If you own a small business, switching to an S Corporation could save you thousands in taxes each year. Here’s why:

- Avoid Double Taxation: Unlike C Corporations, S-Corps pass profits directly to shareholders, skipping corporate-level taxes.

- Lower Payroll Taxes: Pay self-employment tax (15.3%) only on your salary, not on profit distributions.

- Qualified Business Income (QBI) Deduction: Deduct up to 20% of your business income, thanks to a recent tax law change.

- Expense Deductions: Write off wages, health insurance, home-office costs, and more, directly reducing taxable income.

- Loss Pass-Throughs: Offset other income with business losses, reducing your overall tax burden.

For example, an S-Corp owner earning $200,000 could save over $16,000 annually by splitting income into a $95,000 salary and $105,000 in distributions. However, you must follow IRS rules, like paying yourself a reasonable salary, to avoid penalties. Consulting a tax professional is key to maximizing these benefits while staying compliant.

How S-Corp Pass-Through Taxation Works

S-Corp vs C-Corp Tax Treatment Comparison

The Basics of Pass-Through Taxation

With pass-through taxation, your S-Corp doesn’t pay federal income tax at the corporate level. Instead, all income, losses, deductions, and credits are passed directly to you and any other shareholders. You’ll report your share of the business’s performance on your personal Form 1040 and pay taxes based on your individual income tax rate, which ranges from 10% to 37%.

"S corporations are corporations that elect to pass corporate income, losses, deductions, and credits through to their shareholders for federal tax purposes." – IRS

Here’s how it works: your S-Corp files Form 1120-S annually to report its earnings or losses. While the business itself doesn’t pay federal income taxes, each shareholder receives a Schedule K-1 that details their share of the company’s income, deductions, and credits. These figures are then included on your personal tax return.

One key point to remember: you’re taxed on your share of the S-Corp’s income regardless of whether you actually receive it as cash. For instance, if your business made $150,000 in profit but retained $100,000 for future expenses, you’d still owe taxes on the full $150,000.

