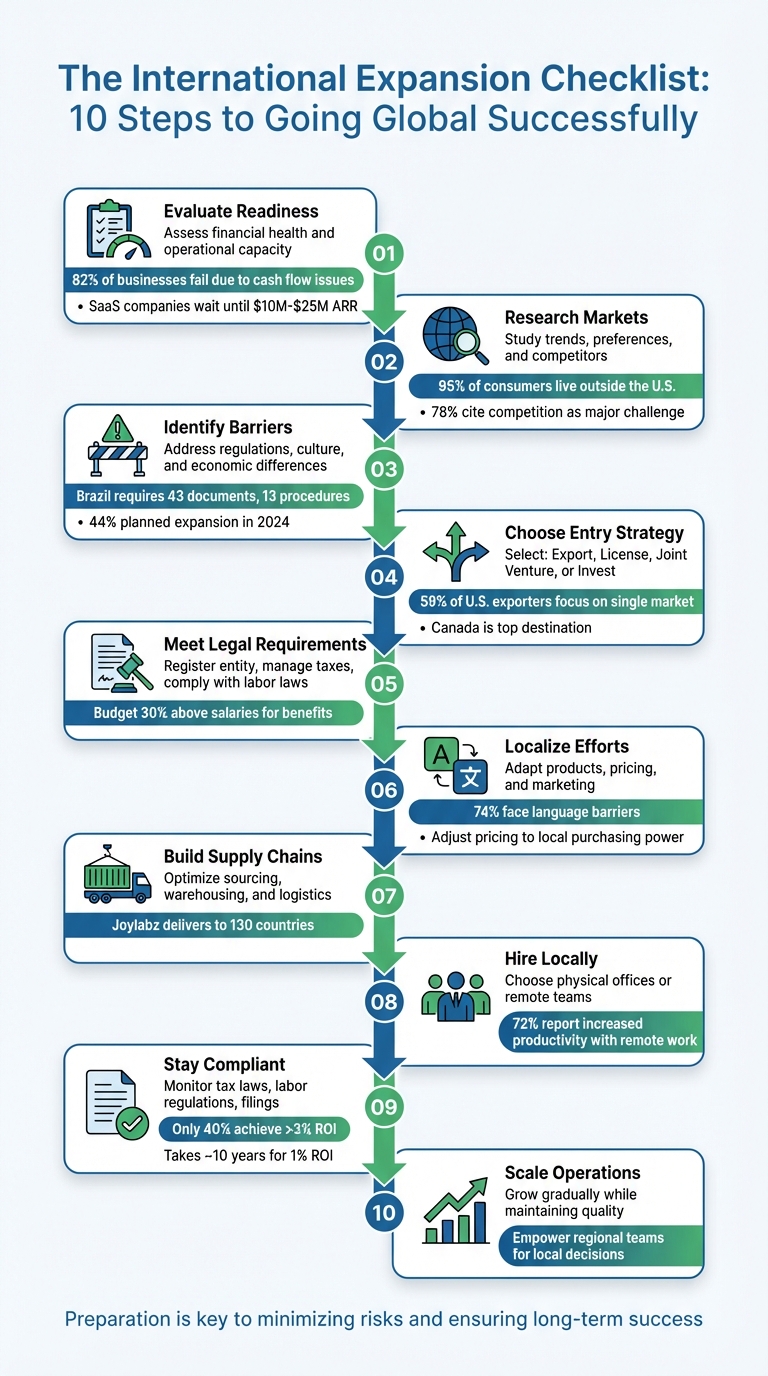

Expanding your business internationally can be rewarding, but it’s also challenging. Without proper planning, you risk financial losses, legal issues, and operational setbacks. Here’s a quick guide to help you succeed:

- Evaluate Readiness: Ensure your financial health and operations can support expansion.

- Research Markets: Identify target markets by studying trends, customer preferences, and competitors.

