When you hire remote employees in different states, your business may be legally required to comply with that state’s payroll tax rules. This is due to state tax nexus, which is triggered when an employee physically works in a state, even if your company isn’t based there. Here’s what you need to know:

- Payroll Obligations Start Immediately: Many states require payroll tax withholding and unemployment insurance registration from day one of an employee working in the state. Unlike how economic nexus affects remote businesses, no revenue threshold applies.

- State-Specific Rules: Rules vary widely. For example, some states base withholding on wages earned, while others use workday thresholds. In 21 states (e.g., Ohio, Pennsylvania), withholding starts immediately.

- Penalties for Non-Compliance: Failing to register or withhold taxes can result in back taxes, penalties, and interest. Some states can audit retroactively with no time limit.

- Local Taxes May Apply: Cities like New York City and Philadelphia may have additional tax requirements beyond state-level obligations.

- Tools and Tracking Are Essential: Accurate tracking of employee locations and using compliance tools can help you stay ahead of varying state laws.

To stay compliant, register for payroll accounts in new states as soon as you hire, track where employees work, and understand the specific rules for each state where your employees are located. This proactive approach can prevent costly mistakes and ensure smooth operations for your business.

What is State Tax Nexus?

State tax nexus refers to the connection between a business and a state that creates tax obligations. Essentially, it determines when a state has the authority to require a business to collect and pay taxes. Catherine Shaw, State and Local Tax Partner at Cherry Bekaert, puts it simply:

Nexus simply means there is enough connection between a taxing jurisdiction and the business it seeks to tax to successfully impose its tax.

Once this connection is established, the state can require businesses to register, file tax returns, and pay various taxes, including payroll taxes.

Traditionally, nexus was tied to a physical presence, like having an office, warehouse, or retail store in a state. However, the rules have evolved. For instance, hiring a remote employee now creates an immediate presence in that state, triggering the need to register for state withholding and State Unemployment Insurance (SUI) accounts. After the 2018 South Dakota v. Wayfair ruling, states can also base nexus on economic activity. But when it comes to payroll taxes, there’s no revenue threshold – your obligation begins immediately.

Activities That Trigger Nexus

Certain activities can establish nexus, but not all lead to the same tax responsibilities. Hiring a remote employee is one of the most common ways to trigger payroll tax nexus. In fact, a 1975 Supreme Court decision confirmed that even one remote employee can create nexus.

Other activities that establish nexus include owning or leasing property, such as offices, warehouses, or storage facilities. These typically lead to corporate income or franchise tax obligations. Even using independent contractors or employees for services or sales can create nexus in some states.

Business travel is another factor. While many states apply a "de minimis" threshold before requiring tax withholding for employees traveling on business, this can still lead to nexus in some cases. Additionally, sales tax nexus can be triggered by reaching specific sales thresholds under economic nexus rules, though this generally doesn’t impact payroll taxes.

