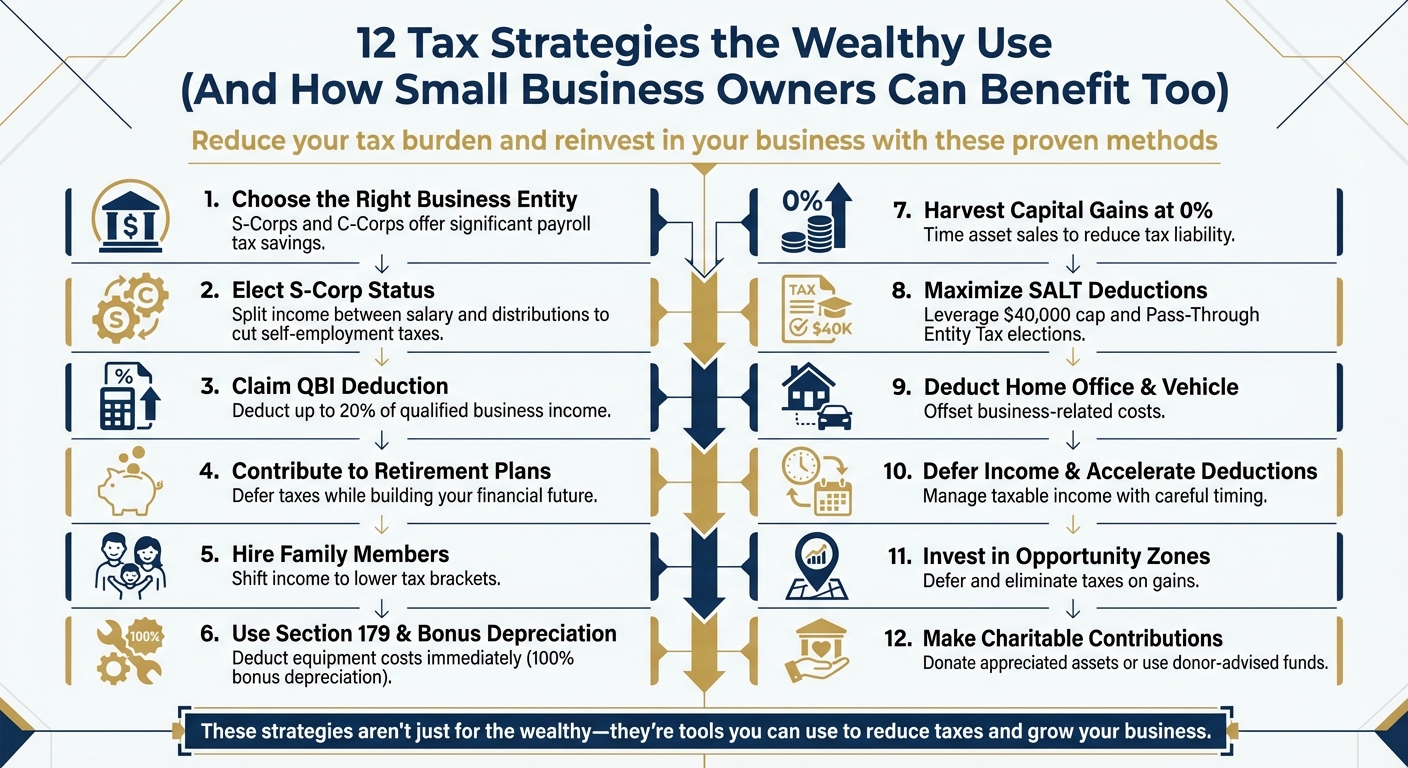

Wealthy individuals save big on taxes by using strategies that are also available to small business owners. From choosing the right business structure to leveraging deductions, these methods can help you optimize your tax savings and reinvest in your business. Here’s a quick rundown of the strategies covered:

- Select the right business entity: S-Corps and C-Corps offer significant savings on payroll taxes and income.

- Elect S-Corp status: Split income between salary and distributions to cut self-employment taxes.

- Claim the QBI deduction: Deduct up to 20% of qualified business income.

- Contribute to retirement plans: Defer taxes while building your financial future.

- Hire family members: Shift income to lower tax brackets.

- Use Section 179 and bonus depreciation: Deduct equipment costs immediately.

- Harvest capital gains at 0%: Time asset sales to reduce tax liability.

- Maximize SALT deductions: Leverage higher limits and Pass-Through Entity Tax elections.

- Deduct home office and vehicle expenses: Offset business-related costs.

- Defer income and accelerate deductions: Manage taxable income with careful timing.

- Invest in Opportunity Zones: Defer and eliminate taxes on gains.

- Make charitable contributions: Donate appreciated assets or use donor-advised funds for maximum tax impact.

These strategies aren’t just for the wealthy – they’re tools you can use to reduce taxes and grow your business. Let’s explore each one in detail.

12 Tax Strategies Wealthy Individuals and Small Business Owners Use to Save on Taxes

1. Choose the Right Business Entity for Tax Savings

The structure of your business plays a huge role in determining your tax obligations and potential savings.

Tax Savings Potential

If you’re a sole proprietor or operating an LLC with default tax treatment, you face a 15.3% self-employment tax on all net earnings. This breaks down to 12.4% for Social Security and 2.9% for Medicare. For instance, if your business earns $100,000 in profit, you’ll owe about $15,300 in self-employment taxes – before factoring in income tax.

On the other hand, selecting an S-Corporation allows you to divide your income between a salary (subject to payroll taxes) and tax-free distributions. Meanwhile, C-Corporations benefit from a flat 21% tax rate, which is generally lower than the top individual tax rate of 37%.

Additionally, pass-through entities can take advantage of the 20% Qualified Business Income (QBI) deduction under Section 199A. This deduction reduces the effective top tax rate on business income from 37% to roughly 29.6% – a significant advantage, especially as this benefit becomes permanent in 2025 under the One Big Beautiful Bill Act (OBBBA).