- Address Barriers: Understand local regulations, taxes, and cultural differences.

- Choose Entry Strategy: Options include exporting, licensing, joint ventures, or direct investments.

- Meet Legal Requirements: Register entities, manage taxes, and comply with labor laws.

- Localize Efforts: Tailor products, pricing, and marketing to match local expectations.

- Build Supply Chains: Optimize sourcing, warehousing, and logistics for efficient delivery.

- Hire Locally: Decide between physical offices or remote teams, and onboard the right talent.

- Stay Compliant: Monitor tax laws, labor regulations, and corporate filings.

- Scale Operations: Gradually grow while maintaining quality and compliance.

Preparation is key. Use tools and services to manage compliance, streamline operations, and focus on growth. This checklist helps minimize risks and set your business up for long-term success.

10-Step International Business Expansion Checklist

Step 1: Evaluate Your Business’s Readiness for International Expansion

Before diving into international markets, take a hard look at your financials and operations. Cash flow issues are a leading cause of business failure – 82% of businesses fail because of them. Expanding internationally only amplifies these risks. For example, U.S.-based Enterprise SaaS companies often wait until they reach $10M to $25M in Annual Recurring Revenue (ARR) before entering global markets. This isn’t random – it’s because a successful expansion requires both financial strength and operational stability.

Review Financial Health and Cash Flow

Start by calculating your Operating Cash Flow (OCF) – the net cash your core business generates. Then, subtract capital expenditures from OCF to determine your Free Cash Flow (FCF), which is what you can use for discretionary investments. To ensure financial flexibility, aim for a Working Capital Ratio (current assets divided by current liabilities) between 1.2 and 2.0.

Run financial scenarios to prepare for potential challenges. For instance, simulate a 10% drop in domestic sales alongside a 20% increase in expansion costs. This will help you understand your Cash Burn Rate – how long you can sustain operations before reaching profitability. As Ken Boyd, an Accounting and Finance Expert at Ramp, explains:

"Strong cash flow management is one of the most reliable indicators of business survival and long-term resilience".

Also, check your accounts receivable. If it takes more than 60 days to collect payments domestically, you might face liquidity issues when funding international operations.

Once you’ve clarified your financial metrics, it’s time to evaluate whether your operations are ready to scale globally.

Check if Your Operations Can Scale

Expanding internationally means your operations must handle increased complexity. In fact, 73% of U.S. business leaders say entering new markets is a major challenge. Start by asking yourself: Can your onboarding, fulfillment, and customer support processes work seamlessly without constant oversight? Are these processes documented well enough for a new team in another country to replicate?

Be honest about your team’s capacity. Forty-one percent of executives point to local talent shortages as a key barrier to growth. Your current team may already be stretched thin. Map out every core workflow to identify dependencies on specific individuals or systems. Use cloud-based tools to centralize documentation and enable cross-border collaboration.

To test your readiness, consider a pilot strategy. For example, partner with a local distributor or test an online marketplace before committing to a full-scale rollout. This approach allows you to evaluate whether your infrastructure can handle multiple time zones, currencies, and regulatory requirements without becoming overwhelmed.

A solid foundation in both financial and operational readiness is essential for navigating the next steps in your international expansion journey.

sbb-itb-ba0a4be

Step 2: Research Your Target Markets

After confirming your business is ready for expansion, the next step is developing a global expansion strategy to select the right markets. Here’s a staggering fact: 95% of the world’s consumers live outside the United States. That’s a huge opportunity, but success hinges on choosing markets wisely and understanding what those customers want.

Study Market Trends and Customer Preferences

Start with secondary research to get a broad understanding of potential markets. Resources like the CIA World Factbook, World Bank Data Catalog, and UN Statistical Yearbook can provide valuable insights into population demographics, income levels, and industry trends. For a more detailed look, check out the Country Commercial Guides (CCGs) from the U.S. Commercial Service. These guides break down market conditions, regulations, and opportunities by country.

