Understanding digital product taxes across U.S. states is complex. Tax rules vary widely, with some states taxing digital goods like e-books, software, and streaming services, while others offer full exemptions. Here’s what you need to know:

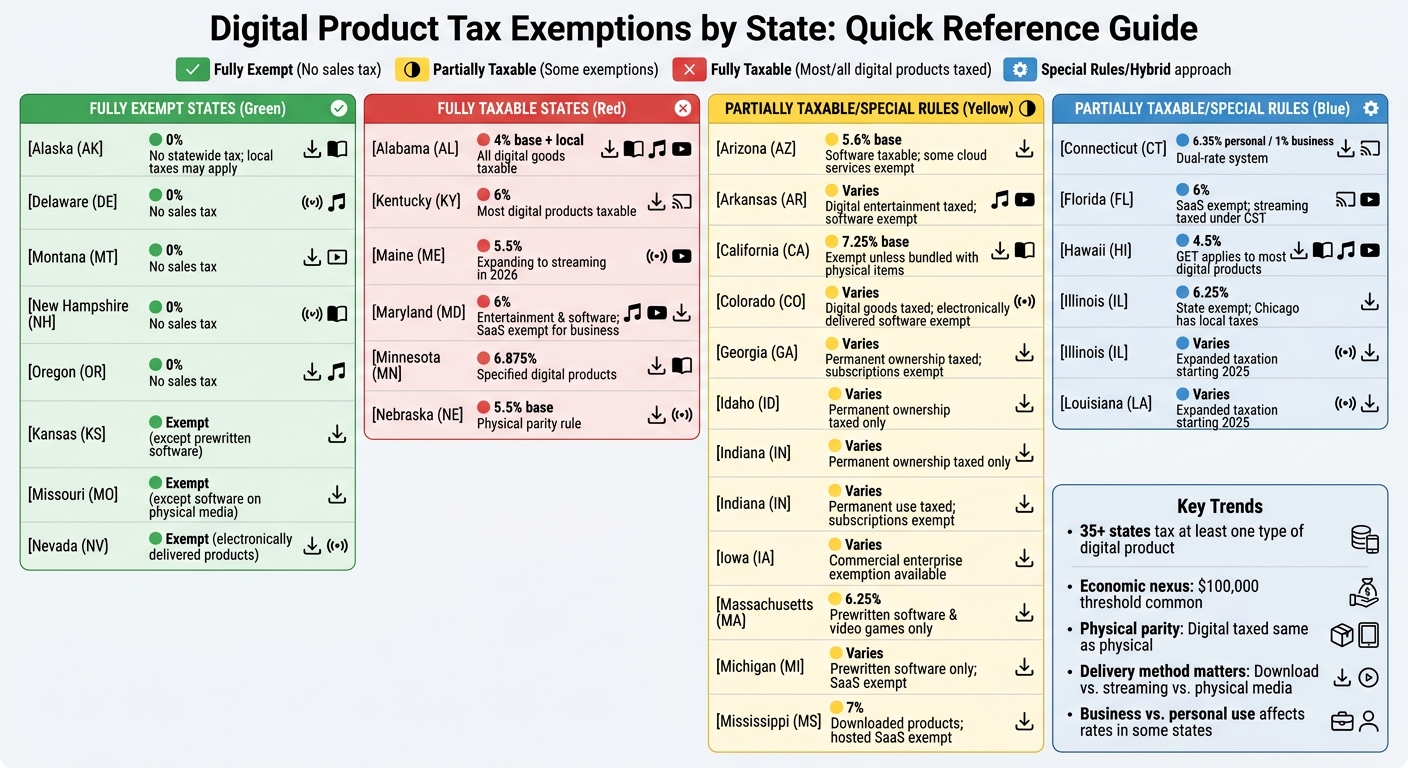

- Taxed States: Over 30 states tax at least one type of digital product. For example, Alabama taxes all digital goods, while Colorado taxes most but exempts electronically delivered software.

- Exempt States: Alaska, Delaware, Montana, New Hampshire, and Oregon do not impose sales taxes, including on digital goods.

- Unique Approaches: States like California exempt most digital products unless paired with physical items. Florida exempts SaaS but taxes physical media.

- Local Variations: States like Alaska and Illinois have local taxes or exceptions, complicating compliance.

- Key Trends: Economic nexus laws, like South Dakota v. Wayfair, mean remote sellers may owe taxes in states where they meet sales thresholds.

Quick Comparison

| State | Tax Status | Notable Exemptions | Unique Rules |

|---|---|---|---|

| Alabama | All digital goods taxable | Minimal exemptions | Local taxes add complexity |

| Alaska | No statewide tax | Varies by local jurisdiction | Local sales taxes apply in some areas |

| California | Most digital goods exempt | E-books, software | Physical items bundled with digital are taxed |

| Florida | SaaS exempt | Digital downloads | Streaming services taxed under CST rules |

| Texas | Most digital goods taxable | Custom software | Economic nexus applies |

Staying compliant requires monitoring state-specific rules and recent legal changes. Remote sellers should focus on economic nexus thresholds by state and delivery methods to avoid unexpected liabilities.

1. Alabama

Tax Exemption Status

In Alabama, all digital products are treated as taxable. The state views digital goods as taxable tangible personal property, no matter how they’re delivered. According to the Alabama Department of Revenue, if a product is taxable in its physical form, it remains taxable when delivered electronically.

"The form in which tangible property is delivered by the seller to the purchaser is of no consequence." – Alabama Department of Revenue

This means businesses selling digital products in Alabama must handle taxes just like sellers of physical goods. The state sales tax rate is 4.00%, but local taxes can push the combined average rate to 9.29%. Remote sellers need to factor in these rates to stay compliant with sales tax.

Taxable Digital Products

Alabama taxes a range of digital products, including computer software, streaming services, e-books, digital photographs, and digital blueprints. The state also taxes specified digital products (SDPs), which cover many types of electronically delivered content. Even credit card transaction fees are subject to sales tax when tied to a taxable digital product.

Businesses are required to register for a sales tax permit and collect both state and local taxes on digital sales. The state’s guidance emphasizes that digital versions of physical products are taxable, even if not explicitly listed.

This broad taxation approach leaves little room for exemptions.

Exempt Digital Products

Alabama provides limited exemptions for digital products. Internet access services are exempt due to a federal moratorium, but this doesn’t cover Voice over Internet Protocol (VoIP) or similar telephony services. Labor charges for installation or repair can also be exempt, but only if they’re separately stated on the invoice.

Other exemptions include wholesale or resale transactions made to licensed retail merchants and sales to U.S. and Alabama government agencies. However, these exemptions apply to the type of transaction, not the digital product itself, making Alabama one of the stricter states when it comes to taxing digital goods.

sbb-itb-ba0a4be

2. Alaska

Tax Exemption Status

Alaska stands out as one of the few states with no statewide sales tax (0%). This means digital products are generally not taxed at the state level. Along with Delaware, Montana, New Hampshire, and Oregon, Alaska is part of a small group of states without a general retail sales tax.

"Alaska does not impose a statewide sales and use tax, making it one of the few states without a general retail sales tax. Instead, sales tax in Alaska is administered at the local level."