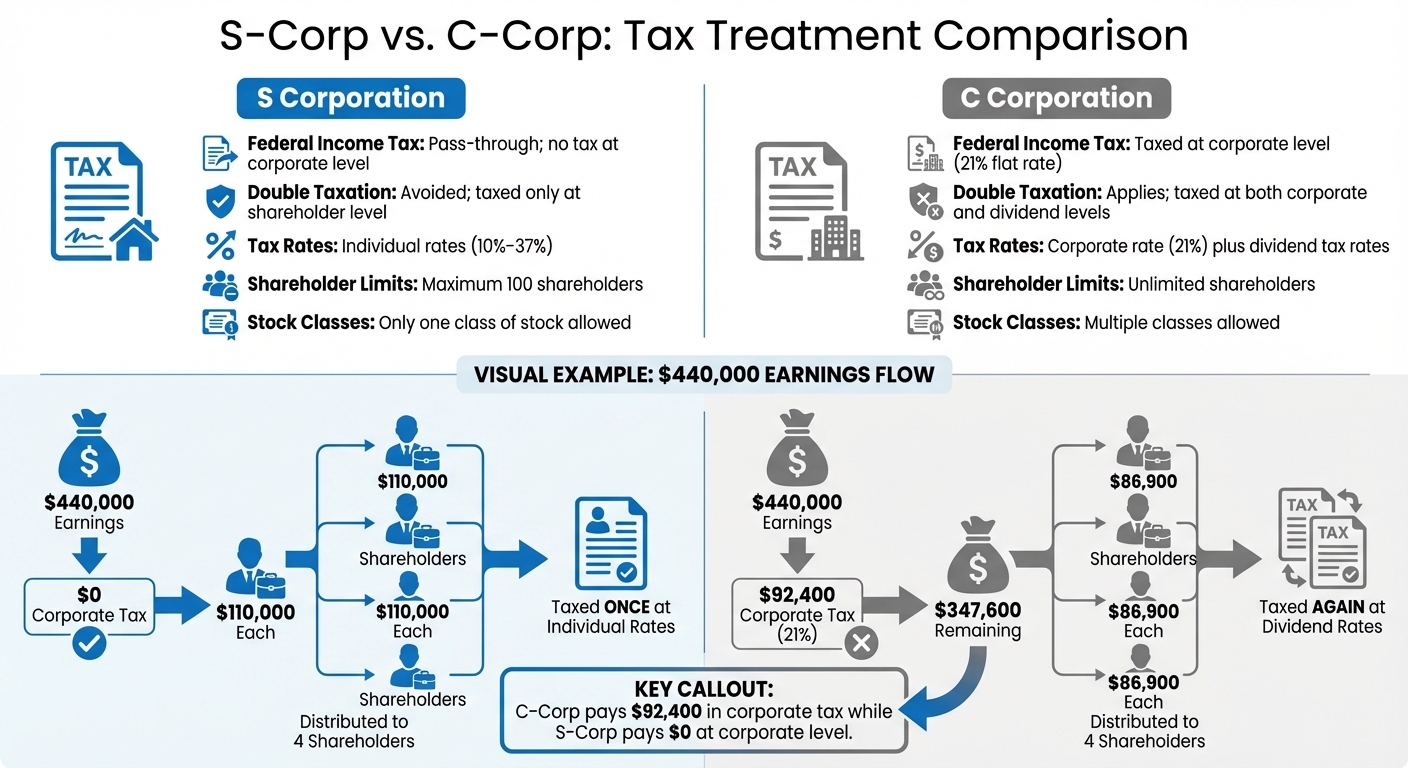

S-Corp vs. C-Corp Tax Treatment

The main distinction between S-Corps and C-Corps lies in how profits are taxed. C-Corporations face double taxation: the IRS taxes the company’s profits at a 21% federal corporate tax rate, and then shareholders pay taxes on dividends they receive – at rates ranging from 0% to 23.8%. S-Corps avoid this double taxation by passing income directly to shareholders, who only pay taxes at their personal rates.

For example, in 2025, Investopedia analyzed a C-Corp earning $440,000. After paying the 21% corporate tax ($92,400), only $347,600 remained for distribution among four shareholders, giving each $86,900. This amount was then taxed again on their individual returns. By contrast, an S-Corp earning the same $440,000 would skip the $92,400 corporate tax entirely.

| Feature | S Corporation | C Corporation |

|---|---|---|

| Federal Income Tax | Pass-through; no tax at the corporate level | Taxed at the corporate level (21% flat rate) |

| Double Taxation | Avoided; taxed only at the shareholder level | Applies; taxed at both the corporate and dividend levels |

| Tax Rates | Individual rates (10%–37%) | Corporate rate (21%) plus dividend tax rates |

| Shareholder Limits | Maximum 100 shareholders | Unlimited shareholders |

| Stock Classes | Only one class of stock allowed | Multiple classes allowed |

"Perhaps the most significant benefit of an S-corporation over a C-corporation is the avoidance of double taxation." – Rocket Lawyer

That said, while S-Corps avoid federal income tax, some states impose their own taxes. For example, California charges a 1.5% franchise tax on S-Corp net income (with a minimum $800 fee), and New York City applies an 8.85% corporate tax. Always check your state’s specific tax rules to avoid surprises. Next, we’ll dive into strategies to further reduce your tax burden.

How to Reduce Self-Employment Taxes with Salary and Distributions

Understanding Salary vs. Distributions

If you’re an S-Corp owner, you wear two hats: employee and shareholder. This unique setup allows you to split your income into two categories – a W-2 salary and profit distributions. Here’s where the tax benefits come into play: while your salary is subject to FICA taxes (15.3% total for Social Security and Medicare), distributions are only taxed as ordinary income, skipping payroll and self-employment taxes entirely.

The IRS, however, requires you to pay yourself a "reasonable salary" before taking distributions. What counts as reasonable? It depends on factors like your experience, role, and industry standards.

"S corporations must pay reasonable compensation to a shareholder-employee in return for services that the employee provides to the corporation before non-wage distributions may be made to the shareholder-employee." – IRS Fact Sheet 2008-25

To ensure compliance, do your homework. Research market salaries for your position, document your rationale, and formalize it with a job description and board resolution. The IRS has taken action against S-Corp owners who paid themselves disproportionately low salaries. For example, in one case, a CPA who paid himself $24,000 in salary while taking much larger distributions had his salary adjusted to $93,000 by the IRS.

Avoid the temptation to skip a salary altogether. Excessive distributions without reasonable wages can trigger audits, and the IRS may reclassify those distributions as wages. This could result in penalties, including a 20% accuracy-related fee on any underpayment. To simplify compliance, consider using payroll services (typically $30–$50/month) to handle withholdings and filings. It’s also wise to review your salary annually.

