Want to know how much your business is worth? Here’s a quick breakdown of the three main ways to value your business:

- Asset-Based Valuation: Calculate the value of your assets minus liabilities. Best for businesses with significant physical assets.

- Income-Based Valuation: Focus on your business’s ability to generate future earnings, using methods like Discounted Cash Flow (DCF) or Seller’s Discretionary Earnings (SDE).

- Market-Based Valuation: Compare your business to similar ones recently sold in your industry.

Each method suits different situations – whether you’re selling, attracting investors, or planning for the future. Start by organizing your financial records, choose the right method, and make adjustments for non-recurring expenses to get an accurate picture. Professional appraisals cost $3,000–$10,000, but DIY tools like ValuAdder ($275) can also help. Keep in mind, combining methods often gives the best results.

Key takeaway: Knowing your business’s worth helps you make smarter decisions and avoid undervaluing or overvaluing your company. Let’s dive deeper into how each method works.

3 Main Valuation Methods for Small Businesses

Determining your business’s worth can be approached in three main ways: by focusing on assets, earnings, or market comparisons. Here’s a closer look at each method to help guide your valuation.

1. Asset-Based Valuation

This method calculates your business’s value by subtracting liabilities from assets. In simple terms, total assets minus total liabilities equals the business value.

Assets can be split into two categories:

- Tangible assets: These include physical items like real estate, equipment, inventory, vehicles, and cash.

- Intangible assets: These cover non-physical elements such as trademarks, brand reputation, and customer relationships.

Liabilities include accounts payable, loans, leases, and taxes.

"The asset approach to valuation may be the most straightforward method because it is based directly on the value of a company’s assets less any liabilities it has incurred." – Dean L Swanson, Certified SCORE Mentor

This approach is often the most conservative, providing a "floor" valuation. It’s particularly effective for businesses like manufacturing or real estate, where physical assets play a dominant role. Depending on your situation, you’ll choose between:

- Going Concern: For ongoing businesses, using standard balance sheet values.

- Liquidation Value: For businesses closing, calculating the value of assets in a quick sale scenario.

A key concept here is Goodwill, which represents the amount a buyer might pay above the net asset value. To ensure accuracy, consider hiring a professional appraiser with credentials like ABV (Accredited in Business Valuation) or ASA (Accredited Senior Appraiser). While this method provides only part of the picture, it’s essential for understanding your company’s financial foundation.

2. Income-Based Valuation

This approach estimates your business’s value based on its ability to generate future earnings. Essentially, it converts future profits into their present value.

Two key sub-methods include:

- Discounted Cash Flow (DCF): Projects cash flows for 5–10 years and applies a discount rate to reflect risk.

- Capitalization of Earnings: Divides a single period of expected income by a capitalization rate, ideal for businesses with stable and predictable earnings.

For small businesses with under $5 million in revenue, the focus is on Seller’s Discretionary Earnings (SDE) – your net profit plus your salary, benefits, and non-essential expenses. In 2024, the average SDE multiple across industries was 2.57x. For larger businesses, EBITDA (Earnings Before Interest, Taxes, Depreciation, and Amortization) becomes the standard metric.

"SBA lenders base their calculations on tax returns, not the adjusted financials sellers present… Undocumented ‘seller discretionary expenses’ won’t count toward cash flow for loan purposes." – Danielle Hunt, Author, EBIT Community

Small business discount rates typically range from 15% to 30%, reflecting industry risk and future uncertainty. When calculating earnings, prioritize recent years to capture current trends. SBA lenders often require a Debt Service Coverage Ratio (DSCR) of 1.25x to 1.5x, based on historical tax returns, to confirm the validity of your income-based valuation.

This method provides a dynamic way to value your business, especially when paired with market comparisons.

3. Market-Based Valuation

This method uses the sales data of similar businesses to estimate your company’s market value. By analyzing actual transactions, you can arrive at a fair market price.

The market-based approach considers both external factors – like economic conditions, interest rates, and industry trends – and internal ones, such as your company’s size, stability, and revenue quality. These factors directly influence the valuation multiple a buyer is willing to pay.

For example, in February 2025, two plumbing companies with identical profits showed how market differences affect valuations:

- Company A: With $10 million in revenue and $2 million in EBITDA, it focused on commercial maintenance across 200+ buildings, with no single customer exceeding 5% of revenue. It achieved a 6.5x multiple ($13 million value).

