Struggling to decide between a business credit card and a business loan? Here’s the bottom line:

- Business Credit Cards: Ideal for smaller, short-term expenses like office supplies, travel, or utilities. They offer revolving credit, quick approvals, and perks like cash back or travel rewards. However, they come with higher interest rates (18%-36%) and lower credit limits (average: $56,100).

- Business Loans: Best for large, long-term investments like real estate, equipment, or expansion. They provide a one-time lump sum, lower interest rates (6%-30%), and higher borrowing limits (up to $5M+). But they take longer to approve and often require collateral.

Quick Comparison

| Feature | Business Credit Card | Business Loan |

|---|---|---|

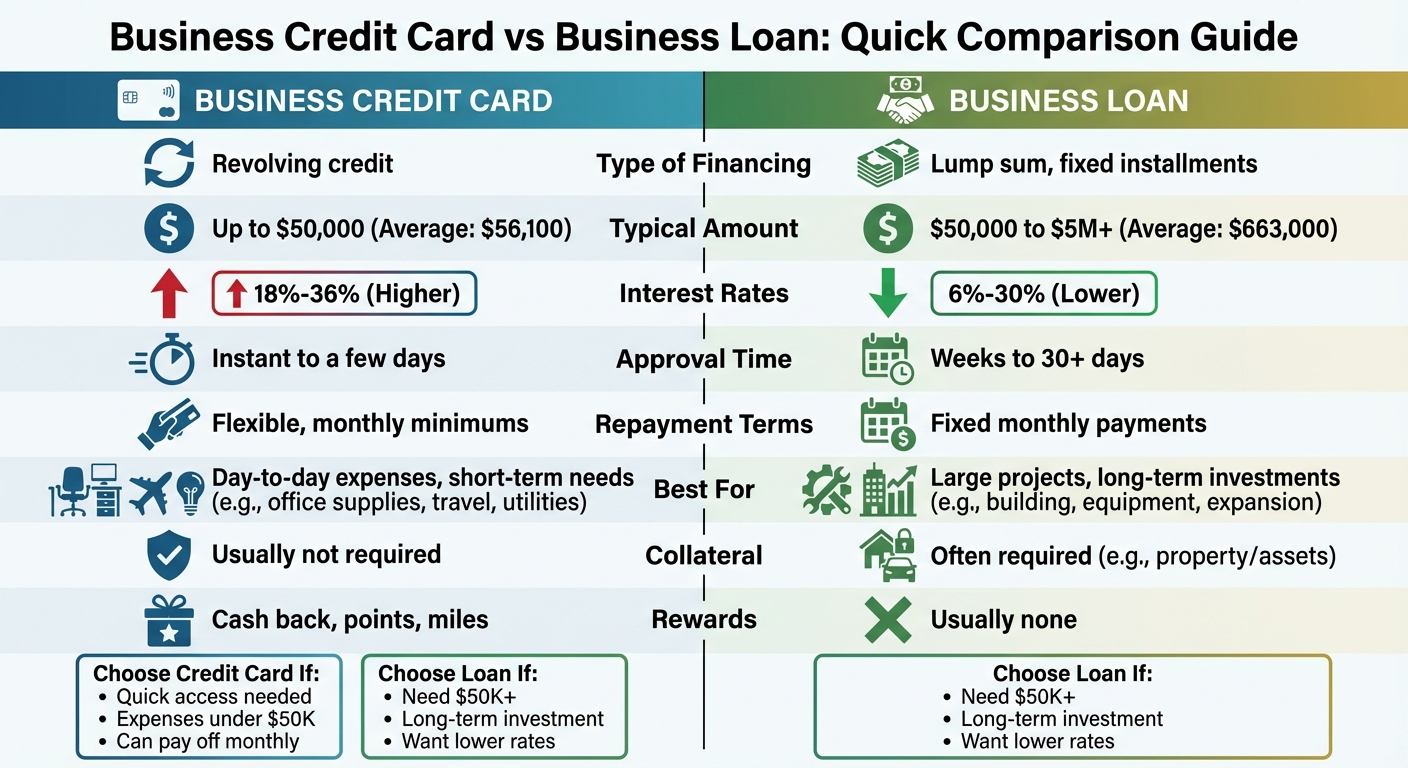

| Type of Financing | Revolving credit | Lump sum, fixed installments |

| Typical Limit/Amount | Up to ~$50,000 (avg. $56,100) | $50,000 to $5M+ (avg. $663,000) |