– Bradley Feimer, Regulatory Counsel, Sovos

However, taxation in Alaska isn’t entirely absent. Local jurisdictions can impose their own sales taxes, which are based on the buyer’s location. Businesses operating in areas governed by the Alaska Remote Seller Sales Tax Commission (ARSSTC) must comply with local tax rules and nexus requirements.

The next section explains how these local regulations impact the taxability of digital products.

Taxable Digital Products

In jurisdictions participating in the ARSSTC, digital products are subject to local sales taxes. According to the Alaska Municipal Sales Tax Program, any digital goods or services delivered to these areas are taxable. This includes:

- Software downloads

- Cloud-based software (SaaS)

- Streaming services

- Subscriptions

- Other online services

The tax is typically calculated based on the buyer’s billing address, which is used to determine the point of delivery.

It’s worth noting that major cities like Anchorage and Fairbanks do not impose a general sales tax. However, they might have specific excise taxes on items such as lodging or alcohol. To ensure compliance, businesses should carefully review the tax codes of the municipalities they operate in, as tax rates and rules can vary widely.

Key Exceptions

Certain local jurisdictions offer exemptions for specific products, such as newspapers or professional medical services. Businesses should contact local tax authorities to understand the procedures for claiming these exemptions. Similarly, tax-exempt entities must adhere to local guidelines to maintain their exemption status.

Because Alaska’s tax system is decentralized, businesses need to focus on local nexus rules and municipal tax codes rather than relying solely on state-level regulations.

3. Arizona

Tax Exemption Status

Arizona operates a bit differently when it comes to taxing digital products. Instead of a traditional sales tax, the state uses a Transaction Privilege Tax (TPT). This tax is technically imposed on the seller for the privilege of doing business in the state, but the cost is usually passed along to the buyer. The base TPT rate is 5.6%, but when you factor in local taxes, the total rate can range from 5.6% to 11.2%.

Arizona is an origin-based state for TPT purposes. This means the tax rate is determined by the seller’s location, not the buyer’s. However, remote sellers, including those looking to start a business in the USA as a foreigner, need to register and collect TPT if their Arizona sales exceed $100,000 in gross revenue. Below, we’ll break down which digital products are taxed and which are exempt under Arizona law.

Taxable Digital Products

Most digital products in Arizona are taxable, as they fall under the retail classification. Here are some key points:

- Prewritten software is taxable whether it’s downloaded or accessed remotely via the cloud.

- Digital goods that are fully downloaded onto a device – like audio files, e-books, movies, and digital subscriptions – are also taxed.

- Streaming services and Software-as-a-Service (SaaS) are typically considered taxable because they are treated as digital products or tangible personal property.

While the state taxes most digital products, there are a few important exceptions.

Exempt Digital Products

Certain digital products and services qualify for exemptions in Arizona:

- Custom software modifications designed for a single buyer are exempt if they’re separately stated.

- Digital services, as outlined in ARS 42-5077, are not taxed. This includes some cloud computing services like Platform as a Service (PaaS) and Infrastructure as a Service (IaaS).

"The gross income, gross receipts, gross proceeds, purchase price or sales price from selling, leasing, licensing, purchasing or using digital services as defined in section 42-5077 is excluded from tax."

– Arizona Revised Statutes § 42-5002

Additionally, digital goods that are streamed or viewed without being permanently downloaded are excluded from municipal tax. Even if users can view, save, or print output, or if transitory files like cookies are transferred, these remain classified as excluded digital services.

Key Exceptions

The method of delivery plays a major role in determining taxability. Products that are fully downloaded are generally taxable, while those that are only accessed remotely may not fall under certain tax classifications. Municipalities can tax prewritten software and electronically transferred digital goods, but they cannot impose TPT or use tax on digital services or digital goods that are only accessed remotely.

For businesses purchasing prewritten software or digital goods for employees in multiple states, Multiple Points of Use (MPU) certificates can help apportion the tax. This allows businesses to allocate tax based on a reasonable method supported by their records. This approach underscores the complexities of navigating digital product tax compliance across the U.S. For many, this process begins with forming a company in the US to establish a legal presence.

4. Arkansas

Tax Exemption Status

Arkansas has a unique approach to taxing digital products, combining standardized definitions from the Streamlined Sales and Use Tax Agreement (SSUTA) with its own specific exemptions. The state generally imposes sales and use tax on "specified digital products" sold to end users. The main legal framework for these taxes is outlined in Arkansas Code §26-52-3013 and §26-52-304. This setup creates a distinction between taxable digital entertainment and certain software-related items that are exempt.

Taxable Digital Products

Digital entertainment products, such as digital audio (music and ringtones), audio-visual works (movies and TV shows), digital books, and streaming services, are subject to sales and use tax in Arkansas.

Exempt Digital Products

Despite taxing most digital entertainment, Arkansas provides exemptions for certain software and subscription-based products. Prewritten computer software and video games are tax-exempt if delivered electronically or through a "load and leave" method (using a temporary medium). Subscriptions to digital newspapers, journals, periodicals, and academic databases also qualify for exemptions. Additionally, custom software development and programming services are not taxable, and technical support charges for software are excluded from tax if they are itemized separately on the invoice.

Key Exceptions

The way charges are presented on an invoice can determine whether a product remains tax-exempt. For example, electronically delivered software licenses retain their exemption only if their charges are clearly separated from any physical items, like manuals or backup disks. On the other hand, software delivered on tangible media – such as CDs or USB drives that the buyer keeps – is treated as taxable tangible personal property.

5. California

Tax Exemption Status

In California, digitally transmitted products are not subject to sales tax. These items are classified as "electronic data products" rather than tangible personal property, which exempts them from taxation. With the state’s base sales tax set at 7.25%, the tax status of a digital product hinges on how it is delivered.

Exempt Digital Products

Digital products delivered solely as electronic downloads are tax-free. This exemption covers a range of items, including canned (noncustom) software, eBooks, mobile apps, digital images, and stock databases. Streaming services also generally avoid state sales tax, though certain cities in California may apply a local Utility Users Tax (UUT). The California Department of Tax and Fee Administration clarifies:

"The transfer of a downloadable file such as an eBook or an ‘app’ without purchasing any physical storage medium is not a taxable transaction."

However, this tax-free status depends on strict adherence to delivery rules, which are outlined in the exceptions below.

Key Exceptions

California applies an "all-or-nothing" approach when it comes to taxing digital products. If a seller includes any physical component – like a printed manual or a backup copy on a flash drive, CD, or DVD – alongside the electronic download, the entire sale becomes taxable. As noted by the California Department of Tax and Fee Administration:

"If as part of the sale, you provide your customer with a printed copy of the electronically transferred information or a backup data copy on a physical storage medium, such as a flash drive, your entire sale is usually taxable."

To keep digital sales tax-free, businesses must ensure that no physical items are included in the transaction. This is a critical consideration for foreign entrepreneurs following a non-resident LLC formation guide to establish their digital presence.

6. Colorado

Tax Exemption Status

Colorado’s approach to taxing digital goods underwent a significant shift with the introduction of HB21-1312 on July 1, 2021. While some entrepreneurs compare business formation services to navigate such regulatory changes, this legislation classified digital goods as "tangible personal property", making them taxable regardless of how they are delivered. As stated in the legislation:

"The method of delivery does not impact the taxability of a sale of tangible personal property."

