Protecting your real estate investments starts with understanding the legal structures that shield your personal assets. LLCs and Series LLCs are two popular tools that create a separation between your business and personal finances, reducing your risk in lawsuits or creditor claims. However, these protections are not absolute – compliance, proper record-keeping, and insurance play a critical role in maintaining your safeguards.

Key Takeaways:

- LLCs: Limit personal liability by separating business and personal assets. They’re ideal for small portfolios and provide tax benefits.

- Series LLCs: Offer liability isolation for multiple properties under one umbrella, reducing costs and simplifying management for larger portfolios.

- Risks: Personal liability can still occur due to negligence, personal guarantees, or failing to maintain proper legal and financial boundaries.

- Compliance: Regular filings, separate bank accounts, and clear documentation are essential to preserve liability protections.

- Insurance: Acts as a financial safety net, covering claims that LLCs cannot.

Bottom Line: Choose the right structure based on your portfolio size and location, maintain compliance, and pair it with strong insurance coverage to safeguard your assets.

How LLCs Protect Real Estate Investments

An LLC acts as a shield between your personal assets and your rental properties. By forming an LLC, you create a legal divide between your business and personal affairs. This means that if a tenant gets injured on your property and decides to sue, they can usually only target the assets owned by the LLC – like the rental property itself – rather than your personal home, car, or savings.

How LLCs Separate Personal and Business Assets

Here’s why this separation is so important for real estate investors.

When you invest through an LLC, your personal liability is generally limited to the amount you’ve put into the business. For example, if you contribute $50,000 to an LLC that owns a rental property, and a lawsuit results in a $200,000 judgment, creditors are typically restricted to the LLC’s assets – such as the property or business funds. Your personal assets, like your home or retirement savings, remain protected.

This protection works in reverse, too. If you’re sued for something unrelated to your real estate business, such as a car accident, creditors usually can’t go after properties held by your LLC. This legal separation ensures your personal liabilities don’t jeopardize your investment portfolio, and vice versa.

On top of liability protection, LLCs also come with tax advantages. They allow for pass-through taxation, which means profits and losses are reported on your personal tax return, avoiding the double taxation that corporations face. Plus, you can claim deductions for expenses like mortgage interest, property taxes, repairs, and depreciation. It’s no wonder that over 60% of real estate investors choose LLCs for their combination of liability protection and tax efficiency.

Steps to Form an LLC for Real Estate

To set up an LLC for your real estate investments, follow these key steps:

- Check Name Availability: Make sure your desired LLC name is available in your state and reserve it with the Secretary of State.

- Designate a Registered Agent: This can be an individual or a service that will receive legal documents and official notices on behalf of your business.

- File Articles of Organization: Submit this document with your state to officially establish the LLC as a legal entity.

- Obtain an EIN: Get a free Employer Identification Number (EIN) from the IRS. This number functions like a business Social Security Number, enabling you to open business bank accounts and file taxes separately.

- Open a Business Bank Account: Keeping personal and business funds separate is critical. Mixing them can lead to courts “piercing the corporate veil,” which could make you personally liable for business debts.

- Draft an Operating Agreement: This document outlines the rules for managing the LLC, including ownership and decision-making processes. It’s especially important for single-member LLCs to show the business operates independently of personal finances.

- Transfer Property Into the LLC: If you’re moving an existing property into the LLC, you’ll need to record a deed (such as a warranty or quitclaim deed). Check with your mortgage lender first, as transferring property with a mortgage might trigger a due-on-sale clause, requiring immediate loan repayment.

Maintaining LLC Compliance Requirements

Setting up an LLC is just the first step. Ongoing compliance is essential to maintain your liability protection. As Jonathan Kessler, Head of Credit and Cash Management Solutions at PNC Private Bank, emphasizes:

"Creating an LLC and then walking away is not a substitute for good planning or recordkeeping".

To keep your LLC in good standing:

- File Annual Reports: Submit these on time to update ownership or business details and avoid penalties or dissolution.