For those planning to sell their business, C-Corporation shareholders may exclude up to $15 million in capital gains under the expanded Qualified Small Business Stock (QSBS) rules for stock acquired after July 4, 2025. As accountant Vinay Navani from WilkinGuttenplan explains:

"If I’m starting a business, I want to look hard at whether I want to be a C corporation or a pass through, especially if I could reasonably see myself selling my business in three-plus years."

These distinctions are vital for businesses of all sizes, offering tailored opportunities to reduce tax burdens.

Applicability to Small Business Owners

Choosing the right entity isn’t just for large corporations. Small business owners should consider electing S-Corp status once profits hit around $50,000 annually. At this level, the payroll tax savings from distributions typically outweigh the additional compliance costs.

In addition, many high-tax states now allow Pass-Through Entity (PTE) tax elections, enabling business income to be taxed at the entity level. This can help bypass the $10,000 federal cap on State and Local Tax (SALT) deductions, making it a valuable tool for small businesses.

Compliance with U.S. Tax Laws

Your filing requirements depend on your business structure. For example:

- Sole proprietors file a Schedule C with Form 1040.

- C-Corporations use Form 1120.

- S-Corporations file Form 1120S.

The IRS emphasizes that the best structure depends on each business owner’s unique situation. As they note:

"The answer to the question ‘What structure makes the most sense?’ depends on the individual circumstances of each business owner."

If you choose S-Corporation status, paying yourself a "reasonable salary" that aligns with industry standards is essential. This ensures compliance with IRS guidelines and avoids potential penalties.

Ease of Implementation

Beyond tax benefits, consider the complexity of setting up and maintaining your chosen structure. LLCs are particularly flexible, as they can be taxed as a sole proprietorship, partnership, S-Corp, or C-Corp depending on your needs. Electing S-Corporation status requires filing Form 2553 with the IRS, while operating as a C-Corporation involves more formalities, such as detailed recordkeeping, formal meetings, and complex tax filings.

CPA Mike Jesowshek highlights the importance of action:

"Learning tax strategies is great, but knowledge alone doesn’t create savings – taking action and structuring your business correctly does."

Choosing the right entity lays the groundwork for all future tax-saving strategies, aligning with your income, reinvestment goals, exit plans, and state tax considerations.

sbb-itb-ba0a4be

2. Elect S-Corporation Status to Cut Self-Employment Taxes

Once you’ve selected the right business structure, opting for S-Corporation status can lead to noticeable tax savings by reducing the amount you pay in self-employment taxes.

Tax Savings Potential

S-Corporation status offers a smart way to minimize self-employment taxes by splitting your income into two parts: a reasonable salary and distributions. The salary portion is subject to the 15.3% FICA tax (covering Social Security and Medicare), but distributions avoid payroll taxes and are only taxed as ordinary income.

Here’s an example for a business earning $150,000 annually:

| Structure | Salary | Distributions | Employment/Self-Employment Tax | Estimated Annual Savings |

|---|---|---|---|---|

| Sole Proprietor | N/A | $150,000 | ~$21,194 | $0 |

| S-Corporation | $75,000 | $75,000 | ~$11,475 | ~$9,719 |

For 2026, Social Security tax only applies to wages up to $176,100. On average, S-Corporation owners save between $5,000 and $50,000 annually compared to sole proprietors or standard LLCs. However, it’s essential to follow the rules. As Morgan V. Giebel Cannon, CPA, explains:

"The potential savings are real, but so are the rules and responsibilities that come with this structure."

Applicability to Small Business Owners

S-Corporation status works best for small business owners whose net income consistently exceeds $60,000–$80,000. Below that range, the added costs – such as payroll processing ($40–$150 per month), higher tax preparation fees ($800–$2,500 more than a Schedule C), and state compliance fees ($100–$800) – can offset the tax benefits.

One key requirement is paying yourself a "reasonable salary" that aligns with industry standards. This is a common focus for IRS audits, with 73% of S-Corp audits reviewing owner compensation. To avoid issues, use resources like Bureau of Labor Statistics data or industry surveys to document your salary decision.

Compliance with U.S. Tax Laws

To elect S-Corp status, file Form 2553 with the IRS by March 15 of the year you want the election to take effect. Your business must meet these criteria:

- Be a domestic entity.

- Have no more than 100 shareholders.

- Issue only one class of stock.

- Ensure shareholders are individuals, certain trusts, or estates (not partnerships, corporations, or non-resident aliens).

Once elected, you’ll need to file Form 1120-S annually and issue Schedule K-1s to shareholders, detailing their share of income, deductions, and credits. Additionally, S-Corp owners must file quarterly payroll reports (Form 941) and annual unemployment tax forms (Form 940).

BusinessAnywhere offers S-Corp tax election filing for $147, simplifying the Form 2553 submission process.

Ease of Implementation

Running an S-Corporation requires formal payroll, corporate recordkeeping, and filing a separate business tax return. As SDO CPA points out:

"If you expect net income above $80,000 for at least two consecutive years, S-Corp election typically makes sense."

Another perk is that if you’re a shareholder owning 2% or more of the business, the company can pay your health insurance premiums. While these premiums are included in your W-2 wages, they aren’t subject to FICA taxes when reported correctly, and you can still deduct them on your personal tax return. This adds another layer of savings to the salary-distribution strategy.

3. Claim the Qualified Business Income (QBI) Deduction

The Qualified Business Income (QBI) deduction is a powerful way to lower your taxable income – potentially by up to 20%. This deduction, made permanent for tax year 2026 under the One Big Beautiful Bill Act, offers a straightforward approach to reducing federal taxes over the long term.

Tax Savings Potential

Here’s how it works: If you have $100,000 in qualified income, you could claim a $20,000 deduction. However, the actual tax savings will depend on your tax bracket and overall financial situation.

