Managing rental properties casually works at first, but as your portfolio grows, risks increase. Transitioning to a formal business structure – like forming an LLC for a rental property – can protect your personal assets and improve your operations. Key signs it’s time to formalize include managing multiple properties, earning higher rental income, and wanting stronger liability protection. An LLC separates personal and business finances, shields you from lawsuits, and offers tax advantages. Pairing this with professional tools like property management software and dedicated bank accounts ensures smoother operations and better financial management. Let’s break down how to make this shift effectively.

When to Formalize Your Rental Property Operations

Deciding when to formalize your rental property operations can be tricky. Some landlords delay the process, while others rush into it too soon. The key lies in spotting the right moments that signal it’s time to shift from casual management to a more structured, business-focused approach. Below are some clear indicators that it might be time to step up your rental management game.

Managing Multiple Properties

Owning just a few rental units might allow you to rely on instinct, but once your portfolio starts growing, those instincts often fall short. As Jake Belding from Buildium puts it:

"When you’re managing a growing portfolio, it’s easy to run on gut feelings… But as you add more doors, that gut feeling gets harder to trust".

The challenges increase quickly – tracking rent payments, handling maintenance requests across multiple locations, and addressing varying tenant needs can get overwhelming. At this stage, data-driven systems become essential. For landlords managing portfolios of 0–100 units, keeping metrics in check is key: aim for a delinquency rate below 5%, unit turnover time of 14 days or less, and a vacancy rate under 7%. Without formal systems to monitor these numbers, small problems can snowball into costly setbacks.

Higher Rental Income and Tax Considerations

As your rental income grows, it’s not just your bank account that notices – so does the IRS. The distinction between operating as a hobby versus a business carries serious tax implications. The IRS evaluates whether you operate as a business based on whether you maintain "complete and accurate books and records" and handle your activities in a "businesslike manner".

If you’re still blending personal and business expenses in the same bank account or neglecting to track deductions, you’re not only risking an audit but also leaving valuable tax benefits on the table. Setting up a dedicated business account is a simple yet crucial step toward proper financial separation, tax compliance, and maximizing deductions.

Legal Liability and Financial Risk

Operating as a sole proprietor can leave your personal assets vulnerable. If a tenant or visitor gets injured on your property and decides to sue, your personal savings, home, and other assets could be at risk. Rocket Lawyer highlights this concern:

"If you are a sole proprietor with liability insurance, risk personal exposure for claims exceeding your policy limits".

Even with insurance, there are limits to coverage. For instance, if a lawsuit results in a $1 million judgment but your policy only covers $250,000, you’re personally on the hook for the remaining $750,000. By formalizing your operations as an LLC, you create a legal barrier – lawsuits target the business entity, not your personal assets. This kind of protection becomes increasingly important as your portfolio expands and your exposure to potential legal claims grows. The next section will dive deeper into the structured protections an LLC provides.

How an LLC Protects Rental Property Owners

An LLC creates a legal shield, separating your personal assets from the risks associated with your rental property business.

