Getting worker classification right is crucial to avoid tax issues, legal penalties, and compliance risks. Workers can either be employees or independent contractors, and misclassification can lead to fines, unpaid taxes, and other liabilities. Here’s what you need to know:

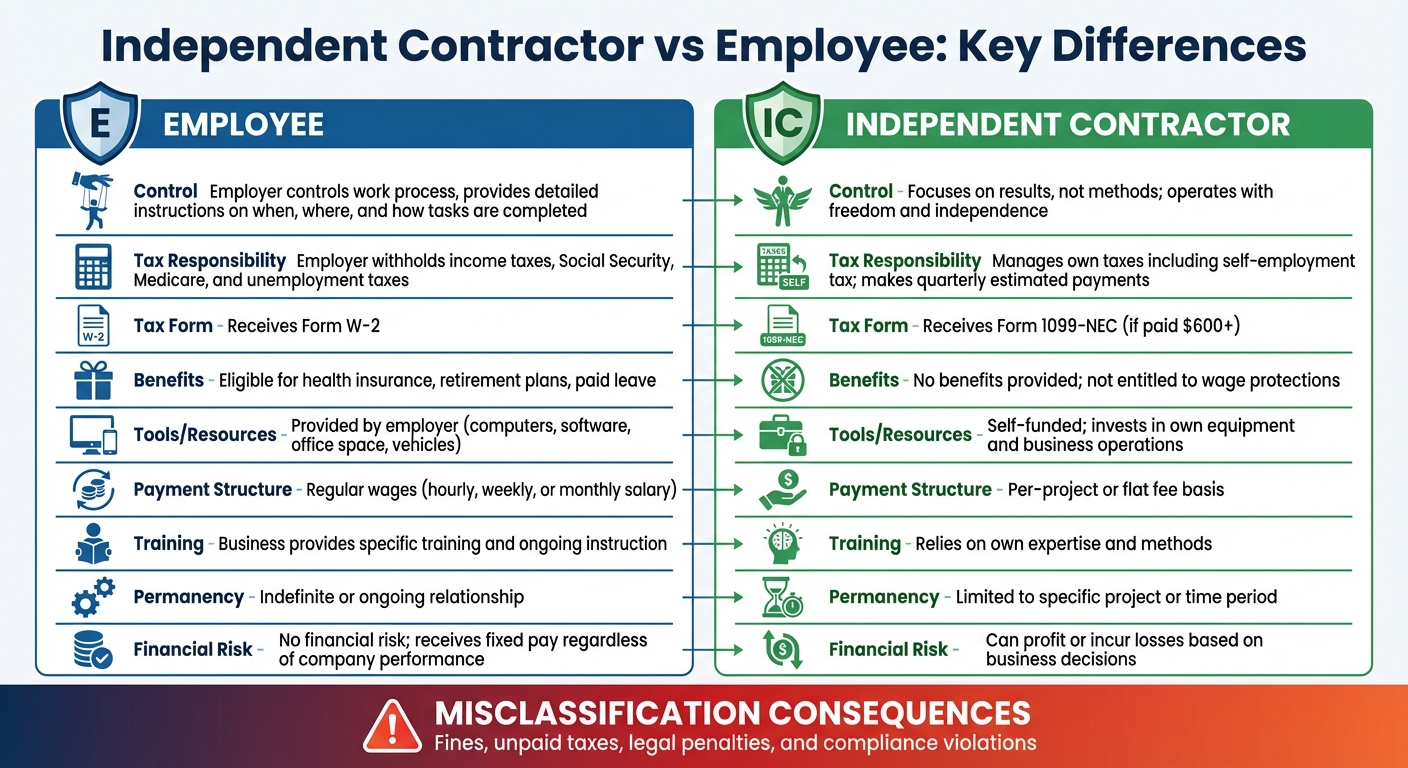

- Employees: Employers must withhold income taxes, contribute to Social Security, Medicare, and unemployment taxes, and provide benefits like health insurance or paid leave. Employees receive Form W-2 for tax reporting.

