business’s whole story and can provide a false indication of tax liability."

– David J. Brennan Jr., Esq., Senior Attorney, Moffa, Sutton, and Donnini PA

When responding to nexus questionnaires, include a detailed cover letter that provides context and ensures your situation is accurately represented. You can also explore voluntary disclosure agreements to limit lookback periods and minimize penalties. These steps can help you address potential risks while ensuring your business is compliant.

Verify Your Business Registration and Compliance Status

Being registered for one tax type doesn’t mean you’re covered for all your obligations. For instance, registering for Sales and Use Tax doesn’t automatically enroll your business for other taxes, like Excise or Modified Business Taxes. Double-check your state records to ensure your business status is listed as "Active" (and not "Out of Business"), and confirm that your trade names and taxable sale dates match your actual operations.

It’s also important to verify that your business is correctly coded for local jurisdictions, such as cities, counties, or Special Purpose Districts (SPDs), as these designations can impact your tax rate. Ensure your Franchise Tax Charters, business type, and Certificates of Authority align with current state records. Additionally, make sure your NAICS codes are accurate, as these industry classifications are often used to identify audit candidates.

The consequences for unregistered businesses can be severe. For example, Nevada typically has a 3-year audit lookback period for registered businesses, but this extends to 8 years for unregistered ones. In Texas, businesses are required to keep records for at least 4 years, but if filings are incomplete or missing, audits can stretch even further.

"For tax returns that are unfiled, a state can usually go after a business indefinitely. In other words, theoretically, 20 years from now, a state could tell a business it is responsible for 20 years of taxes if no returns were filed."

– Journal of Accountancy

To avoid surprises, conduct periodic reviews of your historical records. Look for fluctuations in reported data, open collection records, or late filings that might raise red flags. Reconcile the tax you’ve collected and accrued with the amounts you’ve actually paid to catch errors before an auditor does. If you uncover compliance issues, BusinessAnywhere’s compliance support services offer a streamlined way to address registration and filing needs across multiple states from a single platform.

sbb-itb-ba0a4be

Documentation Checklist for State Tax Audits

When you receive an audit notice, the countdown begins. Having your documents well-organized and easily accessible can make a big difference between a straightforward resolution and a drawn-out investigation. State auditors will require specific records to verify your tax filings, and incomplete or missing documents can lead to penalties or extended review periods. Here’s what you’ll need to prepare.

Entity and Ownership Documents

Start by gathering your formation documents, such as Articles of Organization or Incorporation, operating agreements or bylaws, membership ledgers, and IRS Schedule K-1 forms. These establish ownership details and compliance. Your membership ledger should clearly list the names, contact information, and ownership percentages of all members. Schedule K-1 forms are critical for reporting each member’s share of income, losses, and credits.

"Accurate proof of ownership is crucial for tax compliance. It ensures that all members report their share of business income, losses, and deductions."

– Rick Mak, Global Entrepreneur and Business Strategist

If your ownership structure has changed, make sure to include documentation like membership interest purchase agreements or amendments to your operating agreement. Additionally, provide business licenses, permits, and DBA (Doing Business As) statements, as auditors often request these for compliance verification. For businesses with physical assets or loans, include property leases and loan agreements that detail borrower names, terms, and settlement sheets.

If formal ownership documents are missing, a notarized affidavit can serve as a sworn statement of ownership. Keep signed and dated copies of all agreements for reference. Businesses required to file Beneficial Ownership Information Reports (BOIR) can use BusinessAnywhere’s BOIR filing service to comply with FinCEN regulations for just $37.

Once your ownership documents are in order, move on to your financial records to strengthen your audit preparation.

Accounting and Banking Records

Auditors will closely examine your financial records to ensure accuracy. Start with your general ledger, which provides an overview of all transactions. Include subsidiary journals for sales, purchases, and disbursements, along with your chart of accounts and trial balances.

Bank statements for all business accounts are essential. Auditors will compare reported revenue with actual cash flow, so gather statements from checking, savings, and merchant accounts. Include canceled checks or digital payment confirmations with corresponding invoices.

Prepare complete financial statements, including profit and loss (P&L), balance sheets, and cash flow statements for the audit period. If you use accounting software, have the data ready in electronic format, as many states (like Missouri and Texas) prefer digital submissions. Also, provide working papers and accounting data used to prepare your tax reports, along with reconciliation schedules showing tax accrued versus tax paid.

Include depreciation schedules and asset listings to support deductions. If you have employees, provide payroll registers and copies of W-2s and 1099s. For cash-heavy businesses, prepare cash register "Z" tapes, petty cash vouchers, and handwritten records summarizing payments to back up income and expenses.

Organize your records by year and sub-categorize them by income or expense type. A summary of transactions for each category can help auditors navigate large volumes of data. Always send high-quality copies, not originals, and keep the originals safely stored. For entrepreneurs managing operations across multiple states, BusinessAnywhere’s bookkeeping and accounting services can help maintain audit-ready records that meet state requirements.