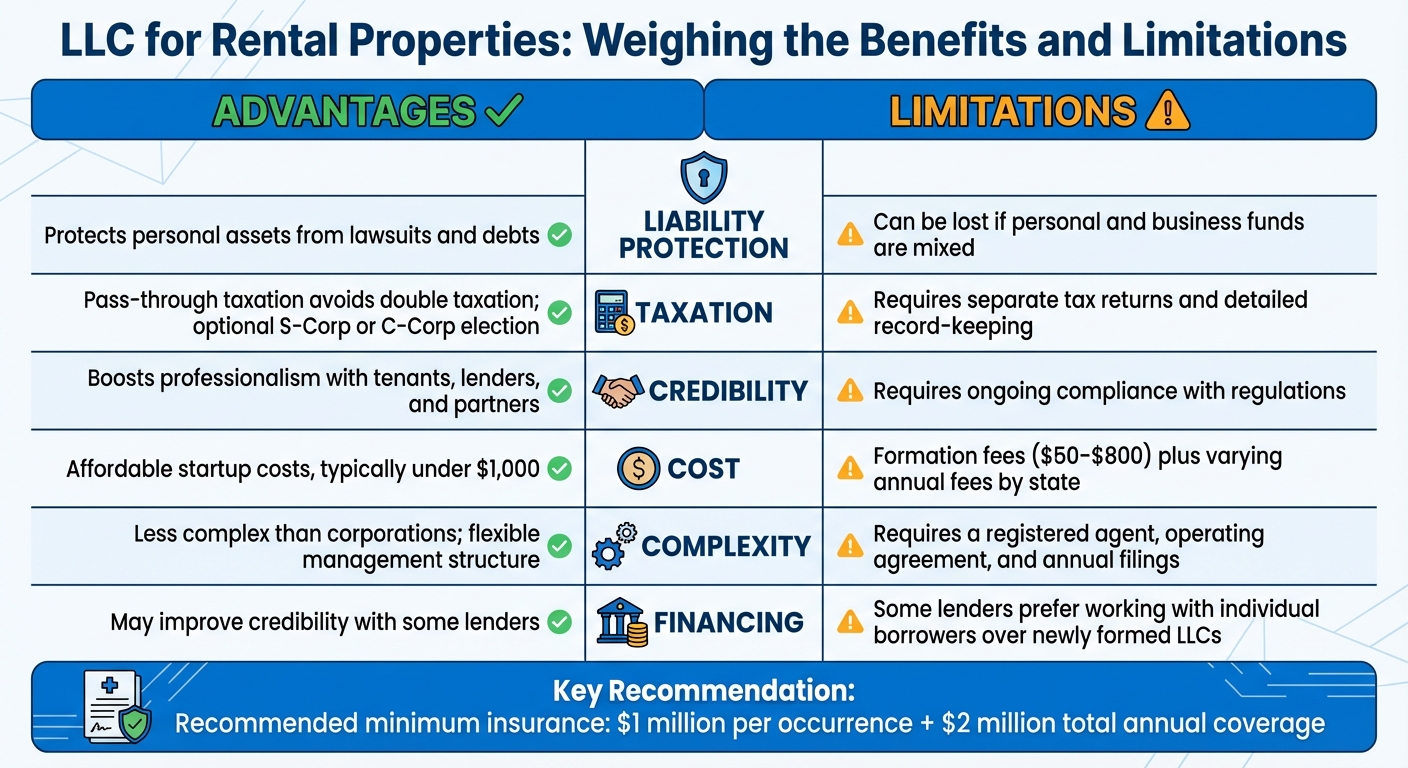

Advantages of an LLC

The primary advantage of forming an LLC is protecting your personal assets. By establishing a legal barrier, an LLC ensures that your personal finances – like your home, savings, or other assets – are not at risk if your rental business encounters lawsuits or debts. As the IRS explains:

"A Limited Liability Company (LLC) is a business structure allowed by state statute… members of the company cannot be held personally liable for the company’s debts or liabilities".

In practical terms, this means legal or financial claims are directed at the LLC, not you personally.

Another key benefit is tax flexibility. By default, LLCs use pass-through taxation, which means profits are taxed only once at the individual level, avoiding the double taxation seen in corporations. Additionally, you can choose to file taxes as an S-Corp or C-Corp by submitting IRS Form 8832, tailoring your tax approach to fit your financial goals.

LLCs also enhance your professional credibility, which can be a game-changer. Operating under an LLC can inspire confidence among tenants, lenders, and business partners. This professional image may help you secure better financing, attract reliable tenants, and negotiate more favorable terms with contractors and vendors.

However, it’s equally important to understand the challenges and responsibilities that come with forming an LLC.

