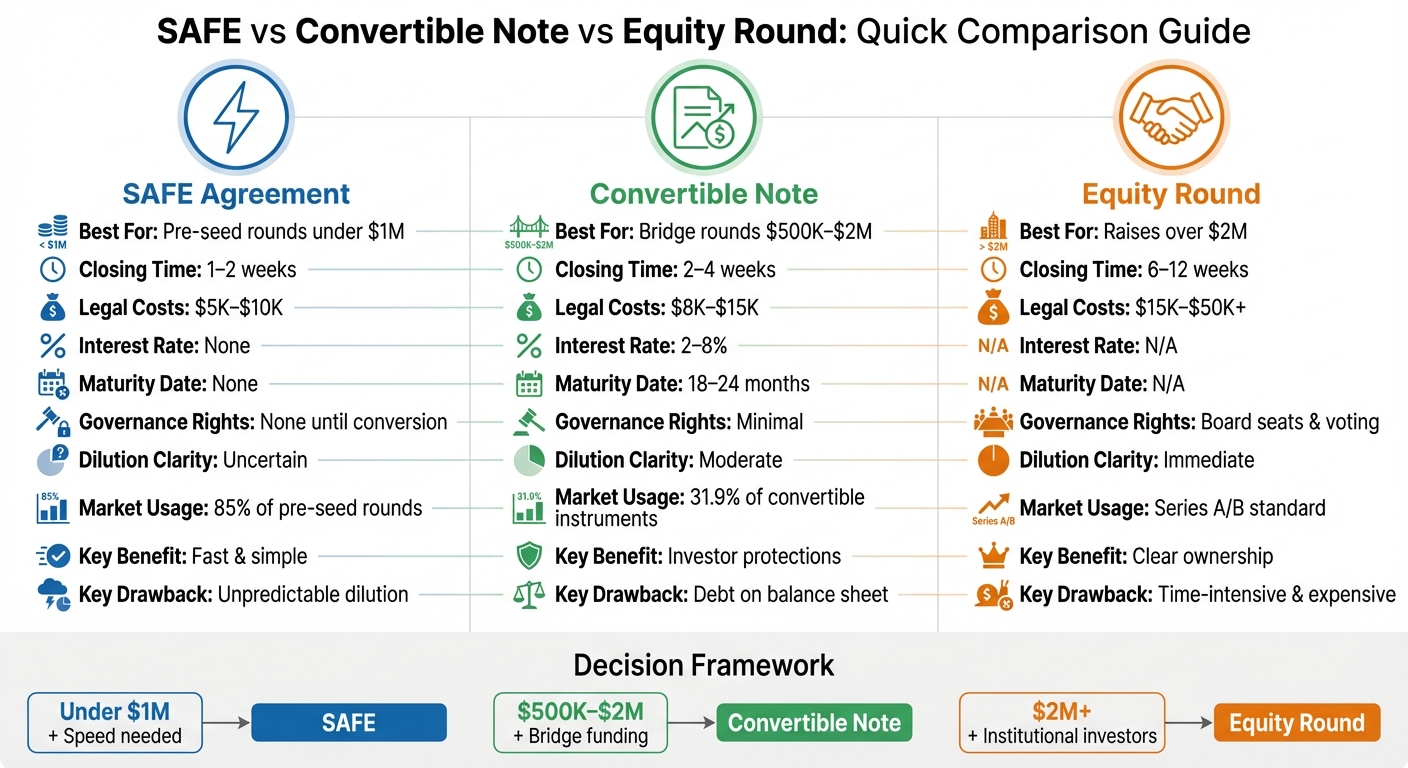

Choosing the right fundraising method is critical for startup success. Here’s a quick breakdown of the three main options for early-stage funding:

- SAFEs (Simple Agreement for Future Equity): Fast and affordable, SAFEs are ideal for pre-seed funding under $1M. They don’t accrue interest or have a maturity date but can lead to unpredictable dilution during conversion.

- Convertible Notes: A hybrid of debt and equity, convertible notes offer investors added protections like interest (2–8%) and repayment obligations. These work well for bridge rounds between $500K–$2M but add complexity due to their debt structure.

- Equity Rounds: Best for raises over $2M, equity rounds provide immediate ownership clarity and governance rights like board seats. However, they are costly and time-intensive, often requiring 6–12 weeks and $15K–$50K+ in legal fees.