By 2022, Colorado became one of 35 states taxing certain digital products.

Taxable Digital Products

In Colorado, digital products like e-books, audio files, video content, and streaming subscriptions are subject to sales tax. Cloud-based data storage also falls under taxation, categorized as "mainframe computer access".

Despite this broad taxation, there are notable exemptions, particularly for software products delivered electronically.

Exempt Digital Products

Software delivered electronically, including prewritten software and SaaS (Software as a Service), is not subject to sales tax. Custom software and data processing services are also exempt. Even prewritten software, which is taxable when sold on physical media, becomes tax-free when delivered as a digital download. Gail Cole from Avalara highlights this distinction:

"Digital products are generally taxable, though electronically delivered software is exempt."

This exemption underscores the importance of delivery methods in determining taxability.

Key Exceptions

The "mainframe computer access" classification for taxable services includes specific exceptions. For instance, tax does not apply when access is solely for reviewing or acquiring data maintained by the vendor. Similarly, access related to electronic software delivery or the use of software hosted by an application service provider is excluded from taxation.

7. Connecticut

Tax Exemption Status

Connecticut takes a unique approach to taxing digital goods by using a dual-rate system that depends on the buyer’s intent. Since October 1, 2019, the state has taxed digital products and electronically delivered prewritten software at different rates depending on whether the purchase is for personal or business use. For personal use, the standard sales tax rate is 6.35%, while purchases for business purposes are taxed at a much lower rate of 1%. Unlike states that impose additional local taxes, Connecticut keeps it simple by applying only the state rate, which is a key consideration when operating in multiple states.

Taxable Digital Products

Digital products subject to tax in Connecticut include:

- Digital audio-visual works: Movies and TV shows

- Digital audio works: Music and podcasts

- Digital books: E-books

- Streaming services

Electronically delivered prewritten software is also taxable, with the applicable rate depending on whether the purchase is for personal or business use. This clear distinction ensures that both categories are taxed appropriately.

Key Exceptions

The standout exception in Connecticut’s tax policy is the reduced 1% rate for electronically delivered prewritten software bought for business purposes. To apply the correct rate, sellers must accurately identify whether the buyer is an individual or a business at checkout. This ensures that customers are charged the correct amount and prevents overpayment.

8. Delaware

Tax Exemption Status

Delaware stands out for its lack of state-level sales tax on any products, including digital goods. As part of the NOMAD states – New Hampshire, Oregon, Montana, Alaska, and Delaware – the state applies a 0% tax rate to digital products. There are no local sales taxes in Delaware, and this exemption applies across the board, regardless of how the digital product is delivered. Whether it’s a permanent download, a subscription service, or cloud-based access, all are treated the same under Delaware’s tax-free policy. This means businesses selling to Delaware customers don’t have to worry about economic nexus thresholds or obtaining a state sales tax permit. The tax-free status applies uniformly to every category of digital products.

Exempt Digital Products

Delaware’s tax structure ensures that all forms of digital products are completely exempt. This includes categories such as SaaS, downloaded software, eBooks, digital publications, streaming services, and digital audio or video files. While many states impose taxes on SaaS or downloaded software, Delaware remains an exception, making it a haven for businesses in the digital space.

Key Exceptions

Since Delaware doesn’t have a sales tax system, there are no exceptions to its tax-free policy. This favorable environment is one reason Delaware is a popular choice for business incorporation. However, companies should remember that tax obligations may still arise in other states where their customers reside. Delaware’s straightforward approach to taxation sets it apart from many other states discussed earlier.

9. Florida

Tax Exemption Status

In Florida, digital products are not subject to sales or use tax because they aren’t classified as tangible personal property. The state’s 6% sales tax generally doesn’t apply to most digital goods delivered electronically. However, if a business surpasses the $100,000 annual sales threshold to Florida consumers, it must register with the Florida Department of Revenue, even though digital-only transactions are typically tax-free. Additionally, local counties may add a discretionary surtax ranging from 0.5% to 1.5%, which can slightly adjust the effective tax rate. This approach distinguishes Florida from states that treat digital products as taxable tangible goods.

Exempt Digital Products

Florida exempts Software as a Service (SaaS) when accessed via the cloud or browser.

"Florida does not impose sales tax on SaaS delivered entirely electronically. SaaS is considered an intangible service rather than tangible personal property." – Sela Tax & Accounting LLC

This exemption also covers digital downloads like e-books, music files, and video content purchased as permanent downloads. Custom software, regardless of delivery method, is also exempt – a key difference from prewritten software. Similarly, information services and data products delivered digitally are not taxed.

Key Exceptions

There are exceptions to these exemptions. For example, Florida imposes tax when digital goods are sold alongside physical items. Digital products delivered on tangible media – such as CDs, DVDs, or USB drives – are subject to the standard 6% sales tax. If a digital product is bundled with a tangible item, the entire sale becomes taxable.

Streaming services are treated differently under Florida law.

"Digital goods are not considered ‘tangible personal property’ and so are not subject to Florida sales or use tax. However, video, direct-to-home satellite, and related services… are subject to Florida communications services tax, or CST." – Gail Cole, Avalara

Streaming providers offering video, audio, or data transmission services must register for and collect the Communications Services Tax (CST) instead of the standard sales tax. Businesses handling digital products must maintain clear documentation, such as contracts and invoices, to prove that their products are delivered electronically.

For entrepreneurs managing these complexities, platforms like BusinessAnywhere provide tools to streamline U.S. business registration, compliance, and ongoing maintenance.

10. Georgia

Tax Exemption Status

Starting January 1, 2024, Georgia began applying sales and use tax to specific digital products, other digital goods, and digital codes when the purchase grants permanent lifetime access. This shift, introduced through Senate Bill 56 and signed into law on May 2, 2023, aligns Georgia with states like Alabama, Arizona, and North Carolina. However, it differs from states such as California and Florida, which typically exempt digital goods from sales tax.

Taxable Digital Products

The tax affects specific digital products such as digital audio files (e.g., music, podcasts, ringtones), digital audiovisual works (e.g., movies, TV shows), and digital books (e.g., e-books, magazines). The main criterion is permanent ownership – for instance, a one-time purchase of a digital movie that provides lifetime access is taxable. Similarly, digital codes that unlock these products are also taxed. On the other hand, digital products requiring ongoing payments, like monthly subscriptions, are generally not subject to this tax.

Exempt Digital Products

Certain items remain exempt from sales tax, including prewritten computer software delivered electronically or via "load and leave" methods. Custom software is also tax-exempt, regardless of how it’s delivered. Additionally, streaming services and subscription-based platforms are excluded, as they require continuous payments rather than granting permanent use rights.

"The legislation includes an exemption for the sale of prewritten computer software transferred electronically to the purchaser or delivered to the purchaser electronically by means of load and leave; however, this exemption ‘shall not include sales of specified digital products, other digital goods, or digital codes.’" – Deloitte Tax LLP

Key Exceptions

Only purchases that provide permanent access are taxable. For example, a Netflix subscription remains untaxed due to its monthly payment model, while a digital movie bought for permanent download is taxable. Charges for software customization are also exempt, provided they are itemized separately on the invoice. Businesses are expected to maintain clear documentation of delivery methods and payment structures to ensure compliance with tax rules. Georgia’s approach underscores the importance of transparency in payment terms, a trend seen in other state regulations as well.