Limitations to Consider

While an LLC offers many benefits, it does come with financial and administrative responsibilities. For starters, there are formation and annual fees. These costs vary by state, with setup fees ranging from $50 to $800, and annual fees adding to your expenses, especially if you manage properties in multiple states.

On the administrative side, you’ll need to handle tasks like appointing a registered agent, obtaining an EIN (Employer Identification Number), and drafting an operating agreement. While not all states require an operating agreement, skipping it could weaken your legal standing if disputes arise.

Maintaining the "corporate veil" – the legal separation between personal and business finances – requires strict discipline. Mixing personal and business funds in the same account can lead courts to "pierce the corporate veil", which would eliminate your liability protection. To avoid this, you’ll need to open a dedicated business bank account and keep meticulous financial records.

It’s also important to note that forming an LLC doesn’t replace the need for landlord liability insurance. Experts recommend maintaining liability insurance with a minimum of $1 million per occurrence and $2 million in total annual coverage. While the LLC structure protects you legally, insurance covers actual claims and legal costs.

LLC Pros and Cons Comparison

Here’s a quick breakdown of the main advantages and limitations of forming an LLC:

| Feature | Advantages | Limitations |

|---|---|---|

| Liability Protection | Protects personal assets from lawsuits and debts | Can be lost if personal and business funds are mixed |

| Taxation | Pass-through taxation avoids double taxation; optional S-Corp or C-Corp election | Requires separate tax returns and detailed record-keeping |

| Credibility | Boosts professionalism with tenants, lenders, and partners | Requires ongoing compliance with regulations |

| Cost | Affordable startup costs, typically under $1,000 | Formation fees ($50–$800) plus varying annual fees by state |

| Complexity | Less complex than corporations; flexible management structure | Requires a registered agent, operating agreement, and annual filings |

| Financing | May improve credibility with some lenders | Some lenders prefer working with individual borrowers over newly formed LLCs |

Whether or not you should form an LLC depends on your specific circumstances, including your risk tolerance, the size of your rental portfolio, and your long-term goals. For landlords managing multiple properties or facing significant liability risks, the benefits of legal protection and tax options often outweigh the costs and administrative work. Carefully weighing these factors will help you make an informed decision about structuring your rental business.

How to Convert Your Rentals into a Formal Business

If you’ve decided to formalize your rental operations, there are three essential steps to follow: registering your LLC, transferring property ownership to the LLC, and setting up solid business systems. Each step helps protect your legal interests and optimize tax benefits.

Registering Your LLC

Start by selecting a name for your LLC that includes "LLC" or a similar designation. Make sure the name is unique by checking your state’s business registry, and register in the state where your property is located.

Next, appoint a registered agent. This person or service will handle legal and tax documents during business hours. While you can act as your own agent, many landlords prefer professional services for privacy and reliability. These services typically cost between $100 and $300 annually. For example, BusinessAnywhere offers registered agent services for $147 per year after an initial free year.

The key legal step is filing the Articles of Organization (or Certificate of Formation) with your state’s Secretary of State. This document includes details like your LLC’s name, address, and registered agent. Filing fees vary by state, ranging from $50 to $800. Additionally, you’ll need to obtain a free EIN (Employer Identification Number) from the IRS for banking and tax purposes. If you’d rather not handle this yourself, services like BusinessAnywhere can assist with EIN applications.

Finally, draft an Operating Agreement. This document outlines ownership stakes, profit distribution, and management responsibilities. Even if your state doesn’t require it, having an Operating Agreement shows that your LLC operates independently, which can help prevent legal disputes.

Once your LLC is officially registered, it’s time to transfer your property titles into the LLC.

Moving Properties into Your LLC

Transferring property titles to your LLC requires coordination with your lender, insurance company, and local authorities. First, check with your lender about any due-on-sale clause that might be triggered by the transfer.