Another useful tool is TradeStats Express, which lets you analyze U.S. export data and compare it to a target country’s import trends. For instance, if exports from the U.S. to a specific country are growing faster than that country’s overall imports, it’s a strong signal of demand for American products.

Once you’ve identified three to five promising markets, dive into primary research. This means going beyond the numbers – conduct surveys, organize focus groups, or interview potential customers to uncover their specific needs. Attending international trade shows is another excellent way to test your product’s appeal and gather direct feedback. These hands-on methods can reveal details that data alone can’t, like preferred payment systems (e.g., iDEAL in the Netherlands, WeChat Pay in China) or popular communication platforms (e.g., WhatsApp, LINE).

This research lays the groundwork for understanding your competition.

Analyze Local Competitors

Knowing your competition is essential – 78% of U.S. business leaders say it’s a major challenge in international expansion. Start by identifying the key players in your target market. Who are they, how much market share do they control, and where are they located?. Evaluate their pricing strategies and the perceived value of their products to find a competitive price point for your offerings.

You can also compare U.S. export data with your target country’s import statistics to see where U.S. companies are already thriving. Tools like the Top Export Market Rankings can help you analyze the competitive landscape in your industry. Look for gaps in the market – areas where local competitors aren’t meeting customer needs or where your product can stand out.

Don’t just focus on price. Consider other factors like logistics, customer service, and localization. For example, if local competitors offer faster shipping or more flexible payment options, you’ll need to meet or exceed those standards to stay competitive.

Step 3: Identify Entry Barriers and Risks

After pinpointing promising markets and evaluating the competition, the next step is to address potential obstacles that could disrupt your expansion plans. Every international market presents its own challenges, including regulatory requirements, cultural differences, and economic uncertainties. Ignoring these factors can lead to costly mistakes. For example, operating in Brazil may require navigating 43 documents and 13 procedures. Recognizing these hurdles in advance is essential.

Research Regulatory and Compliance Requirements

Dealing with foreign regulations can be tricky. Start by understanding the import and export documentation required for your target market. For instance, U.S. exporters must use the Automated Export System (AES) to report shipments valued at $2,500 or more. Skipping this step could result in border delays or fines.

Product standards and certifications are another common challenge. Many regions enforce strict requirements, such as the EU’s CE mark or China’s CCC certification, which involve thorough testing and labeling processes. Additionally, familiarize yourself with corporate taxes, VAT, and local sales taxes, as setting up a business presence may require collecting and remitting these taxes.

Intellectual property (IP) protection is another area to prioritize. A U.S. trademark or patent doesn’t automatically apply internationally, so you’ll need to register your IP locally or through systems like the Madrid Protocol. This step ensures your brand is protected and helps you avoid costly rebranding efforts down the line. Keep an eye on data privacy laws, too – regulations like the EU’s GDPR dictate how personal data is handled and transferred across borders.

Choosing the right business structure is equally critical. A subsidiary can provide tax advantages and limit liability, while a branch office ties profits, losses, and liabilities directly to the parent company. Michael Patterson, Partner at Spencer Fane, emphasizes the importance of planning ahead:

"You can make a lot of money in a destination country, but if you didn’t plan it right tax-wise, it can really hurt."

To ensure compliance, explore Country Commercial Guides from the U.S. Commercial Service for insights into market-specific requirements. Use the Consolidated Screening List (CSL) to vet foreign partners and confirm they’re eligible to receive exports. Secure a local tax ID early to ease banking, hiring, and tax filing processes, and work with local tax advisors or labor lawyers to navigate complex regulations.

Once regulatory challenges are addressed, shift your focus to understanding the cultural and economic landscape of your target market.

Understand Cultural and Economic Differences

Legal compliance is only part of the equation – cultural and economic factors play a significant role in shaping your market strategy. Begin by examining macroeconomic indicators like GDP growth, inflation, employment rates, and purchasing power parity. These metrics can help you gauge the market’s economic stability and whether customers can afford your product.

