An LLC, or Limited Liability Company, is a business structure in the U.S. that protects personal assets from business liabilities. It combines the liability protection of a corporation with the simplicity of a sole proprietorship or partnership. LLCs also offer flexible tax options, including default pass-through taxation to avoid double taxation.

Key Types of LLCs:

- Single-Member LLC: For solo owners. Simple to manage, taxed as a sole proprietorship by default.

- Multi-Member LLC: For businesses with two or more owners. Taxed as a partnership unless another option is chosen.

- Series LLC: Allows separation of assets and liabilities under one umbrella. Common for real estate investors.

- Professional LLC (PLLC): Designed for licensed professionals like doctors or lawyers. Protects against business debts but not personal malpractice.

Choosing the Right LLC:

- Single Owner? Go for a Single-Member LLC.

- Multiple Owners? A Multi-Member LLC is a good fit.

- Licensed Professional? Check if your state requires a PLLC.

- Managing Multiple Assets? Consider a Series LLC for liability separation.

Pro Tip: Always check your state’s laws, as not all LLC types are available in every state.

Quick Comparison Table:

| LLC Type | Best For | Default Tax Treatment |

|---|---|---|

| Single-Member LLC | Solo entrepreneurs | Sole Proprietorship |

| Multi-Member LLC | Co-owners, family businesses | Partnership |

| Series LLC | Real estate, asset management | Varies by state |

| Professional LLC | Licensed professionals | Varies (often Sole Proprietorship or Partnership) |

LLCs offer flexibility, liability protection, and tax advantages, making them a popular choice for small business owners. The right type depends on your business structure, state regulations, and specific needs.