To formalize the transfer, prepare and record a new deed. A Warranty Deed ensures a clear title, while a Quitclaim Deed simply transfers your current interest. For personal transfers to your own LLC, a Quitclaim Deed is usually sufficient. You’ll need to record the deed with your local county clerk’s office; recording fees typically range from $20 to $100.

"If you mix funds, you could lose your liability protection in court (this is called ‘piercing the corporate veil’)."

– David Bitton, Co-founder, DoorLoop

Update your property insurance to list the LLC as the insured party. You’ll also need to notify your tenants about the ownership change. Sending a Landlord Introduction Letter is a good way to explain the transition and provide updated rent payment instructions. While existing leases remain valid, you may want to issue a Lease Amendment to specify that the LLC is now the landlord.

With the property transfer complete, the final step is to establish strong business systems to manage your operations.

Creating Business Systems

Set up dedicated financial and operational systems to ensure smooth business operations. Open a business bank account using your LLC’s EIN and Articles of Organization. A business credit card can also help separate personal and business expenses while building credit for your LLC.

Use accounting software to track income, expenses, and tax deductions. Schedule reminders for annual state filings, franchise taxes, and any required local rental licenses. These systems are essential for maintaining the legal and operational benefits of formalizing your rental business.

Property management software can further streamline your operations by centralizing rent collection, tenant screening, and maintenance requests. This creates a professional experience for tenants and ensures you have the documentation needed for tax and compliance purposes. Tools like BusinessAnywhere’s dashboard can help you manage registered agent services, virtual mailboxes, compliance alerts, and annual report filings – all in one place.

sbb-itb-ba0a4be

Tools and Requirements for Professional Property Management

After setting up your LLC and transferring your properties, the next step is ensuring your business has the right tools to run smoothly. Using professional property management software can simplify tasks like rent collection, maintenance tracking, and lease renewals, saving you a significant amount of time each year.

Property Management Software

To keep up with the demands of a formalized business, digital tools are a must. The right property management software can handle critical tasks automatically. For instance, platforms that offer online rent collection with automatic reminders and late fee enforcement can help maintain steady cash flow without the hassle of chasing checks. Another key feature to look for is integrated tenant screening, which allows you to instantly review credit, criminal, and eviction histories. This can help you avoid costly mistakes – evictions can cost $3,500 or more and take at least four weeks to resolve.

Additionally, having a portal for maintenance requests is crucial. Tenants should be able to submit requests easily, triggering automatic notifications to vendors and tracking progress until completion. This kind of system can prevent minor issues from escalating into expensive repairs. Financial tracking tools within the software can also simplify tax preparation and safeguard your LLC’s liability.

In short, using proven property management software can streamline operations, allowing landlords to grow their portfolios while maintaining a professional and efficient approach.

BusinessAnywhere Services for Landlords

In addition to software, comprehensive service solutions can further reduce your administrative workload. BusinessAnywhere offers a range of services tailored for rental property owners who want to consolidate their management tasks. For example, they provide $0 LLC formation (you only pay state fees), EIN application services for $97, and registered agent services for $147 per year after a free first year.

The virtual mailbox feature is particularly beneficial for landlords managing properties across different states or from afar. Starting at $20 per month, this service includes unlimited mail scanning and global forwarding, ensuring you never miss critical documents like legal notices or tax paperwork. BusinessAnywhere also provides compliance alerts for important filings, such as annual reports and BOIR (Beneficial Ownership Information Report) submissions. BOIR filing through their platform costs just $37.

Compliance and Annual Reporting

To keep your LLC in good standing, you’ll need to stay on top of state and federal reporting requirements. Most states require an annual report to be filed with the Secretary of State, with fees ranging from $50 in some states to as high as $800 in California, which charges an annual franchise tax regardless of your profitability. Missing these deadlines can result in penalties or even the administrative dissolution of your LLC.

