When it’s time to leave your business, you have three main options: selling, merging, or closing. Each path has pros and cons, so choosing the right one depends on your goals, financials, and the state of your business. Here’s a quick overview:

- Selling: Offers the highest payout but requires preparation, like cleaning up financials and diversifying your customer base. Expect 6–12 months to complete the process.

- Merging: Combines your business with another for growth opportunities but may require you to stay involved. Success depends on financial alignment and smooth integration.

- Closing: The fastest option but often the least profitable. It involves liquidating assets, settling debts, and filing final taxes.

Planning 3–5 years in advance is key to maximizing value and avoiding last-minute stress. Whether you want a clean break or to stay partially involved, preparing your business for transferability is critical. Below, we’ll dive into each option step-by-step, including timelines, risks, and tax strategies.

Business Exit Strategy Comparison: Timelines, Costs, and Risks

Preparing Your Business for Exit

Getting your business ready for an exit requires thoughtful planning and a proactive approach. The goal is to make your business appealing and easy to transfer. The groundwork you lay before starting the sale process often determines how successful your exit will be. Whether you’re considering a sale, merger, or even liquidation, preparation is key.

Conducting an Exit-Readiness Assessment

Think like a buyer when evaluating your business. Start with your financial records – they’re the backbone of your business’s value. You’ll need at least three to five years of audited or reviewed financial statements.

Work with your accountant to adjust your EBITDA (Earnings Before Interest, Taxes, Depreciation, and Amortization). This involves removing non-recurring expenses, personal costs run through the business, and other one-time items to highlight the true earning potential, also known as "Seller’s Discretionary Earnings". A clear financial picture is crucial for attracting buyers.

Another area to examine is customer concentration. If one client accounts for more than 20% to 25% of your revenue, buyers may see this as a risk and discount your valuation. To avoid this, start diversifying your customer base well in advance – building new relationships takes time.

Operational readiness is just as important. Ask yourself: Could your business operate smoothly without you for three months? If not, it’s time to document standard operating procedures (SOPs), delegate responsibilities, and reduce reliance on your involvement.

Lastly, review your commercial contracts for any clauses that could complicate a sale, such as change-of-control provisions or assignment restrictions. Addressing these issues early can save you headaches during due diligence.

"A clean slate heading into due diligence reduces uncertainty discounts buyers may otherwise apply."

- Wendy G. Marcari, Member of the Firm, Epstein Becker Green

Once your financials and operations are in order, ensure your legal and tax structure is aligned with your exit goals.

Choosing the Right Business Structure

Your business structure – whether it’s an LLC, S-Corporation, or C-Corporation – plays a huge role in how sale proceeds are taxed and the flexibility of negotiations. Sellers often prefer S-Corporations or LLCs to avoid the double taxation that can come with C-Corporations.

Buyers, on the other hand, usually favor asset sales for tax advantages and to sidestep historical liabilities. Sellers, however, tend to prefer stock sales since they qualify for capital gains treatment, which is taxed at a lower rate than ordinary income. The structure you choose impacts your options and the amount you keep after taxes.

If your business is currently a sole proprietorship or partnership, consider converting to an LLC or electing S-Corp status well before your exit. An S-Corp tax election allows for pass-through taxation, meaning profits are taxed only at the individual level, not at the corporate level. This can significantly boost your after-tax earnings.

"The way your company is structured, whether as a corporation, S corporation, or limited liability company, will affect how sale proceeds are taxed."

- Wendy G. Marcari, Partner, Epstein Becker & Green, P.C.

For those planning ahead, Business Anywhere’s Business Registration service can help you set up the right structure, and their S-Corp Tax Election service ($97) simplifies filing IRS Form 2553 to optimize your tax position.

Once your structure is optimized, align your timeline and costs with your chosen exit strategy.

