Even if you’re the sole owner of your real estate LLC, having an operating agreement is essential. Here’s why:

- Proof of Ownership: Your operating agreement confirms you own the LLC, which is often required by banks or lenders.

- Liability Protection: It helps maintain the separation between personal and business assets, shielding you from personal liability.

- Avoiding Default Rules: Without an agreement, state laws dictate how your LLC operates, which may not align with your goals.

- Financial Clarity: Outlines how profits, losses, and taxes are handled, preventing issues like phantom income surprises.

- Succession Planning: Ensures smooth management of your LLC if you’re incapacitated or pass away.

Skipping this document can lead to legal, financial, and operational risks. Even though it’s not always legally required, drafting one is a smart move for protecting your business and personal assets.

Why Real Estate LLCs Need Operating Agreements

Real estate LLCs often encounter challenges like tenant disputes or property damage claims, making an operating agreement a crucial tool. Let’s break down how this document can benefit real estate LLCs.

Protecting Your Personal Assets from Property Liabilities

In real estate, having proper documentation isn’t just helpful – it’s essential. An operating agreement acts as a shield, reinforcing the separation between your personal assets and the liabilities of your LLC. This separation, often referred to as the "corporate veil", is vital in situations like tenant lawsuits or contractor liens. The agreement typically includes a Statement of Limited Liability, which clearly states that you, as an individual, are not personally responsible for the LLC’s debts or obligations. As Thomson Reuters puts it:

"An operating agreement is invaluable in laying out how the LLC is arranged, how it will be run, and how it goes about its work. Essentially, an operating agreement is a contract; once signed, the LLC members are bound by its terms".

For single-member LLCs, this document is particularly important. It serves as proof that your business operates separately from your personal affairs, ensuring you’re not mistakenly treated as a sole proprietor. This distinction strengthens your limited liability protection.