- Keep Financial Records: Use the LLC’s bank account and credit cards exclusively for business transactions.

- Sign Properly: Sign contracts as an agent of the LLC (e.g., "John Doe, Member of XYZ LLC") to avoid personal liability.

- Hold Annual Meetings: Even for single-member LLCs, holding meetings and recording minutes shows that your LLC operates as a legitimate business.

Additionally, LLC owners must report Beneficial Ownership Interest under the Corporate Transparency Act.

Finally, while an LLC offers long-term asset protection, it doesn’t replace the need for insurance. General liability insurance, typically ranging from $500,000 to $2 million, along with property and umbrella policies, adds an extra layer of immediate financial security. Together, an LLC and insurance create a strong safety net for your real estate investments.

Up next, we’ll dive into how Series LLCs can provide even more specialized protection for your assets.

Series LLCs Explained

A Series LLC is a unique type of legal entity that combines a single master LLC with multiple independent series under its umbrella. Each series operates as its own entity, with separate assets and specific business purposes. This setup can slash entity-related costs by as much as 60–80% compared to forming and maintaining multiple traditional LLCs. The standout feature? Liability isolation. For example, if a tenant files a lawsuit over an injury at a property held in Series A, creditors can typically only go after Series A’s assets, leaving the other series untouched. This streamlined and cost-efficient structure makes Series LLCs an attractive option for many business owners.

How Series LLCs Are Structured

The Series LLC operates on a parent-child model. The master LLC acts as the legal foundation, while each series functions independently, maintaining its own assets, bank accounts, and records. All of this is managed under a single state filing and one operating agreement.

This structure dramatically reduces costs. For instance, real estate investors managing three or more properties can cut their entity expenses by up to 80% compared to forming separate LLCs. States like Oklahoma charge a flat $100 fee for the master LLC, regardless of how many series are created, while Delaware imposes an annual fee of about $300, making it an appealing choice for businesses.

To preserve the liability protection between series, it’s crucial to maintain strict separation. Each series must have its own bank accounts, accounting records, and contracts. Legal documents should clearly specify the series involved, such as "ABC Holdings, LLC – Series 123 Main St", to ensure clarity and proper identification of assets.

When to Use a Series LLC for Real Estate

For real estate investors managing multiple properties, a Series LLC can be a practical and efficient solution. If you own three or more properties in states that recognize this structure, the benefits can far outweigh the costs. You can consolidate management under one master LLC while still protecting each property from liabilities tied to others.

This setup also allows for operational flexibility. Each series can have its own managers or ownership structures, making it a great fit for partnerships where investors want to keep properties separate without forming entirely new companies. As your portfolio grows, adding a new series is straightforward – just amend the operating agreement. There’s no need to file new articles of organization with the state.

That said, Series LLCs aren’t suitable for every situation. If you own properties in states that don’t recognize this structure, you may lose the liability protections it offers. Additionally, some traditional banks may hesitate to finance properties held within a Series LLC, so it’s wise to consult with lenders early in the process.

States Where You Can Form a Series LLC

By 2025, around 20 U.S. jurisdictions will have adopted laws specifically allowing Series LLCs. These include Alabama, Arkansas, Delaware, the District of Columbia, Illinois, Indiana, Iowa, Kansas, Missouri, Montana, Nevada, North Dakota, Ohio, Oklahoma, Puerto Rico, South Dakota, Tennessee, Texas, Utah, Virginia, Wisconsin, and Wyoming.

Delaware is particularly popular for Series LLCs because of its established legal framework and business-friendly policies. It also offers a "Registered Series" option, where each series may require a separate state filing, typically costing around $75 annually. This added registration can provide more legal certainty for lenders.

In Texas, you can choose between "Protected Series", which are created internally without additional state filings, or "Registered Series", depending on your financial and operational needs. Wyoming stands out for its affordability and privacy protections, with an annual report fee of just $60. Meanwhile, Oklahoma uses a Protected Series model, with no extra fees for individual series beyond the $100 master LLC formation fee.