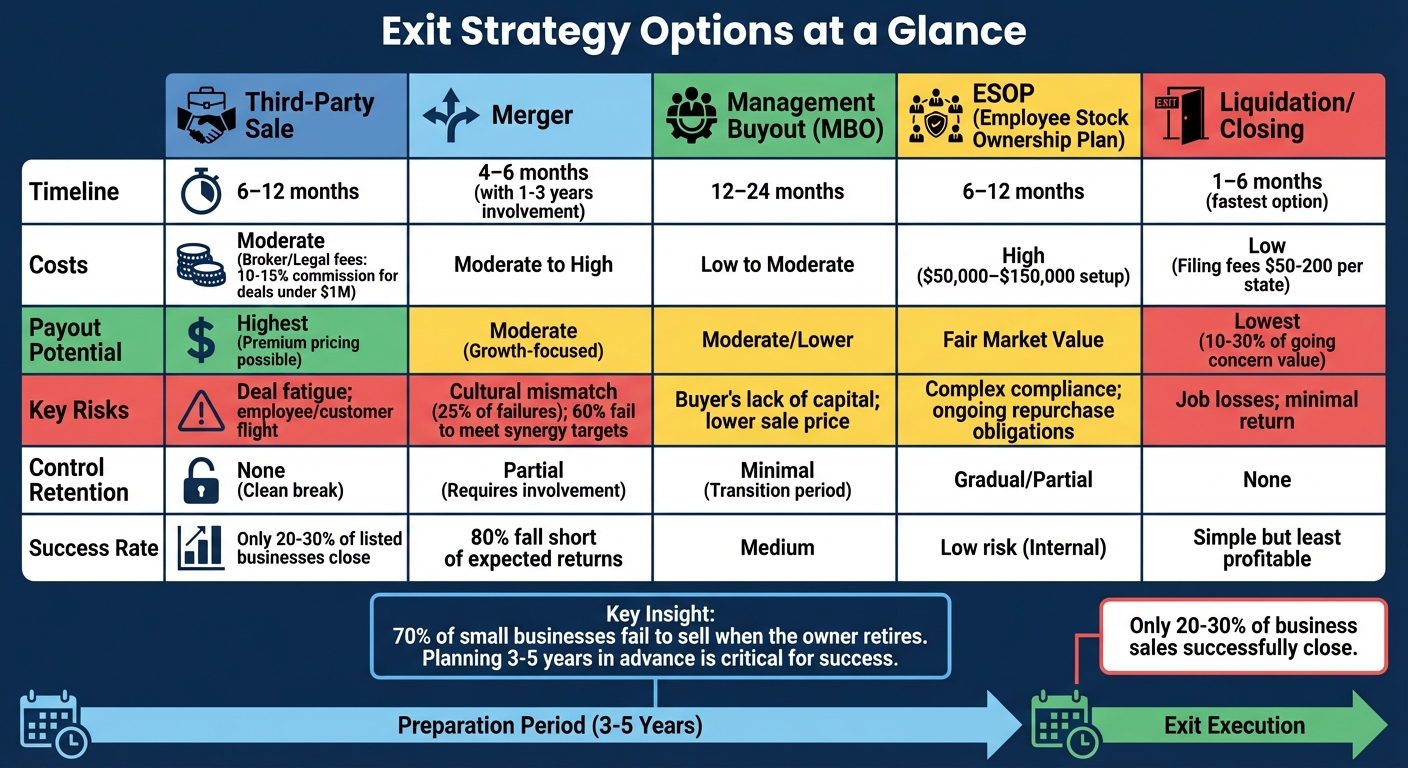

Preparation Timelines and Costs Comparison

Each exit strategy comes with its own preparation demands, timelines, and costs. Here’s a quick breakdown to help you plan:

| Strategy | Timeline | Costs | Key Risks |

|---|---|---|---|

| Third-Party Sale | 6–12 months | Moderate (Broker/Legal fees) | Deal fatigue; employee/customer flight |

| Management Buyout | 12–24 months | Low to Moderate | Buyer’s lack of capital; lower sale price |

| ESOP | 6–12 months | High ($50,000–$150,000) | Complex compliance; ongoing repurchase obligations |

| Family Succession | 2–5 years | Low (Tax planning) | Family dynamics; successor incompetence |

| Liquidation | 1–6 months | Low | Lowest financial return (10–30% of value); job losses |

If you’re aiming for maximum value, start cleaning up your financials three to five years before your exit. This gives you time to address customer concentration, reduce dependency on you, strengthen your management team, and resolve legal or regulatory issues.

