If you’re a U.S. citizen, green card holder, or resident alien with foreign financial accounts totaling over $10,000 at any point in the year, you need to file an FBAR (FinCEN Form 114). This isn’t a tax form – it’s a report to the U.S. Treasury to disclose foreign accounts. Failure to file can result in penalties up to $16,117 per violation for non-willful cases or 50% of the account balance for willful violations.

Key points for digital nomads:

- Threshold: Combined foreign account balances exceeding $10,000 trigger the filing requirement.

- Accounts to report: Includes checking, savings, brokerage accounts, fintech wallets (e.g., Wise, PayPal), and accounts with signature authority.

- Deadlines: April 15 (automatic extension to October 15).

- Penalties: Non-willful violations can cost $16,117 per form; willful violations are much higher.

To file, use the FinCEN BSA E-Filing System. You’ll need account details, peak balances, and currency conversions using the Treasury’s year-end exchange rate. If you’ve missed filings, the IRS offers programs to catch up and avoid hefty penalties. Regular tracking and professional help can simplify compliance. For a comprehensive solution, consider using a Digital Nomad Kit to manage your global operations.

Who Must File FBAR as a Digital Nomad?

If you’re a U.S. person and the combined value of all your foreign financial accounts exceeds $10,000 at any point during the year, you’re required to file an FBAR (Report of Foreign Bank and Financial Accounts) [4].

Who qualifies as a U.S. person? This includes U.S. citizens (even dual or accidental citizens), green card holders, and resident aliens who meet the Substantial Presence Test. As Ipanema Partners aptly explains:

"If you’re a US Person, your reporting obligations follow you everywhere. Doesn’t matter where you live, where you earn your money, or how long it’s been since you set foot in the country." [5]

The $10,000 threshold applies to the total maximum value across all accounts. This means even if no single account hits $10,000, the cumulative balance could still require reporting [4].

You also need to report accounts where you hold signature authority – the ability to manage or direct funds – even if you don’t own the account. For example, managing a foreign business account with $500,000 on behalf of your employer would still need to be reported on your personal FBAR [4].

It’s worth noting that about 62% of Americans filing from abroad owe no federal income tax, yet FBAR reporting still applies to them [5]. Keep in mind, the FBAR is informational only – it doesn’t calculate or impose any tax liability.

Account Types That Require FBAR Reporting

Not all foreign assets need to be reported – only financial accounts. Here’s a breakdown of what must be included:

| Account Category | Specific Examples to Report |

|---|---|

| Standard Banking | Checking, savings, money market, and fixed-term deposits (CDTs) |

| Investment | Brokerage accounts, mutual funds, and securities accounts |

| Retirement/Insurance | Foreign pension plans (e.g., UK SIPPs, Canadian RRSPs) and life insurance with cash surrender value |

| Business/Other | Business accounts (if >50% ownership or signature authority), cooperative accounts, and fintech wallets (Wise, Revolut, PayPal) |

For joint accounts, report the full value even if you share ownership. Additionally, owning more than 50% of a foreign business entity means you must report its foreign accounts on your personal FBAR [4].

Some assets don’t require reporting, such as foreign real estate, physical precious metals, or cash stored in a safe deposit box. Similarly, accounts held in U.S. military banking facilities, IRAs, and tax-qualified U.S. retirement plans are exempt [4].

Challenges Specific to Digital Nomads

Digital nomads face unique hurdles when it comes to tracking and reporting foreign accounts. Constant relocation often means juggling multiple accounts across various countries, each with different currencies and reporting standards.

One major challenge is currency conversion. You’re required to convert the maximum account values to USD using the U.S. Treasury’s official Year-End Exchange Rate for December 31 of the reporting year [4].

Another complication comes from international fintech platforms like Wise, Revolut, or PayPal. If these platforms are based outside the U.S., their digital wallets count as foreign financial accounts and must be included in your total.

Tax professional Chip Moreno frequently encounters confusion among expats:

"I’ve helped dozens of expats navigate FBAR filing, and the most common thing I hear is: ‘I had no idea I was supposed to report that.’" [4]

On top of this, digital nomads may face challenges related to their tax home. While this primarily impacts eligibility for the Foreign Earned Income Exclusion (FEIE), frequent moves without establishing a fixed base could lead the IRS to determine that your tax home remains in the U.S. [7]. Regardless of your tax home status, the FBAR requirement applies as long as the $10,000 threshold is met.