California, on the other hand, does not permit the formation of domestic Series LLCs. However, it does recognize foreign Series LLCs. In such cases, each series must register separately and pay its own annual LLC taxes and fees.

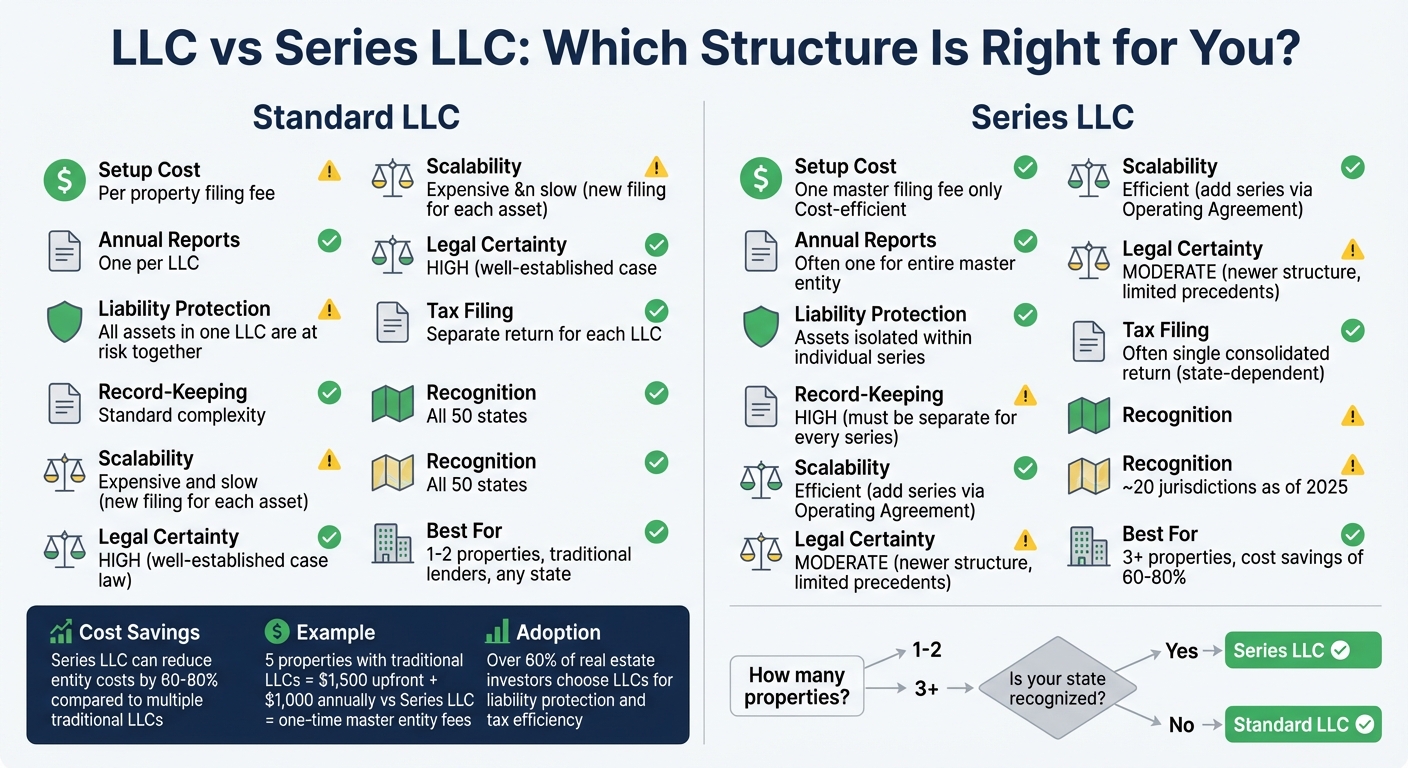

LLC vs Series LLC: Which Structure Is Right for You?