Nexus Challenges for Multi-State Businesses

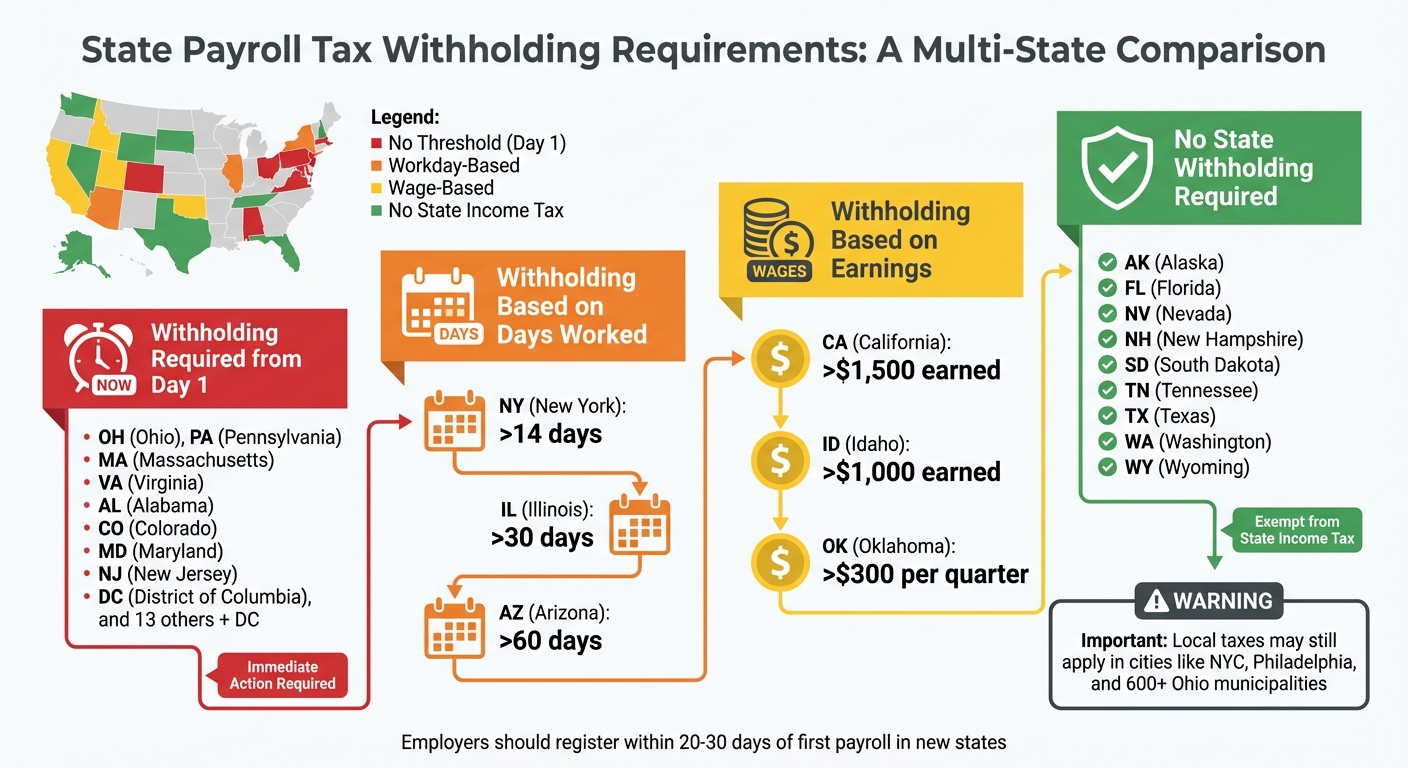

For businesses operating in multiple states, navigating nexus rules can get complicated. Each state has its own definition of nexus, its own thresholds, and its own penalties for noncompliance. For example, 21 states and the District of Columbia require withholding from the very first day an employee works there. States like Alabama, Colorado, Maryland, Massachusetts, New Jersey, and Pennsylvania follow this rule.

Other states have workday thresholds before requiring nonresident withholding, ranging from 14 to 60 days. Some states base their requirements on income earned. For instance, California mandates withholding once an employee earns more than $1,500 in the state, while Idaho’s threshold is $1,000.

On top of state-level obligations, local taxes can also come into play. Cities like New York City, Philadelphia, and various municipalities in Ohio impose additional income or wage taxes beyond state requirements. Understanding these layers of rules is essential for managing payroll tax obligations when employing remote workers across different states.

sbb-itb-ba0a4be

How Remote Employees Create Payroll Tax Nexus

Remote Work and Payroll Nexus

When it comes to payroll taxes, remote employees bring unique challenges. Unlike traditional nexus, which is often tied to physical or economic presence, hiring a remote worker in another state immediately creates a physical presence there. This means payroll tax obligations are determined by where the work is performed, not where the company is headquartered.

Here’s the catch: while sales tax nexus often requires hitting a revenue threshold – like $100,000 – there’s no such minimum for payroll taxes triggered by an employee’s physical presence. From the moment a remote worker starts, employers are responsible for setting up state withholding and State Unemployment Insurance (SUI) accounts. And since registration can take weeks, this isn’t something you can afford to delay.

This immediate responsibility highlights the need for businesses to fully grasp the tax implications of remote work – a topic we’ll dive into further.

Common Misconceptions About Remote Work Nexus

Even with clear guidelines, myths about remote work and nexus continue to circulate. One common misunderstanding is that remote employees only create tax obligations if they’re involved in sales or if the business meets certain revenue thresholds. In reality, just having an employee physically present in a state establishes nexus. As Tim Bjur, JD, a Tax & Accounting Expert, puts it:

Telecommuting from a home office usually creates income tax nexus and a filing requirement for their out-of-state employer.

Another misconception is that hiring contractors instead of employees eliminates nexus concerns. While contractors don’t require payroll tax withholding, they can still create a physical presence for income and sales tax purposes if they’re performing work on behalf of your business.

Some business owners also assume that as long as they don’t have an office or warehouse in a state, they’re off the hook for local tax obligations. However, in nearly all states, even a single employee working remotely from home qualifies as a physical presence. That presence can trigger not only payroll taxes but also corporate income tax requirements. For instance, California mandates a minimum corporate tax of $800 for businesses with nexus in the state.