Cultural norms and communication styles also demand attention. Some cultures prefer direct communication, while others lean toward more subtle approaches. Business etiquette varies widely – what’s considered professional in the U.S. might come across as too casual or even offensive elsewhere. A 2023 survey of C-suite executives revealed that 44% of businesses planned to expand internationally in 2024, but many underestimated the importance of cultural adaptation.

Localization is key to bridging these gaps. Tailor your messaging to reflect local customs and values, and ensure customer support operates in local time zones on popular platforms like WhatsApp, LINE, or WeChat. Pricing strategies should also be localized – what’s considered premium in one market might be standard or overpriced in another.

Payment preferences vary by region, so offer local options like iDEAL in the Netherlands, WeChat Pay in China, or digital wallets in India to simplify transactions. Additionally, adapt your website’s user experience (UX) to accommodate local address formats, phone number structures, and even right-to-left layouts for languages like Arabic or Hebrew.

Hiring local talent can be a game-changer. Employees familiar with the local culture, laws, and customer behavior can help you fine-tune your approach and avoid costly mistakes. They can also adapt your value proposition to better resonate with local audiences. Lastly, setting up a local bank account is crucial for managing in-country payments like payroll. Be prepared for lengthy "know your client" procedures during this process.

Step 4: Select Your Market Entry Strategy

Once you’ve assessed market conditions and potential barriers, the next step is choosing the right entry strategy. Your decision should balance factors like capital investment, control, and risk tolerance. Different industries and goals call for different approaches, and here are some common strategies to consider.

Exporting is a quick and cost-effective way to enter a market. By selling products directly or through local distributors, you can test demand without setting up a legal entity in the target country. While this approach minimizes upfront costs, it also limits your control over how distributors handle your brand. Interestingly, about 59% of U.S. exporters focus on a single market, with Canada being the top destination.

If your business relies heavily on intellectual property, licensing and franchising can offer lower-risk pathways to market entry. Licensing involves granting a local company the rights to use your intellectual property in exchange for royalties. This reduces financial exposure but requires careful oversight to protect your brand and IP. Franchising, on the other hand, allows local operators to run businesses using your established model. This method accelerates expansion and shifts much of the financial burden to franchisees, though maintaining brand consistency across borders can be a challenge.

For markets that require deeper integration, joint ventures and strategic alliances are worth exploring. A joint venture involves co-owning a business with a local partner, enabling you to share both the risks and rewards while gaining immediate access to local expertise. A strategic alliance, by contrast, allows for collaboration without creating a new legal entity, offering more flexibility. Both options require strong partnerships and clearly defined roles to succeed.

If you’re ready to fully commit resources, acquisitions and greenfield investments provide the highest level of control. Acquiring a local business offers instant access to infrastructure, market presence, and operations. However, it comes with high costs and full exposure to risk. Building operations from scratch – known as a greenfield investment – demands even more time and capital but allows you to design everything to fit your exact needs. As Greg Sandler from American Express points out:

"Formulating a strategy for going global requires the same kind of planning and market analysis needed for success in domestic markets".

Ultimately, your choice of market entry strategy should align with your product’s complexity, your risk appetite, and the market’s strategic importance. For key markets central to your long-term growth, it may make sense to invest heavily upfront. For smaller or experimental markets, starting lean with exporting or partnerships can be a smarter move. Once your strategy is set, the next step is to focus on localizing operations and building the necessary infrastructure.

Step 5: Meet Legal and Regulatory Requirements

Navigating legal and regulatory requirements can feel like an uphill battle, especially with varying standards across different countries. Take Brazil, for instance – starting a business there requires 43 documents and more than 13 official procedures. Even in countries with simpler processes, dealing with tax filings, labor laws, and entity registration can be a maze of paperwork and deadlines. That’s why choosing the right business structure is a critical first step toward aligning with your international goals.