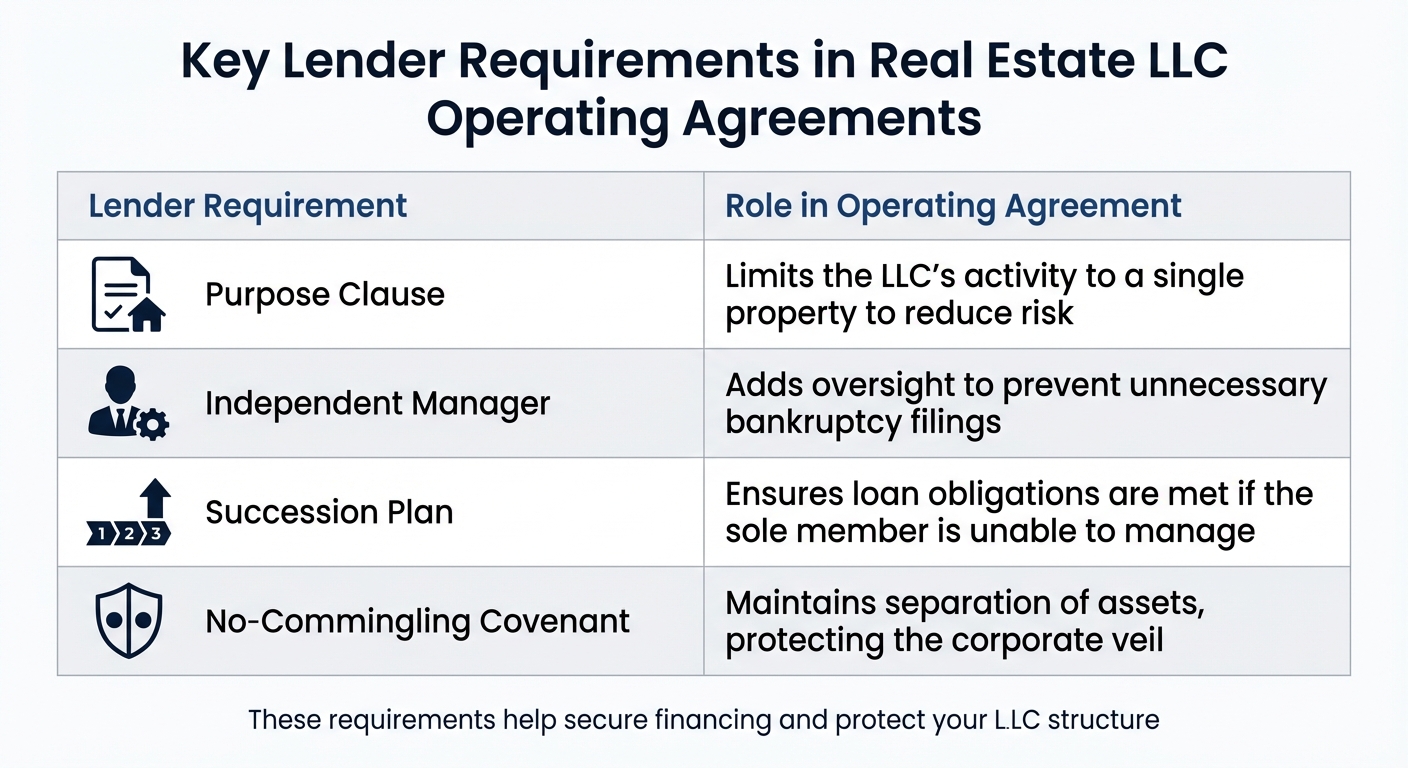

Meeting Bank and Lender Requirements

Financial institutions usually won’t open a business bank account or approve a real estate loan without a signed operating agreement. For real estate LLCs, lenders often require the entity to be a Single Purpose Entity (SPE). This means your LLC is restricted to owning and managing only the property being financed, which minimizes risk for the lender. Including a purpose clause in the operating agreement ensures compliance with this requirement.

Here’s a quick look at some common lender requirements and their roles in an operating agreement:

| Lender Requirement | Role in Real Estate LLC Operating Agreement |

|---|---|

| Purpose Clause | Limits the LLC’s activity to a single property to reduce risk. |

| Independent Manager | Adds oversight to prevent unnecessary bankruptcy filings. |

| Succession Plan | Ensures loan obligations are met if the sole member is unable to manage. |

| No-Commingling Covenant | Maintains separation of assets, protecting the corporate veil. |

The agreement also specifies who has the authority to sign financial documents on behalf of the LLC, simplifying interactions with banks and lenders. Beyond securing financing, an operating agreement can help with tax planning and regulatory compliance.

Supporting Tax Elections and Compliance

By default, single-member LLCs are treated as "disregarded entities" for tax purposes. However, an operating agreement allows you to formalize a different tax election, such as opting for S-Corp status, which can provide certain tax benefits. As Nevada Corporate Headquarters explains:

"An operating agreement can specify whether your LLC is taxed as a sole proprietorship, S corporation, or C corporation. This allows for flexibility in tax planning".

The agreement also clarifies key financial details, such as how profits and losses are distributed, the accounting method used, and the LLC’s tax year. This level of organization not only aids in tax planning but also provides a clear framework in case of an IRS audit. By keeping your business finances distinct and well-documented, you reduce the risk of the IRS classifying business income as personal income – an outcome no one wants.

sbb-itb-ba0a4be

What to Include in Your Real Estate LLC Operating Agreement

Your operating agreement should address the specific needs of a real estate LLC, covering everything from managing properties to handling major financial decisions. Here’s a breakdown of the key elements to include.

Property Management Procedures

Define who makes decisions and at what level of authority. Start by clarifying whether your LLC will be member-managed (you handle operations directly) or manager-managed (you designate someone else to oversee things). Even if you’re the sole member, specifying this distinction is important for legal clarity.

Separate routine tasks – like minor repairs or drafting standard leases – from significant decisions, such as refinancing, selling, or undertaking major renovations. Clearly outline what qualifies as a "major decision" in your agreement. This structure not only ensures smooth operations but also demonstrates that your LLC is a legitimate business entity.

Peterson Law, LLP underscores the importance of this:

"An operating agreement is not just a formality. It’s the rulebook that governs how the real estate LLC operates, how decisions are made, how profits are distributed, and what happens when things go wrong."

Include provisions for removing managers, indemnifying them for good-faith mistakes, and requiring regular reports (e.g., quarterly updates or annual tax filings). These measures establish clear authority and accountability, helping separate personal and business matters.

Investment and Income Distribution Rules

Financial guidelines are just as important as operational ones. Start by documenting your initial contributions – whether cash, property, or services – to establish your investment basis. Then, specify how and when profits will be distributed.

A common oversight for single-member LLCs is ignoring phantom income. Depreciation can create taxable income on paper even if profits are reinvested. To address this, include a clause requiring minimum distributions to cover tax liabilities. Peterson Law, LLP highlights this issue:

"If the operating agreement doesn’t address minimum distributions to cover tax liabilities – or the timing and amount of payouts – members may find themselves in financial distress."

Additionally, set aside reserves for maintenance, vacancies, or future improvements. Outline procedures for capital calls if additional funding becomes necessary.

Procedures for Closing or Transferring Property

To avoid complications, clearly define how property sales, transfers, or LLC dissolution will be handled. This is especially crucial in cases of sale, incapacity, or death. According to FindLaw:

"If you want the LLC to end after your death, you add a termination or dissolution clause. If you do not have such a clause, state law might dictate that the LLC go to your heirs."

Specify a successor manager and detail steps for selling or transferring property, including 1031 exchanges. Also, outline the liquidation order: debts first, followed by assets, and finally distributions. Having these procedures documented simplifies dealings with lenders and title companies when it’s time to sell or refinance.