State Thresholds for Payroll Nexus

Understanding how payroll thresholds differ across states is a key part of navigating the complexities of remote work compliance.

State-by-State Threshold Comparison

Payroll tax rules vary significantly from state to state, creating a maze for businesses managing remote employees. Some states base withholding requirements on the number of days worked. For instance, in New York, withholding kicks in after 14 days, while Illinois and Arizona enforce it after 30 and 60 days, respectively. On the other hand, states like California and Oklahoma use wage thresholds. In California, withholding starts when an employee earns more than $1,500, whereas Oklahoma sets a much lower threshold at just $300 per quarter.

Not all states follow these models. In 21 states and the District of Columbia, there’s no threshold at all – employers must withhold taxes from the very first day an employee works in the state. This applies to states like Ohio, Pennsylvania, Massachusetts, and Virginia. Meanwhile, nine states – Alaska, Florida, Nevada, New Hampshire, South Dakota, Tennessee, Texas, Washington, and Wyoming – don’t have a state income tax, meaning no payroll withholding is required.

| State | Threshold Type | Requirement |

|---|---|---|

| California | Wage-based | Withholding starts after earning >$1,500 |

| Texas | No income tax | No state withholding required |

| New York | Workday-based | Withholding starts after >14 days worked |

| Florida | No income tax | No state withholding required |

| Ohio | No threshold | Withholding starts from day one |

| Illinois | Workday-based | Withholding starts after >30 days worked |

| Pennsylvania | No threshold | Withholding starts from day one |

These varying thresholds emphasize the importance of having payroll systems that can handle such complexities, laying the groundwork for effective compliance.

Compliance Challenges from Varying Thresholds

The diversity in state rules makes payroll management a daunting task. As Tim Bjur, JD, a tax and accounting expert at Wolters Kluwer, explains:

The assortment of state income tax nexus, withholding, and nonresident filing rules can create headaches for both employers and employees. Telecommuting work arrangements add another layer of complexity to understanding those rules.

One of the most challenging aspects? Retroactive withholding. Once an employee meets a threshold – whether based on workdays or wages – states often require employers to retroactively withhold taxes from their first day of work in that state. To avoid this administrative nightmare, some employers opt to start withholding immediately when an employee begins working in a new state, regardless of thresholds.

The situation becomes even trickier when employees work in multiple states or relocate temporarily during the year. Tracking workdays across various jurisdictions and managing different wage thresholds demands advanced payroll systems and constant oversight, making compliance a continuous challenge.

Payroll Tax Withholding Obligations After Establishing Nexus

Once nexus is established, your next step involves tackling payroll tax obligations head-on. This includes registering with the appropriate authorities, setting up your payroll system correctly, and ensuring ongoing compliance with reporting requirements.

Registering for State Payroll Taxes

Before you can start withholding payroll taxes, you’ll need to register your business with the state. This process usually begins with registering your entity with the state’s Secretary of State or Corporations Division. Afterward, employers must complete two additional registrations:

- State income tax withholding account: Typically handled by the Department of Revenue.

- State unemployment insurance (SUI/SUTA) account: Managed by the Department of Labor.

Each registration results in a unique account number and comes with its own reporting requirements. Timing is crucial – most states expect you to register within 20 to 30 days of issuing your first payroll in that state.

Some locations add another layer of complexity with local tax registration. Cities like Philadelphia, New York City, and many municipalities in Ohio (over 600, to be exact) impose their own wage taxes, requiring separate registration and reporting. For states with intricate local tax systems, using geocoding tools to pinpoint the correct tax jurisdiction based on employee addresses can help you avoid costly errors.

On top of that, workers’ compensation insurance is often required when nexus is established through a remote employee. This insurance must be specific to the state where the employee works, adding yet another step to the compliance process.

Penalties for Non-Compliance

Failing to meet registration and tax obligations can lead to severe consequences. Tyler Heard, CPA at Smith + Howard, explains:

If a state tax authority discovers that you have nexus and didn’t pay income taxes, it can assess unpaid state income tax, fees, and penalties for any tax year in your business’s history – even back to day one.

Here’s the kicker: there’s no statute of limitations for state tax audits if you haven’t filed or paid taxes as required. This means states can go back indefinitely to collect unpaid taxes, along with penalties and interest.

For example, New York imposes a 5% penalty per month on unpaid payroll taxes, up to a maximum of 25%. Interest is added to all overdue amounts, quickly escalating the financial damage. Even if you’ve withheld taxes correctly but failed to register on time, states like California and New York are known for aggressively penalizing late registration.