- Company B: Despite $20 million in revenue and $2 million in EBITDA, it relied on three general contractors for 70% of its revenue. It only secured a 2.75x multiple ($5.5 million value).

To use this method:

- Identify comparable businesses using Standard Industrial Classification (SIC) codes.

- Access private transaction data through M&A advisors or brokers.

- Present a valuation range instead of a single figure to account for market fluctuations.

Industry-specific multipliers are also critical. Sources like the Business Reference Guide from Business Valuation Resources can provide reliable benchmarks. This approach helps tie your valuation to real-world transactions, offering a clearer perspective on your business’s market potential.

sbb-itb-ba0a4be

How to Calculate Your Business Value: Step-by-Step

Building on the asset-based, income-based, and market-based methods discussed earlier, here’s how you can calculate your business value step by step.

Step 1: Collect Your Financial Documents

The foundation of any accurate valuation is well-organized financial records. Start by gathering your key financial statements – balance sheets, income statements (profit and loss), and cash flow statements – for the past three years [4,14]. Additionally, collect your federal and state tax returns for the same period.

Beyond financials, you’ll need legal documents, operational reports, and comprehensive lists of your assets and liabilities [4,14]. Include details about employees, customers, and vendor agreements. These records are not just for valuation – they’re also critical if you plan to sell your business. A 2025 survey found that 37% of small-business owners intended to sell within the next year.

When preparing these documents, pay close attention to add-backs. These are non-recurring expenses like personal travel, meals, or one-time costs (e.g., office relocation or legal fees). Properly documenting these adjustments helps calculate your Seller’s Discretionary Earnings (SDE) accurately [4,14]. If you opt for a professional valuation, expect it to take three to four weeks and cost between $3,000 and $5,000 [12,15].

Step 2: Select the Right Valuation Method

Once your documents are ready, the next step is choosing a valuation method that aligns with your business type and profile.

- Income-based methods work well for profit-driven service businesses.

- Asset-based methods are ideal for companies with significant tangible assets.

- Market-based methods are suited for industries where comparable sales data is available.

For smaller businesses (under $5 million in sales), SDE is typically used, while larger companies rely on EBITDA [3,7,15,13]. Industry standards also vary – service businesses often sell for 2–3× annual profit, manufacturing for 4–5×, and technology companies can reach 6–10× or more due to growth potential. Professional valuators often use multiple methods, like Discounted Cash Flow (DCF) and comparable transactions, to ensure a more reliable estimate [3,18].

Step 3: Make Necessary Adjustments

After choosing your method, refine your valuation by making adjustments for non-recurring and discretionary expenses.

Normalize earnings by adding back costs a new owner wouldn’t face, such as personal expenses or non-market salary adjustments [3,4]. These adjustments can significantly impact your valuation. For example, a business with $450,000 in net income could have an operational profit (EBITDA) of $800,000 after proper adjustments.

Next, apply risk multipliers. Businesses with recurring revenue and a diverse customer base typically earn higher multipliers, while those with high customer concentration or heavy owner dependence get lower ones. Finally, subtract any outstanding debts, accounts payable, or unpaid invoices from your valuation to determine your net worth accurately. These adjustments are essential, especially if your business represents a large portion of your overall financial picture.