The Beneficial Ownership Information Report (BOIR) is a newer federal requirement for small LLCs, filed with FinCEN, to disclose individuals who own or control the company. Staying compliant with this requirement is critical. Additionally, you’ll need to keep track of any local rental licenses and permits, which vary by location. Many property management software platforms include compliance tracking features that send reminders for these recurring obligations, helping you avoid missed deadlines.

Conclusion

Turning your rental properties from a casual side gig into a formal business is about more than just filing paperwork – it’s about safeguarding your personal assets, optimizing tax benefits, and creating a foundation for growth. By forming an LLC, you separate your personal and business finances, providing a layer of legal protection while also improving tax management. This step not only secures your wealth but also prepares you to adopt tools that streamline your operations.

Using efficient systems can make managing your properties much easier. Property management software can handle tasks like rent collection, tenant screening, and maintenance tracking automatically. Keeping business finances separate with dedicated accounts also helps you stay organized and ready for audits. Attorney Christine Mathias from Nolo emphasizes the importance of this structure:

"The larger the rental business, and the lower your tolerance for risk, the more you should consider forming an LLC."

Companies like BusinessAnywhere can further simplify the process. They offer services such as LLC formation (state fees apply), registered agent support, and virtual mailbox options to reduce administrative headaches. Their compliance alerts ensure you stay on top of key filings like annual reports, and their EIN application service helps you get tax-ready quickly.

FAQs

What are the main advantages of setting up an LLC for my rental properties?

Forming a Limited Liability Company (LLC) for your rental properties offers several advantages, starting with protecting your personal assets. By keeping your personal finances separate from your rental business, an LLC ensures that if legal or financial troubles arise, only the LLC’s assets are at stake. Your personal savings, home, and other belongings remain shielded.

An LLC can also make managing taxes easier and might even lower your overall tax liability. Rental income and expenses flow directly to your personal tax return, helping you avoid double taxation. On top of that, you can deduct common business expenses – like mortgage interest, repairs, insurance, and even a portion of home-office costs – directly from your rental income.

Beyond financial benefits, an LLC adds a layer of professionalism to your rental business. You can establish a dedicated business bank account, keeping your finances organized and making it easier to grow your portfolio or bring in partners. This structure not only simplifies operations but also boosts your credibility with lenders and potential investors.

What steps do I need to take to transfer my rental properties into an LLC?

To move your rental properties into an LLC, you’ll need to take a few key steps. First, form an LLC in the state where each property is located. This involves filing the required formation documents, getting an EIN (Employer Identification Number), and drafting an operating agreement. Once the LLC is established, update the property deeds to list the LLC as the new owner.

You should also open a separate bank account for the LLC, revise any leases to name the LLC as the landlord, and keep the business’s financial records separate from your personal finances.

Following these steps not only shields your personal assets but also helps you manage your rental properties more efficiently and professionally.

What tools can help me manage my rental properties more efficiently after setting up a formal business?

Once you’ve set up your rental properties as a formal business, the right tools can make a world of difference in managing them efficiently. For starters, property management software can bring everything under one roof – whether it’s rent collection, lease tracking, or handling maintenance requests. With a single dashboard, you can keep tabs on all your operations without juggling multiple systems.

Then there are accounting tools specifically tailored for rental properties. These can take care of your bookkeeping, track expenses, and even generate tax-ready reports, ensuring your finances stay organized and compliant. On top of that, automation tools can take over repetitive tasks like sending out rent reminders or processing tenant applications, cutting down on manual work and saving you precious time.

With these tools in place, you can simplify your day-to-day operations, work more efficiently, and concentrate on scaling your rental business.

Related Blog Posts

- LLC for Rental Property: Do You Actually Need One to Protect Your Personal Assets?

- How to Title Rental Properties in an LLC Without Blowing Up Your Financing or Insurance

- What Is a Holding Company LLC for Real Estate (and When Should You Form One)?

- The Most Common LLC Mistakes That Let Tenants’ Lawyers Come After Your Personal Assets