For those considering liquidation, keep in mind that while it’s the fastest option, it typically recovers only 10% to 30% of the business’s value as a going concern. From a financial perspective, it’s often the least desirable path.

sbb-itb-ba0a4be

How to Sell Your Business: Step-by-Step

Selling a business can be a lengthy and intricate process. On average, it takes 6 to 12 months from listing to closing. However, only about 20% to 30% of businesses listed for sale successfully close a deal. To improve your chances, focus on three key phases: determining an accurate valuation, identifying the right buyers, and structuring the deal to safeguard your interests.

Valuing Your Business and Finding Buyers

Getting the valuation right is essential. This typically involves using multiple valuation methods to establish a credible range. For smaller, owner-operated businesses valued under $10 million, Seller’s Discretionary Earnings (SDE) is the go-to metric. Larger companies with established management teams usually rely on EBITDA.

To calculate an accurate valuation, normalize your financials. This means adjusting for one-time expenses, personal perks, and owner salaries to reveal the true earnings of the business. These adjustments directly impact the valuation multiple. For example:

- Small businesses with less than $1 million in SDE often sell for 2×–4× SDE.

- Mid-sized companies (with $1–10 million in EBITDA) typically sell for 4×–8× EBITDA.

As of Q3 2025, the median asking price for U.S. businesses was $352,000. However, risk factors like high customer concentration (where one client accounts for more than 10% to 15% of revenue) or heavy reliance on the owner can reduce your valuation by 20% to 40%. A professional valuation costs between $5,000 and $50,000, depending on the complexity of the business.

"Valuation is both an art and a science."

- Thomas Smale, CEO, FE International

After determining your valuation range, it’s time to find potential buyers. These typically fall into three categories:

- Strategic buyers: Competitors or partners looking for synergies, often willing to pay a 20% to 40% premium.

- Financial buyers: Private equity firms focused on return on investment.

- Individual buyers: Entrepreneurs or "corporate refugees" aged 40–59, who make up about 40% of the buyer market.

Create a "buyer map" with 50 to 100 potential acquirers. You can work with a business broker – who typically charges a 10% to 15% commission for deals under $1 million – or approach industry contacts directly. When reaching out, keep initial emails short (under 150 words) and highlight key metrics like revenue, growth rate, and profit. Always secure a signed Non-Disclosure Agreement (NDA) before sharing sensitive details. Start with lower-priority prospects to refine your pitch before reaching out to your top 10 to 30 ideal buyers.

Once you’ve identified serious buyers, you can proceed to formal negotiations.

Negotiation and Structuring the Sale

Formal negotiations typically begin with a Letter of Intent (LOI). This non-binding document outlines essential terms like the purchase price, deal structure (asset versus stock sale), exclusivity period, and closing conditions.

The structure of the deal is critical:

- Asset sales: Preferred by buyers since they can "step up" the asset basis for tax depreciation and avoid inheriting liabilities.

- Stock sales: Favored by sellers because they benefit from lower capital gains tax rates.

To avoid delays, ensure all your financial and legal documents are organized in a Virtual Data Room (VDR) before signing the LOI. During due diligence, buyers will scrutinize everything from customer contracts to employee agreements. Time is of the essence here – delays can derail the process.

A Quality of Earnings (QoE) report, which costs between $35,000 and $150,000, can help identify potential issues early and validate your adjusted EBITDA.

"Your broker represents the deal. Your attorney represents you. For every sale over $500,000, you need both."