How to File FBAR: Step-by-Step Process

To file your FBAR, use the FinCEN BSA E-Filing System. This is an entirely online process – no paper forms required – and the system will guide you through each step.

Information You Need Before Filing

Before you start, make sure you have the following details ready:

- Personal Information: This includes your legal name (as it appears on your tax return), Social Security Number (SSN) or Individual Taxpayer Identification Number (ITIN), date of birth, and current mailing address. If you reside abroad, foreign addresses are acceptable.

- Account Details: For each foreign account, gather:

- The account number (or another identifier if no number exists).

- The type of account (e.g., bank, securities, or other).

- The full name and physical address of the financial institution, including its city and country.

- Maximum Account Value: Identify the highest balance the account reached during the calendar year – not just the year-end balance. Use your monthly or quarterly statements to find this peak. For joint accounts, report the total balance, not just your portion.

- Ownership Status: Specify whether you own the account individually, jointly, or if you only have signature authority over it.

Once you’ve gathered all this information, you’re ready to file.

Using the FinCEN BSA E-Filing System

Access the filing system at bsaefiling.fincen.treas.gov and select "File FinCEN 114". You can submit as a guest or create an account to save your progress and track submissions.

- Choose "Individual" as your filer type if you’re filing for yourself or jointly with a spouse.

- Enter your personal details in the designated fields.

- Move on to the account details section and input each account’s:

- Institution name and address.

- Account number and type.

- Maximum balance in the account’s original currency.

Convert foreign balances to U.S. dollars using the Treasury Department’s official exchange rate for December 31 of the reporting year. Tax professional Mel Whitney advises:

"You must use the Treasury Department’s Year-End Exchange Rate for December 31, 2025, to convert any foreign currency amounts to USD – even if your account hit its peak value at a different time of year." [10]

After entering all accounts, electronically sign the form and submit it. Save the BSA ID number shown on the confirmation screen – this is your proof of filing. Download and keep both the confirmation and the final PDF for your records.

How to Track Foreign Account Balances

It’s crucial to monitor your foreign accounts regularly, as the $10,000 threshold applies to the aggregate value of all accounts, even if the spike is temporary.

- Quarterly Monitoring: Review your accounts every three months. Many banks provide monthly or quarterly statements showing daily or end-of-month balances. Identify any periods where balances spiked.

- Foreign Currency Accounts: Use a simple spreadsheet to track peak balances in the local currency. You don’t need to convert these to USD until filing time, but keeping a record of local peaks will make the process easier.

- Digital Nomad Tools: If you use platforms like Wise, Revolut, or Payoneer, download transaction histories and balance reports. These platforms often allow you to export data in CSV format, helping you pinpoint maximum balances across multiple currencies.

Keep digital copies of your statements, peak balance records, and filing confirmations for at least five years. Use a secure cloud storage solution to ensure access from anywhere. Regular tracking and organization will simplify the filing process and help you stay compliant.

FBAR Filing Deadlines and Extensions

Once you understand what needs to be reported and how to do it, the next step is knowing the deadlines and any extensions available.

Standard FBAR Due Dates

The FBAR filing deadline falls on April 15 of the year after the calendar year you’re reporting. For example, if you’re filing for 2025, your FBAR is due on April 15, 2026. However, all filers – including digital nomads – automatically receive a six-month extension, pushing the deadline to October 15.

Unlike federal income tax returns, which require filing Form 4868 to request an extension, the FBAR extension is automatic. If you miss the April 15 deadline, you still have until October 15 to file without incurring penalties. As Chip Moreno, an expert in expat taxes, explains:

"The October 15 extension is automatic – you don’t need to file any form or request it. If you miss April 15, you still have until October 15 with no penalty." [11]

There is one exception: if you have only signature authority (and no financial interest) over an account, the FBAR deadline for 2025 extends further to April 15, 2027.

