Yes, you can transfer a property purchased in your personal name to an LLC, but it requires careful planning to avoid legal, financial, and tax issues. Here’s what you need to know:

- Why Transfer to an LLC?

It protects your personal assets from liabilities tied to the property and can offer privacy by listing the LLC’s name on public records. For rental or investment properties, it’s often a smart move. - Risks to Watch For:

- Due-on-Sale Clause: Most mortgages allow lenders to demand full repayment if ownership is transferred without approval.

- Tax Changes: Some states may reassess property taxes or impose transfer taxes.

- Insurance Gaps: Title and casualty insurance may not automatically transfer to the LLC.

- Loss of Benefits: For primary residences, you could lose tax advantages like the capital gains exclusion or homestead exemptions.

- Steps to Transfer Property to an LLC:

- Form the LLC: File Articles of Organization, get an EIN, and set up a business bank account.

- Prepare the Deed: Draft a Warranty or Quitclaim Deed to transfer ownership.

- Notarize and File the Deed: Record the deed with your county recorder’s office.

- Update Records: Notify your lender, tax assessor, utility companies, and insurance providers.

- Mortgage Considerations:

The mortgage remains in your name even after the transfer. To avoid triggering the due-on-sale clause, communicate with your lender and ensure payments stay current. If needed, refinancing in the LLC’s name may be an option. - Tax and Legal Advice:

Consult a CPA and real estate attorney to navigate tax implications, ensure compliance, and maintain liability protection.

Transferring property to an LLC is doable, but it’s not without risks. Take the right steps, stay informed, and seek professional guidance to protect your investment.

Is Transferring Property to an LLC Right for You?

Deciding whether to transfer your property to an LLC depends on your specific circumstances. While it’s perfectly legal across the United States, the practicality of such a move hinges on factors like the type of property, your mortgage terms, and your financial goals. Let’s break it down.

Legal Requirements for Transferring Property After Closing

Once you’ve weighed the personal advantages, it’s time to look at the legal steps. Transferring property to an LLC post-closing is allowed in all U.S. states. To start, you’ll need to set up an LLC by filing Articles of Organization (or a Certificate of Formation) with your state and designating a registered agent. Filing fees vary widely, ranging from $50 to over $500 depending on the state, and recording fees for the deed are typically around $100, though this can differ by county.

After establishing your LLC, you’ll need to draft a new deed – usually a Warranty Deed or Quitclaim Deed – to transfer the title from yourself (the grantor) to your LLC (the grantee). This deed must be notarized and recorded with your county recorder’s office to make it official. However, keep in mind that about 20% of these transfers face complications due to mortgage clauses.

What to Check Before Making the Move

Your first step? Review your mortgage agreement carefully. Most mortgages include due-on-sale clauses, which give lenders the right to demand full repayment if ownership is transferred. While lenders don’t always enforce this clause, transferring property without their consent could put you at risk. If your loan is with Fannie Mae or Freddie Mac, you can use their online tools to see if a transfer might trigger the clause.

Attorney David J. Willis explains:

"transferring title without lender consent is not a default, not even a technical one"

This means lenders can demand repayment, but they aren’t obligated to.

Also, be aware of state-specific rules. For instance, in California, transferring property to an LLC might lead to a property tax reassessment based on the current market value. On top of that, California imposes an $800 annual franchise tax on all LLCs, regardless of whether they turn a profit.

It’s wise to consult a real estate attorney and tax advisor before proceeding. They can guide you through lender restrictions, state requirements, and potential tax implications, helping you avoid costly mistakes that could undermine your liability protection or result in unexpected expenses.

When Does Transferring Property to an LLC Make Sense?

For investment properties and rentals, transferring ownership to an LLC often makes the most sense. An LLC creates a legal shield, protecting your personal assets – like your home, car, and savings – from lawsuits tied to the property.

If you own multiple investment properties, you might consider placing each one in a separate LLC. This strategy acts as a “firewall,” ensuring that a lawsuit involving one property won’t jeopardize the others. Some investors opt for Series LLCs, which allow multiple properties to be held in separate compartments under a single entity.

Another advantage of LLC ownership is increased privacy. When property is held by an LLC, only the LLC’s name and address appear in public real estate records, keeping your personal details out of view.