- Alex Lubyansky, M&A Attorney, Acquisition Stars

Key terms to negotiate include:

- Earnouts: Payments tied to future performance.

- Non-compete clauses: To protect the buyer’s investment.

- Seller financing: Common with individual buyers.

- Transition assistance: To ensure a smooth handoff.

Strategic buyers may offer higher multiples due to the potential for cost savings and synergies.

Tax Planning for 2026 Sales

Tax planning plays a huge role in maximizing your net proceeds. If you’ve held Qualified Small Business Stock (QSBS) for over five years, you may qualify for up to $10 million in tax-free gains under Section 1202. This applies to C-Corporation stock issued after September 27, 2010, for businesses with less than $50 million in gross assets.

For stock sales, long-term capital gains rates (0%, 15%, or 20%, depending on income) apply if the business has been held for over a year. Asset sales, however, can trigger ordinary income tax rates – up to 37% in 2026 – on items like inventory and accounts receivable.

Timing is everything. If capital gains rates are expected to increase, closing before year-end might save you money. Work with a tax advisor to explore strategies like Grantor Retained Annuity Trusts (GRATs) or installment sales, which spread tax liability over time. Seller financing can also help defer taxes while providing steady income.

For S-Corporation owners, ensure your election is current and all distributions are well documented. If adjustments are needed, services like Business Anywhere’s S-Corp Tax Election ($147) can help optimize your tax position before the sale.

In 2024, small business sales rose by 5%, with 9,456 businesses sold. With 77% of buyers confident about purchasing at acceptable prices in the 2025–2026 market, now is a promising time to sell – provided you’ve done your homework and structured the deal carefully.

How to Merge Your Business: Step-by-Step

A merger isn’t the same as a sale. Instead of stepping away, you’re joining forces with another company to create something bigger and better. On average, this process takes about 4 to 6 months to complete. Businesses typically pursue mergers to achieve synergies – whether it’s combining complementary products, expanding into new regions, or benefiting from economies of scale that make the merged entity more valuable than the two companies on their own.

The process involves forming a new legal entity and conducting thorough due diligence. Both companies examine each other’s financials, operations, and compatibility to agree on a fair equity split, which is determined through professional valuations. Before finalizing the deal, key decisions must be made, such as selecting the CEO, deciding on board composition, choosing a headquarters, and naming the new company. It’s important to note that 25% of executives cite cultural mismatches as the main reason mergers fail.

Types of Mergers and Their Benefits

Mergers can take three main forms, each offering distinct benefits:

- Horizontal mergers: Combine competitors to increase market share and cut overlapping costs.

- Vertical mergers: Unite companies at different points in the supply chain, like a manufacturer merging with a distributor, to improve efficiency and control.

- Strategic mergers: Focus on leveraging each company’s strengths to fill gaps in the other.

Take the 2006 Disney–Pixar merger as an example. By retaining Pixar’s creative culture and leveraging Disney’s distribution capabilities, this partnership boosted revenue by over 20% within five years. Another case is the T-Mobile–Sprint merger, which aimed for a $6 billion cost synergy target by efficiently integrating networks while keeping customers happy.

Synergies from mergers generally fall into three categories:

- Cost synergies: Reducing duplicate roles and facilities.

- Revenue synergies: Cross-selling and bundling products.

- Financial synergies: Gaining tax advantages and reducing the cost of capital.

While cost synergies often appear within 1 to 2 years, revenue synergies can take up to 5 years to fully materialize. However, the road isn’t always smooth – over 60% of M&A deals fail to meet synergy targets, and 80% of mergers fall short of delivering expected shareholder returns shortly after closing.

"Synergies are the fruit that M&A deals hope to capture – but far too many deals end up with rotten apples."

- Ernie Lopez, Founder, MergerAI

To ensure realistic goals, conduct a bottoms-up analysis of areas like staffing, facilities, and IT systems to pinpoint overlaps. Use industry benchmarks, such as cost per revenue dollar, to validate your assumptions.