After exploring the benefits of LLCs and Series LLCs, it’s time to dive into their differences to help you decide which structure aligns best with your investment strategy. The choice between a standard LLC and a Series LLC often hinges on factors like the size of your portfolio, the location of your properties, and how much administrative complexity you’re prepared to handle. Each option comes with its own structure, costs, and trade-offs.

Side-by-Side Comparison: LLC vs Series LLC

One of the biggest distinctions lies in cost and scalability. For instance, imagine you own five properties and decide to form a separate LLC for each. In a state with a $300 formation fee and a $200 annual fee, you’d pay $1,500 upfront and $1,000 annually. With a Series LLC, you’d only pay those fees once for the master entity.

| Feature | Standard LLC | Series LLC |

|---|---|---|

| Setup Cost | Charges per property | Typically one master filing fee |

| Annual Reports | One per LLC | Often one for the entire master entity |

| Liability Protection | All assets in one LLC are at risk together | Assets are isolated within individual series |

| Record-Keeping | Standard | High (must be separate for every series) |

| Scalability | Expensive and slow (new filing for each asset) | Efficient (add series via Operating Agreement) |

| Legal Certainty | High (well-established case law) | Moderate (newer structure, limited court precedents) |

| Tax Filing | Separate return for each LLC | Often a single consolidated return (state-dependent) |

Standard LLCs are recognized in all 50 states and backed by extensive legal precedents. Series LLCs, however, are only authorized in about 20 jurisdictions as of 2025. If your properties are in states that don’t recognize Series LLCs, the liability protections they offer might not hold up in court.

This comparison highlights the strategic differences between the two structures, which we’ll break down further.

Advantages and Disadvantages of Each Structure

Standard LLCs are simple and universally accepted. They’re ideal for investors with one or two properties, especially if you’re working with traditional lenders or operating in states without Series LLC statutes. However, as your portfolio grows, so do the costs. Each property requires its own formation fee, annual report, and registered agent, leading to repetitive administrative work.

Series LLCs, on the other hand, are a better fit for investors with three or more properties in states that recognize this structure. They can reduce entity-related costs by 60% to 80% compared to forming multiple traditional LLCs. Adding a new property is straightforward – just amend the operating agreement, skipping the need for new state filings. Plus, each series can select its own tax classification, offering flexibility for diverse investment strategies.

"The savings in administrative overhead alone can justify the Series LLC structure for businesses with three or more separate ventures." – Cantrell Law Firm

That said, Series LLCs require strict record-keeping. Commingling funds between series can void liability protections. Additionally, some traditional lenders may hesitate to finance properties held in a Series LLC, so it’s wise to check with your bank before committing to this structure.

If your properties span multiple states, confirm whether each state recognizes Series LLCs. For properties in states that don’t, you’ll need to form a traditional LLC for those assets. In jurisdictions that support Series LLCs, and if you can maintain strict financial separation, the structure is more efficient. Otherwise, a standard LLC offers simplicity and broader compatibility with lenders.

Choosing between these two structures is a key step in shaping your asset protection strategy.

sbb-itb-ba0a4be

When You’re Still Personally Liable Despite Having an LLC

Even with proper LLC compliance, there are situations where you could still find yourself personally liable. While an LLC generally protects personal assets, certain actions or oversights can strip away this shield. For real estate investors, understanding these pitfalls is crucial to avoid jeopardizing your home, savings, or other personal assets.

Piercing the Corporate Veil: What It Means

If a court decides that your LLC is merely an extension of yourself rather than a separate legal entity, it can "pierce the corporate veil." This means creditors can go after your personal assets, bypassing the LLC’s protections.

"If the owners fail to maintain a formal legal separation between their business and their personal financial affairs, a court could find that the corporation or LLC is really just a sham (the owners’ alter ego)." – Amanda Hayes, Attorney

Courts typically use a two-part test: first, they check if there’s a clear separation between personal and business finances. Then, they look for signs of fraud or reckless behavior. For example, using the LLC’s bank account to pay personal expenses – like credit card bills or streaming subscriptions – can trigger this scrutiny. Another red flag is undercapitalization, where the LLC lacks enough funds to cover foreseeable expenses. Single-member LLCs often face closer examination, and administrative missteps like missing annual reports, failing to maintain a registered agent, or skipping meeting minutes can weaken your protection even further. Recognizing these triggers is the first step in safeguarding your assets.