However, transferring your primary residence to an LLC is generally not advisable. Doing so could mean losing valuable benefits like the Section 121 capital gains exclusion (up to $250,000 for individuals or $500,000 for married couples), homestead tax exemptions, and possibly mortgage interest deductions. Additionally, the IRS might classify the transfer as a gift, which could trigger gift taxes as high as 40%.

| Factor | Personal Ownership | LLC Ownership |

|---|---|---|

| Liability | Personal assets at risk | Limited to LLC assets |

| Privacy | Owner name on public record | LLC name on public record |

| Taxation | Individual tax returns | Pass-through (default) or S-Corp |

| Homestead Exemption | Available for primary residence | Generally lost |

| Management | Individual control | Governed by Operating Agreement |

If your property is a rental generating income, if liability protection is a concern, or if you’re growing a real estate portfolio, transferring to an LLC could be a smart move. On the other hand, for primary residences or properties with strict mortgage terms, the potential complications might outweigh the advantages.

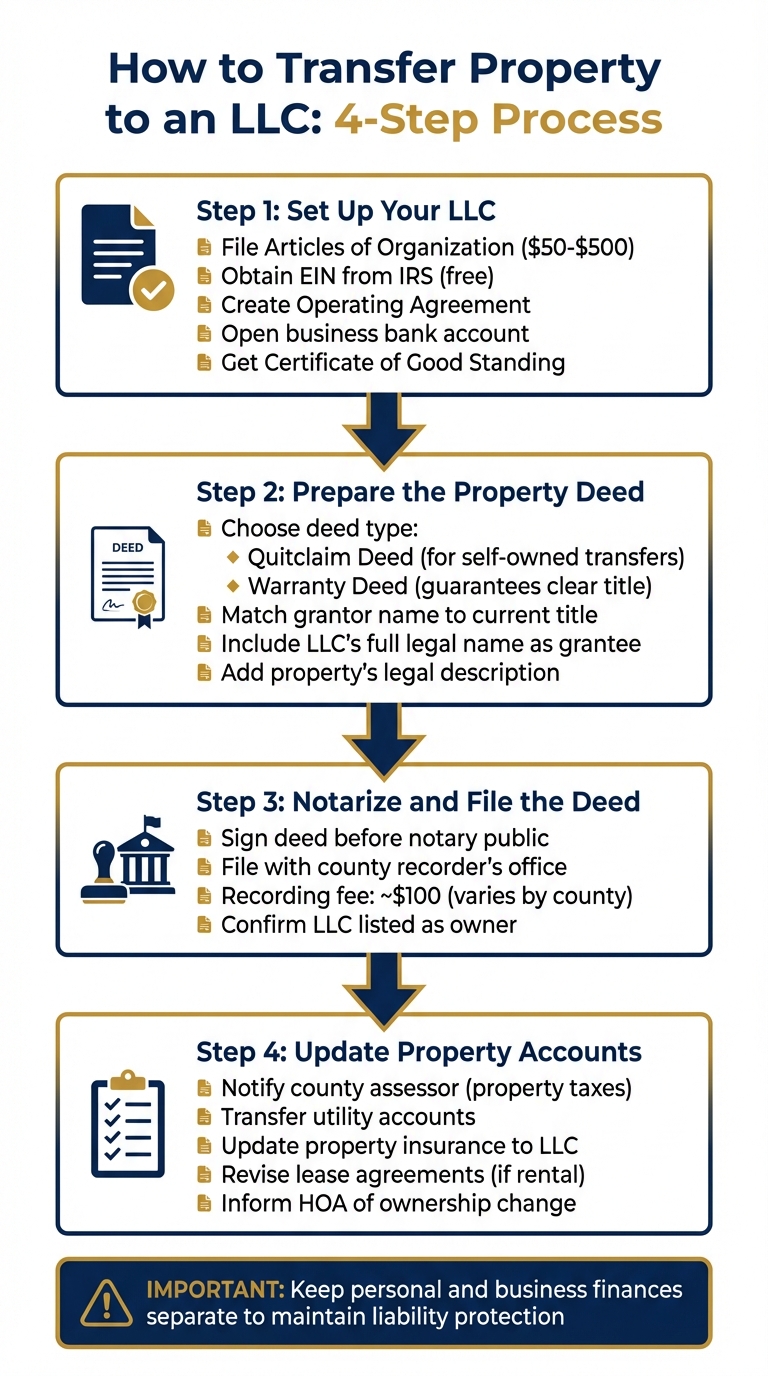

How to Transfer Property to an LLC: Step-by-Step

If you’re ready to transfer property to an LLC, the process typically involves four key steps. Each step requires careful attention to legal details to ensure the transfer is valid and properly documented.