Integration Planning and Common Pitfalls

Once the merger type is chosen, the focus shifts to integration. Planning for this phase should begin during due diligence, not after the deal closes. Appoint an Integration Manager two weeks before announcing the merger to oversee the process through an Integration Management Office (IMO).

The first 100 days are critical. During this time, create a detailed plan with clear KPIs, timelines, and budgets. Track metrics like customer retention, order fulfillment rates, sales pipeline continuity, and financial reporting schedules. Establish an Executive Steering Committee (ESC) with senior leaders from departments like legal, finance, IT, and operations to guide decisions during the transition.

Ignoring cultural alignment can be disastrous, as seen in the Kraft–Heinz merger of 2015. Despite being a $45 billion deal supported by Warren Buffett and 3G Capital, the merger faltered due to clashing cultures – Kraft’s brand-focused approach didn’t mesh with 3G’s aggressive cost-cutting style. The result? A 60% drop in share price and years of stagnant growth. Today, CEOs often demand a 20% or more price discount for acquisitions involving cultural mismatches.

"In the absence of clear communication, employees will assume the worst."

Common mistakes include skipping thorough due diligence, inaccurate valuations, and losing key talent. Review contracts early to identify clauses that could give vendors or landlords leverage during the merger. Identify critical employees and consider offering retention bonuses or clear career paths to reduce uncertainty. Transparent communication about changes in roles, compensation, and policies is essential to maintaining productivity.

Flexible deal structures can also help. For example, earnouts tie part of the payment to future performance, while seller notes can bridge valuation gaps. Organizing essential documents in a Virtual Data Room early on can simplify due diligence. Looking ahead, due diligence increasingly includes evaluating ethical AI practices and human-AI collaboration frameworks.

A well-executed integration plan not only protects the value of the merger but also aligns with your broader business goals.

Dual‑Track Readiness for More Options

Keeping both merger and sale options open can strengthen your negotiating position. This "dual-track" approach involves preparing for either outcome, giving you flexibility. It includes getting your financials audit-ready, normalizing earnings, organizing legal documents, and identifying potential buyers or merger partners.

Since only 20% to 30% of businesses listed for sale successfully close a deal, having multiple paths improves your chances. Dual-track readiness requires upfront investments in valuations, legal advice, and streamlined financial records. Tools like Business Anywhere’s business formation tools can help ensure your corporate structure is set up for either option. Starting early is crucial – thorough preparation allows you to control the process and achieve the best outcome, whether through a sale or a merger that sets your business up for long-term success.

How to Close Your Business: Step-by-Step

Closing a business may feel like a daunting task, but for some, it’s the most suitable exit strategy. This process gives you full control over the shutdown, but it requires careful attention to legal and tax obligations. Skipping critical steps could leave you vulnerable to ongoing fees, unpaid taxes, or even identity theft if your business licenses remain active.

"If a business dissolution is not handled properly, you could face significant liability after you close your doors… Failure to properly dissolve a business can result in the business being considered active by the state, which entails continued compliance with state requirements, including filing annual reports and paying state taxes."

- Scarinci Hollenbeck, LLC, Business Attorneys

On average, the process takes 3 to 12 months, depending on your business structure and how quickly you can settle debts and complete state filings. Before making any major moves, consult with your lawyer and accountant to create a plan that addresses creditors’ concerns and avoids complications, or use a company dissolution service to manage the paperwork for you.

Legal Steps for Dissolution

Closing a business legally involves more than just shutting the doors. For corporations, the board must pass a resolution, and shareholders need to approve it. LLCs require member consent. These decisions must be recorded in meeting minutes or written resolutions. Once approved, you’ll need to file Articles of Dissolution (or a Certificate of Dissolution) with the Secretary of State in every state where your business is registered. Don’t forget to cancel all business licenses, permits, and DBA names to avoid renewal fees or potential identity theft.

Corporations must also file IRS Form 966 within 30 days of adopting the dissolution plan. If your business employs 100 or more workers, you’re required to comply with the Worker Adjustment and Retraining Notification (WARN) Act, which mandates 60 days’ notice for mass layoffs or plant closings.