FBAR, FATCA, and Tax Return Deadlines Compared

Understanding how FBAR deadlines align with other reporting obligations can help streamline your planning. Here’s a quick breakdown of the deadlines for U.S. citizens living abroad:

| Form | Initial Deadline | Automatic Extension | Final Deadline (with Form 4868) |

|---|---|---|---|

| FBAR (FinCEN 114) | April 15 | October 15 (automatic) | October 15 |

| FATCA (Form 8938) | April 15 | June 15 (for expats) | October 15 |

| Income Tax Return | April 15 | June 15 (for expats) | October 15 |

Since FATCA (Form 8938) is filed as part of your income tax return, its deadlines align with your tax filing schedule. On the other hand, the FBAR is managed separately by the Treasury Department through FinCEN, which is why it benefits from its own automatic extension process.

Common FBAR Mistakes and How to Avoid Them

Navigating FBAR rules can be tricky. Here’s a breakdown of common mistakes and how to steer clear of them.

Misunderstanding When Filing Is Required

One common misconception is assuming that if you owe no U.S. taxes, you don’t need to file an FBAR. Many digital nomads use the Foreign Earned Income Exclusion to reduce or eliminate their tax liability and mistakenly think this exempts them from FBAR reporting. That’s not true. As Katelynn Minott, CPA and CEO of Bright!Tax, explains:

"Your tax return reports your income. Your FBAR reports your money’s location. If you’ve got both, you need to file both." [12]

The FBAR filing requirement is based solely on whether your foreign accounts collectively exceeded $10,000 at any point during the year – not on whether you owe taxes. Even if your taxable income is zero, you must file if your foreign accounts meet the threshold. Keep in mind that the $10,000 limit applies to the combined total of all your foreign accounts [4][12].

Now, let’s look at how brief spikes in your account balances can complicate compliance.

Overlooking Brief Threshold Crossings

Digital nomads often transfer funds between accounts for business expenses, client payments, or currency exchanges. These transfers can temporarily push your total foreign account balance above $10,000 – triggering the FBAR filing requirement for the entire year, even if it happens for just one day.

For example, imagine you hold $8,000 in one account and transfer $6,000 from another account before making a withdrawal. Your aggregate balance briefly shows $14,000. Even though the funds weren’t “doubled,” that momentary spike means you must file an FBAR.

To avoid this mistake, track the maximum account value for each account throughout the year – not just the December 31 balance. Use monthly statements to identify any brief peaks. Also, remember to convert foreign currency amounts using the official December 31 exchange rate [4][6].

This brings us to another common area of confusion: distinguishing FBAR from FATCA.