By balancing your income between salary and distributions, you can set yourself up for real tax savings. Here’s how it works in practice.

Example: Tax Savings with a $200,000 Income

Let’s break this down with a real-world example. Imagine your S-Corp generates $200,000 in net income. After researching, you decide that $95,000 is a reasonable salary, leaving $105,000 for distributions.

| Income Component | Amount | FICA Tax (15.3%) | Tax Owed |

|---|---|---|---|

| Salary | $95,000 | Yes | $14,535 |

| Distributions | $105,000 | No | $0 |

| Total Income | $200,000 | – | $14,535 |

On a $95,000 salary, your FICA tax comes out to $14,535, while the $105,000 in distributions bypasses payroll taxes entirely. Now, compare this to operating as a sole proprietor or standard LLC, where the full $200,000 would face the 15.3% self-employment tax – resulting in $30,600. By structuring your income with a salary and distributions, you save $16,065 annually in payroll taxes.

Keep in mind, both salary and distributions are still subject to ordinary income tax at your personal rate. However, the $105,000 taken as distributions may also qualify for the 20% Qualified Business Income (QBI) deduction. This could further reduce your taxable income, adding another layer of savings.

Using the Qualified Business Income Deduction (Section 199A)

Once you’ve optimized your salary and distributions, S-Corp owners can take advantage of another tax-saving tool: the Qualified Business Income (QBI) deduction. This deduction, made permanent under the One Big Beautiful Bill Act of July 4, 2025, allows you to deduct up to 20% of your qualified business income from your federal taxable income. For example, if your S-Corp generates $100,000 in QBI, you could reduce your taxable income by $20,000.

It’s important to note that QBI specifically refers to the income reported on your Schedule K-1 – the profit distributions from your S-Corp – not your W-2 salary. However, your salary plays a role in calculating the deduction, particularly for higher-income earners. The deduction is claimed on your Form 1040, whether you itemize or take the standard deduction.

Who Qualifies for the QBI Deduction

Eligibility for the QBI deduction is key to maximizing your tax savings. All S-Corp shareholders can claim the deduction, but the amount depends on taxable income. For 2026, single filers earning less than $203,000 and joint filers earning less than $406,000 qualify for the full 20% deduction. Above these thresholds, the deduction becomes limited by W-2 wages or the business’s property value. For most businesses, the deduction is capped at 50% of W-2 wages or 25% of wages plus 2.5% of qualified property, whichever is higher.

If you’re in a Specified Service Trade or Business (SSTB) – fields like law, accounting, consulting, or financial services – there are stricter rules. For SSTBs, the deduction phases out completely at $278,000 for single filers and $556,000 for those married filing jointly.

| 2026 Filing Status | Full Deduction Below | Phase-Out Range | Complete Phase-Out (SSTB) |

|---|---|---|---|

| Single / Head of Household | $203,000 | $203,000 – $278,000 | $278,000 |

| Married Filing Jointly | $406,000 | $406,000 – $556,000 | $556,000 |

| Married Filing Separately | $203,000 | $203,000 – $278,000 | $278,000 |

Starting in 2026, there’s also a $400 minimum deduction for qualifying businesses with at least $1,000 in active income, even if other factors would normally reduce the deduction to zero.

Example: Calculating Your QBI Deduction

Let’s break down how this deduction works with an example. Suppose your total income is $200,000, with $95,000 as salary and $105,000 in distributions. Your QBI would be $105,000, and you’d qualify for the full 20% deduction. If your taxable income after standard deductions is $175,000, the calculation would look like this:

- QBI: $105,000

- QBI Deduction (20%): $21,000

- New Taxable Income: $175,000 – $21,000 = $154,000

At a 24% marginal tax rate, this $21,000 deduction could save you around $5,040 in federal taxes.

Now, consider a higher-income scenario where your total income is $300,000. You pay yourself a $120,000 salary and take $180,000 in distributions. Here, 20% of your $180,000 QBI equals a $36,000 deduction. However, since your income exceeds the threshold, the 50% wage limitation applies. With 50% of your $120,000 salary equaling $60,000, the deduction is capped at $36,000.