Situations Where LLC Protection Doesn’t Apply

Even without piercing the corporate veil, there are scenarios where LLC protection won’t shield you. Personal guarantees are a common example. If you personally guarantee a loan or mortgage for your LLC, you’re on the hook if the business defaults.

"By signing a personal guarantee, you’re volunteering your personal assets as security for the debt if the business can’t repay the loan." – Amy Loftsgordon, Attorney

Additionally, actions like negligence, fraud, or reckless behavior fall outside the LLC’s protective scope. Failing to pay payroll taxes is another serious issue – the IRS can hold you personally responsible. Even something as simple as signing contracts in your own name instead of explicitly stating your role within the LLC (e.g., "John Smith, Member of ABC Properties LLC") can expose you to personal liability.

How to Strengthen Your Liability Protection

To keep your LLC’s protections intact, always use dedicated business accounts and sign documents with your name and title – such as "Your Name, Title – [LLC Name]." Establishing a detailed Operating Agreement, holding annual meetings, and documenting key decisions with written resolutions or meeting minutes are also essential steps. Make sure your business cards, invoices, and correspondence clearly identify your LLC to reinforce its separate legal status.

Insurance is another critical safeguard. General liability insurance typically covers $500,000 to $2,000,000, depending on your level of risk. You can also add an umbrella policy for extra protection. To minimize exposure, distribute excess profits instead of letting them accumulate in the LLC. When seeking loans, consider non-recourse financing, which doesn’t require personal guarantees – though these options may be harder to find for smaller investors.

Compliance and Risk Management for Real Estate LLCs

Starting an LLC is just the beginning; staying compliant with state regulations, maintaining proper insurance, and keeping accurate records are what truly safeguard your assets. Ignoring these responsibilities can put your asset protection at risk and lead to hefty fines. In fact, the cost of non-compliance is, on average, 2.7 times higher than maintaining a proper compliance program. Below, we’ll dive into the essential filings and tasks that help preserve your LLC’s legal and protective status.

Annual Filing and Compliance Tasks

To keep your LLC in "good standing", every state requires annual or biennial filings. Missing these deadlines can result in administrative dissolution, which strips your LLC of its legal protections and your ability to operate. Filing fees vary by state, typically ranging from $75 to $500.

For Series LLCs, maintaining separate bank accounts and records for each series is a must to ensure liability remains isolated.

To make compliance easier, Business Anywhere offers automated reminders and filing services. These tools help you stay on top of annual reports, policy updates, and state-specific requirements. This proactive approach forms the backbone of effective risk management, especially when paired with proper insurance and management tools.

Why Insurance Matters Beyond LLC Protection

While compliance ensures your LLC remains legally protected, insurance covers the financial fallout of potential claims. An LLC shields your personal assets by limiting liability to the business, but insurance is what handles the actual costs of claims. Securing sufficient liability coverage and considering an umbrella policy can provide an extra layer of protection.

When transferring property into your LLC, updating your insurance policies is critical. You’ll likely need endorsements for both title insurance and property/casualty insurance that name the LLC as an "additional insured". Without these updates, standard policies may not cover claims after ownership changes. Additionally, regular property maintenance and routine inspections can help reduce the risk of injury claims – one of the most common sources of landlord litigation.

Tools That Simplify LLC Management

Managing compliance for multiple properties can quickly become overwhelming. Business Anywhere simplifies this with an all-in-one dashboard. Their services include registered agent support (free for the first year, then $147 annually) and virtual mailbox services starting at $20 per month, offering unlimited mail scanning and global forwarding. You can explore more about their registered agent service here and virtual mailbox options here.