| Interest Rates | 18%-36% | 6%-30% |

| Approval Time | Instant to a few days | Weeks to 30+ days |

| Repayment Terms | Flexible, monthly minimums | Fixed terms |

| Best For | Day-to-day expenses, short-term | Large projects, long-term needs |

Key takeaway: Use credit cards for flexibility and immediate access to funds. Opt for loans when you need substantial funding with structured repayment. Your choice depends on how much you need, how fast you need it, and your repayment plans.

Business Credit Cards vs Business Loans: Main Differences

The key distinction lies in how funds are accessed and repaid. Business credit cards provide a revolving line of credit, allowing ongoing access to funds up to a set limit. In contrast, business loans involve a one-time disbursement of funds, repaid through fixed installments over a predetermined term.

Approval processes also vary significantly. Credit card applications are typically straightforward, often completed online, with decisions made in minutes or within a few days. On the other hand, business loans demand more detailed documentation – such as tax returns, cash flow statements, and business plans – and can take weeks or even a month to process and approve.

When it comes to qualifications, credit cards are generally easier to secure. They largely depend on personal credit and require minimal business history. Business loans, however, often require a track record of at least one year in operation, strong financial statements, and, in many cases, collateral or a personal guarantee.

Cost structures also differ. Credit cards typically have higher variable interest rates, ranging from 18% to 36%. However, you can avoid interest entirely by paying the balance in full each month. Business loans, by comparison, usually offer lower interest rates – between 6% and 30%, with traditional bank loans averaging 6% to 12% – but interest accrues regardless of early repayment.

These differences highlight how each option caters to different financial needs and levels of flexibility.

Side-by-Side Comparison: Business Credit Cards and Business Loans

| Feature | Business Credit Card | Business Loan |

|---|---|---|

| Type of Financing | Revolving line of credit | Installment loan |

| Typical Funding Amount | Up to $50,000 (Average: $56,100) | $50,000 to $5M+ (Average: $663,000) |

| Interest Rates | 18%–36% variable | Fixed or Variable: 6%–30% |

| Repayment Terms | Flexible; minimum monthly payments | Fixed monthly payments over a set term |

| Approval Time | Instant to a few days | Several days to 30+ days |

| Qualification | Good/excellent personal credit | Strong financials, 1+ year in business, collateral |

| Typical Uses | Day-to-day expenses, travel, supplies | Real estate, equipment, expansion |

| Rewards | Cash back, points, miles | Usually none |

| Collateral | Usually not required | Often required |

sbb-itb-ba0a4be

Business Credit Cards: How They Work and What to Expect

What Are Business Credit Cards?

A business credit card is essentially a revolving line of credit tailored for business owners. It helps manage cash flow and cover everyday operational costs. You can borrow, repay, and borrow again – up to your credit limit – as long as your account remains in good standing.

One of the biggest perks? personal and business finances separate, making bookkeeping and tax prep a whole lot easier. Plus, using one responsibly helps establish a business credit history, which can be a game-changer when you need larger financing in the future. For context, the average business credit card limit is about $56,100, though corporate cards can go as high as $100,000 to $500,000 or more.

However, most business credit cards come with a personal guarantee. This means you’re personally on the hook for the debt if your business can’t pay it back. Unlike personal credit cards, these often lack strong consumer protections, such as those for fraud or billing disputes. On the bright side, issuers typically provide tools to streamline expense management – think receipt matching, employee cards with spending limits, and real-time transaction tracking.

Now that you know the basics, let’s dive into the benefits of using a business credit card.

Advantages of Business Credit Cards

Business credit cards come with several perks, making them a convenient option for short-term and flexible financing.

One standout advantage is speed and flexibility. Approvals are often quick – sometimes instant or within a few days – giving you fast access to funds when you need them most. Most cards also offer a 21–25 day grace period, meaning if you pay off your balance within that time, you won’t pay any interest.