For high earners, balancing distributions and W-2 wages is crucial. A 2.5:1 ratio between QBI and W-2 wages is often recommended – meaning for every $2.50 in distributions, you should allocate at least $1 as salary. This ensures you can claim the full deduction without hitting wage-based limitations. Consulting a tax professional can help you fine-tune this balance and optimize your S-Corp’s tax strategy.

sbb-itb-ba0a4be

Business Deductions and Loss Pass-Through Benefits

Once you’ve fine-tuned your salary and distribution strategies, it’s time to explore additional ways to cut your tax bill. Two key methods for S-Corp owners to reduce taxable income are business expense deductions and loss pass-throughs. Every qualified expense you deduct directly lowers your company’s taxable income – and since this income flows through to your personal tax return, it reduces your personal tax liability as well. If your S-Corp operates at a loss, that loss can offset other income sources, such as wages or investment earnings, further lowering your overall tax burden. Let’s dive into the details.

Common Business Deductions for S-Corps

S-Corps can deduct a wide range of business expenses, from everyday operational costs to specific owner-related expenses. These include:

- Owner Wages and Payroll Taxes: Your own salary and associated payroll taxes are deductible.

- Professional Fees and Advertising: Costs for legal, accounting, and marketing services.

- Operating Costs: Day-to-day expenses necessary for running the business.

If you own more than 2% of the company, your health insurance premiums are deductible by the S-Corp when reported as wages on your W-2. On your personal tax return (Form 1040), you can then deduct 100% of these premiums.

Other deductible expenses include:

- Home-Office Expenses: A portion of your rent, utilities, and other home costs, based on the percentage of your home used exclusively for business.

- Vehicle Costs: You can deduct either the standard mileage rate (72.5 cents per mile for 2025) or actual vehicle expenses, depending on which method benefits you more.

- Equipment Costs: Section 179 allows deductions of up to $2.56 million for equipment purchased and placed in service by 2026. Qualifying assets placed in service after January 19, 2025, may also qualify for 100% bonus depreciation.

- Startup and Organizational Costs: New S-Corps can deduct up to $5,000 each in startup and organizational expenses during their first year, provided total costs stay under $50,000.

To maximize these deductions, documentation is critical. Keep thorough records, receipts, and mileage logs, especially for expenses over $75. Set up an accountable plan – a formal reimbursement policy – to handle out-of-pocket expenses for yourself and employees. Without this, reimbursements could be treated as taxable income by the IRS. Finally, ensure personal and business expenses remain separate to avoid complications during audits.

How Loss Pass-Throughs Work

Operating at a loss isn’t always a bad thing for tax purposes. S-Corp losses pass through to your personal tax return via Schedule E, where they can offset other income sources like wages, interest, or capital gains. For instance, if your S-Corp incurs a $30,000 loss in its first year and your spouse earns $80,000 from their job, your combined taxable income drops to $50,000. This could translate to substantial tax savings.

That said, there are four key rules to navigate before claiming these losses:

- Stock and Debt Basis Limitations: You can only deduct losses up to the amount you’ve invested in the company, including any personal loans you’ve made to it.

- At-Risk Limitations: Losses are limited to the amount of your financial risk in the business.

- Passive Activity Loss Limitations: Losses from passive activities (e.g., businesses you don’t actively participate in) may be restricted.

- Excess Business Loss Limitations: There are caps on the total amount of business losses you can deduct in a given year.

If your losses exceed these limits, they’re suspended and carried forward to future years, where they can be deducted once your basis increases. To stay on top of this, track your basis annually using Form 7203. Remember, it’s your responsibility – not the S-Corp’s – to maintain these records.

Other Benefits of S-Corporations Beyond Taxes

Tax savings often grab the headlines when discussing S-Corporations, but there’s much more to this business structure than just reducing your tax bill. Beyond financial perks, S-Corporations offer legal safeguards and a professional edge that can influence how your business operates, grows, and is perceived by others. Whether you’re dealing with vendors, seeking investors, or planning for the future, these advantages can make a noticeable difference.

Limited Liability Protection

One of the standout benefits of an S-Corp is its ability to protect your personal assets. As a separate legal entity, it creates a "corporate veil" that shields your personal property – like your home, car, or savings – from business creditors and lawsuits. If your company runs into legal trouble or financial difficulties, creditors typically can’t go after your personal assets. As Wolters Kluwer explains, "For business law, compliance requirements, and asset protection purposes, [C and S corporations] are identical".