For 2026, the full 20% deduction applies to single filers with taxable income under $203,000 and married couples filing jointly with income under $406,000. The deduction begins to phase out at $272,300 for single filers and $544,600 for joint filers. Even if your business income is modest, a minimum $400 deduction is available for those earning at least $1,000 in qualified business income.

| 2026 Filing Status | Full Deduction Threshold | Complete Phase-out |

|---|---|---|

| Single / Head of Household | Below $203,000 | $272,300 |

| Married Filing Jointly | Below $406,000 | $544,600 |

Keep in mind that these thresholds and phase-outs play a critical role in determining your eligibility.

Applicability to Small Business Owners

This deduction is especially relevant for small business owners operating as pass-through entities, including sole proprietorships, partnerships, S corporations, and limited liability companies. Qualified business income generally refers to net profits from domestic trade or business activities. However, it excludes items like capital gains, interest, dividends, and reasonable compensation paid to S corporation owners.

If you’re in a Specified Service Trade or Business (SSTB) – such as healthcare, law, accounting, consulting, or financial services – you’ll face stricter limitations. For these industries, the deduction phases out entirely once income exceeds the specified thresholds.

Compliance with U.S. Tax Laws

Claiming the QBI deduction is relatively straightforward. You’ll report it on your individual tax return using Form 8995 (Simplified) or, for more complex situations, Form 8995-A (Detailed). High-income earners exceeding the thresholds should note that the deduction is further limited by factors like W-2 wages paid and the unadjusted basis of qualified property (UBIA). In these cases, the deduction is capped at the greater of:

- 50% of W-2 wages paid, or

- 25% of W-2 wages plus 2.5% of UBIA.

Maximizing the Deduction

Want to get the most out of your QBI deduction? Start by lowering your taxable income. Contributing to retirement plans like a Solo 401(k) or SEP-IRA can help you stay within the income range for the full 20% deduction.

For S corporation owners, balancing wages and distributions is key since only profits beyond a reasonable salary qualify for the deduction. If your income exceeds the limits, consider hiring employees instead of contractors to increase your W-2 wage base. Alternatively, investing in equipment can boost your UBIA, creating more room for tax savings.

"The value of a good tax professional is to look for tax savings opportunities for their clients. QBI is a nice place to start!"

- Mike D’Avolio, CPA, JD, Intuit ProConnect Group

4. Use Retirement Plan Contributions to Defer Taxes

Contributing to retirement plans is a smart way to lower your tax bill while securing your financial future. Just like structuring your business entity or optimizing your salary, retirement contributions let you reduce taxable income today while your investments grow tax-deferred until retirement.

When you contribute to traditional retirement accounts, you’re using pre-tax dollars. This means the amount you contribute is subtracted from your taxable income, reducing the taxes you owe now. It’s a win-win: you save on taxes today while building a nest egg for tomorrow.

Tax Savings Potential

For 2025, you can contribute up to $23,500 to a 401(k) plan through elective deferrals. If you’re 50 or older, you can add another $7,500 in catch-up contributions, bringing the total to $31,000. Business owners with a Solo 401(k) can contribute both as an employee and an employer, allowing for combined contributions of up to $70,000 (or $77,500 if you’re 50 or older).

Other retirement plans offer similar advantages. For example:

- SEP IRAs allow contributions up to the lesser of $70,000 or 25% of your compensation.

- SIMPLE IRAs, which are great for smaller teams, let you contribute $16,500 in salary reductions, plus employer matching.

These contributions directly lower your taxable income, potentially even dropping you into a lower tax bracket.

"One of the most effective ways to reduce taxable income is through retirement plans. High-income business owners can use these to defer income while securing future financial stability."

- Christopher J. Picciurro, CPA/PFS

Applicability to Small Business Owners

Choosing the right retirement plan depends on your business size and structure. Here’s how some popular plans compare:

| Plan Type | 2025 Max Contribution | Setup Complexity | Best For |

|---|---|---|---|

| SEP IRA | $70,000 or 25% of pay | Easy | Sole proprietors or small teams |

| SIMPLE IRA | $16,500 (plus match) | Easy | Businesses with 100 or fewer employees |

| Solo 401(k) | $70,000 ($77,500 if 50+) | Moderate | Business owners with no employees (except a spouse) |

For owner-only businesses or those employing just a spouse, Solo 401(k)s offer the highest contribution potential. On the other hand, SEP IRAs are ideal for sole proprietors or small teams, providing high contribution limits with minimal setup. SIMPLE IRAs work best for businesses with fewer than 100 employees, offering an easy way to encourage employee participation.

Retirement contributions also help you stay under income thresholds for other tax benefits. For example, contributing to a Solo 401(k) or SEP IRA can keep your taxable income below $406,000 for married couples, preserving the full 20% Qualified Business Income (QBI) deduction.

Compliance with U.S. Tax Laws

Setting up a retirement plan is more flexible than you might think. For instance, you can establish a SEP IRA as late as your tax filing deadline, including extensions. SIMPLE IRAs, however, must generally be set up between January 1 and October 1, though new businesses might have some extra flexibility.

Small employers can also take advantage of tax credits. Businesses with 1–50 employees can claim up to $5,000 annually for three years to cover startup costs for retirement plans. Simply file Form 8881 to claim the Credit for Small Employer Pension Plan Startup Costs. Plus, if you implement automatic enrollment, you can receive an additional $500 credit per year for three years.

Ease of Implementation

Once you’ve chosen the right plan, implementing it is straightforward. SEP and SIMPLE IRAs are easy to set up through most financial institutions and require minimal ongoing maintenance. Solo 401(k)s involve slightly more steps but remain manageable for most small business owners. The key is selecting a plan that aligns with your business’s size and your retirement savings goals.

"The goal as a business owner is to turn as many after-tax dollars into pre-tax dollars as legally possible."

- Mike Jesowshek, CPA

Timing is everything. While SEP IRAs allow for late establishment, contributing early in the year gives your investments more time to grow tax-deferred.