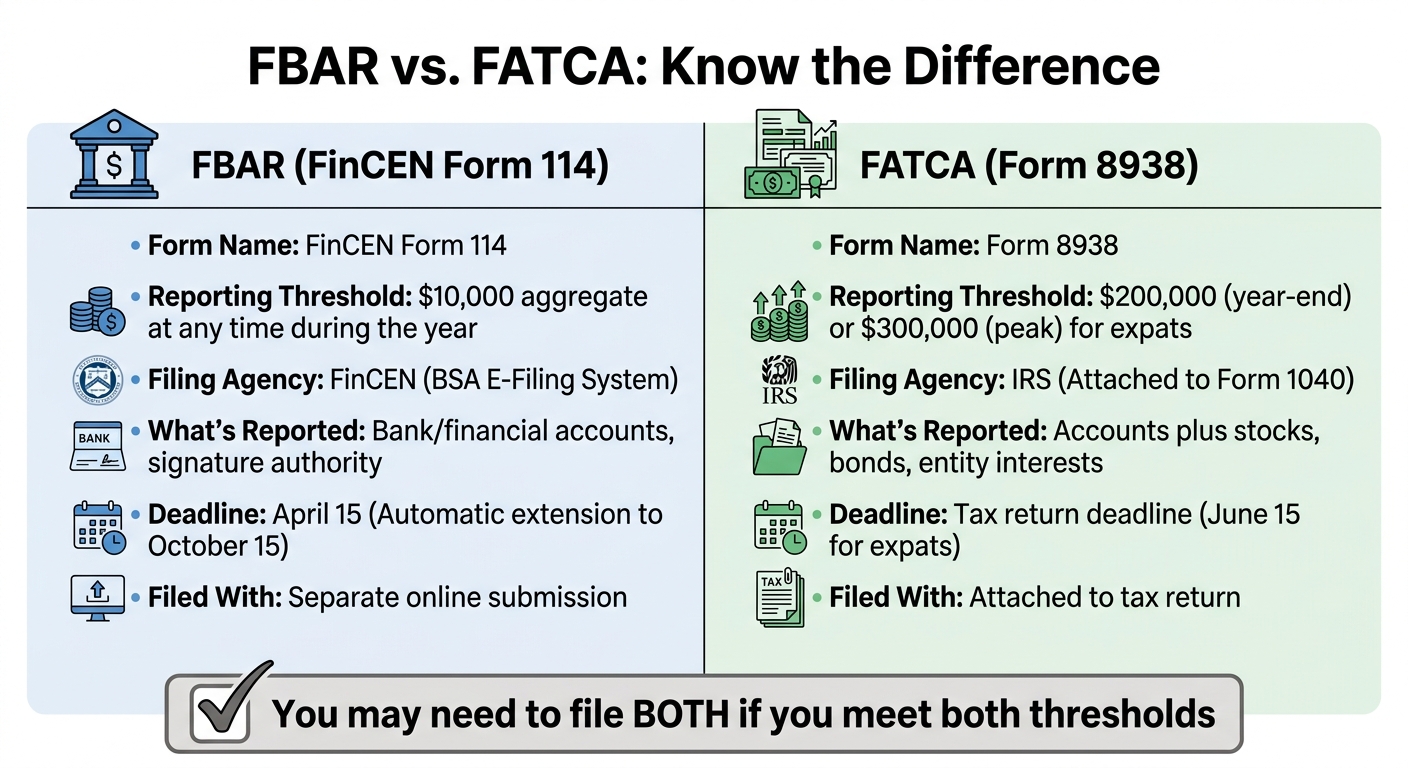

Confusing FBAR with FATCA

FBAR and FATCA (Form 8938) are often mixed up, but they’re not the same. Each has different thresholds, purposes, and filing agencies, and misunderstanding these differences can lead to filing errors or missing forms entirely.

Here’s the key distinction: FBAR focuses on accounts – bank accounts, brokerage accounts, and even accounts where you have signature authority. FATCA, on the other hand, covers assets – including accounts, foreign stocks, bonds, and ownership interests in foreign entities.

For expats, the FBAR threshold is $10,000 in aggregate at any point during the year. FATCA’s threshold is much higher: $200,000 on December 31 or $300,000 at any time during the year (for single filers) [3][4].

The filing process is also different. FBAR is submitted to FinCEN via the BSA E-Filing System, while FATCA (Form 8938) is attached to your tax return and filed with the IRS. If you meet both thresholds, you’ll need to file both forms [3][4].

Here’s a quick comparison to clarify:

| Feature | FBAR (FinCEN Form 114) | FATCA (Form 8938) |

|---|---|---|

| Reporting Threshold (Expats) | $10,000 aggregate at any time [4] | $200,000 (year-end) or $300,000 (peak) [4] |

| Filing Agency | FinCEN (BSA E-Filing System) [6] | IRS (Attached to Form 1040) [6] |

| Scope | Bank/financial accounts, signature authority [4] | Accounts plus stocks, bonds, entity interests [3] |

| Deadline | April 15 (Auto-extension to Oct 15) [6] | Tax return deadline (June 15 for expats) [3] |

It’s worth noting that many digital nomads may have an FBAR obligation without a FATCA obligation, as their foreign accounts exceed $10,000 but remain well below FATCA’s $200,000 threshold.

sbb-itb-ba0a4be

FBAR Penalties and How to Fix Past Mistakes

Understanding FBAR penalties and how to correct past mistakes is essential for staying compliant, especially for digital nomads managing multiple foreign accounts. Failing to file an FBAR can lead to steep penalties, but the IRS provides clear options to address errors – particularly if you act before an investigation begins.

Non-Willful vs. Willful FBAR Violations

The IRS distinguishes between unintentional mistakes and deliberate evasion. A non-willful violation happens when someone fails to file due to negligence or oversight rather than intentional disregard. As Chip Moreno explains:

"Non-willful means your failure to file was due to negligence, inadvertence, or an honest mistake – not intentional disregard." [15]

For non-willful violations, the penalty can go up to $16,536 per annual FBAR form. Following the Supreme Court’s decision in Bittner v. United States, this penalty is assessed per form, not per account [13].

Willful violations, however, are much more severe. Penalties can reach the higher of $165,353 or 50% of the account’s highest balance per year. In cases of fraud or tax evasion, criminal charges may also apply, including fines of up to $250,000 and 5 years in prison – or as much as $500,000 and 10 years if connected to other criminal activity [13]. The IRS typically has six years from the filing deadline to assess these penalties [15].