When it comes to settling debts, there’s a strict order to follow:

- Secured creditors (lenders with collateral) come first.

- Next are employee wages and benefits.

- Then, tax authorities.

- Finally, unsecured creditors, like vendors and credit card companies.

Only after all debts are cleared can you distribute any remaining assets to shareholders or members. Collect outstanding accounts receivable as soon as possible – once customers know you’re closing, they may deprioritize payments.

"Before terminating your lease, selling equipment, and disconnecting utilities, talk to your lawyer and accountant. They’ll help you develop a plan to present to creditors, whose cooperation you need during this process."

If you sell assets instead of distributing them, use a non-recourse bill of sale to ensure the buyer assumes all associated risks. Keep your business bank account open for 30–60 days after closing to handle any outstanding checks or tax refunds. Finally, retain all business records for 7 years to safeguard against audits or disputes.

For help staying compliant during the dissolution process, Business Anywhere’s registered agent services can ensure you receive important state notices promptly.

Once the legal steps are complete, you’ll need to address your final tax obligations.

Tax Implications and Final Filings

Tax responsibilities don’t end when you close your business. You’ll need to file a final income tax return for the year your business shuts down. The type of return depends on your business structure:

- Sole proprietors use Schedule C (Form 1040).

- Partnerships file Form 1065.

- S-Corporations file Form 1120-S.

- C-Corporations file Form 1120.

Make sure to check the "Final Return" box on all applicable forms, including income, employment, and shareholder (K-1) tax filings.

If you sell business assets, report any gains or losses on Form 4797 (Sales of Business Property). Keep in mind that gains on depreciated assets may be subject to depreciation recapture, which is taxed as ordinary income instead of at the lower capital gains rate.

If you had employees, you’ll need to file final Forms 941 or 944 and Form 940 (FUTA) to report employment taxes. Pay all withheld income, Social Security, and Medicare taxes immediately, as these are held "in trust" and carry severe personal liability under the Trust Fund Recovery Penalty. This penalty equals 100% of the unpaid tax and can be applied to responsible individuals, including officers and directors. Provide final W-2s to employees by January 31 of the following year or sooner if requested. For contractors paid $600 or more, issue Form 1099-NEC.

"In general, the IRS considers the end of your tax year to be the date that your business closes."

While the IRS doesn’t cancel Employer Identification Numbers (EINs), you should send a formal letter to close your business account after filing all final returns. In many states, you’ll also need a tax clearance certificate before the Secretary of State will approve your dissolution. The IRS can audit your records for up to three years, or six years if you underreported income by more than 25%. To protect yourself, keep all tax and financial records for at least 7 years.

One potential benefit of voluntary closure is the ability to claim capital losses on your final return, which can help reduce your tax burden. If your business sponsored a qualified retirement plan like a 401(k), you’ll need to file a final Form 5500 by the last day of the seventh month after the final asset distribution.

Voluntary Closure vs. Bankruptcy Comparison

After completing your final filings, you’ll need to decide whether voluntary closure or bankruptcy is the best option for your financial situation.

| Feature | Voluntary Closure | Bankruptcy (Chapter 7) |

|---|---|---|

| Tax Impact | File final returns; claim capital losses to offset income. | Debt cancellation may be taxable income unless specific exclusions apply; requires IRS Bankruptcy Tax Guide. |

| Timeline | Typically 3–12 months depending on entity type and state processing. | Can be faster for liquidation but involves court-mandated schedules. |

| Costs | Filing fees ($50–$200 per state) plus professional fees for CPA/attorney. | High legal and court fees; assets liquidated by a trustee. |

| Control | Founders manage the wind-down and distribution of remaining assets. | Court-appointed trustee takes control of all business assets and operations. |

Voluntary closure allows you to negotiate with creditors and control the timing of asset sales, which can help you minimize taxes and maximize value. Bankruptcy provides an automatic stay that halts creditor collection efforts, but it also means relinquishing control to a court-appointed trustee. If your business can’t pay outstanding payroll taxes, you might qualify for an Offer in Compromise (IRS Form 656) to reduce the debt.