11. Hawaii

Tax Exemption Status

Hawaii takes a different route when it comes to taxation, opting for a General Excise Tax (GET) instead of a conventional sales tax. This GET applies broadly to nearly all business activities, including digital product sales. The statewide GET rate is 4%, with an additional 0.5% county surcharge, resulting in an effective rate of about 4.5%. Under this system, digital products are taxable, with prewritten and licensed software classified as tangible personal property, while custom software is taxed as a service. Unlike other states that offer exemptions for specific products, Hawaii taxes nearly all digital transactions, creating a straightforward framework for businesses.

Taxable Digital Products

The GET covers a wide range of digital products, including:

- SaaS

- Downloaded software

- Ebooks and digital publications

- Streaming media

- Digital art

- Mobile applications

- Digital codes

Businesses generally pass the effective 4.5% rate on to their customers.

Exempt Digital Products

Hawaii’s exemptions are based more on the purchaser or the product’s use rather than the product itself. For example, sales to certain organizations – like 501(c)(3) or 501(c)(14) nonprofits, public schools, government agencies, nonprofit hospitals, and homes for the aged – may qualify for exemptions. Additionally, licensed resellers can benefit from a reduced wholesale GET rate of 0.5%, provided they have valid Hawaii resale certificates. Remote sellers, however, must adhere to specific conditions for exemptions.

Key Exceptions

Remote sellers must pay attention to Hawaii’s economic nexus thresholds. If a business surpasses $100,000 in sales or completes 200 transactions within a calendar year, they are required to register for a GET license – even without a physical presence in the state. Once the 200-transaction threshold is hit, the business must collect GET, regardless of total revenue. Sellers can register through the Hawaii Department of Taxation‘s online portal to ensure compliance.

12. Idaho

Tax Exemption Status

In Idaho, digital products are taxed only when the purchaser gains permanent ownership of the product. The state classifies digital products – like music, books, videos, and games – as tangible personal property if permanent usage rights are granted. According to the Idaho State Tax Commission:

"Digital videos, games, music, and books that the buyer has a permanent right to use are tangible personal property."

Services like subscriptions and streaming platforms are generally not taxed, as they do not provide permanent ownership. This distinction forms the basis for determining the taxability of digital products.

Taxable Digital Products

Digital products are subject to tax when permanent ownership is transferred. This includes items like downloadable music files, eBooks, videos, and games. However, prewritten software delivered electronically is exempt as long as no physical media is involved, and custom software is always excluded from taxation.

Exempt Digital Products

Certain digital products and services are exempt from taxation in Idaho. These include:

- Subscription-based services (e.g., streaming platforms)

- Rentals or leases of digital content

- Cloud storage and SaaS (Software as a Service)

- Digital photographs delivered electronically

- Online-only newspapers and magazines

Additionally, Idaho’s tax rules exempt "load and leave" software installations – where software is installed directly on a customer’s system without any physical media. While exemption certificates aren’t required for electronically delivered software, businesses should keep clear records of delivery methods and subscription details to confirm their tax-exempt status.

Key Exceptions

There are specific cases where digital products become taxable. For example, if a product – such as software – is delivered on physical media (like a CD-ROM or USB drive), it is taxable, even if the same product would be exempt when delivered electronically. Idaho Code section 63-3616(b) and Sales Tax Rule 027 outline these regulations, while data center exemptions may apply under Idaho Code section 63-3622VV. To ensure compliance, businesses should document delivery methods and ownership terms carefully, adhering to Idaho’s "permanent-right-to-use" standard.

13. Illinois

Tax Exemption Status

Illinois stands out when it comes to taxing digital products. The state does not classify electronically downloaded data as "tangible personal property", which means most digital products are not subject to the 6.25% sales and use tax. According to 86 Ill. Adm. Code 130.2105(a):

"Information or data that’s downloaded electronically (e.g., downloaded books, musical recordings, newspapers, or magazines) do not constitute the transfer of tangible personal property and are not subject to Illinois sales and use tax."

While many states – 35 as of 2022 – tax specific digital products like audio, video, and books, Illinois explicitly excludes these items. However, local jurisdictions, such as Chicago, may impose their own taxes even when the state provides exemptions. This creates a layered framework for taxing digital products in Illinois.

Exempt Digital Products

Illinois exempts several types of digital products from taxation, including electronically downloaded books, music, newspapers, and magazines. Software as a Service (SaaS) is typically not subject to the Retailers’ Occupation Tax, though providers might need to pay the Servicemen Occupation Tax if tangible property is involved in delivering the service. Similarly, custom software is treated as a service and remains tax-exempt.

Taxable Digital Products

On the other hand, prewritten software is generally taxable because it is treated as tangible personal property. If software is delivered on physical media or involves any transfer of tangible property, it becomes subject to tax. The main distinction lies in whether the product involves a tangible component or is purely digital.

Key Exceptions

Local taxes add another layer of complexity to Illinois’s tax structure. For example, Chicago imposes a 9% Amusement Tax on streaming services and plans to introduce a Social Media Amusement Tax (SMAT) starting January 1, 2026. Companies serving customers in Chicago must register separately and collect these taxes. Businesses need to carefully monitor customer locations and delivery methods to ensure they comply with both state and local tax requirements.

14. Indiana

Tax Exemption Status

Indiana takes a specific approach to digital product taxation by focusing on what it calls "specified digital products." These include digital audio works, digital audiovisual works, and digital books – but only when they are sold for permanent use. Sales tax expert Gail Cole explains:

"Specified digital products are taxable when the end user has the right of permanent use that’s not conditioned upon continued payment."

In practical terms, this means that one-time purchases granting permanent access are taxable. On the other hand, subscription-based services offering temporary access are generally not taxed. Additionally, Indiana applies sales tax to prewritten software, regardless of whether it’s delivered electronically or on physical media, and also taxes Software as a Service (SaaS).

Taxable Digital Products

Indiana’s tax rules cover a range of digital products. Prewritten software and SaaS platforms are taxable no matter how they’re delivered – electronically or otherwise. Digital codes, such as vouchers or access codes that unlock digital products, are taxed in the same way as the products they provide access to. For example, if you buy a code to download a taxable e-book, the code itself is subject to tax.

Exempt Digital Products

Some digital products are not subject to sales tax in Indiana. For instance, digital photographs are explicitly exempt. Custom software created for specific clients, as well as digital information and data processing services, are also excluded from taxation. Virtual items sold on streaming platforms are another notable exemption. According to Revenue Ruling 2022-03ST, issued in November 2022, the Indiana Department of Revenue clarified:

"The sales of such virtual items are not subject to Indiana sales and use tax as either sales of specified digital products or digital codes regardless of whether sold with or without an interactive overlay functionality."