Start by deciding on a structure – whether it’s a subsidiary, branch, or representative office – since each comes with its own tax and liability considerations. Once you’ve made your choice, proceed with filing incorporation documents, drafting corporate bylaws, and appointing a board of directors.

Tax compliance is another major piece of the puzzle. Obtain a local tax ID (like an EIN in the U.S.), register with both national and local authorities, and determine if your business has a "nexus" that could trigger sales tax obligations. To optimize inter-company transactions, conduct a transfer pricing study. As Michael Patterson, Partner at Spencer Fane, warns:

"You can make a lot of money in a destination country, but if you didn’t plan it right tax-wise, it can really hurt".

Labor regulations are equally vital. Make sure employment contracts align with local laws, and budget an additional 30% on top of base salaries for benefits and payroll administration. If you’re hiring international staff, don’t forget to secure work visas, set up payroll withholding, and provide mandatory benefits. For businesses operating across multiple states, filing for foreign qualification ensures you notify local authorities as required.

To stay on top of compliance, services like BusinessAnywhere can help. Their registered agent and compliance alert system offers a legal address and ensures you don’t miss important filings, all for $147 annually after the first free year. For more complex issues – like opening local bank accounts, navigating KYC (Know Your Customer) requirements, or managing statutory reports – partnering with local experts is a smart move.

Step 6: Localize Your Products, Services, and Marketing

Once you’ve assessed market risks and strategies, the next step is tailoring your products, services, and marketing to fit local needs. Localization goes beyond translation – it’s about adapting every aspect of your offering, from language and pricing to user experience and customer support, to align with local expectations and cultural norms.

Start with language and messaging. A word-for-word translation won’t cut it. You’ll need to adjust tone, humor, and even your value proposition to resonate with local audiences. For example, what works in one region might feel tone-deaf in another. In fact, 74% of U.S. business leaders report that language barriers are a major challenge when entering new markets.

Pricing is another area where adaptation is crucial. Simply converting $49/month to another currency won’t work. Instead, align your pricing with local purchasing power. For instance, a $49/month subscription in the U.S. might need to drop to $19/month in Southeast Asia to remain accessible. Display prices in local currency to reduce confusion, and consider how taxes are shown. While European customers expect tax-inclusive pricing, U.S. shoppers are accustomed to seeing taxes added at checkout.

Payment methods are equally important. Credit cards may dominate in some markets but are less common in others. Offer locally preferred payment options – like iDEAL in the Netherlands, Alipay in China, or digital wallets in India – to ensure smooth transactions. Similarly, adapt your user interface to accommodate local address formats and phone number conventions.

Customer support is another critical piece. Providing help in the local language and time zone can make a huge difference. Use the communication platforms your audience prefers – such as WhatsApp in Latin America, LINE in Japan, or WeChat in China. Other adjustments, like customizing packaging or introducing mobile-only subscription tiers, can also enhance your product’s appeal.

Step 7: Establish Supply Chains and Logistics

Getting your products to customers in different countries isn’t as simple as picking a shipping carrier. It involves making strategic choices about sourcing, warehousing, and delivery to balance speed, cost, and control.

First, decide where to manufacture or source your products. Working with local suppliers in your target market can cut down on lead times and production costs, helping you respond quickly to customer needs. On the other hand, if you choose to keep production in your home country, expect longer shipping times and higher freight costs. To find reliable suppliers, use directories like Alibaba, ThomasNet, or Global Sources, and protect payments with tools like Alibaba’s Trade Assurance.

This logistical planning works hand-in-hand with your localized marketing efforts, ensuring that your products reach customers efficiently and without unnecessary costs.

When it comes to warehousing, you have two main paths. Third-Party Logistics (3PL) providers can handle storage, packing, and returns, making it an excellent option for testing new markets without a major upfront investment. For instance, Joylabz partnered with Shipwire in 2012 to fulfill orders across 130 countries. Rachel Silver, Joylabz’s Customer Relations Manager, explained:

"Now, if a kid halfway around the world watches our video and is inspired, he can get a Makey Makey delivered in just a few days without paying exorbitant shipping fees".