Understanding these options can help you choose the path that best aligns with your financial goals while protecting your personal assets. For assistance with federal reporting requirements during closure, Business Anywhere’s BOI filing services can help ensure compliance before dissolving your entity.

Key Considerations and Tax Planning for 2026 Exits

As you gear up for a potential exit in 2026, it’s crucial to keep several financial and tax factors in mind. Did you know that about 70% of small businesses fail to sell when the owner retires? And of those listed for sale, only 20–30% actually close a deal. To avoid these challenges, carefully assess the financial implications and risks of each exit option.

Evaluating Payout Potential and Risks

Different exit strategies can lead to vastly different financial outcomes. For example, selling to a third-party buyer often delivers the highest payout. Why? Competitive bidding and buyer synergies can drive up valuations. On the other hand, a management buyout (MBO) usually results in lower valuations since internal managers often lack sufficient capital and hold more negotiating power.

If you’re considering an Employee Stock Ownership Plan (ESOP), keep in mind that valuations are based on fair market value, as determined by an independent appraisal. Liquidation, however, typically yields the lowest returns, as it focuses solely on asset value.

Other factors, like operational dependence or high customer concentration, can significantly reduce your business’s valuation and make closing a deal more difficult. To safeguard your proceeds, consider negotiating indemnification caps at 10–15% of the purchase price for general claims. Escrow holdbacks – often 5–10% for 12 months – are also common to cover potential breaches. If you’re bridging valuation gaps with an earn-out, make sure to include operating covenants to prevent post-closing performance manipulation.

Here’s a quick comparison of exit options:

| Exit Option | Payout Potential | Risk Level | Control Retention |

|---|---|---|---|

| Third-Party Sale | Highest (Premium) | High (Due Diligence) | None (Clean Break) |

| MBO | Moderate/Lower | Medium (Financing) | Minimal (Transition) |

| ESOP | Fair Market Value | Low (Internal) | Gradual/Partial |

| Family Succession | Variable (Discounted) | High (Dynamics) | High (Mentorship) |

| Liquidation | Lowest (Asset Value) | Low (Simple) | None |

"If the business cannot run without you, it is worth less. Buyers want to know that revenue, customer relationships, and operations will continue after you leave."

- BuyerEdge

Once you’ve analyzed the risks and payout potential, the next step is to focus on tax strategies that can help you maximize your net proceeds.

Tax Tools and Timing Strategies

Smart tax planning could increase your net proceeds by 15–25%. Key changes coming in 2026 include the One Big Beautiful Bill Act (OBBBA), which permanently adjusts individual income-tax brackets and the Section 199A QBI deduction. Additionally, the federal estate and gift tax exemption will rise to approximately $15 million per individual (or $30 million for joint filers) starting January 1, 2026.

The Qualified Small Business Stock (QSBS) rules are also improving. For stock issued after July 4, 2025, the gain-exclusion cap increases to $15 million, with the gross-assets test rising to $75 million. The holding period for partial exclusion will be 50% for three years and 75% for four years, making C-corporation conversions more appealing for founders targeting a 2026 exit.

For those considering ESOPs, these remain a powerful tool for deferring taxes. C-corporation owners can defer capital gains taxes indefinitely by using a Section 1042 rollover and reinvesting proceeds into qualified replacement property like U.S. stocks or bonds. S-corporations with a 100% ESOP-owned structure pay zero federal income tax, which can significantly free up cash for debt repayment. While ESOP setup costs can range between $50,000 and $150,000, the potential tax savings often outweigh these expenses.

Timing your transactions strategically is just as important. For example:

- Installment sales: These spread gain recognition over several years, helping to avoid higher tax brackets and manage AMT thresholds.