Risks of Operating Without an Agreement

When you operate an LLC without an operating agreement, you’re essentially leaving the fate of your business to state default rules – and those rules often don’t align with the needs of real estate investors. Here’s what’s at stake.

State Default Rules May Not Match Your Needs

State default rules are designed to be broad, generic guidelines, typically catering to multi-member LLCs. This approach can create serious complications for real estate investors. Without a tailored agreement, state laws could dictate what happens to your property if you pass away or become incapacitated – and the outcome might be far from what you intended.

Howard Ross, an attorney at Battaglia, Ross, Dicus & McQuaid, P.A., highlights the issue:

"If your single-member LLC doesn’t have an [operating agreement], Florida’s default state laws will apply… While these rules are often OK, they can provide unwanted results."

For instance, default laws might transfer your rental properties to a relative who has no interest – or experience – in managing them. Worse, they might enforce formalities like mandatory meetings that make little sense for a single-owner LLC. Peterson Law, LLP also warns:

"Without an operating agreement, California’s default LLC rules will control. These rules may not reflect the intent of the investors and often fail to account for the nuanced realities of real estate ownership."

Another potential pitfall is phantom income from depreciation. State rules won’t require your LLC to distribute cash to cover the taxes on this income, leaving you with a tax bill and no clear way to pay it.

Reduced Asset Protection

One of the main reasons for forming an LLC is to shield your personal assets from lawsuits or debts tied to your property. But without an operating agreement, that protection becomes much weaker. Courts or creditors could argue that your LLC is just an "alter ego" of yourself – a legal way of saying it’s not a separate business entity but more like a sole proprietorship. This opens the door to personal liability through a process called "piercing the corporate veil."

Andy Kaiser, an attorney at Kaiser Law Firm, explains the stakes:

"If a court doesn’t see your LLC as an entity separate from you, you could lose the liability protection that an LLC offers."

An operating agreement is a critical piece of evidence showing your LLC is a legitimate business. Without it, your LLC risks looking like a personal hobby, especially if there’s any overlap between your personal and business finances. Even if you’ve kept separate bank accounts, the lack of documented procedures makes it harder to defend your case if creditors or courts challenge your LLC’s legitimacy.

Unclear Procedures and Potential Conflicts

Beyond liability concerns, not having an operating agreement can create operational headaches. Without documented procedures, even routine decisions can become unnecessarily complicated. Who has the authority to sign a lease or approve a major repair if you’re temporarily unavailable? What if you need emergency funds for a sudden expense, like a roof replacement?

This lack of clarity can make it difficult to work with banks, title companies, or insurance providers. They may hesitate to engage with your LLC if they can’t confirm who has the legal authority to act on its behalf. These delays and inefficiencies can cost you time and money. Worse, you might unknowingly make decisions that jeopardize your LLC’s tax status or liability protections.

Thomson Reuters underscores the importance of having clear rules in place:

"An operating agreement is invaluable in laying out how the LLC is arranged, how it will be run, and how it goes about its work. Essentially, an operating agreement is a contract; once signed, the LLC members are bound by its terms."

Even as the sole member of your LLC, documented procedures add credibility and ensure smooth operations. They also prevent unnecessary delays when you refinance, sell, or transfer property.

These risks highlight why having an operating agreement isn’t just a formality – it’s a necessity. Next, we’ll cover how to create one that works for your specific needs.

How to Create an Operating Agreement for Your Real Estate LLC

Crafting an operating agreement is a crucial step when setting up your real estate LLC. It outlines the rules, roles, and responsibilities within your business, ensuring clarity and legal protection.

Templates vs. Custom Agreements

When creating your operating agreement, you can choose between using a template, hiring an attorney to draft it, or combining both approaches. The right choice depends on your needs and budget.

Many online legal services offer templates at varying price points. These often include guided questionnaires to help you address key provisions. For a single-member real estate LLC with straightforward operations, a template can be an affordable and efficient option.

That said, templates come with limitations. As one legal expert explains:

"While [writing it yourself] is the most inexpensive way to go, you risk omitting important points if you don’t know what to include."

If your LLC involves multiple properties, complex profit-sharing arrangements, or unique succession plans, a custom agreement drafted by an attorney ensures all contingencies are addressed. A hybrid approach is often recommended: start with a professional template to create a draft, then have an attorney review it for compliance and legal soundness. This is particularly important in states like California, Delaware, Maine, Missouri, and New York, where operating agreements are legally required.

Steps to Draft Your Agreement

Whether you use a template or work with an attorney, drafting your operating agreement involves the following steps:

- Basic Information: Include your LLC’s name, principal business location, and your registered agent’s name and address. Define your business purpose, such as real estate investment or property management. Adding a "lawful purpose" clause allows flexibility for future ventures.

