Figuring out how to pay yourself from your LLC depends on how your business is taxed. Here’s a quick breakdown:

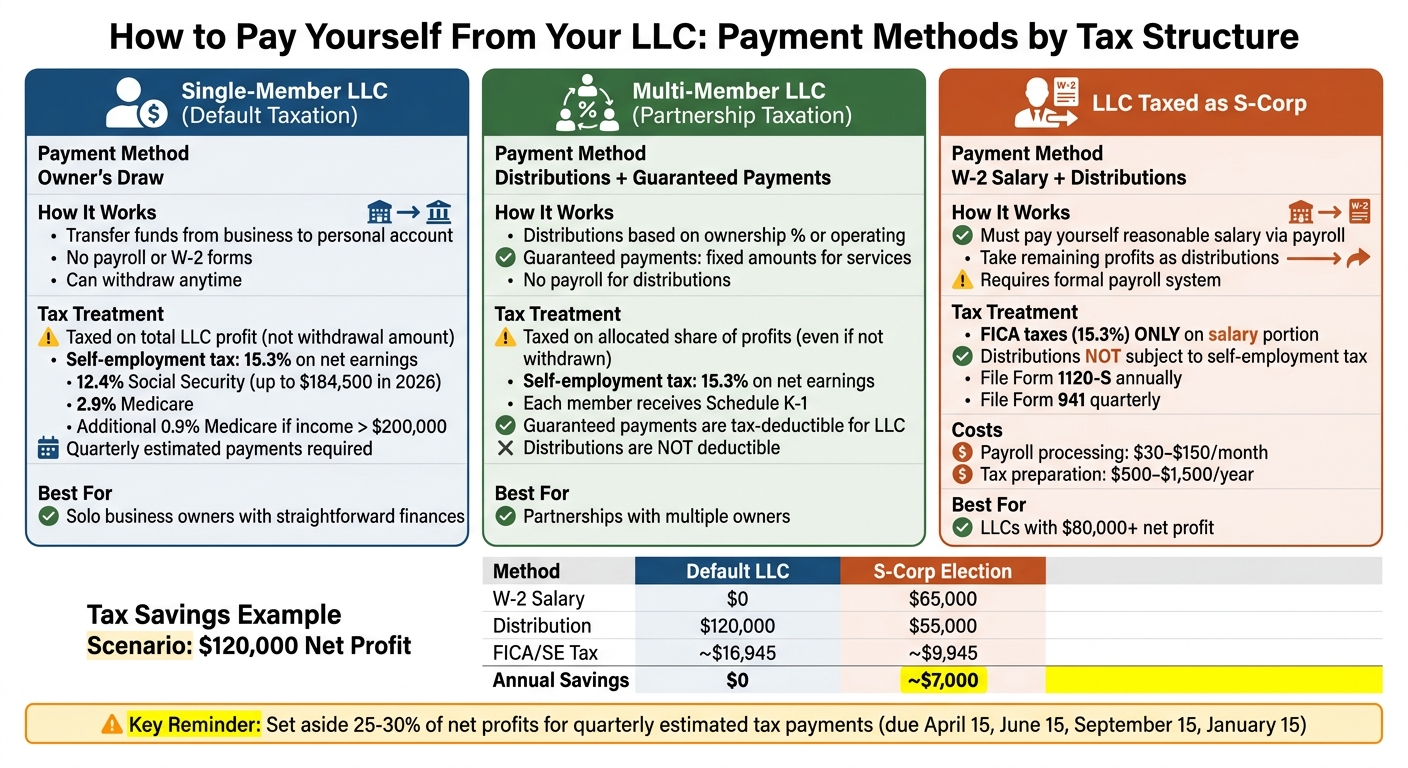

- Single-Member LLCs: Pay yourself using an owner’s draw. Simply transfer funds from your business account to your personal account. Taxes are based on your LLC’s total profit, not the amount you withdraw.

- Multi-Member LLCs: Distribute profits among members based on ownership percentages or terms in your LLC operating agreement. Payments don’t involve payroll but are subject to self-employment taxes.

- LLCs Taxed as S-Corps: Pay yourself a reasonable salary through payroll and take the remaining profits as distributions. This structure can save on self-employment taxes but requires more administrative work.

Key Points:

- Self-employment taxes (15.3%) apply to net profits for default LLCs.

- S-Corp election can reduce taxes by splitting income into salary (taxable) and distributions (not subject to payroll taxes).