If you realize you’ve been operating with nexus without proper registration, it’s critical to address the issue immediately. Voluntary Disclosure Agreements (VDAs) can offer some relief by waiving penalties and limiting the lookback period to three to five years instead of allowing states to go back indefinitely. However, VDAs are generally off the table once an audit has started, so acting quickly is essential.

Compliance Steps for Remote Employees in Multiple States

Managing payroll compliance for remote employees working across state lines can be tricky, but staying organized and using the right tools can make the process much smoother.

Configuring Payroll Systems for Multiple States

When remote work establishes a nexus in a state, it’s essential to act promptly. Start by registering with the state’s Department of Revenue for income tax withholding and the Department of Labor for unemployment insurance. Most states require this within 20–30 days of running your first payroll.

Set up your payroll system to meet each state’s unique requirements. Use a four-part test – considering work performed, base of operations, location of direction/control, and the employee’s residence – to determine the correct state for unemployment taxes. For states with reciprocity agreements (around 16 states in total), ensure you collect non-residency certificates, like Pennsylvania’s Form REV-419, to avoid double withholding.

Geocoding can be a game-changer for payroll systems, especially when assigning local tax jurisdictions for cities like New York City, Philadelphia, or the hundreds of municipalities in Ohio. Double-check that your records accurately reflect where employees are working to avoid errors.

Monitoring Employee Work Locations

Keeping track of where employees physically work is critical since payroll taxes are based on their actual work location. During onboarding, have employees confirm their primary work address. For those who travel or work across multiple states, track workdays for each pay period to maintain an audit trail. Many human capital management systems allow employees to update their work locations, which helps keep payroll records up to date.

Regularly auditing your payroll system is another key step. This ensures that employee work locations match your records and that state accounts remain active. This is especially important for hybrid workers or employees who relocate, even temporarily, as working in a new state can trigger compliance obligations. Dedicated compliance tools can help streamline these processes and reduce manual effort.

Using Compliance Tools and Services

To simplify multi-state payroll management, consider using compliance tools. Comprehensive payroll and compliance platforms can handle tasks like state registrations, tax calculations, and withholding across different jurisdictions. Tax research tools can also help you stay informed about state-specific rules, reciprocity agreements, and local tax requirements.

For businesses seeking integrated support, platforms like BusinessAnywhere offer registered agent services and state filing assistance through a single dashboard. This can be especially helpful when establishing nexus in multiple states and managing ongoing compliance needs.

If new remote hires create additional tax responsibilities, specialized software that integrates with your existing systems can be a lifesaver. These tools often update automatically as regulations change, ensuring you stay compliant without added stress.

Reciprocity Agreements and Nexus Exceptions

Understanding Reciprocity Agreements

When it comes to remote work and state tax obligations, reciprocity agreements can help simplify things. These agreements allow employees to pay income tax only to their home state, even if they work in another state. Instead of employers withholding taxes for the work state, they withhold for the employee’s home state instead, making payroll easier and avoiding double taxation.

As of July 2022, 17 states (including the District of Columbia) have active reciprocity agreements. Most of these agreements are bilateral, like the one between Maryland and Pennsylvania, which ensures mutual tax exemptions for residents. Some states, such as Indiana, Minnesota, and Wisconsin, use unilateral agreements, automatically granting reciprocity to states that offer similar benefits to their residents.

"State tax reciprocal agreements make it easier for employees to file state income tax returns. For employers, withholding taxes is simpler because they only need to withhold state and local taxes for the employee’s home state." – Vanessa Kahkesh, Content Marketing Manager, Rippling

To take advantage of reciprocity, employees need to file a non-residency certificate with their employer. Each state has its own form for this: Michigan uses MI-W4, Virginia uses VA-4, and Pennsylvania requires REV-419. Without this paperwork, employers must follow the standard rules for multi-state tax withholding.

It’s important to note that while income tax withholding is governed by reciprocity agreements, unemployment insurance is determined by the state where the work is performed. Employers also need to register for withholding accounts in both the work state and the home state to ensure proper compliance.

Here’s a quick look at some reciprocity agreements and the forms required:

| Work State | Reciprocal Resident States | Non-Residency Certificate Form |

|---|---|---|

| Arizona | CA, IN, OR, VA | WEC |

| Illinois | IA, KY, MI, WI | IL-W-5-NR |

| Indiana | KY, MI, OH, PA, WI | WH-47 |

| Maryland | D.C., PA, VA, WV | MW 507 |

| Michigan | IL, IN, KY, MN, OH, WI | MI-W4 |

| New Jersey | PA | NJ-165 |

| Ohio | IN, KY, MI, PA, WV | IT-4 |

| Virginia | D.C., KY, MD, PA, WV | VA-4 |

| Wisconsin | IL, IN, KY, MI | W-220 |

In addition to reciprocity agreements, some states offer temporary work exceptions to further simplify tax withholding.