Quick Comparison

| Feature | SAFE | Convertible Note | Equity Round |

|---|---|---|---|

| Closing Time | 1–2 weeks | 2–4 weeks | 6–12 weeks |

| Legal Costs | $5K–$10K | $8K–$15K | $15K–$50K+ |

| Interest Rate | None | 2–8% | N/A |

| Maturity Date | None | 18–24 months | N/A |

| Governance Rights | None | Minimal | Board seats, voting |

| Dilution Clarity | Uncertain | Moderate | Immediate |

Your choice depends on your funding stage, timeline, and relationship with investors. SAFEs dominate pre-seed rounds, convertible notes suit bridge funding, and equity rounds are tailored for institutional investments. Plan carefully to avoid dilution surprises or legal complications.

SAFE vs Convertible Note vs Equity Round Comparison Chart

1. SAFE Agreement

A SAFE (Simple Agreement for Future Equity) is an investment tool that gives investors the right to future equity, typically converting during significant events like a Series A funding round, acquisition, or IPO. Unlike traditional loans, SAFEs don’t accrue interest, have no maturity date, and don’t require repayment. This straightforward structure makes them appealing for early-stage startups seeking quick and efficient funding.

The hallmark of a SAFE is its deferred valuation. Instead of determining your company’s current value, investors agree on either a valuation cap (the maximum price at which their investment will convert) or a discount rate (commonly 15%–25% off the future share price). When the company raises a priced round, the SAFE converts into preferred stock at the more favorable of these two options – either the capped price or the discounted price.

SAFEs are designed to be efficient and cost-friendly. They use concise, standardized templates (usually 1–5 pages) and can close within 1–2 weeks, with legal costs ranging from $5,000 to $10,000. This speed is a key reason why SAFEs are now used in 85% of pre-seed funding rounds.

In February 2026, Joshua Ismin, Co-founder and CEO of Psylo, shared: "I was surprised at how quickly a round came together using SAFEs… it just created momentum so much quicker".

Most SAFEs issued today (85%) are "post-money" SAFEs, a standard introduced by Y Combinator in 2018. This version allows investors to immediately calculate their ownership percentage, rather than waiting for the SAFE to convert. However, it also means founders bear the full dilution from multiple SAFEs. If you plan to issue several SAFE rounds, it’s crucial to model your cap table carefully to anticipate the total dilution impact before committing.

| Feature | SAFE Agreement |

|---|---|

| Legal Classification | Warrant / Right to purchase equity |

| Interest Accrual | None |

| Maturity Date | None |

| Typical Length | 1–5 pages |

| Closing Timeline | 1–2 weeks |

| Legal Costs | $5,000–$10,000 |

| Investor Rights | No voting or board rights until conversion |

Up next, we’ll dive into how convertible notes stack up in terms of structure and investor protections.

sbb-itb-ba0a4be

2. Convertible Note

A convertible note is essentially a short-term loan that transforms into equity during a future funding event, like a Series Seed or Series A round. Unlike SAFEs, convertible notes are considered liabilities on your balance sheet. This structure creates a creditor-investor relationship, offering investors stronger protections, such as priority repayment rights if the company faces liquidation.

Convertible notes have three distinct features that set them apart from SAFEs: interest accrual, a maturity date, and repayment obligations. Interest typically accrues at an annual rate of 2%–8% and converts into equity during the financing event. The maturity date, often set between 18 and 24 months, acts as a deadline for conversion. If no qualified financing round – commonly defined as raising at least $1 million – occurs before this date, investors can demand repayment in cash.

"A Convertible Note worked well for Cake as we were able to obtain early funding which allowed us to build and grow, while avoiding the delays and complications of a valuation", shared Jason Atkins, President & CEO of Cake Equity.

The process of setting up a convertible note is more involved than a SAFE. It typically requires 10–15 pages of documentation, takes 2–6 weeks to finalize, and incurs legal fees ranging from $8,000 to $15,000. This added complexity reflects the debt-based nature of the instrument and the stronger protections it provides to investors. Convertible notes are particularly popular in markets like biotech and hardware – industries with longer development cycles and tangible assets – where the debt structure aligns well with investor expectations.

In 2025, convertible notes made up about 15% of pre-seed funding rounds, with SAFEs dominating the remaining 85%. However, by early 2024, convertible notes accounted for 31.9% of all convertible instruments, signaling a preference for structured terms and downside protections. If you’re raising $2 million or more, working with traditional angel investors, or operating in a capital-heavy industry, a convertible note could be the more suitable option. Next, we’ll dive into equity rounds, which provide immediate ownership clarity and governance advantages.