Key Exceptions

The concept of permanent use plays a pivotal role in Indiana’s tax policy. Transactions that provide only temporary access, such as monthly subscriptions, do not meet the threshold for taxable "specified digital products." The November 2022 ruling also clarified that virtual items providing free platform access or lacking a connection to computer software are not taxable. For businesses, it’s essential to determine whether their digital offerings grant permanent ownership or only subscription-based access, as this distinction directly impacts tax obligations. Indiana’s approach underscores the complexity of navigating digital tax rules across different states.

15. Iowa

Tax Exemption Status

Iowa started taxing digital products on January 1, 2019, following the implementation of Senate File 2417. Before this, all electronically delivered products were not subject to sales tax. The state also became a member of the Streamlined Sales and Use Tax Agreement (SST), adopting standardized definitions for "specified digital products." These include non-tangible items transferred electronically via websites or apps.

One notable feature of Iowa’s tax system is the Commercial Enterprise exemption, which provides extensive relief for qualifying B2B transactions. According to the Council On State Taxation, Iowa stands out as the only state offering such broad sales tax exemptions for digital business inputs. While digital products are generally taxable, sales to qualifying businesses for their exclusive use are exempt.

Taxable Digital Products

Despite the Commercial Enterprise exemption, most digital products remain taxable in Iowa. This includes both prewritten and custom software, regardless of whether it is delivered physically or electronically. The Iowa Department of Revenue clarified:

"Beginning January 1, 2019, prewritten computer software is subject to sales tax whether delivered or accessed in physical form (as tangible personal property) or electronically (as a specified digital product)."

Software as a Service (SaaS) is also taxable. It refers to vendor-hosted software accessed online. Other taxable items include information services, such as subscriptions to credit reports, research databases, and real estate listings. Electronic storage services, which involve storing files, documents, and records, are also subject to tax. Additionally, Iowa taxes "video game services", which include access to games, in-game currency exchanges, and hosting services.

Exempt Digital Products

The Commercial Enterprise exemption provides the most significant tax relief in Iowa. To qualify, the purchaser must be a for-profit business, an insurance company, a financial institution, or part of specific professions like law, medicine, or farming. Gail Cole from Avalara explains:

"Specified digital products are generally taxable unless purchased by a commercial enterprise and used exclusively by or furnished to that commercial enterprise."

Nonprofit entities are not eligible for this exemption, except for nonprofit insurance companies and financial institutions. Additionally, internet access remains exempt under federal law, and web hosting services are not taxable in Iowa. Sales to "non-end users" – those who buy digital products for further commercial broadcast, licensing, or distribution – are also exempt.

Key Exceptions

The exclusivity requirement is a crucial condition for businesses claiming the Commercial Enterprise exemption. The digital product must be purchased and used exclusively by the qualifying commercial enterprise, with any non-commercial use kept to a minimum. Live webinars are exempt if they allow interactive participation similar to in-person presentations. According to the Iowa Department of Revenue:

"Purchasing access to a live webinar is not taxable, if the live webinar allows for a level of participation which is substantially similar to an in-person presentation."

However, pre-recorded webinars without interactive participation are taxable as "news or information products." Certain organizations, such as legal aid groups that were previously exempt from sales tax on tangible property, retain their exempt status when purchasing digital products. Iowa’s unique exemptions highlight the importance of businesses thoroughly understanding tax and company formation regulations for digital products.

16. Kansas

Tax Exemption Status

Kansas stands out as one of the states that doesn’t apply sales tax to digital products. The state categorizes digital goods as intangible property and hasn’t adopted the "specified digital products" definitions set by the Streamlined Sales and Use Tax Agreement (SSUTA), unlike 24 other states. Sales tax expert Gail Cole explains:

"Kansas does not tax specified digital products and has not adopted any of the SST-specified digital products definitions"

This policy sets Kansas apart from states that tax a wide range of digital goods. However, while most digital products are tax-free, there are key exceptions to note.

Taxable Digital Products

One major exception is canned (prewritten) software, which is taxable in Kansas regardless of how it’s delivered. Whether the software is provided on a physical medium or downloaded electronically, it is subject to sales tax. This distinction is important for businesses operating in the state. For foreign entrepreneurs, understanding non-resident LLC formation can help clarify these state-specific tax obligations.

Exempt Digital Products

Kansas provides a broad exemption for many digital goods delivered electronically. Items like digital audio files (music, podcasts), digital books (e-books, magazines), and streaming services (movies, TV shows) are all tax-exempt. Additionally, custom software is not subject to sales tax, no matter how it is delivered – whether physically or electronically.

Key Exceptions

Customization of canned software introduces specific tax rules. If a business customizes canned software for a buyer, the charges for customization can qualify for a tax exemption. However, these customization fees must be listed separately on the invoice. If the charges are not itemized, the entire transaction could be considered taxable canned software. This requirement ensures that only the customization work receives the appropriate tax treatment.

17. Kentucky

Tax Exemption Status

Kentucky applies a flat 6% sales tax to digital products, treating them as tangible personal property for tax purposes. This means most digital goods are subject to taxation. As a member of the Streamlined Sales and Use Tax Agreement (SSUTA), Kentucky uses standardized definitions for specific digital products, which simplifies tax compliance for businesses operating across different states. Additionally, local governments in Kentucky cannot impose additional sales taxes, ensuring the state-wide rate remains a consistent 6%. This consistency makes it easier to understand which digital products fall under taxable or exempt categories.

Taxable Digital Products

The following digital products are taxable in Kentucky:

- Digital audio works like music, podcasts, and ringtones

- eBooks

- Digital audiovisual works, including movies, TV shows, and streaming services

- Finished artwork and digital photographs

- Periodicals, newspapers, and magazines

- Video or audio greeting cards

- Electronic games

- Prewritten computer software (whether downloaded or accessed remotely as SaaS)

- AI-powered applications

- Digital codes

Exempt Digital Products

Certain categories are exempt from sales tax in Kentucky, such as:

- Custom software

- Specific professional services

- Sales to government agencies for official government functions

- Occasional sales of digital property

Key Exceptions

Kentucky provides a small seller exemption for services if their gross receipts are less than $12,000 in a calendar year. However, this exemption does not extend to businesses selling digital property. Additionally, if a purchaser returns digital property for a full cash or credit refund without needing to buy a more expensive item, the transaction is considered tax-exempt.

18. Louisiana

Tax Exemption Status

Louisiana has introduced notable changes to its tax treatment of digital products. Through House Bills 8 and 10, the state expanded its sales tax to include digital products starting in December 2024, with full implementation by January 1, 2025. These laws align the tax treatment of digital and physical products – if a physical book is exempt, so is its digital version. Additionally, the state now taxes all software consistently, eliminating the distinction between custom and prewritten software.

Taxable Digital Products

Louisiana taxes a wide variety of digital goods and services. This includes streaming movies, TV shows, music, podcasts, digital books, digital codes, apps, and games. Software-as-a-Service (SaaS) platforms like Office 365, Zoom, and Salesforce are treated as taxable prewritten software access. Other taxable services include information services – such as newsletters, tax guides, research publications, mailing lists, and database subscriptions – as well as media services like GPS systems, cable TV, satellite TV, and satellite digital audio radio services.