- Keep personal and business finances separate to protect liability and avoid IRS issues.

- Pay quarterly estimated taxes to avoid penalties.

This guide shows how to choose the right payment method based on your LLC type and tax structure.

Single-Member LLC: How to Pay Yourself With Owner’s Draw

What Is an Owner’s Draw?

If you’re running a single-member LLC, one of the ways to access your business profits is through an owner’s draw. This is when you transfer money from your business account to your personal account. Unlike a formal salary, an owner’s draw doesn’t involve payroll, W-2 forms, or tax withholding.

For tax purposes, the IRS treats a single-member LLC as a "disregarded entity." This means your business’s income and expenses are reported on your personal tax return using Schedule C. From an accounting perspective, an owner’s draw reduces your owner’s equity on the balance sheet – it doesn’t show up as a business expense on your profit-and-loss statement.

Here’s an important note: your taxes are based on the total net profit of your LLC, not the amount you withdraw. For example, if your business earns $100,000 in profit but you only take out $60,000 for personal use, you’ll still be taxed on the full $100,000.

Step-by-Step: How to Take an Owner’s Draw

Taking an owner’s draw is relatively simple, but it’s important to do it properly to maintain the liability protection of your LLC. Avoid paying personal expenses directly from your business account, as this could blur the lines between personal and business finances.

- Calculate Your Net Profit: Start by determining your net profit after all business expenses. Decide how much to draw, keeping in mind taxes and business reserves. A common guideline is the 30/30/40 rule: allocate 30% for taxes, 30% for reinvestment, and 40% for personal use.

- Transfer Funds Correctly: Move the money from your business account to your personal account via check or ACH transfer. Be sure to label the transaction as "Owner’s Draw" in your records for clarity.

- Stick to a Schedule: While you can take draws whenever you need, setting a consistent schedule – like weekly or monthly – makes record-keeping easier and helps with personal budgeting.

Now that you understand how to take a draw, let’s look at how it impacts your taxes.

How Owner’s Draw Affects Your Taxes

When you take an owner’s draw, no taxes are withheld at the time of transfer. Instead, you’re taxed on your LLC’s total profit. As a single-member LLC owner, you’re responsible for self-employment tax, which is 15.3% of your net earnings. This is calculated on 92.35% of your net business income and includes:

- 12.4% for Social Security (up to $184,500 in 2026)

- 2.9% for Medicare

- An additional 0.9% Medicare tax for incomes over $200,000 (for single filers)

Because taxes aren’t automatically withheld, you’ll need to make quarterly estimated tax payments using Form 1040-ES. The deadlines for these payments are April 15, June 15, September 15, and January 15. To avoid penalties (which can run about 8% annually for underpayment), it’s a good idea to set aside 25% to 30% of your net profit in a separate savings account specifically for taxes.

"Owner’s draws are not a business expense – they don’t reduce your taxable income. They’re simply a transfer of already-taxed profit from the business to you personally." – Slava Akulov, CEO, Jupid

sbb-itb-ba0a4be

Multi-Member LLC: How to Pay Yourself With Distributions

How Your Operating Agreement Controls Distributions

In a multi-member LLC, the operating agreement is the key document that determines how and when members get paid. This agreement can override state laws by clearly outlining how profits are divided among members. By default, profits are often split based on ownership percentages. However, the operating agreement can include alternative arrangements, like allocating profits based on capital contributions or the value of work provided ("sweat equity").

The agreement also establishes the payment schedule. Some LLCs distribute profits monthly, while others choose quarterly or annual payouts. It can also specify whether profits must be distributed to members or reinvested in the business. If no operating agreement exists, state law governs how profits are allocated. This distinction is important for understanding the difference between profit distributions and fixed payments.

Distributions vs. Guaranteed Payments

Multi-member LLC owners can be compensated in two ways: through profit distributions or guaranteed payments.

Profit distributions represent a member’s share of the LLC’s profits, as determined by ownership percentages or other terms in the operating agreement. These are only paid when the business is profitable and has enough cash available.

Guaranteed payments, on the other hand, are fixed amounts paid to members for their services, similar to a salary. These payments are made regardless of the LLC’s profitability. This arrangement is particularly helpful when one member actively manages the business while others take a more passive role.

The tax treatment of these two payment types differs significantly:

- Guaranteed payments are treated as a business expense, reducing the LLC’s taxable income.

- Distributions are not deductible since they are considered a transfer of equity.