5. Split Income with Family Members

Building on earlier strategies like entity selection and retirement contributions, splitting income with family members can significantly reduce your tax burden. The concept is simple: shift income from a high tax bracket (like a parent at 37%) to a family member in a lower bracket (such as an adult child at 22%). This difference could result in a 15% tax savings on the transferred income.

For small business owners, there are legitimate ways to make this happen. For example, you can hire family members to perform actual work for your business. Another powerful option is the Augusta Rule (IRC Section 280A(g)), which lets you rent your home to your business for up to 14 days each year. This allows your business to deduct the rental expense while you receive the income tax-free. In a real-world example from 2025, a medical group owner used this rule to generate $14,000 in tax-free income, contributing to $54,000 in overall tax savings.

"The Augusta Rule (IRC 280A(g)) lets you rent your home to your own business for ‘retreats’ or meetings, deduct the expense from your business, and receive the rent tax-free." – Kenneth Dennis, Vice President, KDA Inc.

Tax Savings Potential

The financial benefits of income splitting can add up quickly, especially for business owners who involve multiple family members.

One advanced approach is using Family Limited Partnerships (FLPs). These allow you to transfer business interests at a discounted value (typically 25% to 40%, due to lack of marketability and control), which can lower estate tax liabilities. Under the current exemption of $15 million per person for 2026, this strategy becomes even more valuable.

| Strategy | Primary Tax Benefit | Key Requirement |

|---|---|---|

| Hiring Children | Deductible wages; potential payroll tax savings for minors | Reasonable pay for actual work |

| Family Limited Partnership | Reduced estate taxes through valuation discounts | Requires qualified appraisal and legitimate business purpose |

| Augusta Rule | Tax-free rental income; business expense deduction | Limited to 14 days with documented business events |

Applicability to Small Business Owners

Income splitting works best when family members contribute real value to your business. For instance, a teenager could manage social media or inventory for a retail operation, while a spouse might handle bookkeeping or administrative tasks for a consulting firm.

Paying family members’ wages is deductible, and for children under 18, Social Security and Medicare taxes may not apply. In 2025, children under 18 can earn up to $15,750 tax-free, thanks to the standard deduction.

However, the IRS scrutinizes family employment arrangements. To avoid issues, document job descriptions, hours worked, and tasks completed. Pay rates must be in line with what you’d pay a non-family employee.

For more advanced strategies like FLPs, professional guidance is critical. These require a qualified appraisal and must serve a clear business purpose beyond tax savings. The IRS closely monitors such arrangements, so thorough documentation is essential.

Compliance with U.S. Tax Laws

To ensure compliance, family members must perform legitimate work. Use proper payroll forms (like W-2s) and withhold taxes as required.

Be mindful of the "kiddie tax" rules, which apply to unearned income (such as dividends or partnership distributions) for children under 19 – or under 24 if they are full-time students. This income is taxed at the parents’ rate, so shifting passive income may not always be beneficial. Prioritize earned income through actual employment to sidestep these rules.

"The IRS won’t respect allocations that exist only on paper: Ownership must be real." – SDO CPA

For FLPs, waiting 6 to 12 months after forming the partnership before gifting interests can help demonstrate that the entity serves a legitimate purpose. This can also reduce the risk of the IRS challenging the arrangement as a "step transaction".

When using the Augusta Rule, keep detailed records like meeting agendas, attendee lists, and minutes to prove the business purpose of your events.

Ease of Implementation

Hiring family members is relatively straightforward. Set up payroll, document their responsibilities, and ensure pay is reasonable. Most payroll software can handle these tasks efficiently.

The Augusta Rule is also easy to implement. Determine a fair market rental rate for your home, document your business meetings, and stay within the 14-day limit.

FLPs and gifting strategies, on the other hand, require more expertise. You’ll likely need an attorney for partnership agreements, an appraiser for business valuations, and a CPA for tax reporting. These upfront costs can be worthwhile if your business has significant value.

If you’re just starting out, focus on simpler strategies like hiring family members or using the Augusta Rule. As your business grows, consider more advanced approaches with professional guidance. Regardless of the strategy, thorough documentation is non-negotiable to support these income-shifting methods.

6. Apply Section 179 and Bonus Depreciation for Equipment

Using equipment deductions can be a smart way to reduce taxable income and improve cash flow. Just like adjusting your business structure or fine-tuning wages, timing your equipment purchases strategically can turn expenses into immediate tax benefits.

When you buy equipment for your business, you can deduct the full cost in the same year. Section 179 allows you to write off the entire purchase price of qualifying equipment, software, and furniture as soon as it’s put into use. Once you hit the Section 179 limit, bonus depreciation takes over. Thanks to the One Big Beautiful Bill Act passed in July 2025, bonus depreciation is now permanently set at 100% deductible.

For example, if you buy a $75,000 piece of machinery in 2026, you could deduct the entire amount on your 2026 tax return instead of spreading the cost over several years. In 2026, the Section 179 deduction limit is $2.56 million, with deductions phasing out once your total spending exceeds $3.22 million.

"Section 179 isn’t just some obscure tax code, it’s a practical tool that can give your business a real financial edge. By letting you deduct the full cost of qualifying purchases right away, it can lower your tax bill and free up cash when you need it most."

- Jacob Dayan, CEO, Community Tax LLC

Tax Savings Potential

The ability to write off costs immediately can lead to substantial savings. For instance, if you’re in the 37% tax bracket and purchase $200,000 worth of equipment, you could save approximately $74,000 in federal taxes. Both new and used equipment qualify, as long as the asset is new to your business. It’s worth noting that Section 179 deductions are capped at your business’s taxable income and can’t create a loss, whereas bonus depreciation can generate or increase a net operating loss that you can carry forward.

| Feature | Section 179 | Bonus Depreciation |

|---|---|---|

| Annual Limit | $2.56 million (2026) | No dollar limit |

| Can Create Tax Loss? | No | Yes |

| Flexibility | Choose specific dollar amounts | Generally applies to all assets in a class |

| Order Applied | First | After Section 179 |

What Qualifies for Small Business Owners?