Exempt Digital Products

Despite the broad tax scope, some digital products and services remain exempt. Free digital products are not taxed, nor are digital items used as components in creating new products or proprietary information tailored for specific clients. Additionally, internet access services, data processing, and payment processing services are excluded from taxation. Exemptions also apply to information sold to FCC-licensed newspapers, TV stations, or radio stations for direct broadcast or publication, as well as charges by financial institutions for providing account balance information.

However, sellers must be aware of specific exceptions that could affect compliance.

Key Exceptions

Tax obligations in Louisiana are determined by where the product is used, not where the seller is located. As Alex Lamachenka, Head of DemandGen at TaxCloud, explained:

"Louisiana has signaled that enforcement is coming – and sellers can no longer assume digital offerings fall outside tax rules"

To ensure compliance, sellers should maintain valid exemption certificates for transactions involving healthcare providers and FDIC-insured financial institutions. Carefully reviewing digital offerings is essential to meet these requirements.

19. Maine

Tax Exemption Status

In Maine, digital products are taxed just like their physical counterparts. The state applies a 5.5% sales tax to electronically delivered products that would otherwise be taxable in physical form, as outlined in Me. Rev. Stat. Ann. §1752(9‑E). For example, an e‑book is taxed the same way as a printed book, and downloadable music is treated like a physical CD.

Starting January 1, 2026, Maine will extend its tax to include digital audiovisual and audio services. This means subscriptions, pay-per-view content, and access fees for these services will be taxed, even if there is no permanent download involved.

Maine simplifies tax compliance by maintaining a single statewide rate of 5.5%, with no additional local sales taxes. The state uses destination-based sourcing, which means the tax is based on the buyer’s billing address or where the product is first used.

Taxable Digital Products

Maine taxes a wide range of digital goods. Products classified as Specified Digital Products (SDPs) – such as digital audiovisual works, digital audio works, and digital books – are taxed at the 5.5% rate. Downloadable software, including prewritten computer programs, is also taxable.

As of January 2026, streaming services like Netflix and Spotify will be subject to tax. Subscriptions and access fees for these platforms will be included in the taxable category. Other taxable items include video games, downloadable music, and e‑books, all of which are taxed at the same 5.5% rate.

Exempt Digital Products

Certain digital products and services are exempt from sales tax in Maine. Notably, Software as a Service (SaaS) is not taxed. Additionally, custom programming purchased by a business is exempt, provided that the customization charges are listed separately. If a business buys standard software and customizes it, the standard software is taxable, but the customization portion remains exempt as long as it is separately invoiced.

Products purchased for resale are also exempt, but sellers must provide a valid resale certificate to qualify. These exemptions are subject to specific documentation and thresholds, which are outlined in the state’s regulations.

Key Exceptions

Maine has an economic nexus threshold of $100,000 in gross revenue, which replaced the previous 200-transaction threshold on January 1, 2022. This change aligns with broader trends in state taxation of digital goods. Additionally, sellers with more than $3,000 in taxable sales annually are automatically issued a resale certificate by Maine Revenue Services.

Businesses are required to keep exemption certificates for at least four years. Nonprofit organizations seeking tax exemptions must submit Form APP‑171 through the Maine Tax Portal to obtain an official certificate. Manufacturers can claim exemptions on production equipment by filing Form ST‑A‑117 (Industrial Users Exemption Certificate).

20. Maryland

Tax Exemption Status

Since March 14, 2021, Maryland has applied its standard 6% tax rate to digital products and digital codes, following the override of HB 932. However, an amendment introduced in July 2022 (SB 723/HB 791) exempted enterprise software and SaaS used exclusively for commercial purposes from this tax. The tax is aimed at end users, so products purchased for resale or further commercial distribution are generally excluded. This approach reflects the varied digital product tax policies seen across different states.

Maryland uses destination-based sourcing, prioritizing the customer’s tax address to determine tax obligations. Remote sellers are required to register and obtain an EIN if their annual gross revenue exceeds $100,000 or they complete 200 or more separate transactions.

Taxable Digital Products

Maryland taxes a broad spectrum of digital entertainment and software. Streaming platforms like Netflix and Spotify, as well as downloadable content such as movies, music, audiobooks, and ringtones, fall under the 6% tax. Other taxable items include e-books, digital magazines, newspapers, newsletters, and canned or commercial off-the-shelf (COTS) software delivered electronically. SaaS for personal use, video games, virtual in-game items, and subscriptions to online content are also taxable. If a taxable digital product is bundled with a non-taxable service, the entire transaction is typically subject to tax.

Remote sellers must closely monitor their sales in Maryland to ensure compliance with the $100,000 revenue or 200-transaction threshold.

Exempt Digital Products

Despite the broad tax coverage, Maryland exempts several business-oriented digital products. Since July 1, 2022, enterprise computer systems and SaaS used exclusively for commercial purposes have been tax-exempt. To qualify, the software must be part of an interconnected network, used on multiple devices simultaneously, or designed for operating a computer system. Custom software, including products requiring significant creative configuration, is also exempt.

Certain professional services, such as those offered by legal, medical, accounting, or insurance professionals, are exempt when any digital component is incidental. Additional exemptions include cloud storage, web hosting, SEO services, and data transfer fees. Live, interactive educational instruction for K-12 and higher education is exempt, while prerecorded, non-interactive instruction remains taxable. Products are also exempt if the purchaser holds a copyright or intellectual property interest and uses the product solely for commercial purposes, such as marketing.

Key Exceptions

Maryland draws a clear line between personal and commercial use. For instance, tax preparation software for a sole proprietor is taxable because it does not meet the "enterprise" criteria. In contrast, software deployed within an interconnected network for a large corporation qualifies for exemption. Buyers seeking to exempt customized software must notify the seller; otherwise, the full sales tax applies. Non-end users can claim a resale exclusion by providing a valid resale certificate. According to the Department of Legislative Services, the revenue impact from the 2022 amendments is expected to be minimal.

21. Massachusetts

Tax Exemption Status

Massachusetts applies a 6.25% tax rate exclusively to prewritten software and video games, leaving most other digital products exempt from taxation. While other states have expanded their tax bases to include streaming services and digital media, Massachusetts has maintained this focused approach.

The state uses destination-based sourcing, meaning remote sellers must register for tax collection once their annual sales exceed $100,000. With no additional local sales taxes, the 6.25% rate is consistent across the state, making compliance straightforward by narrowing the scope of taxable digital goods.

Taxable Digital Products

Prewritten software, whether downloaded or delivered on physical media, is the main taxable digital product in Massachusetts, as outlined in Regulation 830 CMR 64H.1.3. Video games also fall under this category.

Software as a Service (SaaS) is considered taxable prewritten software because it enables remote access to software. The delivery method doesn’t matter – if a transaction involves any physical component, the entire purchase is taxable.

Exempt Digital Products

Massachusetts exempts a wide range of digital media from taxation. Digital books, music, videos, and streaming services delivered electronically are not subject to tax. This includes e-books, digital magazines, newspapers, podcasts, ringtones, movies, and TV shows. Unlike states such as Texas or New York, which tax more digital services, Massachusetts keeps its exemptions clear and specific, focusing taxation primarily on software.

Custom software created for specific orders is also exempt. If a vendor modifies prewritten software for a particular buyer, the modification charge is exempt as long as it is reasonably allocated and separately itemized on the invoice. Additionally, data processing services that summarize or compute customer data are not taxable.