3. Equity Round

An equity round, often referred to as a priced round, involves selling newly issued shares of your company to investors at a set price per share. Unlike SAFEs or convertible notes, this approach determines the company’s valuation upfront (known as the pre-money valuation), and investors immediately become shareholders upon closing the deal. This means ownership is established right away, avoiding any delays tied to conversions.

Investors in equity rounds gain a range of protections, which often include voting rights on key company decisions, board seats or observer roles, liquidation preferences (ensuring they receive at least 1x their investment before other payouts during a sale), anti-dilution clauses, and pro-rata rights to maintain their ownership percentage in future funding rounds. These governance features provide clear ownership structures, making equity rounds especially appealing for startups planning to scale and for institutional venture capital firms looking to invest several million dollars or more.

"A priced round is an important step in the development of a startup. It is typically chosen when a large amount of money needs to be raised (several million dollars or more)." – ICLUB

However, these added protections come with increased complexity and cost. Equity rounds require extensive legal documentation – often 50–100+ pages – and typically take 6 to 12 weeks to finalize, compared to the faster 2 to 4 weeks for a SAFE. Legal fees alone can fall between $15,000 and $50,000. The process generally involves four key stages:

- Preparing a data room and financial models (2–4 weeks)

- Marketing to investors and negotiating term sheets (3–6 weeks)

- Conducting due diligence (2–4 weeks)

- Finalizing legal documentation and closing (2–3 weeks)

This structured, time-intensive process stands in stark contrast to the simplicity and speed of SAFEs or convertible notes.

Equity rounds are commonly seen in Series A and Series B funding. Series A rounds typically value companies between $10 and $30 million, with investments ranging from $2 to $15 million. Series B rounds, on the other hand, often value companies between $30 and $100 million, with investments of $7 to $30 million. For startups raising less than $2 million, the high costs and extended timelines of an equity round could result in a 20–40% lower valuation. However, for growth-stage companies with stable business models and institutional investors seeking formal governance structures, equity rounds offer the clarity and protections that have made them standard practice in the industry.

Next, we’ll explore the benefits and trade-offs of these fundraising methods.

Pros and Cons

Choosing the right fundraising method is all about weighing the trade-offs. Each option – SAFE, convertible note, or equity round – has its own set of benefits and drawbacks for both founders and investors. The key is to align the choice with your company’s stage, funding needs, and the relationships you’re building with investors.

SAFEs are known for their speed and simplicity. They can close in as little as 1–2 weeks, with legal costs ranging from $0 to $10,000. Founders appreciate that SAFEs don’t accrue interest or have a maturity date, which removes the pressure of repayment. However, the flip side is the risk of unpredictable dilution at the time of conversion. Post-money SAFEs, which make up 85% of the market, can dilute founders more significantly than pre-money SAFEs when multiple agreements are in play. For investors, SAFEs offer pre-set terms that protect against early-stage risks, but they don’t include governance or voting rights. Additionally, in the event of liquidation, SAFEs rank below debt.

Convertible notes offer a middle ground by acting as debt that eventually converts into equity. They allow founders to defer valuation decisions and come with tax-deductible interest payments. This structure is familiar to many traditional investors, but it comes with its own challenges. Convertible notes add debt to the company’s balance sheet and include a maturity date (typically 18–24 months), which could force repayment or a rushed funding round. For investors, the appeal lies in their seniority during liquidation and a guaranteed return through interest rates ranging from 2–8%. However, convertible notes are more complex and expensive than SAFEs and don’t provide immediate ownership or voting rights.

Equity rounds, on the other hand, provide immediate clarity on ownership and governance. They are particularly attractive to institutional venture capitalists and come with benefits like board involvement and access to expert advice. However, these rounds are the most expensive and time-consuming option. Legal fees can range from $15,000 to over $50,000, and the process often takes 6–12 weeks to finalize. Founders also have to give up some control by granting board seats and voting rights. For investors, equity rounds offer strong protective provisions, such as anti-dilution clauses and liquidation preferences, but require upfront agreement on the company’s valuation and involve extensive due diligence.