Alternatively, setting up your own warehouse gives you full control over operations, but it requires significant investment and comes with the added complexity of managing local labor laws.

Shipping speed and cost are critical factors. Private carriers like DHL, FedEx, and UPS offer quick delivery and handle customs paperwork, but they come at a premium. National postal services may be a more affordable option for domestic deliveries in developed markets. Be sure to calculate your total landed cost – which includes product price, shipping, customs duties, and local taxes – before finalizing pricing. To simplify this process, consider using cloud-based tax compliance tools like Avalara.

For managing correspondence, services like BusinessAnywhere’s Virtual Mailbox can provide a U.S. address for mail forwarding and administrative support. To keep your global teams aligned across time zones, tools like Slack, Asana, or Notion can be invaluable.

Step 8: Set Up Local Operations and Hire Staff

After sorting out your supply chain, the next step is building your local team. Whether you go for a physical office, hire remotely, or opt for a hybrid setup depends on factors like how much risk you’re willing to take, how quickly you want to enter the market, and how much control you need. Each option comes with its own set of challenges and advantages.

Setting up a physical office gives you direct oversight, which can help maintain your brand’s integrity and improve customer experience. However, it’s a costly and time-consuming process that requires a significant upfront investment. On the other hand, hiring remotely through an Employer of Record (EOR) service can be much faster. It allows you to onboard employees in just a few days without the need to establish a local legal entity. Plus, remote work has been shown to boost productivity – 72% of companies reported increased efficiency after adopting a globally distributed workforce model. Job van der Voort, CEO and Co-founder of Remote, highlights the benefits:

"Hiring international employees gives your company a soft landing when entering new markets and allows you to build trust quickly in new places."

For businesses offering highly technical or service-intensive products, having a local physical presence might be essential to provide specialized support. But if you’re working with a smaller budget or simply testing the waters in a new market, starting with a remote model can be a smart move.

To make remote operations run smoothly, centralize all documentation using cloud-based tools. This ensures everyone stays on the same page, even across time zones. Also, consider rotating meeting schedules to distribute the burden of off-hour calls more evenly. For U.S.-based companies looking to expand internationally, services like BusinessAnywhere’s Virtual Mailbox provide a professional U.S. address for mail handling and administrative tasks. Additionally, their Registered Agent services help ensure compliance with state regulations.

Finally, give your regional teams the autonomy to make decisions tailored to their local markets – like pricing, marketing strategies, and customer support – while still adhering to your company’s core standards. This balance between local flexibility and global consistency is key to scaling your business effectively.

Step 9: Maintain Compliance and Scale Your Operations

Once you’ve set up solid local operations, it’s time to focus on two key areas: staying compliant and scaling your business effectively. These tasks require ongoing attention to tax laws, labor regulations, corporate governance, and data protection rules. Overlooking even minor details – like a missed filing or a regulatory update – can lead to hefty fines, legal trouble, or even shutting down your operations.

The rules and requirements differ widely from country to country. For instance, you may need to handle VAT or GST registrations, file corporate income taxes, submit quarterly tax estimates, and manage customs duties if you’re shipping products internationally. Employment laws are another moving target – policies and contracts must be regularly updated to align with local changes. Many regions also demand annual audits, consolidated financial statements, and interim reports to meet legal standards.

To keep up with these requirements, automation can be your best ally. Tools like QuickBooks or Xero can help you manage international transactions and prepare financial statements. If you’re a U.S.-based business, services like BusinessAnywhere provide compliance alerts and annual filing assistance to ensure you meet both state and federal deadlines. Additionally, storing your documents in cloud-based platforms can streamline collaboration across time zones. With these systems in place, you’ll be better prepared to tackle the complexities of scaling.