- Charitable contributions: Bunching donations in 2025 could help you avoid the new 0.5% of AGI floor that starts in 2026.

- SALT cap considerations: With a temporary $40,000 SALT cap in place through 2029, sellers in high-tax states should account for this when calculating net proceeds.

If you’re managing your exit remotely, tools like Business Anywhere’s Digital Nomad Kit can help you stay compliant with U.S. business regulations while working abroad. Their tax filing services can also ensure you meet all federal and state requirements during your exit year.

"Exit tax outcomes are determined years before the deal, not during negotiations."

- Tim Freese, CPA

Choosing the Right Exit Strategy for Your Business

Deciding how to exit your business is a deeply personal and strategic choice. Whether you’re leaning toward selling, merging, or closing, the decision hinges on your goals. Do you want a lump sum of cash right away, or would you prefer an income stream over time? Are you ready for a clean break, or is preserving your business’s legacy a priority? Answering these questions will help you align your personal objectives with the most suitable exit path.

If your main goal is to secure the highest upfront payment, selling your business is often the best route. Strategic buyers – such as competitors or suppliers – may pay a premium for assets like your customer base or proprietary technology, especially when the sale process is well-executed. On the other hand, merging with another company can unlock growth potential and added value, but it typically requires you to stay involved for 1–3 years to ensure a smooth transition. If your business is struggling financially, liquidation might be the most straightforward option, though it usually recovers only 10% to 30% of the business’s value as a going concern.

"A planned exit almost always produces a better outcome – more money, less stress, smoother transition – than one forced by burnout, health issues, or market changes."

- BuyerEdge

No matter which path you choose, having a well-thought-out strategy is essential. Revisit your exit preparation milestones to ensure everything is in order. Getting a professional valuation early on can help you identify any gaps in value and set realistic expectations. If you’re managing your exit remotely, tools like Business Anywhere‘s Digital Nomad Kit can keep you organized and compliant. Their registered agent services and virtual mailbox can also help you stay connected to your U.S. business operations, no matter where you are.

FAQs

How do I know whether selling or merging is better for my business?

Deciding whether to sell or merge your business comes down to your personal goals and current situation. Selling gives you the chance to fully step away and cash out, making it a good option if you’re ready to move on completely. On the other hand, merging means combining your business with another, which can open doors to growth, shared resources, and a bigger market presence. Think about your long-term plans, the state of the market, and whether you’d rather make a clean break or stay involved before making your choice.

What documents should I prepare before due diligence starts?

Before diving into due diligence, it’s crucial to gather essential documents that highlight your business’s value and make the process more efficient. Here’s what you’ll need:

- Financial records: Include past years’ financial statements and tax returns.

- Legal paperwork: Incorporation documents, contracts, and leases fall into this category.

- Valuation reports: Any assessments of your business’s worth.

- Debt and liability details: Information on any outstanding obligations.

- Licenses and permits: Ensure all registrations are accounted for.

- Operational records: This might include customer lists or supplier agreements.

- Intellectual property: If relevant, have documentation ready for trademarks, patents, or copyrights.

Having these documents ready upfront helps keep the transaction process smooth and organized.

How can I reduce taxes on my exit in 2026?

If you’re planning a business exit in 2026, there are several strategies you can use to potentially lower your tax burden. These include:

- Maximizing deductions: Ensure you’re taking advantage of every deduction available to you. This can significantly reduce your taxable income.

- Adjusting the deal’s timing and structure: The way and when a deal is structured can impact your tax liability. For example, spreading payments over multiple years may help reduce the immediate tax hit.

- Leveraging exemptions: For covered expatriates, there’s a $910,000 exclusion in 2026 that can help reduce taxable gains.

Another key area to focus on is income recognition and gain modulation. Properly timing when income is recognized or gains are realized can make a big difference in the taxes you’ll owe.

Since tax laws are always subject to change, especially as 2026 approaches, it’s crucial to work closely with a tax professional. They can provide tailored advice based on your unique situation and ensure you’re up to date with the latest rules.