For example, if a multi-member LLC earns $250,000, and one member receives an $80,000 guaranteed payment, this leaves $170,000 for profit distribution. If Member A owns 60% of the LLC and Member B owns 40%, Member A would receive $102,000 (60% of $170,000), while Member B would receive $68,000 (40% of $170,000).

| Feature | Profit Distributions | Guaranteed Payments |

|---|---|---|

| Basis | Based on ownership or agreed terms | Fixed amount for services or capital |

| Profit Dependency | Only paid if business is profitable | Paid regardless of profitability |

| Tax Treatment | Not deductible; equity transfer | Deductible as a business expense |

| Self-Employment Tax | Active members: subject to tax | Subject to self-employment tax |

| Reporting | Reported on Schedule K-1 | Reported on Schedule K-1 (separately noted) |

Understanding these differences is crucial, as they directly impact how payments are taxed.

Tax Treatment of Multi-Member LLC Distributions

For tax purposes, multi-member LLCs are treated as partnerships. This means each member owes taxes on their share of the LLC’s profits, even if those profits are reinvested and not withdrawn.

Members must pay self-employment taxes at a rate of 15.3% on 92.35% of their net earnings. This includes Social Security (12.4%, up to the wage base of $184,500 for 2026) and Medicare (2.9%). For individuals earning over $200,000, an additional 0.9% Medicare tax applies.

The LLC itself files Form 1065 (Partnership Tax Return) and provides each member with a Schedule K-1. This form details each member’s share of the LLC’s income, deductions, and credits. Members then use this information to complete their personal tax returns.

Since taxes aren’t withheld from distributions, members need to make quarterly estimated tax payments. To avoid surprises, set aside about 25% to 30% of your allocated share of profits – not just the cash you withdraw – to cover federal and state income taxes, as well as self-employment taxes. Always transfer distributions to your personal account to maintain liability protection, instead of using LLC funds for personal expenses.

LLC Taxed as S-Corp: Salary Plus Distributions

What Happens When You Elect S-Corp Taxation

Switching to S-Corp taxation changes how you pay yourself. Instead of taking owner’s draws or distributions, you’ll need to adopt a salary-plus-distributions approach. By filing Form 2553 with the IRS, your LLC’s payment structure shifts. If you’re providing services, you must classify yourself as an employee and pay yourself a W-2 salary through a formal payroll system [2]. The IRS requires this salary to be "reasonable", meaning it should reflect what similar businesses would pay for comparable roles [5]. Essentially, your salary needs to align with market standards.

However, this structure comes with added responsibilities. You’ll need to file Form 1120-S annually and submit quarterly payroll tax returns using Form 941. Your salary will appear on a W-2, while your share of profits will show up on a Schedule K-1. While these changes can lead to tax savings, they also bring extra costs. Payroll processing typically ranges from $30 to $150 per month, and tax preparation can cost anywhere from $500 to $1,500 annually [2].

Let’s break down how to set up this payment structure step by step.

How to Pay Yourself as an S-Corp Owner

Here’s how to handle payments as an S-Corp owner:

- Determine a reasonable salary by researching market rates. Use tools like the Bureau of Labor Statistics, Glassdoor, or PayScale to benchmark salaries. For many service-based businesses, setting your salary at 50% to 70% of net profit is a common practice [3]. Documenting these benchmarks can help you avoid IRS scrutiny.

- Set up a payroll system to handle tax withholdings for federal and state income taxes, Social Security (12.4% on earnings up to $176,100 for 2026), and Medicare (2.9%) [3]. Payroll software or professional services can automate this process, ensuring accurate withholdings and timely filings. Paying yourself consistently – biweekly or monthly – helps maintain clear records and reinforces that your LLC operates as a separate entity.

- Distribute remaining profits after paying your salary. These distributions aren’t subject to payroll taxes but will be taxed as personal income. To cover these taxes, set aside about 25% to 30% of your total profit and make quarterly estimated tax payments [4].

"The IRS knows when someone earning $200,000 sets their salary at $30,000. Audits for unreasonable compensation are real, and penalties include reclassification of distributions as wages."

- Slava Akulov, Founder, Jupid [3]

Tax Savings From S-Corp Election

One of the biggest perks of S-Corp taxation is avoiding self-employment taxes on distributions. In a default LLC, you pay a 15.3% self-employment tax on your entire net profit. With an S-Corp election, this tax only applies to your W-2 salary, while distributions are exempt [3].