- Capital Contributions: Record any initial contributions – cash, property, or services – and your ownership percentage. For single-member LLCs, this formalizes your 100% ownership, reinforcing the separation between personal and business matters.

- Management Structure: Decide how your LLC will be managed. Choosing between a member-managed vs. manager-managed structure is a key decision; while member-management is common for single-member LLCs, a manager-managed structure may be more suitable for passive investors.

- Distribution Rules: Establish how and when profits will be distributed, whether monthly, quarterly, or at your discretion. Don’t forget to name a successor manager to ensure a smooth transition if needed.

- Dissolution Procedures: Outline how assets will be liquidated and creditors paid if the LLC is closed. Include a severability clause to ensure the rest of the agreement remains valid even if one part is invalidated.

Once finalized, store your signed operating agreement at your LLC’s principal office. While you don’t need to file it with the Secretary of State, banks and lenders often require it when opening accounts or applying for financing.

Getting Help from Business Formation Services

Feeling overwhelmed by the process? Business formation services can simplify the task. Platforms like BusinessAnywhere offer LLC formation services starting at $0 (plus state filing fees) and provide add-ons like operating agreements, EIN applications, obtaining an EIN for tax purposes, and registered agent services.

These platforms guide you through each step with clear explanations, making the process accessible even for remote business owners or digital nomads managing real estate investments from afar. While these services are convenient, complex arrangements – such as multiple members or properties in different states – may still require an attorney’s review. As Brette Sember, J.D., advises:

"If you have specific needs or complex terms, it’s wise to review the draft with a qualified attorney to ensure it’s legally sound and truly customized to your business needs."

Ultimately, whether you rely on a template, a hybrid approach, or full legal assistance, having a written operating agreement is far better than operating without one. It’s a foundational document that protects your business and sets you up for success.

Conclusion

The protections and advantages of having an operating agreement are hard to overstate. Even if you’re the only member of your LLC, this document is crucial. Without it, courts could potentially pierce the corporate veil, leaving you personally responsible for business debts and legal claims.

A signed operating agreement doesn’t just safeguard your limited liability – it also serves as solid proof of ownership, which banks and lenders often require for financing. Additionally, it lays out important details like profit distribution, management responsibilities, and succession plans, ensuring your business isn’t subject to default state rules.

Creating an operating agreement can be a straightforward process. You can use a template, work with one of the best LLC formation services, or consult an attorney. As Chris Daming, J.D., LL.M., from Legal GPS puts it:

"An operating agreement is a key business document that shows your business operates like a legit company."

This document is a cornerstone for your real estate LLC, providing both operational clarity and long-term legal protection.

FAQs

Why does a single-member real estate LLC need an operating agreement?

An operating agreement is a key document for a single-member real estate LLC. It strengthens the LLC’s liability protection, helping to keep your personal assets separate from business liabilities. Beyond that, it lays out clear rules for how your business will be managed and financed, reducing the chances of misunderstandings or conflicts down the road.

This document can also enhance your credibility with banks, lenders, and potential partners. It shows you’re serious about your business, which can make securing financing or forming partnerships much easier. Even if your state doesn’t legally require it, having an operating agreement is a smart move to protect your interests and keep your business running smoothly.

Why does a single-member real estate LLC need an operating agreement to protect personal assets?

An operating agreement is a must-have for a single-member real estate LLC because it reinforces the LLC’s status as a separate legal entity. This distinction is what safeguards your personal assets from being tangled up in business debts or lawsuits.

By formally outlining the structure and operations of your LLC, the operating agreement serves as solid proof that your business is independent from you as an individual. Without this document, creditors or courts might challenge that separation, which could put your personal assets in jeopardy. Keeping this boundary intact not only protects your personal finances but also ensures your LLC runs smoothly and with legal clarity.

What risks could I face if my single-member real estate LLC doesn’t have an operating agreement?

Without an operating agreement, your single-member real estate LLC could face unnecessary risks. Without this document, your LLC will automatically follow state laws, which might impose rules on management, profit distribution, or dissolution that don’t match your preferences. Even more concerning, it may be harder to demonstrate that your LLC is a separate legal entity, which could weaken the liability protection designed to keep your personal assets safe from business debts or lawsuits. If a court finds there’s no clear distinction between you and your LLC, you might end up personally responsible for its obligations.

On a practical level, the absence of an operating agreement can also cause headaches. Banks, investors, and potential business partners often require this document to open accounts, secure financing, or formalize agreements. Without it, you could face delays or added scrutiny. An operating agreement also provides a clear framework for handling changes, such as hiring managers, selling property, or dealing with unexpected challenges. This can help you sidestep disputes and avoid legal troubles in the future. Skipping this step leaves your LLC exposed to financial, legal, and operational risks that could easily be avoided.