Section 179 applies to tangible personal property like machinery, office furniture, tools, and off-the-shelf software. It also includes certain improvements to nonresidential buildings, such as roofs, HVAC systems, fire protection systems, and security systems.

For vehicles, the rules are a bit more specific. For example, if you buy a heavy SUV, van, or pickup truck with a Gross Vehicle Weight Rating over 6,000 pounds, you may qualify for a larger deduction compared to a standard passenger car. In 2025, the maximum Section 179 deduction for SUVs was $31,300. Keep in mind that assets must be used primarily for business – if a laptop is used 70% for business and 30% for personal use, only 70% of its cost qualifies for the deduction.

Timing and Compliance

Timing is everything. To qualify for the deduction in a given tax year, equipment must be "placed in service", meaning delivered, set up, and actively used in your business, by December 31. Simply ordering or paying for the equipment isn’t enough. Use Form 4562 to elect the Section 179 deduction and report depreciation. If your Section 179 deduction exceeds your taxable income, the unused portion can generally be carried forward to future years.

This approach works well alongside other tax strategies, such as preserving your Qualified Business Income (QBI) deduction. For example, if you’re approaching the QBI phase-out threshold – around $406,000 for married couples filing jointly in 2026 – these deductions can help you stay below the limit and keep your 20% deduction intact.

Making It Work

The process is straightforward: purchase qualifying equipment, ensure it’s in service by December 31, and file Form 4562. Most accounting software can handle these calculations. Apply Section 179 first to reduce taxable income, then use 100% bonus depreciation for any remaining balance to maximize your savings.

Proper documentation, such as receipts, delivery dates, and records of business use, is essential in case of an IRS audit. When combined with a broader tax strategy, these deductions can provide a meaningful boost to your business’s financial flexibility.

7. Harvest Capital Gains at 0% Tax Rate

Timing your capital gains strategically can help you take advantage of a 0% federal tax rate on long-term investment profits. This approach applies to long-term capital gains, which come from assets held for more than a year. For 2025, married couples filing jointly can qualify for this rate if their taxable income remains below $96,700. Including the standard deduction of $20,250, their adjusted gross income (AGI) could go up to $116,950 while still potentially enjoying a 0% tax rate on long-term gains.

Tax Savings Potential

This strategy can lead to significant savings, as long-term capital gains are usually taxed at 15% or 20%, depending on income. Meanwhile, short-term gains – profits from assets held less than a year – are taxed as ordinary income, with rates climbing as high as 37%. For instance, if you sell $50,000 worth of long-term assets while staying within the 0% bracket, you could avoid paying $7,500 to $10,000 in federal taxes.

If you’re an S-Corp vs LLC tax benefits offer different advantages; for an S-Corporation owner, there’s an extra benefit. Distributions exceeding your "basis" in the company are taxed as capital gains. If your taxable income is low enough, these gains could also fall under the 0% federal tax rate. This works well alongside other strategies like reducing taxable income and maximizing deductions.

Applicability to Small Business Owners

Small business owners can use this strategy to their advantage by lowering their AGI through other tax-saving techniques. If your business has a slower year, it might be the perfect time to sell appreciated assets or compare a sole proprietorship vs S Corp to see if incorporating provides better long-term shielding – whether it’s stocks, real estate, or part of your business interest.

You can also spread asset sales over multiple years to keep your taxable income low. For those selling a business, installment sales can help by dividing payments across several years, ensuring each year’s gain stays within the 0% capital gains threshold.

"By carefully timing capital gains in a low-income year, you can secure long-term tax savings that would otherwise be taxed at a higher rate in the future."

- Oberlander & Co Team

Compliance with U.S. Tax Laws

While pursuing these tax savings, it’s important to follow IRS guidelines. Assets must be held for at least 366 days to qualify as long-term, and you should keep detailed records of purchase and sale dates, as well as the business use percentage of any assets. Additionally, the IRS requires you to offset gains with any capital loss carryovers before applying the 0% rate.

Keep in mind that some states, like California, treat capital gains as ordinary income. Even if you qualify for the 0% federal rate, state taxes may still apply. Check your state’s tax rules to avoid surprises.

Ease of Implementation

Putting this strategy into action is straightforward. Start by calculating your projected taxable income for the year, factoring in all deductions. If you’re within the qualifying range, sell appreciated assets before year-end to lock in the 0% rate. Most tax software and brokerages can help track holding periods and calculate gains automatically. As with other tax-saving strategies, proper planning and documentation are key. Work with your CPA to coordinate retirement contributions, QBI deductions, and expense timing to help you stay within the 0% bracket.

8. Use Higher SALT Deduction Limits

In July 2025, the One Big Beautiful Bill Act raised the SALT (State and Local Tax) deduction cap from $10,000 to $40,000 for the 2025 tax year. This change provides much-needed relief for business owners in states with high taxes. However, for taxpayers with an AGI (Adjusted Gross Income) over $500,000 – or $250,000 for married couples filing separately – the deduction phases out by 30% for every dollar above these thresholds. These new limits open up opportunities for more advanced tax planning.

Tax Savings Potential

When combined with earlier strategies like entity selection, the higher SALT cap can lead to major savings. One particularly effective approach is pairing the increased cap with a Pass-Through Entity Tax (PTET) election, which allows personal SALT expenses to be converted into fully deductible business expenses. Currently, more than 30 states offer PTET programs.

Take this example: In 2025, a tech entrepreneur in Los Angeles earning $1.2 million faced $80,000 in combined state income and property taxes. By working with Straight Talk CPAs to elect California’s PTET for their S-Corp, $35,000 of personal SALT expenses were turned into a fully deductible business expense. Along with other tax strategies, this reduced the entrepreneur’s federal tax rate by over 7 percentage points, saving more than $60,000.