Here’s an example: Imagine an LLC with $120,000 in net profit. As a default LLC, you’d owe around $16,945 in self-employment tax on the full amount. With an S-Corp election and a reasonable salary of $65,000, you’d pay about $9,945 in FICA taxes on the salary, leaving $55,000 as a distribution. This setup could save you roughly $7,000 annually [2].

| Example: $120,000 Net Profit Comparison Default LLC S-Corp Election | ||

|---|---|---|

| W-2 Salary | $0 | $65,000 |

| Distribution | $120,000 | $55,000 |

| Taxable for FICA/SE Tax | $120,000 | $65,000 |

| Estimated FICA/SE Tax | ~$16,945 | ~$9,945 |

| Estimated Annual Savings | $0 | ~$7,000 |

S-Corp election typically makes financial sense when your LLC earns between $60,000 and $80,000 in net profit. Below this range, the administrative costs of payroll and extra tax filings might outweigh the benefits. Above this range, the savings can grow significantly – as long as you stay compliant and pay yourself a reasonable salary.

Tax and Legal Requirements for LLC Owner Compensation

Self-Employment Tax and Quarterly Estimated Payments

When you pay yourself from an LLC, you’re responsible for self-employment taxes, which total 15.3% – split into 12.4% for Social Security and 2.9% for Medicare – applied to 92.35% of your net earnings [2][3]. For the 2026 tax year, Social Security taxes apply to earnings up to $176,100 [3].

To avoid penalties for underpayment (around 8% annually), you need to make quarterly estimated tax payments using Form 1040-ES. These payments are due on April 15, June 15, September 15, and January 15 of the following year. A good rule of thumb is to set aside 25%–30% of your net profits in a dedicated savings account to cover these taxes and avoid surprises at tax time.

Record-Keeping Requirements

Keeping accurate records is essential to staying compliant and protecting your LLC’s legal and financial integrity. Label all payments clearly – such as “Owner’s Draw,” “Distribution,” or “Guaranteed Payment” – and record them as reductions in owner’s equity, not as business expenses [2][3][1].

If your LLC is taxed as an S-Corp and you pay yourself a salary, you’ll also need documentation to support that your compensation is reasonable. Without this, the IRS could audit you, reclassify distributions as wages, and charge back payroll taxes, interest, and penalties of up to 20% on the reclassified amount [2].

Avoid using your LLC’s account to pay for personal expenses. Instead, transfer funds with clear documentation. This not only creates a clean audit trail but also helps maintain the legal separation between you and your business – critical for preserving your LLC’s liability protections.

Common Mistakes to Avoid

One of the riskiest errors LLC owners make is mixing business and personal finances. Commingling funds can lead to “piercing the corporate veil,” where courts may hold you personally liable for business debts. To safeguard your LLC’s liability protection, always maintain separate accounts and ensure all fund transfers are properly recorded.

Inconsistent or incomplete documentation is another red flag for the IRS. Establish a regular payment schedule – whether monthly or bi-weekly – to reinforce that your LLC operates as a distinct entity.

Lastly, underestimating taxes can lead to financial headaches. For example, if you withdraw $10,000 monthly as an owner’s draw, setting aside $2,500 to $3,000 for taxes can help you avoid a hefty tax bill in April, along with penalties for underpayment. Proper planning is key to staying on top of your obligations.

When to Switch to S-Corp Election for Your LLC

Profitability Threshold: When S-Corp Election Saves Money

Choosing the right tax structure can have a big impact on your bottom line. For many LLC owners, switching to an S-Corp election starts making sense when your business consistently earns $80,000 or more in annual net profit [3][4]. Below that level, the costs and added complexity of managing payroll usually outweigh any tax benefits [4].

Here’s a breakdown of potential savings:

- $80,000 net profit: Around $2,100 in savings

- $120,000 net profit: About $7,011 in savings

- $180,000 net profit: Approximately $12,427 in savings [3]

These savings come from dividing your income into two parts: a reasonable salary (which is subject to the full 15.3% FICA tax) and distributions (which avoid FICA taxes). For service-based businesses, a common approach is to set your salary at 50% to 70% of net profit [3].

While the tax savings can be appealing, it’s important to weigh the added responsibilities and costs of an S-Corp before making the switch.

Trade-Offs of S-Corp Election

Electing S-Corp status changes how you operate your business. One major shift is the need for formal payroll processing. This means withholding federal and state income taxes, Social Security, and Medicare from your paychecks. Additionally, you’ll need to file Form 941 quarterly to report payroll taxes and issue a W-2 at the end of the year [2][3].

