Managing rental properties in a different state requires careful planning to avoid legal and financial pitfalls. Here’s what you need to know:

- LLCs Protect Your Assets: Forming an LLC separates your personal assets from your rental business, shielding you in case of lawsuits. Many investors create a separate LLC for each property to limit risks.

- Registered Agents Are Mandatory: States require LLCs to appoint a registered agent with a physical address to handle legal notices and government correspondence.

- Virtual Mailboxes Simplify Remote Management: With mail scanning services, you can access important documents, tenant communication, and tax forms online, no matter where you are.

- Compliance Is Key: States often require annual filings, rental licenses, and local tax payments. Missing these can lead to fines or losing liability protection.

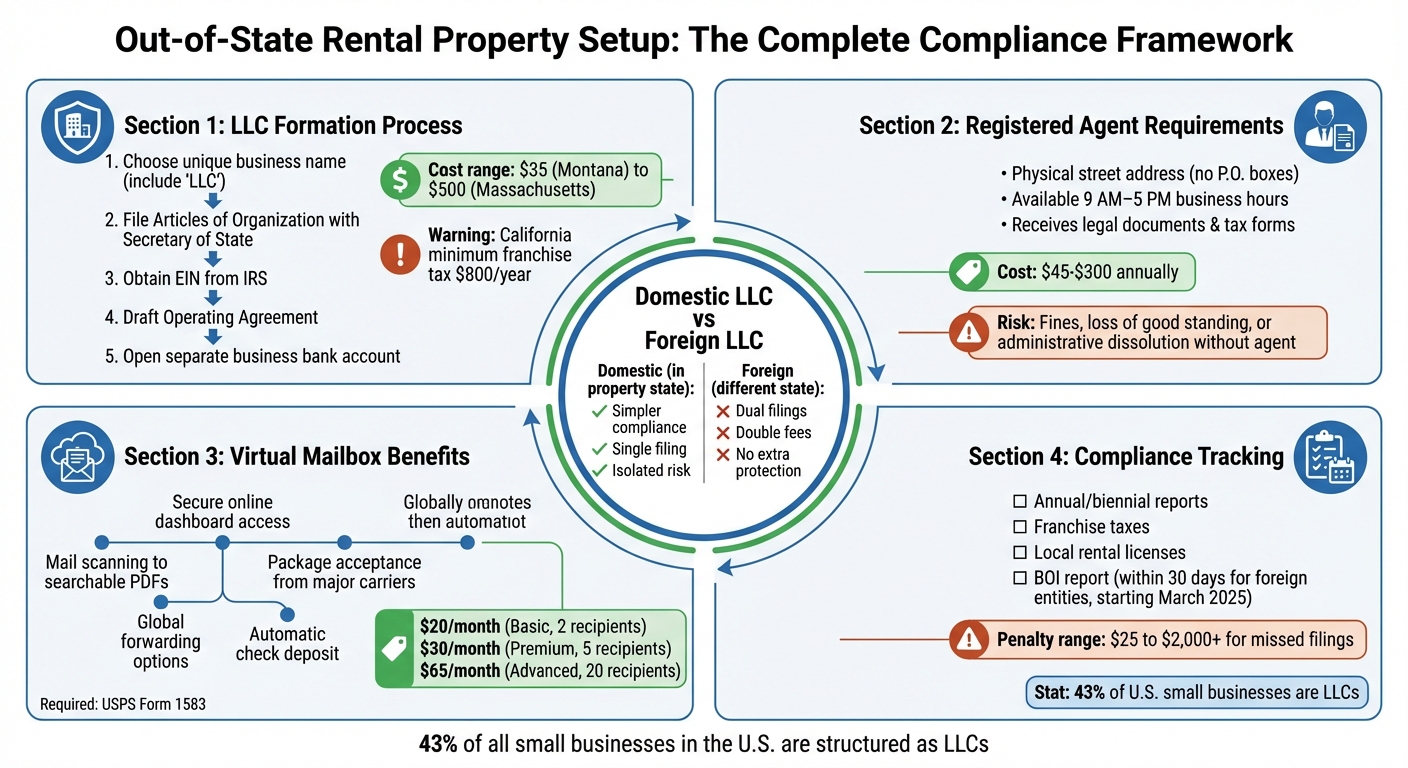

Why LLCs Work Well for Rental Properties

Liability Protection and Tax Flexibility

An LLC provides a shield between your personal assets and your rental business. Once you set up an LLC, it officially becomes the landlord, offering protection for your personal assets in case a tenant decides to sue for damages that exceed your insurance coverage.