Applicability to Small Business Owners

The benefits of this deduction are especially helpful for small business owners. S-corporations, LLCs, and partnerships can take advantage of PTET elections if they are paying significant state taxes and their business qualifies as an active trade or business. For those with income near the $500,000 threshold, timing deductions or deferring income can help preserve the full $40,000 SALT deduction.

"Making a PTE election can allow you to absorb more of the $40,000 annual SALT cap through other taxes while paying the remainder through the PTE strategy."

- Blake Christian, Tax Partner, Holthouse Carlin & Van Trigt LLP

Compliance with U.S. Tax Laws

PTET elections need to be made annually by specific deadlines, such as March 15 for S-corporations. Missing these deadlines means losing the chance to bypass the SALT cap for that year. Additionally, you’ll need to carefully evaluate how state-level credits interact with federal deductions. Some states may not recognize credits for taxes paid at the entity level in another jurisdiction, which could unintentionally increase your overall tax burden. Keeping detailed records, such as board minutes and residency documentation, is crucial when claiming state-specific benefits.

Ease of Implementation

To implement PTET elections correctly, it’s essential to work with a CPA experienced in multi-state taxation. Your advisor should carefully model how entity-level tax deductions, owner credits, and residency rules interact across all states where you operate. Planning ahead is key, as the SALT cap will increase by 1% annually from 2026 to 2029 before reverting to $10,000 in 2030. Strategically timing your SALT payments can help you maximize the $40,000 cap during this period.

9. Claim Home Office and Vehicle Deductions

Home office and vehicle deductions are often overlooked, but they can provide meaningful tax savings for small business owners when properly documented. These deductions allow you to offset ordinary business expenses, lowering your taxable income without requiring extra spending. They work well alongside other tax strategies by directly reducing what you owe.

Tax Savings Potential

If you have a home office, you can choose between two methods for calculating your deduction:

- Simplified Option: Deduct $5 per square foot, up to 300 square feet, for a maximum of $1,500.

- Regular Method: Calculate the business percentage of actual expenses like mortgage interest, utilities, insurance, and depreciation. This method is often more advantageous if your actual expenses exceed $1,500 annually.

For vehicle deductions, you also have two options:

- Standard Mileage Rate: For 2025, the rate is $0.70 per mile, covering fixed and variable costs.

- Actual Expenses Method: Deduct the business percentage of fuel, repairs, insurance, and depreciation.

If you drive a lot for business, these vehicle-related deductions can add up to thousands of dollars in tax savings.

Applicability to Small Business Owners

To qualify for the home office deduction, the space must be used exclusively and regularly for business purposes. It also needs to be your principal place of business, meaning it’s where you handle administrative tasks like billing, bookkeeping, or ordering supplies. Importantly, the space cannot double as a personal area, such as a guest room or family lounge.

For vehicle deductions, the car must be used for business purposes. Common examples include trips to meet clients, traveling between job sites, or running errands like depositing business checks or picking up supplies. However, commuting from home to a regular workplace doesn’t qualify as business use.

Compliance with U.S. Tax Laws

The IRS has strict rules for claiming these deductions. For home offices, you must ensure the space is used exclusively for business – no personal activities are allowed.

Vehicle deductions require detailed recordkeeping. You’ll need a mileage log that includes dates, destinations, business purposes, and miles driven. Even if you use the standard mileage rate, it’s a good idea to track actual expenses during the first year to compare which method offers the better deduction. Since vehicles are considered "listed property", the IRS enforces strict documentation rules.

Ease of Implementation

The simplified home office method is straightforward: measure your office space and multiply by $5. The regular method involves more effort but can result in larger deductions if your expenses are substantial. Choose the method that best balances your time and potential savings.

For vehicles, a mileage tracking app or a simple spreadsheet can make compliance easy. Start by recording your odometer reading at the beginning and end of the year, then log business trips as they happen. This small habit ensures you’re ready to claim every eligible deduction come tax season.

These deductions not only help you save money but also complement broader tax strategies, making them a practical addition to your financial planning.

10. Defer Income and Accelerate Deductions

Timing is everything when it comes to taxes. By strategically deciding when to recognize income and when to pay expenses, you can shift taxable income between years and potentially save thousands. This approach is especially effective for small businesses using cash-basis accounting – a common choice for service providers.

Tax Savings Potential

Deferring income to the following year means you won’t pay taxes on it this year, while paying expenses early creates immediate deductions. For businesses earning $150,000 or more annually, these strategies can result in savings ranging from $10,000 to $50,000.

"Tax planning happens in October. Tax preparation happens in April. The difference is tens of thousands of dollars." – SDO CPA

Here’s an example: If you’re in a 24% tax bracket, deferring $50,000 of income and accelerating $30,000 in deductions shifts $80,000 of taxable income. This could save you $19,200 this year. The benefits are even greater if you anticipate being in a lower tax bracket next year or need to stay under certain thresholds, like the $203,000 (single) or $406,000 (married filing jointly) limits for the Qualified Business Income (QBI) deduction.

How It Works for Small Businesses

This strategy is particularly useful for cash-basis businesses, which include consultants, lawyers, accountants, and healthcare professionals. Under cash-basis accounting, income is recognized when payment is received, and expenses are deducted when paid.

- Deferring income: Delay sending invoices until late December so payment arrives in January. This shifts income into the next tax year.

- Accelerating expenses: Pay bills before December 31 instead of waiting until January or February. You can prepay up to 12 months of expenses, such as insurance premiums, rent, or software subscriptions, under the 12-Month Rule. These payments are deductible immediately, provided the benefit period doesn’t extend more than 12 months from the payment date.