Step 1: Set Up Your LLC and Gather Necessary Documents

Start by filing your Articles of Organization (or Certificate of Formation) with your state to establish your LLC. Filing fees usually range between $50 and $500, depending on where you live. Once your LLC is officially registered, you’ll receive a Certificate of Good Standing, which confirms its legal status.

Next, apply for a free EIN (Employer Identification Number) through the IRS website. You’ll also need an Operating Agreement to outline ownership percentages and management responsibilities within the LLC. Finally, open a business bank account for the LLC. Keeping personal and business finances separate is essential because:

"If you mix funds, you could lose your liability protection in court (this is called ‘piercing the corporate veil’)." – David Bitton, Co-founder, DoorLoop

Step 2: Prepare the Property Deed

Once your LLC is established, you’ll need to draft a deed to transfer ownership. This legal document officially moves the property from you (the grantor) to your LLC (the grantee). The two most common types of deeds are:

- Quitclaim Deed: Best for transferring property you already own, especially for intra-family or self-owned LLC transfers.

- Warranty Deed: Offers more protection to the grantee by guaranteeing a clear title.

"Use a quitclaim deed to transfer only the interest you hold, making it ideal for intra-family or self-owned LLC transfers." – Jane Haskins, Esq., LegalZoom

When completing the deed, make sure your name matches the name on the current property title, and list your LLC’s full legal name as the grantee. Include the property’s legal description and, if required by your state, specify a purchase price or nominal amount.

Step 3: Notarize and File the Deed

After preparing the deed, sign it in the presence of a notary public, as notarization is required in most states. Once notarized, file the deed with your local county recorder’s office or registrar of deeds. This step ensures the transfer is officially recorded and made part of the public record. Filing fees typically cost around $100, but this can vary depending on your county.

Once the deed is filed, confirm that all relevant records now reflect your LLC as the property owner.

Step 4: Update Property Accounts and Notify Relevant Parties

After recording the deed, it’s important to update property-related records and notify all necessary parties to reflect the new ownership. Here’s what you’ll need to do:

- Property Taxes: Notify the county assessor’s office so future tax bills are addressed to your LLC.

- Utilities: Contact utility providers (electric, gas, water, internet) to transfer account ownership to the LLC.

- Insurance: Update your property insurance to list the LLC as the insured entity. If you have title insurance, request an endorsement naming the LLC to maintain coverage.

- Rental Properties: If the property is rented out, revise lease agreements to name the LLC as the landlord and formally notify tenants of the change.

- Homeowners Associations: Inform any homeowners or community associations about the ownership transfer.

When signing documents related to the property in the future, use the format: "[Your Name], Managing Member of [LLC Name]."

Articles of Organization filing fees vary by state.

Handling Mortgage and Lender Issues

Managing mortgages and lender concerns is a critical step when transferring property to an LLC. It ensures you maintain both advantages and disadvantages of an LLC for a rental property regarding liability and tax benefits without running into unexpected hurdles.

How Mortgages Impact LLC Transfers

When you transfer property to an LLC, the mortgage stays in your name. This means you’re still personally responsible for the loan payments, even though the LLC legally owns the property. Here’s where it gets tricky: most residential mortgages come with a due-on-sale clause. This clause allows the lender to demand immediate repayment of the entire loan if the property is transferred without their approval. Ignoring this clause could breach your mortgage agreement.

Lenders often learn about these transfers through updates to the deed, changes in the name on payment checks, or adjustments to the property’s insurance policy. If the lender enforces the due-on-sale clause, you may be required to pay off the entire loan balance within 30 days to avoid foreclosure.

These risks highlight the importance of addressing lender concerns before making any moves.

What Is a Due-on-Sale Clause and How Can You Avoid Triggering It?

The Garn-St. Germain Depository Institutions Act of 1982 offers some protections for specific property transfers, like placing property into a revocable living trust for estate planning purposes. However, these protections don’t extend to LLC transfers. Because an LLC is considered a separate legal entity, even moving a property to your own single-member LLC can activate the due-on-sale clause.

"The Garn-St. Germain Act does not protect LLC transfers. An LLC is a separate legal entity, and a transfer from an individual to their LLC, even a single-member one, can trigger a due-on-sale clause." – Paramus Estate Planning

"The due-on-sale clause means that if the mortgage lender does not approve of the transfer, lenders may demand full repayment immediately." – David C. Johnson, Attorney, Virginia Beach Law Group

That said, many lenders don’t enforce this clause as long as your mortgage payments are up to date. As Anila Rasul, Managing Attorney at ASR Law Firm, points out:

"Most lenders elect not to enforce the clause if the subject loan is current and up to date – it’s not good for business to turn a well-performing loan into a non-performing loan."