With your financial records in place, the next step is to gather sales and tax-related documents.

Sales, Revenue, and Tax Records

Sales and revenue records are critical for verifying your reported gross receipts. Start with your sales journals and general ledgers, and include sales invoices, cash register "Z" tapes, and customer listings.

For sales claimed as exempt from sales or use tax, provide valid resale certificates or exemption letters. Missing exemption documentation is a common reason for additional tax assessments. If you operate in multiple states, prepare schedules showing sales by destination, property balances by location, and payroll registers by state to confirm apportionment factors.

Ensure your Federal income tax returns (e.g., Forms 1120, 1065, and related K-1s) and state corporate returns align with your accounting records. Auditors will compare these filings to identify inconsistencies. Include all supporting worksheets used to calculate your tax returns, tax accrual work papers, and records for any overpaid taxes or credits.

"Auditors by law may examine a taxpayer’s books and records to determine the accuracy of taxes paid."

– Texas Comptroller

For payroll taxes, provide state withholding tax returns (e.g., MO 941), payroll registers, and copies of W-2s and 1099s for the audit period. If you’ve claimed deductions for bad debts, ensure these are backed by your general ledger and documented Federal income tax write-offs.

| Record Category | Documents Required |

|---|---|

| Sales & Revenue | Sales journals, invoices, cash register tapes, customer listings, resale certificates |

| Tax Returns | Federal returns (Forms 1120/1065), state income/franchise returns, sales/use returns |

| Accounting | General ledgers, charts of accounts, P&L statements, bank statements |

| Apportionment | Sales by destination, rent by location, property balances |

| Payroll | Payroll registers, W-2s, 1099s, unemployment tax returns |

Reconcile the tax collected and accrued against the amounts paid on your tax returns to catch discrepancies early. Keep digital backups of all records, as many states now request electronic formats. For example, Texas requires records to be kept for at least 4 years, while Nevada mandates 4 years for registered businesses and 8 years for unregistered ones. Group your records by year and type, and include summaries to make the audit process smoother.

Step-by-Step Guide to Managing a State Tax Audit

Once you’ve organized your records, it’s time to tackle the audit process with a clear plan. Here’s how to navigate each step effectively.

What to Do When You Receive an Audit Notice

Start by carefully reviewing the audit notice. Check the details, such as the tax type, the audit period, and the reason for the examination. If your state offers online verification tools, use them to confirm the notice’s authenticity. Determine whether it’s a Correspondence Audit (handled via mail) or a Field Audit (conducted in person at your home, business, or accountant’s office). Typically, audits cover the past three to four years of filings, but if your business isn’t registered with the state, the review could extend up to eight years.

Respond quickly to avoid complications. Ignoring initial notices or questionnaires – like Texas Form 00-750 – can lead to liabilities being assessed without your input. Submit completed questionnaires promptly to schedule an Entrance Conference, where the auditor will explain the audit plan and specify which records they’ll need. If meeting the deadline for gathering records seems challenging, request an extension early – most tax departments will accommodate reasonable requests.

Consider appointing a representative, such as a CPA, attorney, or enrolled agent, to handle communications with the auditor. To formalize this, submit your state’s Power of Attorney (POA) form (for instance, New York’s Form POA-1), which allows the auditor to discuss your case with your chosen representative.

"Taxpayers have the right to retain an authorized representative of their choice to represent them in their dealings with the IRS." – Taxpayer Advocate Service

Once you’ve set up representation, focus on organizing your records to ensure smooth communication.

Organizing and Sharing Audit Documents

Gather all necessary records using a detailed documentation checklist. Arrange them in chronological order and group them by category, including transaction summaries to help the auditor navigate your files. Always send high-quality copies – never mail original documents. Many agencies now allow digital submissions through tools like Secure Messaging or Document Upload platforms, although you typically need an invitation to access these services.

Annotate your documents clearly. For instance, label receipts with their specific business purpose. If you’re submitting travel-related expenses, group tickets with corresponding receipts for meals and lodging, and note the business purpose of each trip.

"If the records are assembled in a neat and orderly manner before [the first] meeting, any unclear items may be resolved with the least amount of time and effort." – Georgia Department of Revenue

Keep a detailed communication log throughout the audit. Record phone calls, emails, and notes from conversations with the auditor in chronological order. During the Entrance Conference, explain your record-keeping system, internal controls, and the volume of records to help establish a streamlined audit plan.

With your documents in order, you’ll be better prepared to address any preliminary findings.

Addressing Preliminary Findings

At the end of the fieldwork, auditors will typically provide schedules outlining potential overpayments or underpayments. You’ll usually have time to review these findings and dispute any adjustments you believe are incorrect. If discrepancies arise, request additional time to locate supporting documents.