Temporary Work Exceptions

Temporary work exceptions are another way to ease tax compliance, especially for short-term assignments. For example, Arizona exempts withholding if an employee works in the state for fewer than 60 days. Similarly, Hawaii provides a 60-day exemption, as long as wages are paid from an out-of-state office.

Other states have their own thresholds. Georgia requires withholding only if an employee works in the state for more than 23 days in a calendar quarter, or if their Georgia wages exceed $5,000 or 5% of their total earnings. Idaho sets a straightforward $1,000 annual earnings limit before withholding kicks in.

However, some states, like New York and Pennsylvania, enforce "convenience of the employer" rules. These rules allow states to tax nonresident income if the employee works remotely for their personal convenience rather than a business necessity. For instance, New York requires withholding after 14 days of temporary work, while Illinois allows up to 30 days.

For employers, keeping detailed records of where employees work is essential. Hybrid or mobile employees can easily cross thresholds that trigger unexpected withholding requirements. Accurate tracking not only ensures compliance but also protects your business during audits. As remote work continues to evolve, understanding these exceptions is key to staying on top of payroll obligations.

Conclusion

Hiring even one remote employee in a different state triggers payroll tax registration requirements. This is because a single worker establishes a physical presence nexus, which means your business must register with that state immediately. Beyond payroll taxes, remote employees can also create obligations for corporate income, franchise, and sales taxes.

Your tax responsibilities are tied to where the work is performed, not where your company is based. This makes it essential to track employee work locations, understand state-specific thresholds, and stay informed about reciprocity agreements and temporary work exceptions. States like California and New York are particularly strict in enforcing these rules. Non-compliance can become a major issue, especially during fundraising or acquisition due diligence, and may lead to expensive remediation efforts.

To stay compliant, document employee work locations during onboarding, implement systems to track their locations, and register for state accounts as soon as you extend an offer letter. For businesses managing remote teams across multiple states, tools like BusinessAnywhere can simplify compliance with features such as registered agent services, compliance alerts, and centralized management tools.

As remote work continues to evolve, these principles remain critical. By understanding nexus rules, keeping tabs on employee locations, and leveraging the right compliance tools, you can avoid penalties and focus on growing your business. Make these practices a core part of your compliance strategy to stay prepared as regulations shift.

FAQs

What should I do after hiring a remote employee in a different state?

When you bring on a remote employee in a new state, the first thing to check is whether your business has established a tax nexus there. A tax nexus means your business has a strong enough connection to the state, making it necessary to register and follow payroll tax rules, such as withholding state income tax and paying state unemployment insurance (SUI).

If a nexus exists, you’ll need to register your business with the relevant state tax agencies and adjust your payroll system to correctly withhold state and local taxes based on where the employee works. Don’t forget to check for any reciprocity agreements between states, especially if the employee works in multiple locations – these agreements can simplify tax withholding.

Keeping accurate records of where your employees work and your tax filings is essential for staying compliant. Good documentation helps you manage multi-state payroll requirements and steer clear of penalties.

How do I know if my business has a tax nexus in a specific state?

If you’re trying to figure out whether your business has a tax nexus in a particular state, you’ll need to assess if your activities or presence there meet the state’s criteria for tax obligations. Nexus is often established through a physical presence, like having employees, offices, or property in the state. But don’t overlook remote employees – if they’re working from a state and their work is substantial or ongoing, that can also create a nexus.

Keep in mind, each state defines nexus differently. Factors such as economic presence or remote work arrangements can play a role. To ensure compliance, it’s important to review the tax laws in every state where your business operates or employs remote workers. Some practical steps include tracking where your employees are located, properly documenting remote work agreements, and consulting state-specific tax guidelines. This can help you avoid any unexpected tax liabilities down the road.

What happens if my business doesn’t meet state payroll tax requirements?

Failing to comply with state payroll tax rules can lead to serious legal and financial problems for your business. If you don’t properly withhold and remit payroll taxes in states where you have a tax nexus – which can be established when employees work remotely – you risk facing penalties, interest charges, and back taxes. On top of that, it could result in audits, which are both expensive and time-consuming.

Not registering for payroll taxes in the correct states or misclassifying employees can also bring fines and potential legal trouble. Employers are responsible for handling state income tax withholdings, unemployment insurance, and any state-specific contributions. Ignoring these responsibilities doesn’t just harm your finances – it can also hurt your company’s reputation and create long-term operational headaches. Staying on top of compliance is crucial to avoid these pitfalls and keep your business running smoothly.