However, during times of rising interest rates, lenders may become more aggressive. They might call in older low-interest loans to encourage refinancing at higher rates.

To reduce your chances of triggering the clause:

- Communicate with your lender beforehand. Explain your plans and request written consent. Mention that the transfer is for asset protection and that you’ll remain the majority owner. Interestingly, around 70% of U.S. mortgages are backed by Fannie Mae or Freddie Mac. If your loan was purchased by Fannie Mae after June 1, 2016, they might allow LLC transfers without enforcing the due-on-sale clause, as long as you retain majority ownership.

- Provide a personal guarantee. This reassures the lender that you’ll still be responsible for the loan payments, even after the LLC holds the title.

- Consider using a land trust first. Some property owners transfer their property into a land trust (which may qualify for Garn-St. Germain protections) and then assign the beneficial interest to the LLC. While this adds a layer of privacy, transferring the beneficial interest could still trigger the clause if the lender becomes aware.

When Refinancing in the LLC’s Name Becomes Necessary

If your lender doesn’t approve the transfer or enforces the due-on-sale clause, refinancing might be your only option. This involves replacing your personal mortgage with a commercial loan in the LLC’s name. While this resolves the issue of mismatched ownership and liability, business mortgages come with different terms. You’ll likely face higher interest rates, larger down payment requirements, and more extensive paperwork, such as business plans, LLC financial statements, and tax returns. Even then, lenders often require you to sign a personal guarantee, holding you personally liable if the LLC defaults.

Refinancing also comes with closing costs, so it’s important to weigh the financial impact. For instance, if you currently have a low-interest mortgage, refinancing at today’s higher rates could significantly increase your monthly payments. Compare these costs to the liability protection an LLC provides to decide whether refinancing is worth it. Over time, this move could also help the LLC establish its own credit history, which may benefit your business in the long run.

sbb-itb-ba0a4be

Tax Implications and Compliance Requirements

When transferring property into an LLC, understanding the tax implications is just as critical as addressing legal and lender requirements. This process doesn’t simply change the name on the deed – it can significantly impact your tax obligations. Being aware of these potential changes beforehand can help you avoid unexpected surprises.

Property Tax Reassessment After Transfer

In many counties, transferring property to an LLC is considered a "change in ownership," which can trigger a reassessment of the property’s value. If your property’s market value has increased since you purchased it, this reassessment could lead to a higher annual property tax bill. For instance, in California, retaining at least 50% ownership might help you avoid reassessment.

This transfer can also eliminate personal tax benefits like homestead exemptions. Additionally, a one-time transfer tax, along with recording fees ranging from $50 to $150, may apply.

Before filing the deed, it’s a good idea to contact your local county assessor’s office to determine if transferring the property to a wholly-owned LLC will be considered a "change in ownership" for tax purposes. Some states have "continuity of interest" rules that allow reassessment waivers if the LLC’s ownership structure mirrors the original deed holders.

IRS Reporting and Required Forms

Transferring property into an LLC also affects IRS reporting, depreciation, and asset valuation. For a single-member LLC, the IRS treats the company as a "disregarded entity", meaning you report rental income and expenses on Schedule E (Form 1040). However, you’ll still need to maintain separate financial records using an EIN. If the LLC has multiple members, it’s treated as a partnership, requiring you to file Form 1065, which adds another layer of complexity.

Be cautious of gift tax issues. If you transfer the property to the LLC without receiving payment (consideration), the IRS may classify the transfer as a gift. The federal gift tax can be as high as 40% of the property’s value. Moreover, transferring your primary residence into an LLC means losing the Section 121 exclusion, which allows individuals to exclude up to $250,000 in profit from capital gains tax when selling.

"Prior to any transfer, a CPA should review the transfer for its effects on gain in the short term and long term and the tax treatment of the entity and its members." – Imants Holmquist, LLC

To stay organized, document everything thoroughly. Record the property’s fair market value, original purchase price, and its depreciation schedule in the LLC’s operating agreement. This ensures a clear paper trail for the IRS and preserves the financial separation necessary to protect your liability shield.

Next, let’s explore how transferring property impacts depreciation and cost basis.

How the Transfer Affects Depreciation and Cost Basis

For single-member LLCs, the transfer doesn’t disrupt your depreciation schedule. Since the IRS views the LLC as an extension of you, your cost basis remains unchanged. You’ll continue reporting depreciation on Schedule E, just as you did before the transfer.