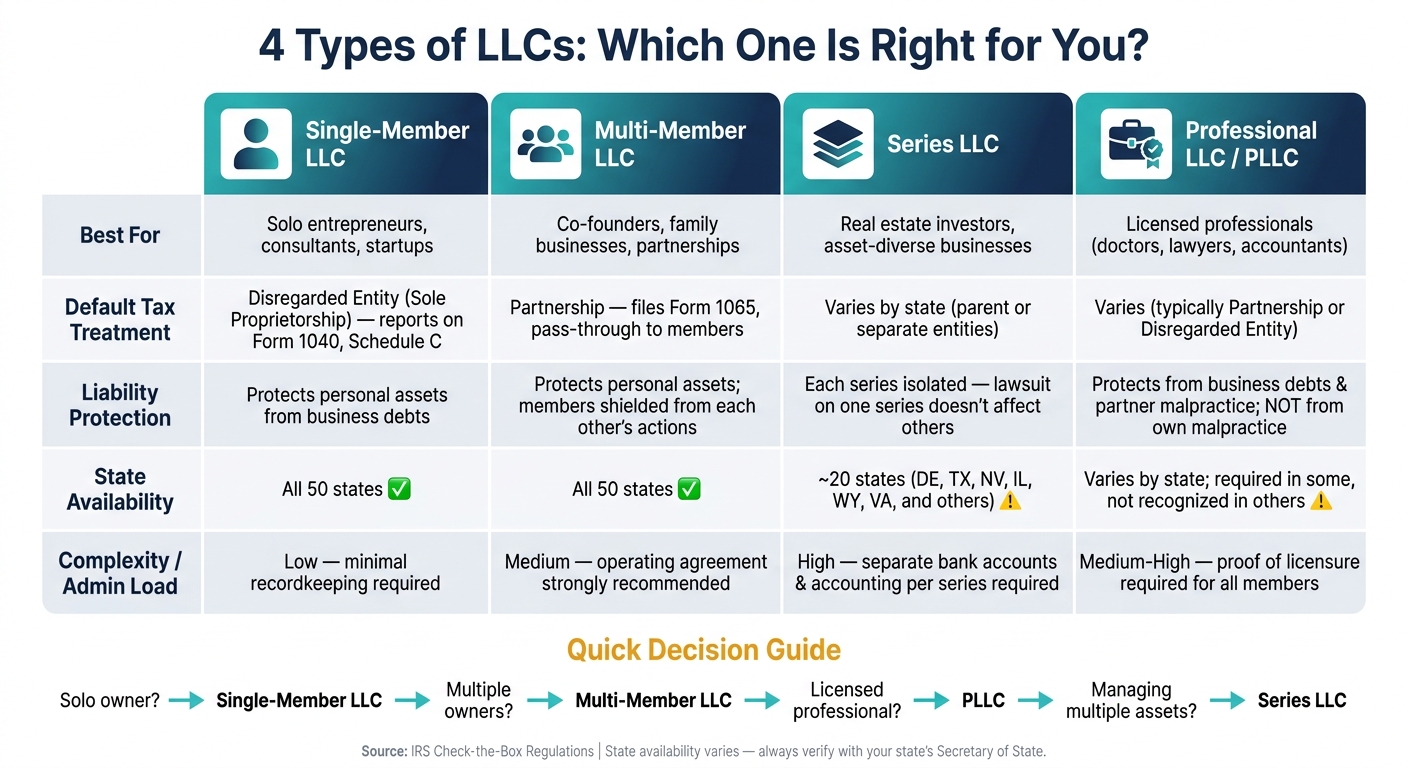

Types of LLCs Explained

When it comes to LLCs, one size doesn’t fit all. The type of LLC you choose shapes how your business is taxed, the extent of liability protection, and even who’s eligible to own it. Let’s break down the four main types so you can decide which one works best for your needs.

Single-Member LLC

A single-member LLC (SMLLC) has just one owner, which can be an individual or another legal entity. For tax purposes, the IRS considers it a disregarded entity. Essentially, this means the business’s income and expenses are reported directly on the owner’s personal tax return – similar to how a sole proprietorship works. This keeps tax filing straightforward.

But here’s the catch: as the sole owner, you’re responsible for self-employment taxes on your share of the business’s net income. Since you’re not technically an employee of your own business, this tax burden can add up. One way to potentially ease this is by opting for S-corp taxation, which we’ll discuss in the LLC Tax Classification Options section.

SMLLCs are allowed in all 50 states, but the level of protection from creditors – especially through "charging order" laws – varies depending on the state. This balance between liability protection and simplicity makes SMLLCs a popular choice for solo entrepreneurs.

Multi-Member LLC

A multi-member LLC (MMLLC) has at least two owners, known as members. By default, the IRS treats it as a partnership for tax purposes. This means the LLC itself files an informational return, but profits and losses are passed through to the members, who report them on their individual tax returns.

Ownership in an MMLLC can be divided flexibly – members can hold varying percentages and take on different roles. For smaller teams, a member-managed vs. manager-managed setup might work best, while larger groups often appoint managers to handle day-to-day operations. Unlike S-Corps, which limit ownership to 100 shareholders, an MMLLC can have an unlimited number of members.

For those looking for more specialized options, there’s the Series LLC, which offers additional layers of protection.

Series LLC

A series LLC is a more advanced setup where a parent LLC oversees multiple internal "series." Each series functions like a separate unit, with its own assets, liabilities, and members. The biggest perk here is liability isolation – if one series faces a lawsuit or debt, the others are typically shielded from the fallout.

This structure is especially appealing to real estate investors who want to manage multiple properties under one umbrella without exposing all their assets to the same risks. That said, to maintain this protection, each series must keep separate and accurate accounting records. Keep in mind, though, that not all states allow series LLCs, so you’ll need to check the rules where you operate.

Professional LLC (PLLC)

A professional LLC (PLLC) caters to licensed professionals like doctors, lawyers, accountants, and architects. It operates much like a standard LLC, offering protection from general business debts and shielding members from liability for each other’s professional mistakes.

However, a PLLC does not protect you from liability for your own malpractice. For instance, if a doctor in a PLLC makes a medical error, they’re still personally responsible. Because of this, malpractice insurance is a must, even if you form a PLLC. In many states, professionals are required to form a PLLC rather than a standard LLC, and the filing process often includes submitting proof of licensure for all members.

| LLC Type | Best Use Case | Default Tax Treatment |

|---|---|---|

| Single-Member | Solo entrepreneurs, consultants, startups | Disregarded Entity (Sole Proprietorship) |

| Multi-Member | Co-founders, family businesses, partnerships | Partnership |

| Series LLC | Real estate investors, asset-diverse businesses | Varies (parent or separate entities) |

| Professional LLC (PLLC) | Licensed professionals (doctors, lawyers, etc.) | Varies (typically Partnership or Disregarded Entity) |

sbb-itb-ba0a4be

How to Choose the Right LLC Type

Comparing LLC Types

Selecting the right LLC type involves weighing several practical factors, such as ownership structure, professional licensing needs, asset protection, management preferences, and state-specific regulations.

| Factor | What to Consider |

|---|---|

| Number of Owners | One owner? Opt for a Single-Member LLC. Two or more? Go with a Multi-Member LLC. |

| Professional Licensing | Professions like doctors, lawyers, architects, and accountants may need to form a PLLC due to legal requirements. |

| Asset Separation | If you manage multiple properties or high-risk assets, a Series LLC can help separate liabilities between them. |

| Management Style | Hands-on owners? Choose member-managed. Passive investors? Manager-managed might be better. |

| State Availability | Standard LLCs are available in all 50 states. Series LLCs, however, are restricted to certain states. |

| Compliance Load | Single-member LLCs require minimal recordkeeping. Multi-member or manager-managed LLCs usually need formal operating agreements and more detailed documentation. |

Keep in mind that most LLC types protect personal assets, provided the LLC is properly maintained. However, PLLCs do not protect members from personal malpractice liabilities. The main differences among LLC types typically revolve around tax treatment, management flexibility, and state-specific rules – not the personal liability shield.