- Independent Contractors: They manage their own taxes, receive Form 1099-NEC if paid $600 or more, and are not entitled to benefits or wage protections under labor laws.

- Key Differences: Employees are under the employer’s control regarding how work is performed, while contractors have more independence and often invest in their own tools or resources.

- IRS and State Tests: The IRS uses the "Common Law" test, while states like California apply stricter rules like the "ABC test", which presumes workers are employees unless specific conditions are met.

Quick Comparison:

| Criteria | Employee | Independent Contractor |

|---|---|---|

| Control | Employer controls work process | Focuses on results, not methods |

| Tax Responsibility | Employer withholds and pays taxes | Contractor handles own taxes |

| Benefits | Eligible for benefits | No benefits provided |

| Tools/Resources | Provided by employer | Self-funded |

| Payment | Regular wages (hourly/salary) | Per-project or flat fee |

Key Takeaway: Misclassifying workers can lead to significant financial and legal consequences. Review worker relationships carefully, document decisions, and follow federal and state guidelines to ensure compliance.

Independent Contractor vs Employee Classification Comparison Chart

Independent Contractors vs. Employees: Main Differences

Understanding the differences between independent contractors and employees is crucial to avoid compliance issues. These differences revolve around control, tax responsibilities, and resource management.

Control and Independence

The level of control is one of the key distinctions between employees and independent contractors. The IRS explains:

"A worker is an employee when the business has the right to direct and control the worker. The business does not have to actually direct or control the way the work is done – as long as the employer has the right to direct and control the work."

For employees, the employer decides the specifics: when, where, and how tasks are completed. This often involves detailed instructions and ongoing training.

Independent contractors, on the other hand, operate with much more freedom. According to the IRS:

"The general rule is that an individual is an independent contractor if the payer has the right to control or direct only the result of the work, not what will be done and how it will be done."

Contractors are focused on delivering agreed-upon results and typically use their own methods. They also tend to work with multiple clients at the same time. This distinction in control extends into tax responsibilities and payment structures.

Tax Withholding and Payment Structure

Tax obligations vary significantly between these two classifications. For employees, employers must handle federal income tax withholding, as well as Social Security and Medicare taxes. Employers also pay their share of these taxes and contribute to federal unemployment tax. At the end of the year, employees receive a Form W-2 summarizing their earnings and tax withholdings.

Independent contractors are responsible for managing their own taxes. Employers do not withhold any taxes from contractor payments. Instead, contractors must pay self-employment taxes – which include Social Security and Medicare – along with income tax through quarterly estimated payments. If a contractor earns $600 or more in a year, the employer is required to issue a Form 1099-NEC.

These tax practices highlight the broader differences in how resources are handled for each worker type.

Tools and Resources

Another major difference lies in the provision of tools and resources. Employees typically receive all the necessary equipment from their employer – such as computers, software, office space, or vehicles – with these costs covered as part of the employer’s operations.

Independent contractors, however, supply their own tools and equipment. This financial responsibility underscores their status as independent businesses rather than workers reliant on a single employer.

The U.S. Department of Labor puts it this way:

"Independent contractors are workers who, as a matter of economic reality, are in business for themselves, whereas FLSA-covered employees are workers who are, as a matter of economic reality, economically dependent on the employer for work."

Examining how much a worker invests in their own tools compared to the employer’s overall investment can help clarify their classification. This is a key factor in distinguishing whether someone is truly independent or economically tied to a single business.

The IRS 3-Part Common Law Test

The IRS uses a three-part Common Law Test to determine whether a worker should be classified as an employee or an independent contractor. This test examines behavioral control, financial control, and the nature of the relationship between the worker and the business. Instead of relying on a single factor, the IRS evaluates the overall relationship using all three elements.

It’s important to note that the IRS focuses on the right to control rather than actual control. This means that even if a business doesn’t actively manage every aspect of a worker’s tasks, merely having the authority to do so could establish an employer-employee relationship.

Here’s a closer look at the three components of the test.

Behavioral Control

Behavioral control addresses how much direction and oversight the business has over the worker’s tasks. Key considerations include the level of instructions, evaluation systems, and training provided.