For equipment purchases, timing is even more critical. Thanks to the One Big Beautiful Bill Act, bonus depreciation returned to 100% for 2026. To qualify for full deductions, equipment must be delivered, installed, and operational by December 31.

| Accounting Method | Income Recognition | Expense Recognition | Deferral Ease |

|---|---|---|---|

| Cash Method | When cash is received | When cash is paid | High – delay billing or prepay bills |

| Accrual Method | When service is provided | When obligation is incurred | Low – requires adjusting delivery dates |

Staying Compliant with IRS Rules

Proper timing is essential to follow IRS guidelines. For cash-basis businesses, the constructive receipt doctrine states that income is taxable as soon as it’s available to you. So, if a check is waiting, you can’t just ignore it to delay taxation. However, not sending an invoice until late December is perfectly legal.

The 12-Month Rule allows you to deduct prepaid expenses like rent or insurance immediately, provided the coverage period doesn’t exceed 12 months from the payment date. For equipment, the IRS requires it to be operational by December 31 to qualify for deductions. Simply ordering or making a down payment isn’t enough – it must be ready for use.

"If you’re a manufacturer looking to expand a product line or a dentist in need of new chairs, and you’re looking for deductions in 2025, now could be a good time to move forward." – Vinay Navani, Accountant, WilkinGuttenplan

Easy Steps to Implement

Start by reviewing your accounts receivable in early December. If you’re nearing a tax bracket threshold or income limit, hold off on sending final invoices until the last week of the year. Most clients won’t pay until January anyway, helping you achieve the deferral you need.

For expense acceleration, identify bills you can pay early, such as insurance premiums, software subscriptions, or rent. Write those checks before December 31 to claim this year’s deduction.

Equipment purchases require more coordination. Work with vendors to ensure delivery and installation by year-end. Keep documentation – like photos, delivery receipts, and invoices – to prove the equipment was operational by December 31.

"The goal as a business owner is to turn as many after-tax dollars into pre-tax dollars as legally possible." – Mike Jesowshek, CPA, Founder of TaxElm

Engaging in tax planning, which typically costs $2,000–$5,000, can deliver a return of over 500% through early savings. Acting before December 31 ensures you maximize these benefits.

11. Invest in Opportunity Zones for Tax Deferral

Opportunity Zones offer a way to defer capital gains taxes by reinvesting those gains into a Qualified Opportunity Fund (QOF). Whether you’ve sold stocks, crypto, real estate, or even your business, you can reinvest those profits into a QOF to defer taxes for up to five years. Even better, after 10 years, any new appreciation in the investment can be completely tax-free.

Tax Savings Potential

Opportunity Zones take the concept of tax deferral to the next level, turning deferred gains into potential tax-free growth. Here’s how the program works:

- Tax deferral: You can defer taxes on your original gains for up to five years.

- Basis increase: After five years, your basis increases by 10% in standard zones or 30% in rural zones.

- Tax-free appreciation: After holding the investment for 10 years, any additional gains become tax-free.

"Opportunity Zones work by converting past gains into future tax-free growth."

- Jimmy Atkinson, Founder of OpportunityZones.com

For instance, if you reinvest gains into a QOF located in a rural zone, you could benefit from the combined advantages of deferral, a higher basis, and tax-free appreciation on any new earnings.

Applicability to Small Business Owners

Small business owners can also take advantage of Opportunity Zones by setting up their own QOF. Filing IRS Form 8996 with your tax return allows you to reinvest gains from selling business assets – like equipment or investments – back into your own business, provided it operates in one of the 8,764 designated Opportunity Zones across the U.S..

"SMB owners can self-certify a QOF (via IRS Form 8996) and inject their own gains into their own OZ business."

- Schwartz & Schwartz

This strategy isn’t limited to real estate. Businesses like manufacturing plants, tech startups, retail stores, and service companies also qualify, as long as at least 50% of their gross income comes from activities within the zone. If your gains are reported on a Schedule K-1, you might even have extra time to plan, since the 180-day reinvestment window often starts on the entity’s tax return due date (typically March 15).

By leveraging this approach, small business owners can reinvest gains into growth while optimizing cash flow.

Compliance with U.S. Tax Laws

To keep your QOF status intact, at least 90% of the fund’s assets must be invested in Qualified Opportunity Zone property. For real estate, this means either purchasing "original use" property or substantially improving existing property by doubling its basis within 30 months. In rural zones, the improvement requirement is reduced to 50%.

Investors must file Form 8949 when realizing the gain to elect deferral and Form 8997 annually to report QOF holdings. Be aware that if you sell or gift your QOF interest before the deferral period ends, it triggers an "inclusion event", making the deferred gain immediately taxable.

These guidelines help ensure your Opportunity Zone investment remains a valuable part of your tax strategy.

Ease of Implementation

Setting up a QOF is relatively simple. You can form an LLC or corporation, file Form 8996 to self-certify as a QOF, and reinvest your capital gains within the 180-day window. To confirm whether your property or business location qualifies, you can use the U.S. Census Bureau’s Geocoder tool.

The program gained permanence on July 4, 2025, through the "One Big Beautiful Bill" Act. For investments made in 2026, tax deferral rules apply until year-end, while the updated "OZ 2.0" framework starts fresh on January 1, 2027, resetting the five-year deferral period. Since its launch in 2018, QOFs have raised an estimated $150 billion in equity.

12. Use Charitable Contributions and Donor-Advised Funds

Charitable contributions offer a smart way for small business owners to manage tax liability while supporting meaningful causes. Instead of donating cash, consider giving appreciated non-cash assets like stocks, real estate, or privately held business interests held for over a year. This approach allows you to deduct the full fair market value of the asset and avoid long-term capital gains taxes (typically 15%–20%).

A donor-advised fund (DAF) takes this strategy a step further. By making a large contribution to a DAF, you gain an immediate tax deduction and can recommend grants to charities over time. This method is especially useful for "bunching" – combining multiple years of donations into one high-income year to exceed the standard deduction.

Tax Savings Potential

Donating appreciated assets can increase the value of your donation by up to 20%. For instance, donating $50,000 in stocks with a $5,000 cost basis could save around $12,000 in taxes at a 24% tax rate. If you sold the stock first, you’d lose a significant portion to capital gains taxes, leaving less for donation.