Attend the Exit Conference to review audit adjustments, discuss penalty waiver recommendations, and address interest assessments. Use this meeting to clarify the criteria for waiving penalties and interest. If disagreements remain, many states offer options like a Reconciliation Conference with an audit manager or an Independent Audit Review (IAR) with a neutral third party to resolve issues before finalizing the audit.

If you can’t pay the full amount immediately, inquire about setting up an installment plan. In some states, like Missouri, paying your liability "under protest" can stop interest from accruing while you appeal the case. If you still disagree with the final results, you can file a Statement of Grounds or a Petition for Redetermination – typically within 60 to 90 days, as specified on the audit notice.

For business owners managing operations across multiple states, tools like BusinessAnywhere’s compliance support services can simplify documentation and help you respond efficiently to audits in different jurisdictions, minimizing penalties and delays.

Building an Audit-Ready System

Once you’ve nailed down a solid documentation checklist, the next step is setting up an audit-ready system. For entrepreneurs juggling businesses across multiple states – especially those living the digital nomad lifestyle – this means shifting from reacting to issues as they arise to proactively managing your records and compliance.

Implementing Effective Record-Keeping Practices

At the heart of audit readiness lies digital traceability. Every figure on your tax return should be backed by a clear and accessible chain of documentation: Transaction → Statement → Receipt → Ledger. This traceability ensures you can quickly provide evidence when needed.

Start by creating a Master Audit Folder in a cloud storage platform like Google Drive or Dropbox. Organize it with subfolders for Income, Expenses, Bank Statements, and Prior-Year Returns. Use clear, standardized naming conventions, such as "2025-Expenses-GasReceipt.pdf", to keep everything in order. This way, you can easily access your records no matter where you are.

"The IRS doesn’t expect perfection; it expects traceability. If you can show where your numbers came from and back them up with consistent documentation, you’ve already won half the battle." – Scott Gettis, Lead at Precision Tax

Set aside 15–30 minutes each month to organize your income, expenses, digital receipts, and mileage logs. This habit will save you from the year-end chaos and help you meet the 5 C’s of audit compliance: Completeness, Consistency, Clarity, Comparability, and Compliance.

For remote businesses, tools like BusinessAnywhere’s virtual mailbox service can simplify your life. These services scan and store your mail digitally, ensuring critical tax documents are captured and organized automatically. When paired with bookkeeping and accounting tools, you’ll have a centralized hub for all your audit-ready records, no matter where you’re located.

Automation can also make a big difference, cutting compliance efforts by over 70%. Platforms that integrate data from accounting software, payment processors, and banking systems ensure your operational data aligns with auditor expectations. For example, in 2025, the Canadian logistics firm Orca used Scrut Automation to achieve SOC 2 audit readiness in just eight weeks.

With these practices in place, you’ll be better equipped to tackle the challenges of multi-state compliance.

Tracking Multi-State Compliance

Once your record-keeping system is solid, staying on top of state-specific obligations gets much easier. For entrepreneurs managing nexus in multiple states, tracking compliance thresholds is essential. Each state has unique rules for sales tax nexus, income tax filings, and exemption certificate requirements. A reliable system should monitor sales activity across jurisdictions and alert you when you’re nearing thresholds that require additional filings.

Create a multi-state reconciliation spreadsheet to track tax collected versus tax paid in each jurisdiction, including local, county, and transit authority taxes. For example, Texas has specific transit tax documentation requirements, and failing to meet them can lead to penalties during an audit.

Keep your exemption certificates up to date. Regularly review resale and exemption certificates for customers making tax-free purchases to ensure they’re valid and properly documented. Many states require certificates to be renewed periodically, and expired ones can lead to retroactive tax assessments.

Automated tools with real-time dashboards can simplify this process by providing a live view of your audit posture, highlighting missing evidence, and allowing you to map controls like data retention or encryption to multiple state or federal standards simultaneously.

Periodic Self-Audits for Readiness

Conducting quarterly self-audits can help you catch compliance gaps before state auditors do. Start by reconciling general ledgers, sales journals, and return worksheets with reported amounts to identify discrepancies. Pay close attention to tax accruals, ensuring that taxes collected or accrued match what’s actually been paid. Discrepancies here are a major red flag for auditors.

Focus on high-risk categories, such as capital asset sales, miscellaneous income, and large fluctuations in gross sales or deductions. Test your internal controls by confirming that invoice taxes align with summary records and returns. Review both expense accounts and accounts payable to ensure taxes on business purchases are correctly handled.

Prepare a one-page Audit Summary for each year. This summary should include totals for each category and brief notes on unusual items, like "high ad spend due to Q2 rebrand". A well-organized summary like this can build trust with auditors by showing that your records are professional and transparent.