Another major selling point? Rewards programs. Many business credit cards let you earn cash back, points, or travel miles on expenses like shipping, advertising, and office supplies.

"Not only will having a credit card help build your business credit… but you can also benefit from any rewards and perks associated with your card".

Arshia Gupta, Small Business Card product executive at Bank of America, emphasizes this point. Some cards even offer 0% introductory APR periods, which can be a lifesaver for managing short-term cash flow without incurring interest costs.

While these benefits are appealing, it’s equally important to weigh the potential downsides.

Disadvantages of Business Credit Cards

Before committing, it’s important to understand the limitations of business credit cards, especially when comparing them to other financing options like business loans.

The biggest downside? Higher interest rates. With APRs typically ranging from 18% to 36%, business credit cards are far more expensive than traditional loans, which average 6% to 12% from banks. Carrying a balance can quickly lead to significant interest costs.

Another limitation is the lower credit limits. While the average business credit card limit is $56,100, loans can range from $50,000 to $5 million or more. This makes credit cards less practical for large expenses like real estate or major equipment purchases. Additionally, if spending isn’t carefully tracked, it’s easy to rack up debt. Late payments can harm both your business and personal credit scores.

Understanding these pros and cons can help you decide if a business credit card fits your financial strategy.

Business Loans: How They Work and What to Expect

What Are Business Loans?

A business loan is a lump sum of money provided upfront by a lender – this could be a bank, credit union, or online lender. Unlike a revolving line of credit, this type of loan gives your business a one-time cash injection. Repayment happens in fixed installments over a set period.

To apply, you’ll need to gather detailed financial documents. Lenders typically evaluate your business credit score, revenue, and operating history. Expect to provide tax returns, cash flow projections, and a comprehensive business plan.

The most common type is a term loan, where you receive a specific amount and repay it over a fixed term. SBA loans, backed by the government, offer lower interest rates and longer repayment terms – sometimes up to 25 years. Equipment loans are tailored for purchasing machinery or vehicles, with the equipment itself often acting as collateral. If you’re looking to cover daily expenses while waiting for cash flow to stabilize, working capital loans are a good option.

Business loans can either be secured (requiring collateral such as real estate or equipment) or unsecured (based on creditworthiness alone). Secured loans often come with better rates but put your assets on the line if you’re unable to repay.

Choosing the right financing option for your business needs is crucial – this alignment ensures you can maximize the benefits of the funding.

Advantages of Business Loans

One of the biggest perks of business loans is the access to large sums of money. Loans can range from $50,000 to over $5 million, with an average loan size of $663,000. This makes them ideal for significant investments like purchasing real estate, machinery, or funding business expansion.

Another advantage is lower interest rates. Traditional bank loans often have rates between 6% and 12%, while the broader market ranges from 6% to 30%. Compare that to business credit cards, which typically carry rates of 18% to 36%.

Fixed monthly payments are another plus. These predictable installments make it easier to manage your budget and cash flow. SBA loans, in particular, stand out for their favorable terms, including longer repayment periods and lower interest rates due to government backing.

"Any situation where you need the machine working asap so business can keep moving, and you’ll be making payments over time as the expenses are larger, will make business loans the better choice compared to revolving credit." – SmallBusinessLoans.com

These benefits make business loans a valuable tool for businesses looking to grow or make large purchases.

Disadvantages of Business Loans

Despite their advantages, business loans come with challenges. The application process can be lengthy and requires extensive documentation. While business credit cards can be approved in days, business loans often take a month or more. Lenders usually require at least a year in business, strong revenue, and good credit scores. Even if you qualify, you may need to provide collateral, which puts your assets at risk if you can’t keep up with payments.

Another drawback is the lack of flexibility. Unlike credit cards, which let you borrow, repay, and borrow again, a business loan gives you a one-time lump sum. If you need additional funds, you’ll have to go through the application process all over again. Fixed monthly payments are another limitation – these remain the same regardless of how your revenue fluctuates, which can strain your cash flow during slower months. Additionally, some loans, like SBA loans, may have prepayment penalties if you try to pay off the balance early.

Weighing these downsides against the benefits can help you decide if a business loan is the right fit for your goals and timeline.