Here’s a look at the costs involved:

- Payroll processing: $30 to $150 per month

- Form 1120-S corporate tax return filing: $500 to $1,500 annually

Some states add extra fees as well. For example, California charges an $800 annual franchise tax, even if your business isn’t profitable [2][6].

Another key consideration is ensuring your salary meets market standards. The IRS expects your compensation to be "reasonable", taking into account your training, duties, time commitment, and what similar roles in your industry earn [2][3]. If you pay yourself an unreasonably low salary (e.g., $30,000) while taking $170,000 in distributions, the IRS may reclassify those distributions as wages. This could result in back taxes, interest, and penalties of up to 20% [2].

How to File for S-Corp Election

If you’re ready to move forward with an S-Corp election, here’s how to get started. File Form 2553 with the IRS to make the election. Timing is critical – if you want the S-Corp status to apply for the current tax year, you must file the form by March 15 [7]. Filing after this date means the election won’t take effect until the following year.

The form itself is straightforward, requiring basic details about your LLC, consent from all members, and your chosen tax year. You can handle the filing yourself or hire an accountant. For example, BusinessAnywhere offers S-Corp election filing services for $97, which includes preparing and submitting Form 2553.

Once the IRS approves your election, you’ll need to set up payroll right away. Tools like Gusto or QuickBooks can simplify the process by automating tax withholdings and quarterly filings. This step is essential for staying compliant and ensuring you reap the tax benefits of S-Corp status.

Conclusion: Choosing the Right Payment Method for Your LLC

Key Takeaways

How you compensate yourself as an LLC owner depends on the IRS tax classification of your business. For most LLCs, this means using an owner’s draw or distributions. However, if your LLC has elected to be taxed as an S-Corp, compensation involves a combination of a W-2 salary and distributions. It’s important to note that both default LLC structures are subject to a 15.3% self-employment tax on net profits[2].

If your LLC is taxed as an S-Corp, things change. You’ll need to pay yourself a reasonable salary through payroll, and any remaining profits can be taken as distributions, which are not subject to the self-employment tax. This setup becomes financially advantageous when your LLC’s net profit consistently exceeds $60,000 to $80,000 annually. Below this range, the additional payroll and administrative costs of an S-Corp may outweigh the potential tax savings[2].

"The rules are actually straightforward once you understand which method applies to your LLC type. A single-member LLC uses owner’s draws. An S Corp LLC uses salary plus distributions. There’s a right answer for each structure – not a judgment call." – Slava Akulov, Founder, Jupid[3]

With this understanding, you can assess your LLC’s financial situation and choose the approach that aligns best with your business goals.

Next Steps for LLC Owners

Start by reviewing your LLC’s tax classification and current profitability. If your net profit is below $60,000, sticking with the default tax setup and using an owner’s draw or standard distributions is likely the simplest and most cost-effective route. For those earning $60,000–$80,000 or more in net profits, it may be worth exploring an S-Corp election. Compare the potential tax savings against the added administrative workload and costs to determine if it’s the right move.

To keep your finances in order, set up a system to track all payments from your business. Clearly label each transaction as either an "Owner’s Draw" or a "Distribution" in your accounting software. It’s also wise to set aside 25%-35% of your net profits for quarterly estimated tax payments to avoid penalties from the IRS[3]. If you’re considering an S-Corp election, consult a tax professional to establish a reasonable salary using reliable data, such as information from the Bureau of Labor Statistics. Taking these steps will not only help you stay compliant but also streamline your tax obligations and keep your business finances on track.

FAQs

How often can I take distributions from my LLC?

When it comes to taking distributions from your LLC, the frequency largely depends on how much profit your business generates. If you’re a single-member LLC owner, you can take owner’s draws whenever needed, as long as your business has the funds. For multi-member LLCs, distributions are typically handled according to the terms outlined in the operating agreement.

If your LLC is taxed as an S-Corp, the process is a bit different. In this case, you’ll need to pay yourself a reasonable salary first, then take additional distributions based on the profits available.

Regardless of your LLC type, keeping detailed records is essential to avoid any potential IRS complications. It’s also wise to time your distributions thoughtfully, considering both your cash flow and tax planning strategies.

Do I pay taxes on owner’s draws?

You don’t pay taxes directly on owner’s draws from an LLC. Instead, the income flows through to your personal tax return. Depending on your LLC’s structure, you might owe self-employment taxes on that income. Make sure to factor this into your tax planning.