- Instructions: Employees often receive detailed guidance about when and where to work, which tools to use, who to hire as assistants, and the order in which tasks should be completed. The more specific and comprehensive these instructions, the more likely the worker is an employee. Independent contractors, on the other hand, are typically given flexibility to determine how they achieve the desired result.

- Evaluation Systems: If a business closely monitors how tasks are performed, it suggests an employee relationship. Evaluating only the final outcomes, without focusing on the process, is more neutral.

- Training: Regular training provided by the business – especially on specific methods – indicates an employee status. Independent contractors usually rely on their own expertise and methods without requiring such training.

Financial Control

The second part of the test examines whether the business controls the financial aspects of the worker’s role. This includes factors like investment, expenses, and payment structure.

- Significant Investment: Independent contractors often invest in their own tools, equipment, or business operations. Employees typically rely on resources provided by the employer.

- Unreimbursed Expenses: Contractors usually bear ongoing costs, such as office rent or equipment maintenance, without reimbursement. Employees, in contrast, are often reimbursed for work-related expenses.

- Opportunity for Profit or Loss: Independent contractors take on financial risk, meaning they can either make a profit or incur a loss based on their business decisions. Employees generally receive a fixed wage, regardless of the company’s financial performance.

- Services Available to the Market: Contractors can offer their services to multiple clients and pursue other business opportunities, unlike employees who usually work exclusively for one employer.

- Payment Method: Employees are typically paid on a regular schedule – hourly, weekly, or monthly. Contractors are often paid a flat fee for completing a specific project or job.

Nature of the Relationship

This part of the test examines how both parties view and structure their working relationship, as well as the practical realities of their arrangement.

- Written Contracts: While contracts can clarify the intended relationship, they’re not definitive. The actual working arrangement carries more weight than what’s written on paper.

- Employee Benefits: Offering benefits like health insurance, retirement plans, paid vacation, or sick leave strongly suggests employee classification.

- Permanency: An ongoing, indefinite relationship indicates employee status. Conversely, a relationship tied to a specific project or time frame points to contractor status.

- Key Activities: If the worker’s tasks are central to the business’s core operations, it’s more likely the business will exert control, indicating an employee relationship.

If you’re unsure about a worker’s classification, you can file Form SS-8 with the IRS for a determination. However, be aware that this process can take over six months.

| Factor | Employee Indicator | Independent Contractor Indicator |

|---|---|---|

| Instructions | Detailed guidance on tasks and processes | Minimal instructions; focus on results |

| Training | Business provides specific training | Worker relies on their own expertise |

| Payment Method | Regular wage (hourly, weekly, monthly) | Flat fee or per-project payment |

| Investment | Relies on employer-provided tools | Invests significantly in own resources |

| Expenses | Typically reimbursed by employer | Often covers own expenses |

| Profit/Loss | No financial risk; fixed pay | Can profit or incur losses |

| Benefits | Receives benefits like health insurance | No benefits provided |

| Permanency | Indefinite or ongoing relationship | Limited to specific project or period |

State Classification Rules and California’s ABC Test

While federal standards set the baseline, many states enforce stricter rules for worker classification. California’s ABC test stands out as one of the toughest, making it crucial for businesses operating there – or hiring workers based in the state – to understand its requirements.

Under California law, every worker is presumed to be an employee. To classify someone as an independent contractor, the hiring business must meet all three criteria of the ABC test. Missing just one means the worker must be classified as an employee, regardless of any contractual agreements.

"In California, employers cannot ‘contract around’ the law. Even if you prefer to be a contractor and sign a written agreement stating so, the courts and the Labor Commissioner will ignore the contract and apply the ABC test to the actual reality of the working relationship."

Failing to classify workers correctly in California can lead to civil penalties ranging from $5,000 to $25,000 per violation. The state estimates it loses around $1.5 billion annually in income taxes, Social Security withholdings, and unemployment taxes due to the misclassification of approximately 3.5 million workers.