For multi-member LLCs, the situation is more complex. The IRS may treat the transfer as either a sale or a partnership contribution, potentially triggering capital gains tax and depreciation recapture. Depreciation recapture taxes prior deductions at a flat rate of 25%.

Single-member LLCs also retain the "stepped-up basis" benefit. This allows heirs to reset the property’s cost basis to its fair market value at the time of your death. The calculation includes the original purchase price, capital improvements, and total depreciation deductions taken over time. Multi-member LLCs, however, don’t automatically get this benefit unless a Section 754 election is made.

| Feature | Single-Member LLC | Multi-Member LLC |

|---|---|---|

| Tax Reporting | Schedule E (Form 1040) | Form 1065 |

| Depreciation Impact | Continues unchanged | May trigger recapture |

| Cost Basis | Carries over from individual | May adjust based on contribution value |

| Stepped-Up Basis | Maintained automatically | Requires Section 754 election |

Properly managing depreciation and cost basis adjustments is vital to protecting the financial benefits of your investment. As a best practice, open a dedicated business bank account for your LLC immediately after the transfer. Mixing personal and business funds can lead to "piercing the corporate veil", which might expose your personal assets to business liabilities. Keep all rental income and depreciation-related expenses completely separate from your personal finances.

Avoiding Common Transfer Problems

Being aware of potential issues ahead of time can help safeguard your investment and preserve your liability protections.

Maintaining Title Insurance and Liability Coverage

One common pitfall during property transfers is the loss of title insurance coverage. Many title insurance policies don’t automatically extend to an LLC after a property is transferred. The key lies in how the policy defines the "insured" party, and older policies often fail to include entities like LLCs as assignees.

A case from 2021 highlights this risk. Soon Han Pak and Chung Huyk Pak purchased a property in 2003 and transferred it to their LLC in 2008 using a quitclaim deed. Years later, when a neighbor claimed an easement on their property, the Paks filed an insurance claim with First American Title. The insurer denied the claim, arguing that the LLC wasn’t the "insured" party under the original policy. The court sided with the insurer, leaving the LLC without coverage.

"Transferring the property by a statutory warranty deed instead of a quit claim deed may have solved the issue in the Pak’s case." – David C. Tingstad, Washington State Business and Real Estate Lawyer, Beresford Booth

To avoid similar problems, reach out to your title insurance company before filing a deed. Request an endorsement to add the LLC as an insured party. If this isn’t possible, consider purchasing a new title insurance policy in the LLC’s name. Additionally, using a warranty deed instead of a quitclaim deed can help preserve coverage, as it guarantees a clear title and maintains the ownership chain.

Don’t forget to update your casualty and liability insurance policies. Most homeowner policies can’t transfer to an LLC and will need to be replaced with commercial coverage issued in the LLC’s name.

Common Mistakes in Deed Preparation and Filing

Even small errors in deed preparation can lead to major legal headaches. For example, the grantor’s name and the full legal description of the property must match the original deed exactly to avoid title disputes.

Deeds must also meet state-specific requirements for signatures, witnesses, and notarization. Some states even require the grantee (the LLC) to sign the deed. Be sure to check with your county recorder’s office for local rules on witness counts, document margins, and any additional forms. For instance, in California, transfers often require Form BOE-502-A (Change in Ownership Statement) to determine if a property tax reassessment applies.

"The main problem with [using a quitclaim deed] is that it nullifies the title policy obtained during the initial purchase of the property under the owner’s personal name." – UpCounsel

Another common mistake is failing to specify the "consideration" (the value exchanged or purchase price) on the deed. If no money changes hands, some states require a minimum stated value or a "love and affection" clause for the transfer to be valid. Once the deed is recorded, it’s crucial to maintain financial separation by depositing all rental income into an LLC-specific bank account. This helps protect your liability shield and prevents "piercing the corporate veil."

If complications arise, seeking professional guidance is essential.

When to Hire Attorneys and Tax Professionals

Certain situations call for expert assistance to ensure a smooth transfer and protect your liability shield. For instance, if your property has an active mortgage, consult an attorney to review the "Due on Sale" clause. This clause could allow the lender to accelerate the loan if the property is transferred. Attorneys can negotiate with lenders or clarify that there’s "no change in beneficial ownership" to avoid triggering the clause.