Keep in mind these limits:

- Cash donations: capped at 60% of adjusted gross income (AGI)

- Non-cash appreciated assets: capped at 30% of AGI

For those aged 70½ or older, Qualified Charitable Distributions (QCDs) allow transfers of up to $108,000 (in 2025) directly from an IRA to a charity. This satisfies Required Minimum Distributions (RMDs) without increasing taxable income.

"Proactive tax planning for business owners, especially around charitable giving, can transform generosity into real tax savings and greater impact."

- Cindy Meares, Director of Tax Services, Cornerstone Wealth Group

Important Timing Note: Starting in 2026, itemizers must exceed a 0.5% AGI floor to claim charitable deductions, and the tax benefit for those in the 37% bracket will drop to 35 cents on the dollar. Plan large gifts before December 31, 2025, to maximize tax advantages.

Applicability to Small Business Owners

Small business owners can donate part of their privately held business interests to a DAF or qualified charity. This eliminates capital gains tax on the appreciation and allows a deduction for the full fair market value, provided you have a qualified appraisal for IRS compliance.

The bunching strategy works well for pass-through entities like S-Corps and LLCs. For example, during a profitable year, you could consolidate several years’ worth of donations into a DAF. A couple with $10,000 in annual giving might save an extra $5,800 over two years by using this approach.

"The goal as a business owner is to turn as many after-tax dollars into pre-tax dollars as legally possible."

- Mike Jesowshek, CPA

State-level incentives can also add value. For instance, states like North and South Carolina offer tax credits for charitable actions such as conservation easements, which can provide up to 25% of the donated value and complement federal deductions.

Compliance with U.S. Tax Laws

To claim charitable deductions, you must itemize on Schedule A of IRS Form 1040 and maintain accurate records. Donations involving private business interests require a qualified appraisal to determine fair market value.

Starting in 2026, corporations will face stricter limits, only deducting charitable gifts exceeding 1% of taxable income, with a total cap of 10%. As Vinay Navani, an accountant at WilkinGuttenplan, explains:

"Starting in 2026, corporations may only deduct gifts in excess of 1% of their taxable income."

Non-itemizers will also see changes. Beginning in 2026, individuals who don’t itemize can deduct up to $1,000 (or $2,000 for married couples filing jointly) for cash donations to operating charities. However, note that Qualified Charitable Distributions from IRAs cannot fund DAFs under current IRS rules.

This strategy fits seamlessly into broader tax planning efforts, like deferring income or accelerating deductions, offering small business owners a way to align charitable giving with tax efficiency.

Ease of Implementation

Donor-advised funds simplify the process of charitable giving while offering immediate tax benefits. Setting up a DAF is straightforward: the sponsoring organization handles administrative tasks like due diligence, investment management, and tax reporting. You simply open an account, contribute assets, and receive a tax deduction. The funds can grow tax-free while you recommend grants to charities over time.

For business owners, a "part-gift, part-sale" strategy can be advantageous. Donating long-term appreciated assets to a DAF helps offset capital gains taxes from rebalancing other parts of your portfolio. Using dedicated business bank accounts to separate business and personal expenses also ensures proper documentation for charitable contributions.

Conclusion

The 12 tax strategies discussed in this article offer small business owners practical ways to reduce their tax obligations while laying the groundwork for long-term financial health. From selecting the right business entity and opting for S-Corp status to taking advantage of retirement contributions and the 100% bonus depreciation made permanent by the One Big Beautiful Bill Act (OBBBA) signed on July 4, 2025, these methods can help save thousands of dollars each year and support smart financial planning.

Success hinges on planning ahead. As Allison Dunn, CEO of Deliberate Directions, puts it:

"Strategic tax planning… transforms taxes from a reactive burden into a proactive wealth-building tool that compounds benefits across multiple years".

This means shifting away from last-minute efforts during tax season. Instead, focus on year-round planning – scheduling major equipment purchases, managing income and deductions, and reassessing your business structure as your company evolves.

Tax laws are intricate and frequently updated. For instance, the OBBBA raised Section 179 limits to $2.5 million, increased SALT deduction caps to $40,000 per household, and boosted gift tax exemptions to $15 million per individual starting in 2026. Working with a qualified CPA or Enrolled Agent can help ensure compliance, avoid penalties, and uncover additional opportunities for savings, such as R&D credits or cost segregation.

FAQs

When does an S-Corp election start saving me money?

When your net income reaches roughly $60,000 to $80,000 or more, opting for an S-Corp election can often lead to tax savings. This is because the reduction in self-employment taxes on distributions usually offsets the extra expenses tied to payroll and compliance. However, it’s essential to take a close look at your individual financial circumstances to determine if this choice makes sense for you.

How do I know if I qualify for the 20% QBI deduction?

To be eligible for the 20% QBI deduction, your taxable income must stay under specific thresholds: $394,600 for married couples filing jointly and $197,300 for all other filers in 2025. This deduction is designed for income earned through pass-through entities, such as sole proprietorships, partnerships, and S corporations. However, it does not apply to income from C corporations.

If your taxable income goes above these thresholds, additional rules and limitations may come into play. For precise guidance, it’s wise to check the latest IRS guidelines or consult a tax professional to ensure you’re making the most of this deduction.

What records do I need to safely claim home office and vehicle deductions?

To qualify for home office deductions, you’ll need to prove the space is used exclusively and regularly for business purposes. This means keeping clear records that show how the area is dedicated to work. Be sure to track related expenses such as mortgage interest, rent, utilities, and any repairs.

For vehicle deductions, maintaining a detailed mileage log is essential. Record the date, miles driven, and the purpose of each trip. Additionally, save receipts for fuel, maintenance, and insurance costs. Keeping accurate and thorough records not only helps you stay compliant but also protects you in case of an audit.