However, this protection isn’t automatic. To maintain it, you need to follow specific corporate formalities. This includes holding annual meetings, documenting decisions in meeting minutes, and keeping your business and personal finances completely separate. Failing to follow these practices – like mixing funds – could lead to "piercing the corporate veil", where courts may strip away your liability protection. By staying diligent with records and financial separation, you ensure that your personal assets remain secure. These legal protections not only safeguard your finances but also strengthen your business’s foundation.

Improved Business Credibility

Beyond asset protection, an S-Corp structure can enhance how others perceive your business. Incorporating signals a level of professionalism and commitment that resonates with clients, vendors, and financial institutions. As Investopedia points out, "S corp status may help establish credibility with potential customers, employees, suppliers, and investors by demonstrating the owner’s formal commitment to the company".

This credibility can open doors. Banks and investors often view corporations as more stable and reliable, making it easier to secure funding. The structured ownership framework of an S-Corp – with clearly defined shares – also simplifies succession planning and ownership transfers, avoiding potential tax complications. Another key advantage is continuity: your business remains operational even if you step away or pass on, offering stability that partners and clients value.

While tax savings offer immediate financial relief, these structural benefits provide long-term resilience and trustworthiness. Together, they empower business owners to create a solid, credible organization that’s built to last.

Conclusion

An S-Corp can potentially lower your tax bill by anywhere from $5,000 to $50,000 annually. This is thanks to a combination of pass-through taxation, self-employment tax savings on distributions, and the Qualified Business Income (QBI) deduction. Recent updates under the One Big Beautiful Bill Act of 2025 – like permanent 100% bonus depreciation and a $40,000 increase in the SALT cap – make S-Corps even more appealing for businesses generating solid profits.

That said, these benefits come with responsibilities. The IRS audits S-Corps at twice the rate of sole proprietorships, with 73% of those audits focusing on "reasonable compensation" issues. Errors in this area can lead to an average of $31,000 in additional taxes and interest. Because of this, working with a tax professional is crucial.

A tax expert can help you set defensible salary levels, track your shareholder basis, navigate state-specific rules, and optimize your QBI deduction. While preparing Form 1120S can cost between $800 and $2,500 annually, this investment often pays off in both savings and audit protection. Their guidance ensures your strategy aligns with your day-to-day operations.

Administrative tasks shouldn’t become a barrier. Services like BusinessAnywhere’s S-Corp Tax Election Filing handle the initial Form 2553 filing for $147. Additionally, professional payroll services – costing around $40 to $150 per month – can take care of accurate quarterly filings. When paired with expert advice, these tools simplify compliance while helping you capture substantial tax savings.

With the right support, an S-Corp generally makes sense if your net income falls between $60,000 and $80,000 or higher. The key is a thoughtful approach: proper planning, professional guidance, and reliable tools to manage the ongoing requirements. This combination ensures you can fully leverage the S-Corp structure to reduce your tax burden.

FAQs

When does it make sense to elect S-Corp status?

Electing S-Corp status can make a lot of sense for small business owners earning between $60,000 and $80,000 (or more) annually. Why? It’s a smart way to cut down on self-employment taxes. With an S-Corp, profits pass through to your personal tax return, so you avoid the hassle of double taxation. Plus, only your wages – not your distributions – are subject to payroll taxes.

That said, there are some strings attached. To qualify, you’ll need to meet IRS rules, which include paying yourself a reasonable salary and staying on top of payroll and tax filing requirements. It’s a great option, but it does come with responsibilities!

How do I choose a “reasonable salary” for the IRS?

When deciding on a "reasonable salary" for the IRS, think about what someone with your skills and experience would typically earn in a comparable role. Take into account industry norms, your qualifications, the responsibilities of the position, and the amount of time you dedicate to the business. It’s important to maintain thorough records, such as detailed job descriptions and salary benchmarks, to justify your decision. Setting a salary that’s too low could raise red flags and lead to audits, while an overly high salary might hurt your tax efficiency.

Do I owe tax on S-Corp profits I don’t withdraw?

No, you don’t owe taxes specifically on S-Corp profits that you choose not to withdraw. Instead, these retained earnings are passed through to your personal income and taxed as part of your individual tax return. The S-Corp itself doesn’t pay taxes on retained earnings – it’s the shareholders who are responsible for reporting and paying taxes on their share of the profits.