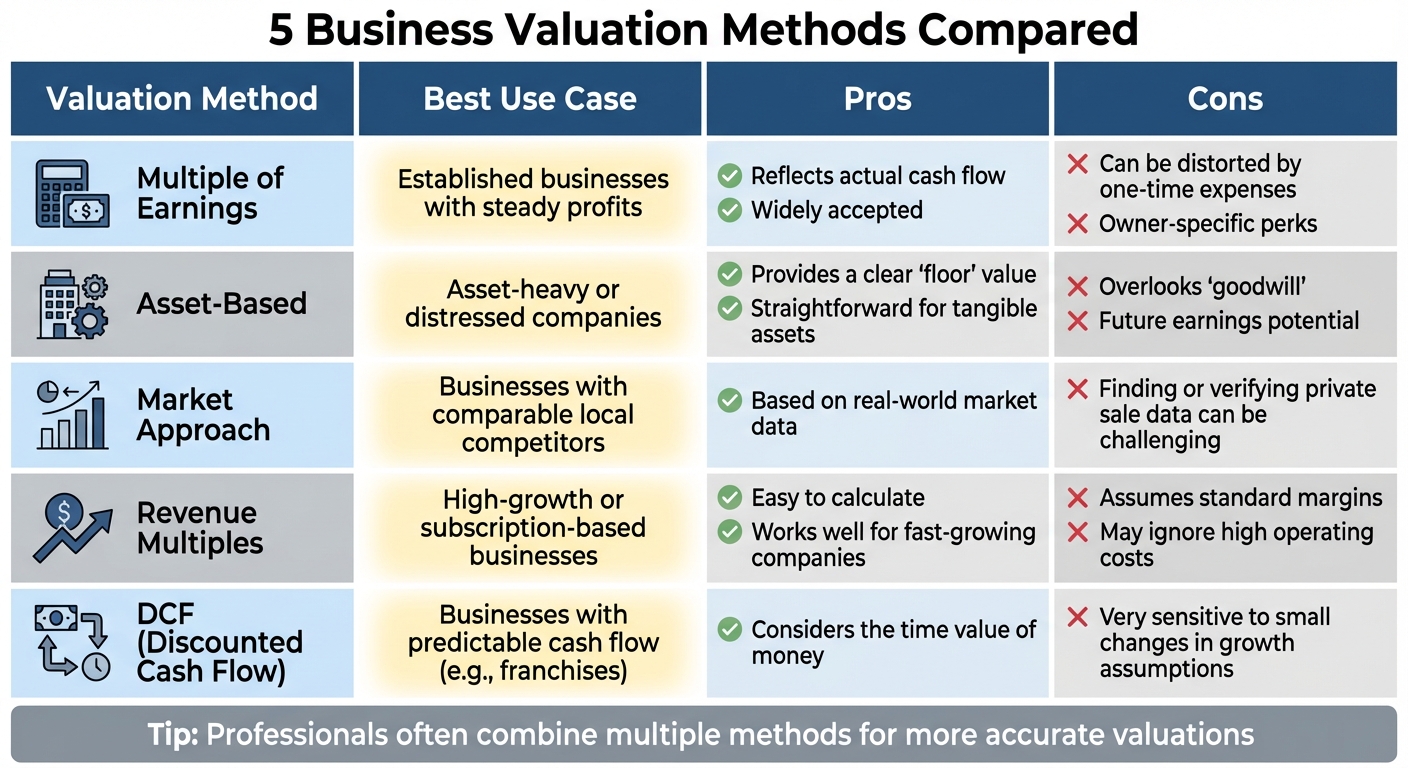

Which Valuation Method Should You Use?

Comparison of 5 Small Business Valuation Methods: Pros, Cons, and Best Use Cases

The best valuation method depends on your business type, profitability, and the purpose behind the valuation. Factors like your business’s structure and long-term goals play a major role in determining the right approach.

For businesses with steady profits, the income-based approach using a multiple of earnings is a common choice. On the other hand, companies with significant physical assets – like manufacturing firms – often benefit from the asset-based approach. This method is especially helpful if the business is struggling financially or unprofitable but holds valuable tangible assets. For startups with high growth potential, the Discounted Cash Flow (DCF) method is favored. By focusing on future cash flow potential instead of past performance, it aligns better with the needs of investors.

"Valuing a small business isn’t mysterious – it’s math, benchmarks, and discipline." – Danielle Hunt

The market-based approach works well when you have access to reliable sales data from comparable businesses in your industry and region. However, for niche industries, finding relevant private company data can be tricky.

Why Use More Than One Method?

Using multiple valuation methods often leads to a more accurate result. As discussed earlier, professionals typically combine approaches – such as asset, income, and market-based methods – and assign weights to each. This "weighted average" approach helps ensure a balanced and fair valuation. For example, you might combine income, market comparables, and revenue multiples to validate your results. This triangulation helps avoid over- or under-valuing your business.

To better understand the strengths and weaknesses of each method, here’s a quick comparison:

Valuation Methods Compared: Pros and Cons

| Method | Best Use Case | Pros | Cons |

|---|---|---|---|

| Multiple of Earnings | Established businesses with steady profits | Reflects actual cash flow; widely accepted | Can be distorted by one-time expenses or owner-specific perks |

| Asset-Based | Asset-heavy or distressed companies | Provides a clear "floor" value; straightforward for tangible assets | Overlooks "goodwill" and future earnings potential |

| Market Approach | Businesses with comparable local competitors | Based on real-world market data | Finding or verifying private sale data can be challenging |

| Revenue Multiples | High-growth or subscription-based businesses | Easy to calculate; works well for fast-growing companies | Assumes standard margins; may ignore high operating costs |

| DCF | Businesses with predictable cash flow (e.g., franchises) | Considers the time value of money | Very sensitive to small changes in growth assumptions |

Tools and Resources for Business Valuation

The right tools and resources can make the valuation process smoother and more accurate, especially when applying the methods discussed earlier.