Key Exceptions

Optional maintenance contracts that include software upgrades are taxed at 50% of the contract price, while contracts without upgrades remain exempt.

For businesses purchasing software for use in multiple states, a Multiple Points of Use (MPU) certificate allows them to apportion the use tax based on the number of Massachusetts users. Software purchased as an ingredient or component part for integration into a product for resale is also exempt. Nonprofit organizations and government agencies can claim exemptions by providing valid Form ST-5 or ST-5C certificates.

22. Michigan

Tax Exemption Status

Michigan generally exempts most digital goods from sales tax, with one major exception: prewritten computer software. In 2004, Michigan expanded its definition of tangible personal property to include prewritten software, aligning its policy with states like California and Florida that also exempt digital products such as e-books and streaming media. The taxability of software in Michigan hinges on whether users have direct control over it. As clarified by the Michigan Department of Treasury:

"The ‘key feature’ in determining whether prewritten software is taxable is whether a party exercises a right or power over it, which turns on how it was delivered".

Downloaded software is taxable because it resides on the user’s device, while software accessed remotely is not. This distinction is central to understanding how Michigan handles digital product taxation.

Taxable Digital Products

The primary taxable digital products in Michigan are prewritten computer software delivered via download or physical media. This includes downloaded video games and mobile applications, as they fall under the category of prewritten software.

Exempt Digital Products

Michigan exempts a broad array of digital content that does not meet the definition of prewritten computer software. Products like e-books, streaming services (covering movies, TV shows, and music), podcasts, and digital audiovisual works are all tax-exempt. Gail Cole from Avalara explains:

"A digital good that doesn’t fall within the definition of ‘prewritten computer software’ is not subject to sales tax or use tax regardless of whether it’s downloaded, streamed, or accessed through a subscription service".

Additionally, Software as a Service (SaaS) is exempt because it is hosted on third-party servers rather than downloaded. Other exempt categories include custom software, digital information services, and data processing services.

Key Exceptions

Michigan applies the "incidental to service" test to determine taxability for transactions that bundle prewritten software with professional services. Another important development is the recent repeal of the statute permitting multiple-points-of-use (MPU) exemption certificates. Previously, these certificates allowed consumers to allocate tax for software used across multiple jurisdictions, but they are no longer available.

23. Minnesota

Tax Exemption Status

Minnesota, as part of the Streamlined Sales and Use Tax Agreement (SSUTA), applies sales tax to a wide range of digital products. This includes "specified digital products", "other digital products", and "digital codes." The statewide sales tax rate is 6.875%, and it applies to all specified digital products, such as digital audio, audiovisual works, and digital books, regardless of how they’re purchased. This broad approach provides a framework for understanding which digital products fall under taxation in the state.

Taxable Digital Products

In Minnesota, various types of digital content are subject to tax. This includes digital audio files like music downloads, ringtones, and podcasts, as well as streaming services for movies and TV shows. Downloaded e-books and online video or computer games are also taxable. Prewritten computer software is treated as tangible personal property and is taxed, but Software as a Service (SaaS) is exempt since it is hosted online. Additionally, digital codes granting access to taxable products are taxed in the same way as the products themselves.

Exempt Digital Products

Not all digital products face taxation in Minnesota. Items such as digital photographs, drawings, charts, and graphs are exempt. Access to digital news articles, data reports, and financial reports is also not taxed. Custom software created for a specific buyer is exempt, unlike prewritten software. Educational materials, including online classes from post-secondary institutions and digital textbooks used in coursework, receive exemptions. Interactive webinars qualify for exemption if they allow real-time interaction and meet specific requirements for parity with in-person events. Beyond these, additional rules and conditions, such as bundled transaction regulations, further clarify the state’s tax policies.

Key Exceptions

Minnesota offers some relief through specific exceptions. For example, the Multiple Points of Use (MPU) exemption applies to digital products used both within and outside the state. Products used in industrial production or as capital equipment in manufacturing are also eligible for relief. In cases of bundled transactions, the entire bundle is taxable unless the taxable portion accounts for 10% or less of the total price. NFTs are subject to tax only when the underlying product or service they represent is taxable. The timing of the sale or use of a digital product is determined by when the seller transfers possession to the buyer or when the product is first used – whichever occurs first.

24. Mississippi

Tax Exemption Status

As of July 1, 2023, Mississippi imposes a 7% sales and use tax on most digital products delivered electronically. This change stems from an expanded definition of tangible personal property, which now includes computer software, though electronically stored or maintained data is excluded from taxation. Whether the tax applies often depends on where the server is located. If software is hosted outside Mississippi and accessed exclusively online, the transaction is exempt from the 7% tax.

Taxable Digital Products

The following digital products fall under the taxable category in Mississippi:

- Downloaded software

- Music files

- Video games

- Electronic reading materials

- Ringtones

Additionally, computer software services performed within the state are also subject to taxation.

Exempt Digital Products

Certain digital services are exempt from Mississippi’s sales tax, particularly when hosted on servers located outside the state. These include:

- Software as a Service (SaaS)

- Platform as a Service (PaaS)

- Infrastructure as a Service (IaaS)

Senate Bill 2449 clarifies this exemption, stating:

"Computer software maintained on a server located outside the state and accessible for use only via the internet is not a taxable retail sale".

Other non-taxable services include information and data processing services, such as payroll, billing, and tax compliance software options.

Key Exceptions

Mississippi offers specific exemptions and methods to simplify tax compliance in certain scenarios. For example:

- Intercompany software transfers: Transfers of software between affiliated entities are treated as non-taxable internal exchanges rather than retail sales.

- Bundled transactions: When taxable and non-taxable items are sold together, businesses can allocate the price between components based on their own records if the vendor does not provide a detailed breakdown.

- Multistate software licenses: Companies with licenses spanning multiple states can use safe harbor methods to allocate tax based on the number of devices or licensed users located in Mississippi versus other states.

25. Missouri

Tax Exemption Status

In Missouri, digital products are generally exempt from sales and use tax because they are not considered "tangible personal property". This means that digital goods delivered electronically are not subject to taxation.

However, software delivered on physical media, like CDs or USB drives, is taxable. On the other hand, the same software delivered digitally is fully exempt. According to the Missouri Department of Revenue:

"Canned software that is delivered digitally, or any custom software, is not taxable."

Let’s take a closer look at which digital products fall into taxable and exempt categories.

Taxable Digital Products

Missouri’s taxable digital products are limited to specific cases. Prewritten software delivered on physical media remains the primary taxable category. This includes off-the-shelf software sold on CDs, DVDs, or USB drives, whether purchased in stores or shipped directly to customers.

Additionally, when services such as installation, training, or maintenance are bundled with taxable software, those services also become taxable. This approach contrasts with many states that apply taxes to a broader range of digital goods.

Exempt Digital Products

Missouri offers broad exemptions for digital products delivered electronically. A June 2023 letter ruling from the Missouri Department of Revenue confirmed that items like digital music, interactive computer services, and subscription-based services are not taxable. Other exempt items include:

- Downloaded software and software upgrades

- Streaming services for music and video

- Custom software

- Internet access fees

Custom software is exempt from taxation regardless of whether it is delivered digitally or on physical media.