Here’s a quick comparison of the key features:

| Feature | SAFE | Convertible Note | Equity Round |

|---|---|---|---|

| Closing Time | 1–2 weeks | 2–4 weeks | 6–12 weeks |

| Legal Costs | $0–$10,000 | $2,000–$15,000 | $15,000–$50,000+ |

| Interest Rate | None | 2–8% | N/A |

| Maturity Date | None | 18–24 months | N/A |

| Repayment Risk | None | High (at maturity) | None |

| Governance Rights | None | Minimal | Board seats & voting |

| Liquidation Priority | Junior to debt | Senior to SAFEs | Preferred status |

| Dilution Clarity | Uncertain until conversion | Moderate | Immediate and clear |

"Convertible promissory notes are a win-win for some investors. Where investors are more risk averse… they may want the option of getting their money back." – Gabriela Suarez, Agile investment expert, SeedLegals

Among SAFEs, 61% follow a "Valuation Cap Only" structure, while 30% combine valuation caps with discounts. This preference highlights the appeal of simplicity and speed in early-stage fundraising. However, trends vary by location. SAFEs dominate pre-seed rounds in Silicon Valley (used in over 95% of deals), while convertible notes are more popular in cities like New York (50%) and Boston (40%), as well as in international markets.

Conclusion

Each fundraising method serves a distinct purpose, depending on your funding goals, timeline, and investor expectations. Whether you opt for SAFEs, convertible notes, or equity rounds, your decision will significantly influence your startup’s trajectory. For pre-seed rounds under $1 million, SAFEs are often the go-to choice, especially for tech startups – 95% of pre-seed deals in Silicon Valley now use this structure. If you’re raising between $500,000 and $2 million for a bridge round, convertible notes may be a better fit, offering the familiarity of a debt instrument with a clear maturity date. On the other hand, equity rounds are typically best for startups raising over $2 million, particularly when institutional venture capital and formal governance structures come into play.

The time and cost involved also vary across these methods. SAFEs are quicker and more affordable, typically taking 2–4 weeks and costing $5,000–$10,000 to execute. Convertible notes and equity rounds, however, require more time and resources, with equity rounds often taking 6–12 weeks and costing upwards of $15,000–$50,000. SAFEs stand out for their simplicity – no maturity date, no interest, and no repayment pressure. In contrast, convertible notes include an 18–24 month term and accrue interest at rates of 5–8% from the start.

Before committing to any agreement, use a cap table calculator to assess potential dilution. This is especially important with post-money SAFEs, which account for 85% of the market and can dilute founders more than expected when multiple instruments convert at Series A. If you’re using a convertible note, plan your next fundraising round at least six months before its maturity date to avoid last-minute repayment stress or tough extension negotiations.

Ultimately, the best choice depends on your startup’s stage and long-term goals. Early-stage founders working toward product-market fit may lean toward the simplicity of SAFEs. Those needing to extend their runway before hitting a major milestone might find convertible notes more suitable. Meanwhile, startups ready for institutional investment and strategic input will benefit from the structure and governance that come with an equity round.

FAQs

How do valuation caps and discounts affect my dilution?

Valuation caps and discounts play a key role in shaping how much ownership founders retain during funding rounds by influencing how investments convert into equity.

A valuation cap establishes the highest company valuation at which an investor’s note converts into equity. This means early investors can purchase shares at a lower price if the company’s valuation exceeds the cap, leading to greater dilution for the founders.

On the other hand, discounts let investors convert their notes into equity at a reduced rate compared to the valuation in future funding rounds. This also results in more shares being issued to investors, which further dilutes the founders’ ownership.

Striking the right balance when negotiating these terms is essential to protect ownership stakes while still attracting early investment.

What happens if a convertible note hits maturity before a priced round?

If a convertible note reaches its maturity date before a priced round occurs, the startup usually has two main paths forward: repaying the principal along with any accrued interest or renegotiating the terms with investors. Maturity often activates clauses requiring repayment or conversion, which means startups might need to extend the note’s timeline or agree on updated terms to prevent having to pay back the note immediately.

When is it worth doing an equity round instead of another SAFE?

An equity round makes sense when your business has an established valuation or you’re looking to raise a large amount of capital – think amounts over $2 million. This approach gives investors immediate ownership and voting rights, ensuring clarity in the ownership structure. It’s a solid choice for more developed startups that want to steer clear of the potential complexities or dilution risks associated with SAFEs, particularly if you’re planning multiple funding rounds or entering strategic partnerships.