Free online calculators like BizSellDirect and HowMuchIsItWorth.app leverage AI trained on thousands of private transactions to estimate what buyers are currently paying. For those looking to align with SBA lending guidelines, ValuMate AI uses a Capital Access Model (CAM) tailored to the fact that 90% of small business buyers rely on SBA financing to complete their deals.

If you’re looking for a multi-method comparison, platforms like Upmetrics and Calculatorica allow you to compare revenue-based, profit-based (SDE/EBITDA), and asset-based valuations side by side. These tools work best when you input accurate financial data, including adjustments like owner salaries or personal expenses. Clean data ensures the insights generated are both relevant and actionable.

For industry-specific insights, resources such as BizBuySell and BusinessBroker.net provide access to comparable sale multiples based on real transactions within your sector. These tools underscore how valuation metrics can vary significantly between industries.

While online tools are helpful, formal appraisals are essential for situations requiring legal or financial precision. Whether it’s for estate planning, investor negotiations, or divorce settlements, a professional appraisal is often necessary. Certified appraisers with credentials like ABV, ASA, or CBA typically charge between $3,000 and $10,000 for a defensible valuation. Tools like BusinessAnywhere can simplify the process by organizing financial data, identifying add-backs, and connecting you with valuation experts tailored to your needs.

"When I need business valuation or transaction support, I call ValuMate AI."

- Jared McGlocklin, Bank of Montgomery

Conclusion

Understanding the value of your business isn’t just about preparing for a sale – it’s about making informed decisions every step of the way. When you know your company’s actual worth, you can plan smarter, whether you’re gearing up for retirement, attracting investors, or just wanting a clearer picture of your standing. Accurate valuation plays a key role in shaping long-term financial strategies.

The three primary valuation methods – asset-based, income-based, and market-based – each bring different perspectives to determining your business’s value. As Ori Eldarov from OffDeal puts it:

"Without a solid understanding of your business’s worth, you risk either accepting a lowball offer that leaves money on the table, or rejecting a fair offer because it didn’t match your expectations".

To get started, gather three years of clean financial records, account for add-backs like personal or one-off expenses, and select the valuation approach that fits your needs. For formal documentation – whether for SBA lending, legal requirements, or investor talks – consider hiring a certified appraiser, which typically costs between $3,000 and $10,000.

Platforms like BusinessAnywhere simplify this process by helping you organize your financial data and compliance records. Their services, ranging from bookkeeping to compliance support, lay the groundwork for an accurate valuation. When your business appears well-organized and low-risk, it often commands a higher valuation multiple.

Take the time to understand your business’s value today. It’s a step that can drive growth, attract the right investors, or set the stage for a successful exit.

FAQs

What’s the fastest way to estimate my business value?

To get a quick estimate of your business’s value, you can calculate its book value – which is simply your assets minus your liabilities. Another approach is to use industry-specific valuation multiples. For example, SaaS or e-commerce businesses often rely on revenue multiples. If you’re aiming for a more precise figure, focusing on cash flow and profitability can give you a clearer picture. These methods offer a straightforward way to gauge value without diving into complex analysis.

How do I choose between SDE and EBITDA for valuation?

Choosing between SDE (Seller’s Discretionary Earnings) and EBITDA (Earnings Before Interest, Taxes, Depreciation, and Amortization) comes down to the size and structure of your business.

For smaller businesses generating less than $2 million in revenue, SDE is often the better choice. It accounts for income and expenses tied directly to the owner, giving a clearer picture of the business’s earnings from the owner’s perspective. On the other hand, if your business is larger or more complex, EBITDA is typically the go-to metric. By excluding owner-specific factors, it provides a more standardized and objective measure of profitability.

Which add-backs are most likely to be questioned by buyers or lenders?

When it comes to add-backs, certain categories often raise eyebrows, including personal expenses, non-recurring costs, and discretionary expenses. These items can have a major impact on a business’s true profitability, which is why they tend to draw scrutiny from buyers or lenders during the valuation process.