"Transferring property to an LLC may trigger [the due on sale] clause unless your lender has expressly waived it or provided written consent. Do not skip this step." – Faisal Moghul, Esq., Managing Partner, Fox & Moghul

Tax professionals are equally important when dealing with capital gains tax, depreciation recapture, or gift tax implications, which can reach up to 40% if the LLC doesn’t pay for the property. Attorneys can also draft operating agreements and member resolutions to ensure corporate formalities are followed, which is key to maintaining liability protections.

"Failing to follow formalities can result in ‘piercing the corporate veil,’ allowing plaintiffs to access your personal assets." – Ada Danelo, Partner, Summit Law Group

If the property is tenant-occupied, legal help is crucial for assigning leases to the LLC and notifying tenants. Professionals can also ensure compliance with state-specific rules on property tax reassessments and real estate transfer taxes. While hiring experts may cost a few hundred to a few thousand dollars, this expense is small compared to the financial and legal risks of errors.

Conclusion

Transferring property from your personal name to an LLC is entirely doable, but it demands careful planning and strict adherence to legal requirements. The process involves several key steps: forming your LLC, preparing and recording the appropriate deed, updating your insurance policies, and keeping your personal and business finances completely separate. Each of these steps must be handled with precision to avoid complications.

There are also risks to keep in mind. For instance, most mortgages include a due-on-sale clause, which could allow your lender to demand full repayment if you transfer the property without their approval. Failing to update your title or casualty insurance could leave you unprotected. Tax implications vary by state, too – some states might reassess your property taxes or impose additional fees, such as California’s $800 annual franchise tax.

"Any transfer should be reviewed by both a CPA and a real estate attorney prior to recording a deed and excise tax affidavit to avoid irreparable harm." – Hart & Associate

Seeking professional advice is crucial. Consulting with attorneys and CPAs can help you navigate potential pitfalls and ensure everything is done correctly. While these services come with a cost, they pale in comparison to the financial and legal risks of skipping this step.

The bottom line? Treat your LLC as a completely separate legal entity from the very beginning. Open a dedicated business bank account, deposit all rental income into that account, sign documents as the managing member, and never mix personal and business funds. Following these practices will help maintain the corporate veil and protect your personal assets. These steps are essential for preserving your liability shield. This protection is a primary reason many choose an LLC vs sole proprietorship for their investments.

FAQs

What tax implications should I consider when transferring property to an LLC?

Transferring property from personal ownership to an LLC can come with tax consequences, depending on how the IRS views the transaction. If the transfer is considered a capital contribution, it’s typically non-taxable. However, you’ll need to document the property’s fair market value and keep detailed records for future depreciation and potential gains. On the flip side, if the IRS treats the transfer as a sale, you might have to report and pay taxes on any capital gains at the time of the transfer.

The tax treatment also depends on how the LLC itself is taxed. If the LLC is classified as a disregarded entity or a partnership, income and losses will pass through to your personal tax return, allowing you to retain the benefits of pass-through taxation. But if the LLC is taxed as a C-corporation, you could encounter double taxation and might lose certain personal deductions, such as mortgage interest. To prevent unexpected tax issues, make sure to properly document the transfer with a deed or bill of sale and seek guidance from a tax professional tailored to your situation.

How can I transfer property to an LLC without triggering the due-on-sale clause?

When transferring property to an LLC, it’s crucial to avoid activating the due-on-sale clause in your mortgage agreement. Start by seeking written approval from your lender. In some situations, you might be eligible for an exemption under the Garn-St. Germain Act. For instance, transferring the property to a revocable living trust while keeping yourself as the beneficiary can help you comply with mortgage terms and prevent issues with your lender. To handle this process smoothly and minimize risks, consult a legal or financial expert for tailored guidance.

Should I transfer my primary residence to an LLC?

Transferring your primary residence to an LLC is generally not a good idea. Doing so could activate due-on-sale clauses in your mortgage, potentially causing problems with your lender. On top of that, it might lead to tax complications and provides limited liability protection for a home you live in. This is because personal use of the property often cancels out the asset protection benefits typically associated with an LLC.

It’s always wise to consult a qualified attorney or accountant before making such a move. They can guide you through the legal, financial, and tax considerations unique to your situation, helping you make the best decision for your circumstances.

Related Blog Posts

- LLC for Rental Property: Do You Actually Need One to Protect Your Personal Assets?

- How to Title Rental Properties in an LLC Without Blowing Up Your Financing or Insurance

- Can You Make Your Existing Real Estate LLC Anonymous, or Do You Need to Start Over in a Privacy State?

- From Side Hustle Landlord to Real Business: When It’s Time to Treat Your Rentals Like a Company