Pros and Cons Comparison

When deciding between financing options, understanding the trade-offs can help you make an informed choice. Business credit cards and business loans each bring their own set of benefits and limitations, impacting how you manage cash flow, interest, and access to funds.

Interest rates are a key difference. Business loans typically range from 6% to 30%, while credit cards often carry higher rates, between 18% and 36%. Additionally, the average business loan amount is around $663,000, compared to the much smaller average credit card limit of $56,100.

Another critical distinction lies in repayment flexibility. Credit cards offer revolving credit, letting you borrow, repay, and borrow again as needed, with the option to make minimum monthly payments. In contrast, loans come with fixed monthly installments over a set term, which provides predictability but limits flexibility if cash flow becomes tight.

Here’s a quick breakdown of the key features:

| Feature | Business Credit Cards | Business Loans |

|---|---|---|

| Advantages | • Quick approval, often within days • Revolving credit replenishes as you pay • No interest if balance is paid in full monthly • Rewards like cash back or travel points |

• Lower interest rates • Access to larger amounts – up to $5 million • Fixed payments simplify budgeting • Longer repayment terms available |

| Disadvantages | • High interest on carried balances • Lower borrowing limits (typically around $50,000) • Risk of overspending and accumulating debt • Possible annual and late payment fees |

• Stricter approval criteria, often requiring collateral • Slower funding process, sometimes 30 days or more • One-time lump sum without revolving access • Potential prepayment penalties |

Your choice depends on your business needs and repayment timeline. Credit cards are ideal for short-term expenses you can pay off within a billing cycle. On the other hand, loans are better suited for significant investments where lower rates and higher limits outweigh the stricter terms.

When a Business Credit Card Makes Sense

A business credit card is a smart choice when you need quick and flexible access to funds for everyday expenses that you can pay off promptly. Think of costs like software subscriptions, office supplies, utilities, or advertising. These cards are designed to handle short-term financial needs rather than large, long-term investments.

They’re also incredibly useful for travel and entertainment costs. Whether it’s booking flights, securing hotel stays, or covering client meals, a business credit card not only provides immediate purchasing power but can also earn rewards like cash back or travel points – benefits that can directly support your business.

"A business credit card provides revolving line of credit that you don’t have to continuously reapply for – a real plus to support the ups and downs of your cash flow" – Live Oak Bank

Another advantage is that using a business credit card helps establish a credit history for your company. This can be a stepping stone to securing larger financing options in the future. Keeping personal and business finances separate is crucial, especially when you consider that around 38% of small businesses fail due to insufficient capital.

To make the most of a business credit card, it’s essential to pay off the balance in full each month. By doing so, you avoid interest charges, which can range between 18% and 36%. Carrying a balance beyond 30 days can quickly negate any rewards or convenience due to these high rates.

Next, let’s look at situations where a business loan might be a better fit for your financial needs.

When a Business Loan Makes Sense

A business loan is a smart choice when you’re dealing with major, one-time expenses that go beyond what a credit card can handle. Think about situations like buying real estate, investing in heavy machinery, acquiring another business, or opening a new location. These kinds of investments often require funding in the range of $50,000 to over $5 million. Clearly, credit cards aren’t built for this scale, which is where loans come in.

Loans also tend to be more cost-effective for large purchases. While business credit cards often carry interest rates between 18% and 36%, traditional business loans usually offer much lower rates, typically between 6% and 12%. For example, if you take out a $50,000 loan at an 8% interest rate over six years, the total interest would be around $23,000. That’s a more affordable way to finance compared to credit cards.

"If your business needs to cover larger costs – such as scaling up operations or purchasing expensive equipment – a business loan can provide a lump sum of money up front." – Capital One

Another advantage of loans is the predictability of repayment. Fixed monthly installments make it easier to manage cash flow and plan for the future, as mentioned earlier.

Business loans are ideal for revenue-generating investments, like purchasing production equipment, securing operational real estate, or stocking up on bulk inventory. On average, business loans amount to about $663,000. If you’re eligible, SBA loans are an excellent option, offering lower rates and more flexible terms. However, keep in mind that SBA loans often come with stricter requirements, such as detailed business plans, tax returns, and cash flow projections.