The ABC Test: Criteria and Application

To classify a worker as an independent contractor under the ABC test, businesses must prove all three of the following conditions:

Prong A (Control): The worker must operate free from the hiring entity’s control or direction when performing their work. This applies both to the written agreement and the actual working relationship. If the business dictates how, when, or where tasks are completed, this prong is likely to fail.

Prong B (Usual Course of Business): The worker’s tasks must fall outside the company’s core business activities. For instance, if a bakery hires a cake decorator – a role central to its operations – the worker would fail this prong. However, hiring a plumber to repair a sink, which is unrelated to baking, would likely pass.

Prong C (Independent Business): The worker must have an independently established business in the same field as their work for the hiring entity. This often means they should hold a business license, operate from a separate location, and market their services to other clients.

Certain professions, such as doctors, lawyers, architects, and specific creative roles, are exempt from the ABC test. Instead, these workers are evaluated under the older Borello test, which uses a broader set of factors to determine classification.

| Prong | Requirement | Common Pitfall |

|---|---|---|

| A (Control) | Worker operates independently of the hiring entity’s control | Business dictates how tasks are performed or sets schedules |

| B (Usual Course) | Work is not part of the company’s main business | Worker performs tasks central to the company’s revenue |

| C (Independent Business) | Worker has their own established business | Worker lacks a business license or does not serve other clients |

The ABC test’s strict criteria mean businesses must carefully evaluate their worker relationships, especially when operating in multiple states.

Multi-State Compliance

Navigating worker classification becomes even more complex for businesses operating across state lines. The Fair Labor Standards Act (FLSA) does not override state laws, so companies must adhere to whichever standard offers the most protection to workers.

"The FLSA does not preempt any other laws that protect workers, so businesses must comply with all federal, state, and local laws that apply and ensure that they are meeting whichever standard provides workers with the greatest protection."

- U.S. Department of Labor

For businesses managing remote or multi-state workforces, applying California’s ABC test as a baseline can be a smart move. This approach helps reduce the risk of misclassification in states with stricter rules.

It’s also essential to track where workers physically perform their duties. For example, if a Texas-based business hires an independent contractor in California, the company must comply with California’s classification laws. This includes filing a Report of Independent Contractors (Form DE 542) with California’s Employment Development Department, even if the business is headquartered elsewhere.

Finally, remember that even if a worker passes California’s ABC test, they must also be evaluated under the IRS Common Law Test for federal tax purposes. Since these tests can produce different results, businesses should document their classification decisions thoroughly and be prepared to justify them under multiple legal frameworks.

How to Classify Workers: Step-by-Step Guide

Getting worker classification right involves a careful, step-by-step process that takes into account both federal and state rules. Here’s a straightforward guide to help you navigate this process while keeping detailed records at every stage.

Step 1: Review the Working Relationship

Start by examining the actual working relationship, not just the terms of the contract. Look at how much control your business has over the worker’s schedule, training, and work conditions. For example, do you set specific hours, provide extensive training, or closely oversee their tasks? Also, take note of how they’re paid – are they receiving a flat fee per project, or are they on an hourly or salaried basis?

"The substance of the relationship, not the label, governs the worker’s status." – IRS

Other factors to assess include whether the worker invests in their own tools or equipment and whether they cover business expenses without reimbursement. Check if they promote their services to other clients or work exclusively for your business. Finally, consider whether you offer employee benefits like health insurance or retirement plans, as these often signal an employer-employee relationship.

This initial review lays the groundwork for applying the appropriate federal and state classification tests.

Step 2: Apply IRS and State Tests

Once you’ve gathered the details, use them to apply the IRS and state guidelines for worker classification. The IRS Common Law Test focuses on three key areas: behavioral control (instructions and training), financial control (expenses and investments), and the type of relationship (contracts and benefits). The main question is whether your business has the right to control how work is done, even if you don’t actively exercise that control.

If you’re in a state that uses the ABC test, you’ll need to evaluate the worker against stricter criteria. Always follow the standard that offers the highest level of worker protection. If you’re still unsure after reviewing all factors, you can request an official determination from the IRS by submitting Form SS-8. Be aware, though, that the response time may take six months or more.