Key Exceptions

Proper documentation is crucial for maintaining tax-exempt status. For example, invoices and sales records should clearly indicate the delivery method for prewritten software. If the software is delivered electronically, explicitly stating this on the documentation helps ensure compliance.

Similarly, when software sales include services like installation or training, ensuring that the software itself is delivered digitally can prevent the entire transaction from being taxed. Clear documentation of the delivery method is essential to avoid issues.

It’s also worth noting that Missouri has not adopted the standardized definitions for "specified digital products" used by states participating in the Streamlined Sales and Use Tax Agreement.

26. Montana

Tax Exemption Status

Montana stands out by not imposing a state-level sales tax, which means all digital products are tax-free. The Montana Department of Revenue clarifies:

"The Wayfair decision does not affect Montanans purchasing goods or services online because Montana does not have a general sales tax." – Montana Department of Revenue

Unlike states such as California or New York that apply sales taxes with occasional exemptions for digital products, Montana’s approach is straightforward – no sales tax on anything, including digital goods. This positions Montana among a small group of states – alongside Alaska, Delaware, New Hampshire, and Oregon – that operate without a general sales tax. This framework eliminates the selective taxation seen in other states, creating a simpler and more predictable system for digital transactions.

Exempt Digital Products

With no state sales tax, all digital products in Montana are completely exempt. This includes:

- Downloaded software and updates

- Streaming services for music and video

- E-books and digital publications

- Online courses

- Subscription-based digital content

There’s no need for exemption certificates in Montana, as the tax-free status applies universally to digital offerings. From streaming platforms to digital textbooks, these products remain untaxed, reflecting Montana’s streamlined approach to digital commerce. However, businesses based in Montana that sell to customers in other states may need to register a business in the US and comply with tax collection requirements if they meet economic nexus thresholds.

Key Exceptions

While digital products are untaxed, Montana residents still pay other non-sales taxes. For example, federal taxes on airline tickets and local taxes on hotel stays or rental cars still apply. Additionally, Montana businesses that sell across state lines must carefully navigate tax obligations in states where their customers reside, as they may be required to collect and remit sales tax in those jurisdictions.

27. Nebraska

Tax Exemption Status

Nebraska applies the principle of physical parity when it comes to taxation: if a product is taxable in its physical form, its digital equivalent is also taxable. This policy has been in place since October 1, 2008, when the state began taxing digitally delivered products.

"Digital works delivered electronically… are subject to Nebraska sales and use tax if they are taxable when delivered in a tangible form." – Sales Tax Institute

The state’s base sales tax rate is 5.5%, but local jurisdictions can add up to 2%, resulting in a maximum combined rate of 7.5% in some areas. Nebraska uses a destination-based tax system, meaning the applicable rate is determined by the buyer’s location, not the seller’s. Remote sellers are required to register and collect tax if they meet the threshold for substantial business activity in the state.

Taxable Digital Products

Nebraska’s taxation of digital products is comprehensive, aligning with its physical parity approach. Taxable items include downloaded software, eBooks, music, movies, audiobooks, and digital codes. Streaming services are also taxed, regardless of the length of access provided.

For instance, an online bookstore charging $9.99 per month for an eBook subscription to a customer in Omaha (where the total tax rate is 7%) would need to collect approximately $0.70 in sales tax each month.

Exempt Digital Products

Unlike many other digital goods, Software-as-a-Service (SaaS) is generally not subject to Nebraska’s sales tax. The state classifies SaaS as a service rather than the sale of tangible property, which exempts most cloud-based tools like CRM systems and project management software. However, there are exceptions. Certain security-related SaaS products, such as firewalls and encryption tools, may be taxable based on state guidance.

"In Nebraska, SaaS (Software-as-a-Service) is generally not subject to sales tax. However, informal guidance from the state indicates that specific Security SaaS products may be taxable." – Kintsugi

For example, a cybersecurity company charging $100 per month to a business in Grand Island (with a 6.5% total tax rate) would need to collect $6.50 in sales tax under these rules. Additionally, digital newspapers published at least weekly, medical records provided to patients, and certain public records are explicitly exempt from sales tax.

Key Exceptions

Nebraska provides additional clarifications for certain scenarios. In cases of bundled transactions involving both physical and digital goods, businesses must itemize taxable and nontaxable components on invoices to ensure proper tax application. Sellers are also advised to maintain detailed transaction records and exemption certificates (Form 13) to prepare for potential audits by the Nebraska Department of Revenue. Additionally, digital codes are taxable at the point of sale.

28. Nevada

Tax Exemption Status

Nevada takes a distinct approach when it comes to taxing digital products. The state does not classify electronically delivered products as "tangible personal property", which means they are exempt from sales and use tax.

"Specified digital products are not considered tangible personal property in Nevada and are not subject to sales and use tax." – Avalara

While Nevada’s standard sales tax rate is 6.85% (with local rates pushing it as high as 8.24%), these rates don’t apply to digital goods. As a member of the SSUTA, Nevada stands out by exempting certain digital products, unlike many other states that impose taxes on them.

Exempt Digital Products

The exemption in Nevada applies to a broad range of digital products delivered electronically. This includes:

- Computer software

- Streaming services for movies and music

- Digital books and electronic magazines

- Clip art and digital audio files (like podcasts and ringtones)

- Program code

Whether customers gain permanent ownership or only temporary access through subscriptions, these products remain tax-free.

For instance, a software company charging $50 per month for a subscription in Las Vegas wouldn’t need to collect sales tax, even though local rates can exceed 8%. Similarly, streaming platforms offering music or video content avoid taxation, unlike in neighboring states where such services are often taxable. Nevada’s clear focus on electronic delivery gives it a unique position in this area.

Key Exceptions

The method of delivery is the deciding factor for tax exemption. To qualify, digital products must be delivered entirely electronically – whether via download or streaming. If the same product is provided on physical media, like a USB drive or CD, it becomes taxable as tangible personal property.

Businesses should keep detailed records of their delivery methods to prove that no physical component was involved, especially in case of an audit. Additionally, since Nevada doesn’t tax digital products, these sales are excluded when calculating the state’s economic nexus thresholds for remote sellers.

FAQs

How do states decide if a digital product is taxable?

States decide how to tax digital products by classifying them as either tangible or intangible property. In some cases, states treat digital goods as tangible property, often because of their perceived value or the way they are delivered. On the other hand, some states completely exempt digital products from taxation or apply varying rules based on the type of product and its delivery method.

Is streaming taxable if I don’t own the content?

Streaming digital content is typically not subject to sales tax if you don’t actually own the content. Many states categorize digital streaming services as either non-tangible personal property or as a service, both of which are often exempt from sales tax. That said, tax laws differ from state to state, so it’s crucial to review the specific rules in your location to stay compliant.

When do remote sellers have to start collecting digital sales tax?

Remote sellers are required to start collecting digital sales tax once they meet the economic nexus criteria in a state. This usually occurs when sales exceed certain thresholds, like $100,000 in revenue or 200 transactions in a year. Since these thresholds differ from state to state, it’s crucial to understand the specific rules in each state where your business operates.