To address these violations, the IRS has introduced specific amnesty programs designed to help taxpayers correct late or missed filings.

Programs for Late or Corrected Filings

If you’ve missed filing FBARs, the IRS offers amnesty programs that can reduce or even eliminate penalties for those who come forward voluntarily. These programs are particularly helpful for digital nomads, who often juggle multiple foreign accounts and complex reporting requirements.

The Delinquent FBAR Submission Procedures (DFSP) is an option if all your foreign income is already reported on your tax returns but you failed to file FBARs. For non-willful violations, this program generally results in no penalties. To qualify, you must submit FBARs for the past six years and include a reasonable cause statement explaining why the filings were missed – such as relying on a tax preparer who didn’t inform you of the requirement.

If you also have unreported foreign income, the Streamlined Filing Compliance Procedures may be a better fit. This program requires filing six years of FBARs along with three years of amended tax returns. For digital nomads living abroad, non-willful violations typically incur no penalty. However, U.S.-based taxpayers may face a 5% miscellaneous offshore penalty. As Katelynn Minott, CPA and CEO of Bright!Tax, puts it:

"If your situation includes foreign income you didn’t report, you’ll likely need to look at Streamlined Filing Compliance Procedures instead. In other words: this path is for taxpayers who got the reporting wrong, not the income." [14]

Here’s a quick comparison of the two programs:

| Feature | Delinquent FBAR Submission Procedures | Streamlined Filing Compliance Procedures |

|---|---|---|

| Best For | Missed FBARs only (all income reported) | Missed FBARs and unreported income |

| FBARs Required | Past 6 years | Past 6 years |

| Tax Returns Required | None (must be current) | Past 3 years (amended) |

| Penalty (Expats) | $0 | $0 (if non-willful) |

| Penalty (U.S. Residents) | $0 | 5% miscellaneous offshore penalty |

| Key Document | Reasonable Cause Statement | Form 14653 (Certification of Non-Willfulness) |

These programs are only available if the IRS hasn’t already started an audit or investigation. Simply filing late FBARs without using one of these programs – known as "quiet disclosure" – is strongly discouraged, as it can lead to further scrutiny.

Given the risks, many digital nomads choose to work with professionals to navigate these processes. Costs typically range from $300 to $600 for DFSP filings or $1,500 to $3,500 for the Streamlined Filing Compliance Procedures, but the peace of mind is often worth the expense.

It’s also worth noting that the IRS now uses AI tools, such as the "CI-FIRST" initiative, to identify unreported foreign accounts and flag questionable filings. This makes voluntary compliance more important than ever.

Practical Tips to Simplify FBAR Filing

Filing an FBAR might seem daunting, but with consistent organization and the right tools, it can become a manageable annual task. Understanding FBAR exemptions for international entrepreneurs can also help determine if you need to file at all. For digital nomads, setting up efficient systems throughout the year is key to staying on top of compliance while focusing on your business.

Maintain Complete Records

Good recordkeeping is the backbone of FBAR compliance. For five years, hold onto detailed records for each account, including:

- Account name and number

- Full name and address of the foreign financial institution

- Account type

- The highest balance the account reached during the year [16]

It’s important to note that FBAR reporting is based on the account’s peak balance at any point during the year – not just the balance on December 31.

To simplify this process, save digital copies of monthly statements as you receive them. A dedicated cloud storage folder labeled by year makes it easy to organize and review these records. This way, identifying peak balances during filing season becomes less of a hassle [4][16].

Additionally, keep a separate file with the exact legal name and branch address of each foreign bank. This information is required when completing FinCEN Form 114 [4][1]. If you have signature authority over business accounts (even if the funds aren’t yours), those accounts must also be documented and reported [4][9].

Use Financial Tracking Software

Manually managing multiple foreign accounts – especially across currencies – can be time-consuming and prone to errors. Financial tracking software can automate much of the work, making it easier to monitor accounts and ensure compliance.