Step 3: Document Your Decision

After completing your analysis, document everything. Keep detailed records that explain your classification decision, including contracts, payment methods, and notes on work arrangements. These records will be crucial if your classification is ever challenged during an audit.

Also, save evidence of the worker’s business investments, such as equipment purchases or licenses, as well as marketing materials showing they serve other clients. If you provide any training or benefits, document who received them and why. This thorough paper trail demonstrates that you made a good-faith effort to comply with the rules.

Step 4: File the Correct Tax Forms

Once you’ve classified the worker, make sure to file the appropriate tax forms:

- For independent contractors earning $600 or more in a year, file Form 1099-NEC by January 31. Contractors are responsible for their own taxes, including self-employment tax, which applies if their net earnings are $400 or more.

- For employees, you’ll need to withhold federal income tax, Social Security, and Medicare taxes from their paychecks. Submit Form W-2 by January 31 to report their wages and withholdings. Additionally, you are responsible for paying the employer’s share of Social Security, Medicare, and unemployment taxes.

| Worker Type | Primary Tax Form | Filing Deadline | Tax Withholding |

|---|---|---|---|

| Independent Contractor | Form 1099-NEC | January 31 | None; worker pays self-employment tax |

| Employee | Form W-2 | January 31 | Employer withholds income, Social Security, and Medicare taxes |

sbb-itb-ba0a4be

Common Classification Mistakes to Avoid

Misclassifying workers can lead to audits, penalties, and unpaid employment taxes. To stay compliant and protect your business, it’s crucial to understand and steer clear of common mistakes. Here are some key areas to watch out for.

Relying on Job Titles Instead of Work Details

A worker’s title or contract doesn’t define their status – what matters is the actual working relationship. Both the IRS and the Department of Labor focus on how the relationship operates in practice, not the labels used.

"What the worker is called is not relevant – a worker may be an employee under the FLSA regardless of the title or label they are given." – U.S. Department of Labor

Pay attention to behavioral control, financial control, and the level of independence when determining classification.

Ignoring State-Specific Rules

Federal guidelines are just the baseline – state laws often impose stricter standards. For example, states like California and New Jersey apply the ABC test, which assumes a worker is an employee unless the company can prove all three test criteria. If your business operates in multiple states, you’ll need to comply with the most protective rules for workers.

Relying only on federal standards could leave you exposed to state-level penalties, including unpaid taxes and wage violations. Always review the specific requirements in each state where your workers are located.

Failing to Reassess Worker Status Over Time

Worker classification isn’t something you decide once and forget. Relationships can change, and so can the classification. For instance, if a contractor starts receiving more training, is required to follow a strict schedule, or becomes deeply integrated into your core business operations, it might be time to reevaluate their status.

"Continuously review all aspects of the worker relationship to detect shifts from contractor to employee status." – IRS

To stay ahead, implement an annual review process to assess each worker’s classification. If you identify a misclassification, you can use the Voluntary Classification Settlement Program (VCSP) by filing Form 8952. This program lets you correct classifications for future periods with reduced penalties, avoiding the risks of waiting for an audit to reveal the issue.

Compliance and Record-Keeping Best Practices

Keeping thorough records and meeting reporting requirements is essential for avoiding penalties. Both the IRS and the Department of Labor require businesses to maintain detailed documentation that supports their worker classification decisions and demonstrates compliance. This section builds on earlier classification guidelines by focusing on how to document and review worker relationships effectively.

Records to Maintain

Proper documentation should cover every aspect of your working relationships. The IRS evaluates actual work practices, not just written agreements, so it’s crucial to record details that address behavioral control, financial control, and the nature of the relationship with each worker. Essential records include:

- Written contracts and agreements

- Training materials and equipment usage logs

- Evaluation reports and invoices outlining payment methods

- Documentation of any instructions provided about how, when, or where work is performed

Also, keep records of benefits – or the lack thereof – such as health insurance, pension plans, or paid time off.