Keep in mind that record retention requirements vary. The IRS generally requires keeping records for three years after filing, but employment tax records must be kept for four years. If you omit more than 25% of your gross income, the retention period extends to six years. For property and assets, retain records until the limitations period expires for the year the asset is sold or disposed of.

For digital nomads managing businesses across borders, BusinessAnywhere’s compliance support services can streamline much of this process. Their tools integrate bookkeeping features with compliance alerts, helping you stay ahead of filing deadlines and regulatory changes while keeping your records audit-ready as your business grows.

Conclusion: Simplifying Audit Preparation for Entrepreneurs

Preparing for state tax audits doesn’t have to be a daunting task. With consistent and organized record-keeping, audits can shift from being a major headache to a manageable part of running your business. Instead of treating audit readiness as a last-minute scramble, make it a regular part of your operations. Keeping detailed documentation, maintaining a clear separation between business and personal finances, and staying organized are your strongest safeguards against audit stress. As Gusto aptly says:

"For the majority of business owners, a tax audit is a nuisance and nothing more. However, it is a nuisance for which you must be prepared".

For entrepreneurs operating across multiple states, the stakes are even higher. Navigating different nexus rules, retention requirements, and exemption policies can quickly become overwhelming. That’s where centralized tools come in handy. Platforms like BusinessAnywhere simplify compliance by combining services like registered agent support for multiple states, virtual mailboxes, bookkeeping, and compliance alerts into one streamlined dashboard. This ensures you never miss critical audit notices and keeps your records in order.

Here’s why organization matters: when your records are clear, complete, and easy to follow, auditors are more likely to trust your compliance efforts. The average cost of a sales tax audit is over $14,000, and much of that expense comes from disorganized or missing records. By following the practices outlined in this checklist, you can significantly lower your audit risk and avoid unnecessary financial penalties.

Staying organized is the cornerstone of long-term compliance. Regularly reconcile accounts, organize receipts, and keep your compliance tracker up to date. With these habits, audit preparation becomes less of a burden and more of a professional routine.

FAQs

What should I do if I receive a state tax audit notice?

If you receive a state tax audit notice, the first step is to carefully read through the letter. It will detail the tax years being reviewed, the type of audit, the specific documents needed, and the deadline for your response. Make sure to note this deadline on your calendar and save a copy of the notice for your records. If anything in the letter is unclear, reach out to the agency directly using the contact information provided.

Once you understand the requirements, start gathering the requested documents. These might include tax returns, receipts, bank statements, payroll records, or other relevant paperwork. Be sure to follow the auditor’s instructions for submitting these materials, whether that’s through a secure upload, certified mail, or an in-person meeting. For more complex audits, you might want to consult with a CPA, tax attorney, or another qualified professional for guidance.

Throughout the audit, maintain clear communication with the auditor. Don’t hesitate to ask questions if you need clarification, and keep detailed records of everything you provide. If you disagree with any findings, you have the option to appeal or request a review. Staying organized and proactive will help you manage the process more smoothly.

How do I know if my business is required to collect state taxes in a specific state?

Determining whether your business needs to collect state taxes comes down to whether it has a nexus in that state. Nexus is established through either a physical presence or economic activity.

- Physical presence: If your business operates a physical location, employs staff, works with contractors, or owns property (like an office or warehouse) in a particular state, you likely have a nexus there. Even having a registered agent in the state can sometimes create this connection.

- Economic activity: Many states set economic nexus thresholds based on your business’s annual sales or transaction volume within their borders. For instance, surpassing $100,000 in sales or completing 200 transactions in a state often triggers tax obligations. These thresholds, however, differ from state to state, so it’s crucial to check the specific rules for each location.

If your business meets either of these conditions, you’ll need to register to collect taxes in that state. Platforms like BusinessAnywhere can make this easier by streamlining compliance, tracking operations across multiple states, and managing registrations from a single, user-friendly dashboard.

What are the main reasons a state tax audit might be triggered?

State tax audits often occur when the information you report doesn’t align with what tax agencies have on file or when certain patterns hint at possible underpayment. Here are some common reasons audits get triggered:

- Data mismatches: If your reported numbers – like sales, use tax, or withholding – don’t match third-party records such as 1099 forms or credit card processing reports, it can raise a flag.

- Unusual deductions or credits: Claims that stand out, like unusually high expenses or sudden shifts in profit margins, might draw extra attention.

- Filing issues: A pattern of late filings, missed deadlines, or frequent amended returns can suggest non-compliance and increase scrutiny.

- Random or risk-based selection: Sometimes audits are purely random, but states also use risk models to identify targets based on factors like industry trends, rapid business growth, or past audit results.

To lower your chances of an audit, keep your records accurate, well-organized, and regularly cross-checked with third-party data. Tools like BusinessAnywhere’s compliance services can help you manage documentation and stay audit-ready.