When it comes to growth, proceed cautiously. Statistics show that only 40% of companies expanding internationally achieve more than a 3% ROI, and it often takes a decade to see even a modest 1% return. To improve your odds, empower your regional teams to tailor pricing, marketing, and customer support to local needs while keeping core brand standards centralized. If you’re hiring in countries like the U.S., plan to budget at least 30% above base salaries to cover benefits and payroll taxes.

At this stage, bringing in local experts can make all the difference. Tax consultants, HR advisors, and legal professionals with in-depth knowledge of specific markets can help you navigate the complexities. Take Brazil, for example – scaling there might involve 13 official procedures and 43 separate documents. It’s a lot to manage, but with the right tools, people, and processes, you can grow your operations efficiently while staying compliant.

Conclusion

Expanding internationally is a bold move, but when done thoughtfully, it can yield impressive results. By working through this checklist – evaluating your readiness, researching markets, setting up local operations, and staying compliant – you can minimize risks and position your business for steady growth. A structured plan helps navigate the challenges and reap the rewards of global expansion.

Statistics show that it can take around 10 years to achieve even a modest 1% ROI, with only 40% of companies surpassing a 3% ROI. However, careful preparation significantly increases the likelihood of success.

For businesses looking to streamline the process, tailored services can make a big difference. Platforms like BusinessAnywhere handle complex tasks such as U.S. business registration, registered agent services, compliance alerts, and virtual mailbox solutions. These tools free up your team to focus on growth and customer acquisition, leaving the administrative headaches behind.

FAQs

How can a business determine if it’s ready to expand internationally?

Expanding into international markets can be a game-changer, but it requires careful preparation. The first step? Financial stability. Your business needs a solid financial base to handle the costs of expansion without putting your current operations at risk.

Next, having clear goals and a well-thought-out strategy is essential. This includes identifying target markets, understanding your competitive edge, and planning for compliance with local laws. Speaking of compliance, knowing the ins and outs of local regulations – like tax laws and employment standards – is non-negotiable. Skipping this step could lead to costly mistakes.

Operational readiness is another key factor. Can your supply chain handle the demands of a new market? Are your products or services tailored to local preferences? And don’t overlook the challenges of managing remote teams – this requires strong systems and communication tools.

Lastly, success in a new market often hinges on your ability to navigate cultural differences and cater to market-specific consumer needs. Understanding these nuances can help you build trust and connect with your new audience.

By taking a close look at these areas, you can gauge whether your business is ready to embrace the challenges – and opportunities – of going global.

What’s the best way for companies to handle cultural differences when expanding into a new market?

Understanding and respecting cultural differences is key when entering a new market. Start by diving into the local customs, communication styles, and business norms. This effort not only helps you grasp what matters to the community but also minimizes the risk of misunderstandings, paving the way for trust with local customers and partners.

Adapting your approach is equally important. Businesses should adjust their products, marketing strategies, and customer service to align with local preferences. This could mean ensuring translations are spot-on, shaping branding to reflect regional values, or being mindful of local sensitivities. Demonstrating respect for the culture and showing a willingness to adapt builds stronger connections and earns credibility in the market.

What are the biggest challenges with international compliance, and how can businesses overcome them?

Expanding into international markets comes with its fair share of challenges. From navigating intricate legal systems to managing tax requirements and adhering to local employment laws, the process can feel overwhelming. The good news? These hurdles can be tackled effectively with thorough market research and by collaborating with local experts, such as legal advisors or tax consultants, who understand the regulations specific to each country.

Equally important is recognizing and respecting cultural differences. Aligning your operations, marketing strategies, and customer service to local preferences can make a world of difference. Building strong relationships with reliable local partners and utilizing tools designed to handle compliance tasks – like tax filings and employment regulations – can also streamline the process. With careful planning and expert guidance, businesses can reduce risks and set the stage for a smoother path to global growth.