Tax-related documents are equally important. Retain copies of forms like Form W-2 for employees, Form 1099-NEC for contractors, and, if applicable, Form SS-8 if you’ve requested an official worker status determination from the IRS. Keep in mind that receiving a determination from the IRS via Form SS-8 can take six months or more.

Filing and Reporting Requirements

When filing taxes, ensure you submit the correct forms. Use Form W-2 for employees, which includes details on withholdings, and Form 1099-NEC for contractors earning $600 or more. Remember, FICA, Medicare, and unemployment taxes only apply to employees.

For businesses filing 10 or more returns, electronic submission is mandatory. The IRS offers the Information Returns Intake System (IRIS) – a free, secure platform for e-filing 1099 forms, requesting extensions, and making corrections. If filing paper returns, include Form 1096 as a summary transmittal.

Beyond filing, ongoing oversight is crucial to ensure compliance.

Annual Review and Updates

Worker classification isn’t static – it can change over time. Conduct annual reviews of your documentation and practices to reflect any changes in your working relationships. For instance, a contractor arrangement might evolve into an employment relationship if the worker starts receiving more training, adheres to a strict schedule, or becomes deeply involved in your core operations.

"The IRS is not required to follow a contract stating that the worker is an independent contractor… How the parties work together determines whether the worker is an employee or an independent contractor." – IRS

Set up a yearly review process to reassess classifications. Look for signs that the level of control has increased, the work has shifted from project-based to ongoing, or new benefits and resources are being provided. Keeping detailed records of these evaluations helps establish a reasonable basis for your decisions, which can reduce tax liabilities in case of an audit.

If you identify a misclassification during your review, you can address it proactively. The Voluntary Classification Settlement Program (VCSP) allows businesses to reclassify workers for future periods with reduced penalties by filing Form 8952. Correcting errors early can significantly reduce financial and legal risks.

Conclusion

Getting worker classification right is crucial for shielding your business from hefty financial and legal consequences. Misclassifying workers can lead to unpaid employment taxes, including Social Security, Medicare, and federal unemployment taxes, and may also result in violations of the Fair Labor Standards Act (FLSA). The FLSA ensures employees receive minimum wage and overtime pay – protections that cannot be signed away.

Rather than relying on job titles or contracts, focus on the actual working relationship. The IRS highlights that worker classification hinges on how tasks are performed and the level of control the business exerts. Regularly review worker classifications using established guidelines and ensure compliance with any stricter state-specific rules. This proactive approach helps maintain compliance and supports effective workforce management.

Keep thorough records of behavioral control, financial arrangements, and the nature of your working relationships. Conduct annual reviews to catch any changes in classification. If you uncover a misclassification, address it promptly. Programs like the Voluntary Classification Settlement Program (VCSP) offer an opportunity to reclassify workers for future periods while receiving partial relief from penalties.

When in doubt, seek advice from a professional or submit Form SS-8 to the IRS for an official determination of a worker’s status. Correct classification not only avoids penalties but also strengthens your relationships with workers and ensures your business operates smoothly. By following these steps, you can confidently manage classifications and safeguard your business’s future.

FAQs

What’s the biggest red flag that a contractor is really an employee?

The most telling sign is whether the business has the right to direct and control how the work is performed. This could involve giving specific instructions, offering training, or closely monitoring the work. When this level of control exists, it usually indicates an employment relationship rather than an independent contractor setup.

Which state’s rules apply if my worker is remote or moves states?

State-specific rules apply to where a worker performs their duties. Tax and compliance requirements for remote work can differ widely depending on the jurisdiction. It’s important to review the tax laws and regulations for the state where the work is being carried out.

How can I fix a worker misclassification without triggering major penalties?

To resolve worker misclassification issues with reduced penalties, the IRS provides the Voluntary Classification Settlement Program (VCSP). This program lets businesses reclassify workers as employees for future tax periods while significantly lowering the penalties usually associated with such misclassification.

Another option is to file Form SS-8, which seeks an official determination of a worker’s status. Additionally, reviewing IRS guidelines on factors like behavioral control, financial control, and the nature of the relationship between the business and the worker can help ensure the reclassification process is handled correctly.