Step-by-Step Decision Guide

- Determine Ownership Structure

If you’re the sole owner, a Single-Member LLC is often the simplest choice. It’s available in every state, easy to manage, and offers straightforward tax options. For businesses with co-founders or partners, a Multi-Member LLC is usually the way to go. In this case, drafting a solid operating agreement is critical. This document outlines key details like profit sharing, voting rights, and exit procedures – helping to avoid disputes later. - Check for Licensing and Asset Needs

If you work in a licensed profession like medicine, law, or architecture, verify your state’s rules. Many states require licensed professionals to form a PLLC, and skipping this step could lead to compliance issues with regulatory boards. If you own multiple assets with separate risks – especially in real estate – a Series LLC can protect each asset individually. This setup ensures that a lawsuit against one asset doesn’t jeopardize the others. - Evaluate the Need for a Series LLC

Only choose a Series LLC if you have a specific legal or tax reason. While it offers liability separation, it also comes with added administrative tasks, such as maintaining separate bank accounts and accounting for each series. For most businesses, a standard LLC is easier to manage. - Consider Geographic Factors

If you plan to operate in a different state from where you form your LLC, you’ll likely need to register as a Foreign LLC in the state where you conduct business. This involves extra fees and paperwork beyond your home state’s requirements.

State Rules and Filing Requirements

State Availability of LLC Types

Not every type of LLC is available in all states. While standard LLCs can be established in all 50 states, specialized structures like Series LLCs and Professional LLCs (PLLCs) face more restrictions.

Series LLCs are allowed for in-state formation in about 20 states, including Delaware, Texas, Nevada, Illinois, Wyoming, and Virginia. However, some states, like California, don’t permit forming a Series LLC locally but do allow foreign Series LLCs to register and operate there.

PLLCs, on the other hand, are governed by varying state rules. In certain states, licensed professionals – such as doctors or lawyers – must create a PLLC, while other states don’t recognize this structure at all. Since regulations differ widely, it’s crucial to review your state’s specific requirements.

For those prioritizing privacy, only Delaware, Nevada, New Mexico, and Wyoming allow anonymous LLCs. These states keep ownership details private and do not make them publicly accessible in their databases.

Filing and Compliance Basics

Once you’ve determined the LLC type your state permits, the next step is navigating the filing process and meeting compliance obligations. The process starts with filing Articles of Organization (or a Certificate of Formation in Delaware) with your state’s Secretary of State office. Filing fees vary widely, ranging from $50 to $500 depending on the state.

Every LLC is required to designate a registered agent – an individual or business with a physical address in the state of formation who is responsible for receiving legal and tax documents on behalf of the company. Additionally, most states mandate filing annual reports and paying ongoing fees to maintain your LLC’s active status.

To ensure smooth operations, draft an operating agreement that defines internal roles and responsibilities while reinforcing asset protection. Before filing, verify that your desired LLC name is available using your state’s Secretary of State database. The name must be unique and include a designator like "LLC", "L.L.C.", or "Limited Liability Company".

For added convenience, services like BusinessAnywhere provide registered agent services starting at $147 per year and offer operating agreement templates for $97 – helpful resources to keep your LLC compliant from the start.

LLC Tax Classification Options

After diving into the basics of LLC structures and filing requirements, it’s time to focus on an essential topic: your tax classification options.

Default Tax Treatment

The default tax treatment for an LLC is straightforward, thanks to pass-through taxation. The IRS automatically assigns a tax classification based on the number of members in your LLC.

For a single-member LLC, the IRS treats it as a sole proprietorship by default. This means the LLC is considered a "disregarded entity", and all profits and losses are reported directly on your personal tax return (Form 1040, Schedule C). For a multi-member LLC, the default classification is a partnership. In this case, the LLC files Form 1065, and income is passed through to members, who report it on their personal returns. Essentially, the LLC itself doesn’t pay federal income tax – profits and losses flow directly to the owners.

As Mark P. Keightley, an economic policy specialist, explains:

"The income of these businesses passes through to their owners and is taxed according to individual income tax rates."