The platform also organizes critical documents like property transactions, lease agreements, and maintenance records. For Series LLCs, it tracks separate bank accounts, financial statements, and compliance tasks for each series. Keeping meticulous records is essential – if records aren’t properly maintained, courts may treat multiple series as a single entity, which could compromise liability protections.

Building Your Asset Protection Strategy

Protecting your assets isn’t a one-and-done deal – it’s an ongoing process that combines smart legal planning, strict financial boundaries, and the right insurance coverage. Whether you’re using a traditional LLC or a Series LLC, keeping your personal and business assets separate is non-negotiable.

Here’s how to build a strong strategy to safeguard your investments.

Main Takeaways

Choose the right LLC structure for your portfolio, and keep personal and business finances separate.

If you own one or two properties, a traditional LLC is straightforward and backed by well-established legal precedent. For larger portfolios – three or more properties – a Series LLC can save you money in the long run. To ensure proper separation, open individual bank accounts for each property or series, secure separate EINs, and make sure all contracts, leases, and deeds are signed under the LLC’s name – not your own. Courts may disregard your LLC’s protections if it’s treated as an extension of your personal finances.

Insurance is your second line of defense.

While an LLC protects your personal assets from business liabilities, insurance is what covers the actual costs of claims. Update your property and title insurance to include the LLC as an additional insured, and consider adding high-limit umbrella policies for extra coverage. Don’t overlook your personal insurance either – adequate car insurance, for example, can help protect your real estate assets if an accident leads to a lawsuit.

Take these practical steps to refine your asset protection strategy.

Action Steps for Real Estate Investors

- Audit your current setup: Are your properties titled under the correct entity? Are your insurance policies up to date? Have you filed all required annual reports on time? If there’s any confusion or overlap between personal and business assets, address it immediately.

- Simplify compliance with tools like Business Anywhere: They offer $0 business formation (state fees apply), free registered agent services for the first year, and automated compliance reminders – all through a single dashboard. Their virtual mailbox service, starting at $20 per month, provides unlimited mail scanning and a professional U.S. address to help maintain your privacy. Check out their business registration services and registered agent support to streamline your processes today.

FAQs

What’s the difference between an LLC and a Series LLC in real estate asset protection?

An LLC (Limited Liability Company) is a single legal entity designed to shield its members from personal liability. However, all the assets owned by the LLC are pooled together. This means if the LLC is sued or owes a debt, any of its assets could be used to settle those claims. There’s no internal division of liability within the company itself.

A Series LLC works a bit differently. It’s like a “parent” LLC that can create multiple “series” under its umbrella. Each series functions independently, with its own assets, liabilities, and members. This setup ensures that the liabilities of one series don’t spill over to affect another. While this structure can help cut costs compared to forming multiple LLCs, it’s worth noting that Series LLCs are only permitted in certain states. Additionally, the legal clarity around their protections continues to evolve in some areas.

What steps should I take to ensure my LLC protects me from personal liability?

To keep your LLC’s liability protection intact, it’s essential to treat it as a distinct legal entity. Start by maintaining separate bank accounts for the business and steer clear of mixing personal and business funds. Also, ensure your LLC has enough funds to meet its financial responsibilities.

Keep a record of major business decisions – whether through meeting minutes or written resolutions – and make sure to file any state-required reports on time. Having a written operating agreement in place and securing the right insurance policies can further reinforce your liability protection. Whenever possible, avoid signing personal guarantees for business debts, as this could put your personal assets at risk.

Can I still be personally liable even if I have an LLC?

Yes, forming an LLC offers some protection, but it doesn’t shield you from personal liability in every situation. You could still be held personally responsible under circumstances like these:

- Personally guaranteeing a loan or mortgage associated with your LLC.

- Participating in fraudulent or illegal activities.

- Mixing personal and business finances, such as combining assets or ignoring necessary formalities.

- If a court decides to pierce the corporate veil, making you personally liable for the LLC’s debts or obligations.

To reduce your risk, focus on keeping detailed records, maintaining clear financial boundaries, and adhering to all legal and compliance obligations for your LLC.