How to Decide What’s Right for Your Business

Choosing the right financing option boils down to three key factors: how much you need, how quickly you need it, and how you plan to repay it. Here’s a quick breakdown:

- For smaller expenses under $50,000 – like office furniture, software subscriptions, or utilities – a business credit card is often the better choice.

- For larger investments, ranging from $50,000 to $5 million, a business loan typically makes more sense.

Cash Flow Considerations

Your revenue patterns play a big role in the decision. If your cash flow fluctuates, a credit card offers flexibility. You can borrow just what you need and repay as funds come in, avoiding the commitment of fixed monthly payments. On the other hand, if your revenue is steady and you’re making long-term investments (like buying a warehouse or expanding operations), a loan’s predictable installments and lower interest rates make budgeting easier.

Speed of Access

Timing matters. Credit cards provide near-instant access to funds, making them ideal for emergencies – like an unexpected equipment repair or a sudden cash flow gap. Loans, however, can take anywhere from two weeks to over a month to process, which is better suited for planned, long-term projects.

Matching the Right Option to Your Needs

Here’s a handy table to help you determine which financing option works best for different scenarios:

| Business Situation | Recommended Option | Why It Fits |

|---|---|---|

| Covering monthly utility bills | Business Credit Card | Automates payments; may earn rewards on recurring expenses. |

| Purchasing a $200,000 warehouse | Business Loan | Large lump sum with predictable, long-term repayment. |

| Buying office furniture ($5,000) | Business Credit Card | Small expense; easy to pay off quickly to avoid interest. |

| Scaling operations or opening a new location | Business Loan | High capital need; fixed installments and lower interest rates aid planning. |

| Emergency equipment repair | Business Credit Card | Immediate access to funds prevents costly downtime. |

| Financing slow-moving inventory | Business Loan | Lower rates make sense for inventory that takes months to sell. |

Credit Readiness

Think about your business’s credit profile. If you’re still building credit, a business credit card is often easier to qualify for than a loan, which usually requires strong financials, collateral, or a proven track record. Plus, responsible credit card use helps establish a solid credit history, improving your chances of securing loans in the future.

Conclusion

When deciding between a credit card and a loan, the choice boils down to your specific financial needs and goals. Credit cards are ideal for managing everyday expenses, bridging short-term cash flow gaps, and earning rewards. On the other hand, loans are better suited for major, long-term investments like equipment or real estate, offering lower interest rates and predictable repayment schedules.

"Deciding which option suits your situation best is important for the success of your business." – Richard Moy, Finance Writer, Ramp

As covered earlier, credit cards shine in flexibility and speed, especially when balances are paid in full each month – turning them into a zero-interest tool that also earns rewards. However, for extended repayment periods, loans are the more cost-effective option, with interest rates typically ranging from 6% to 12%, compared to credit cards’ much higher rates of 18% to 36%.

Credit cards provide quick and ongoing access to funds with fewer qualification hurdles, making them a good starting point for building financial credibility. Loans, while requiring more time to process, offer larger lump sums and structured repayments, making them better for significant investments.

Ultimately, there’s no one-size-fits-all solution. Carefully assess your capital requirements, the urgency of your needs, and your ability to repay. Choosing the right financing option can fuel your business growth without unnecessary financial strain.

FAQs

Will a business credit card affect my personal credit score?

A business credit card can affect your personal credit score if you’re a sole proprietor or if you personally guarantee the card. In these situations, the card’s activity might be reported to personal credit bureaus, which could impact your personal credit history.

What documents do I need to apply for a business loan?

To apply for a business loan, you’ll usually need to gather some essential documents. These often include your business’s official name, tax ID number, financial statements like profit and loss statements, bank statements, and a detailed business plan. Lenders use these to assess your financial stability and determine if you can repay the loan.

Can I use both a business loan and a business credit card?

Yes, you can use both at the same time since they fulfill different needs. A business credit card works well for everyday expenses and provides access to revolving credit. On the other hand, a business loan gives you a lump sum that’s better suited for larger investments or growth-related projects. Using both together can help you handle cash flow, cover short-term expenses, and work toward long-term financial objectives efficiently.