However, there’s a catch: active members are generally responsible for the full 15.3% self-employment tax on their share of business income. This can be a significant expense for those with higher earnings. On the bright side, pass-through owners may qualify for the Section 199A deduction, which allows eligible business owners to deduct up to 20% of qualified business income (QBI). This deduction can provide substantial savings, so it’s worth discussing with your accountant.

Next, let’s explore how choosing a different tax classification could help you refine your tax strategy.

Electing S-Corp or C-Corp Taxation

If the default setup doesn’t align with your financial goals, LLCs have the flexibility to elect other tax classifications. Thanks to the IRS’s "check-the-box" system, you can change your tax status by filing the appropriate form – no need to restructure your business.

To elect S-Corporation taxation, you’ll need to file Form 2553. This option allows LLC owners to divide income into two parts: a "reasonable salary" (subject to payroll taxes) and distributions (which are not subject to self-employment tax). For high earners, this split can lead to significant tax savings. However, S-Corp status comes with restrictions: it’s limited to 100 members, all of whom must be U.S. residents or citizens, and the LLC can only issue one class of stock. If you’re interested in pursuing this option, companies like BusinessAnywhere can handle the Form 2553 filing for $97.

Alternatively, you can opt for C-Corporation taxation by filing Form 8832. While this election subjects profits to double taxation – once at the corporate level (a flat 21% rate) and again when distributed as dividends – it offers distinct advantages. C-Corps have no ownership restrictions, can retain earnings within the company, and are often the go-to structure for venture capital funding. If your long-term plans include raising outside capital or going public, C-Corp taxation might be worth considering.

| Tax Classification | Default or Opt-in | IRS Form | Key Advantage |

|---|---|---|---|

| Sole Proprietorship | Default (1 member) | N/A | Simplicity |

| Partnership | Default (2+ members) | N/A | Flexibility |

| S-Corporation | Opt-in | Form 2553 | Reduces self-employment taxes on distributions |

| C-Corporation | Opt-in | Form 8832 | Ideal for VC funding; retains earnings |

Keep in mind, electing S-Corp or C-Corp status comes with added responsibilities, like quarterly payroll, shareholder meetings, and extra filings. For startups or early-stage businesses, sticking with the default classification is often the simplest and most cost-effective choice – at least until your income grows enough to justify the extra administrative work. If you’re unsure which option is best for your situation, consider scheduling a tax and residency consultation to weigh your options before making a decision.

Key Takeaways

When it comes to choosing the right LLC structure, it’s all about aligning it with your business needs. With over 3.2 million domestic LLCs active in the U.S. as of 2021 – making up 71.7% of all partnerships – it’s clear that LLCs are a popular choice for their ability to protect personal assets and simplify taxes. However, not all LLCs are created equal, and selecting the wrong type can lead to complications later.

The key differences typically boil down to ownership, complexity, and purpose:

- A single-member LLC is ideal for solo entrepreneurs. It’s straightforward, offers pass-through taxation, and gives you complete control.

- A multi-member LLC works well for co-founders or family-run ventures but demands a strong operating agreement to prevent disputes.

- A Series LLC is useful for businesses managing multiple assets, such as rental properties, under one umbrella while keeping liabilities separate.

- A Professional LLC (PLLC) is often mandatory for licensed professionals like doctors, lawyers, or CPAs. It protects against a partner’s malpractice but not your own.

"Choosing the right LLC structure is about matching the structure to how your business actually operates." – Stripe

For most businesses, starting with a basic single- or multi-member LLC is a practical move. You can always revisit and adjust your structure as your business evolves, whether that means adding assets, expanding into new states, or bringing on more partners.

Finally, don’t overlook the importance of keeping your personal and business finances separate. This step is crucial to maintaining the liability protection an LLC provides.

FAQs

Can I switch my LLC from default taxation to S-corp later?

Yes, you can switch your LLC’s default tax status to an S-corp by filing Form 2553 with the IRS. This form is usually submitted within two months and 15 days after the beginning of the tax year or anytime during the tax year before the change takes effect. Make sure to carefully follow the IRS instructions to ensure your election is approved without issues.

Do I need separate bank accounts for each series in a Series LLC?

Yes, each series in a Series LLC must have its own bank account. This is crucial for maintaining the financial independence of each series and ensuring the liability protection that a Series LLC structure offers. Separate accounts help keep the finances of each series distinct, which is important for both legal compliance and effective financial management.

What liability protection does a PLLC not cover?

A PLLC provides limited liability protection for business debts and obligations, but it does not shield the owner from personal accountability for malpractice or professional misconduct. If an owner makes a mistake, acts negligently, or engages in unethical behavior while performing their professional duties, they remain personally liable for those actions.