These tools are particularly useful for:

- Tracking the $10,000 threshold across all accounts, including digital wallets [2][4]

- Logging peak balances throughout the year, so you’re not scrambling to find this information later

Currency conversion is another area where software can save time. All foreign account balances must be converted to USD using the Treasury Reporting Rates of Exchange for December 31 of the reporting year [16][2]. As the IRS explains:

"Filers figure the greatest value in the currency of the account. If not already in U.S. dollars, they convert that value into U.S. dollars using the Treasury Bureau of the Fiscal Service exchange rate on the last day of the calendar year." [16]

Good tracking software applies these rates automatically, ensuring accuracy and compliance. It also serves as a centralized hub for storing account details, peak balances, and other essential information. For particularly complex situations, expert advice can complement these tools to further ease the process.

Work with Professional Services

When dealing with multiple foreign accounts across different jurisdictions, professional assistance can simplify the complexities. For digital nomads managing U.S. business entities alongside personal foreign accounts, things can get tricky – especially when dealing with business accounts, foreign corporations, or trusts.

Services like BusinessAnywhere cater to remote entrepreneurs, offering bookkeeping, compliance support, and tax filing assistance. Their platform consolidates these services into a single dashboard, accessible anytime, making it easier to handle both FBAR requirements and U.S. business obligations.

Professional help is particularly beneficial if you’ve missed filings, manage numerous international accounts, or need to coordinate with FATCA reporting [4][3]. As Chip Moreno, a tax consultant at FileAbroad, points out:

"I’d recommend working with a professional if: You have many accounts across multiple countries; You have complex ownership structures (trusts, foreign corporations, partnerships); You’ve missed prior years." [4]

While private consultations with expat tax specialists typically cost around $377 for a 30-minute session [2], the accuracy and peace of mind they provide can be well worth the expense – especially when non-willful penalties can reach $16,117 per account [4].

Conclusion

Filing the FBAR isn’t just a good idea – it’s a legal obligation for U.S. citizens, green card holders, and resident aliens with foreign accounts totaling over $10,000 at any time during the year. With over 110 countries now sharing account information with the IRS under FATCA agreements, failing to report these accounts is increasingly likely to be detected [8]. Penalties for non-compliance are steep, with fines for non-willful violations often exceeding $16,000 per report and even harsher penalties for willful violations [8][4].

Fortunately, staying compliant doesn’t have to be complicated. Monitor your account balances carefully, keep detailed records for at least five years, and take advantage of the automatic extension to October 15 if you miss the April filing deadline [4][8]. As tax expert Deborshi Choudhury explains:

"The Foreign Bank Account Report isn’t a tax form. You’re not calculating any taxes owed here. It’s simply reporting your foreign financial accounts to stay on the right side of US compliance rules" [2].

For digital nomads or entrepreneurs managing U.S. business entities and multiple foreign accounts, tools like BusinessAnywhere simplify the process. These platforms combine bookkeeping, compliance support, and tax filing services into one dashboard, making it easier to stay organized and meet deadlines.

If your situation involves more complex factors – like ownership of foreign entities, signature authority over business accounts, or missed filings – consider seeking professional advice. A consultation with an expat tax specialist, which typically costs about $377 for 30 minutes, can provide tailored guidance [2]. Additionally, the IRS offers amnesty programs like the Streamlined Filing Compliance Procedures to help those who need to catch up on missed filings [4][8].

FAQs

Does a quick balance spike over $10,000 mean I must file?

If the total balance of all your foreign accounts goes over $10,000 at any point during the year – even for just a moment – you’re required to file an FBAR. A quick spike above this amount doesn’t exempt you from the filing requirement. It’s the highest balance during the year that matters, not how long it stays there.

Do Wise, Revolut, or PayPal balances count for FBAR?

If you have balances in accounts like Wise, Revolut, or PayPal, you might need to report them on an FBAR (Foreign Bank and Financial Accounts Report). This applies if the total value of all your foreign financial accounts exceeds $10,000 at any point during the year. Be sure to carefully review FBAR requirements to understand your reporting responsibilities.

What should I do if I missed FBARs for past years?

If you didn’t file FBARs for past years, the Delinquent FBAR Submission Procedures offer a way to catch up without facing penalties – as long as you meet certain conditions. These include reporting all foreign income accurately and ensuring you’re not currently under audit.

You can submit up to six years of late FBARs electronically through FinCEN’s BSA E-Filing System. Be sure to include a statement explaining why the filings were delayed. This option is generally meant for cases involving non-willful violations.