Many real estate investors take this a step further by creating a separate LLC for each property. This strategy helps limit potential liabilities to just one property. Additionally, LLCs come with the benefit of pass-through taxation, meaning you avoid the double taxation that corporations face. On top of that, you can deduct LLC-related expenses like state filing fees or costs for registered agent services. Filing fees vary widely, from $35 in Montana to $500 in Massachusetts. In California, there’s also a minimum franchise taxes by state of $800.

To keep these protections intact, it’s crucial to separate your personal and business finances. Use a dedicated business bank account, obtain an EIN (Employer Identification Number), and avoid mixing personal and business funds. This separation helps prevent courts from "piercing the corporate veil", which could jeopardize your asset protection. These benefits – asset protection and tax advantages – are key when deciding whether to form a domestic LLC or register as a foreign entity for out-of-state investments.

Domestic vs. Foreign LLCs: What You Need to Know

When investing in rental properties, you’ll generally need to choose between forming a domestic LLC in the state where the property is located or registering an existing LLC as a foreign entity. Most states consider owning and renting real estate as "doing business", which means registration is necessary to stay compliant and maintain liability protection.

Forming a domestic LLC in the property’s state is usually the simpler option. It avoids the extra administrative requirements that come with registering a foreign LLC, such as filing additional annual reports, paying extra fees, and maintaining registered agents in multiple states. On the other hand, using a foreign LLC could expose all your assets – including those in your home state – to lawsuits tied to the out-of-state property.

"If you have a liability issue in California, meaning a lawsuit, the judge is going to follow California law, not Wyoming law. You have no legal nexus or connection to Wyoming whatsoever".

Setting Up an LLC in Another State

Filing Articles of Organization

If you’ve decided to establish a domestic LLC in the state where your rental property is located, the steps are straightforward. Start by choosing a unique business name that includes "LLC" or "Limited Liability Company" and ensure it’s not already in use. Be aware that some words, like "Bank" or "University", may require additional licensing or approval.

Next, file your Articles of Organization – sometimes referred to as a Certificate of Formation – with the appropriate state agency, usually the Secretary of State. This document will specify whether your LLC will be member-managed (owners handle daily operations) or manager-managed (managers are appointed to oversee operations). You’ll also need to name a registered agent with a physical address in the state (P.O. Boxes are not allowed) to receive legal documents and notices.

Once the state approves your filing, obtain an EIN (Employer Identification Number) from the IRS and draft an Operating Agreement. This agreement outlines essential details like ownership percentages, profit distribution, and procedures for membership changes.

Some states, like Arizona, require you to publish your LLC formation in a local newspaper for three consecutive weeks (though certain counties, such as Pima, may be exempt). Filing fees for LLC formation can vary significantly, ranging from $35 in Montana to $500 in Massachusetts.

By forming your LLC in the same state as your rental property, you can avoid unnecessary complications and streamline compliance.

Avoiding Dual Compliance Problems

Steer clear of forming an LLC in a state different from where your property is located and then foreign qualifying it. This approach requires duplicate filings and fees. Foreign qualification creates dual compliance obligations, including additional annual reports, franchise taxes, and filing fees, without offering extra asset protection.

"Forming an LLC in a different state and ‘foreign filing’ it into the property’s state just creates unnecessary costs and paperwork without offering added protection."

– Toby Mathis, Esq., Anderson Business Advisors

Most states consider renting out real estate as "doing business" within their jurisdiction. If you fail to register your LLC properly, you could lose liability protection and face fines. The simplest and most efficient approach is to form a domestic LLC in the state where your rental property is located. This not only simplifies compliance but also isolates risk. In the event of a lawsuit, only the assets within that specific LLC are exposed – not your entire portfolio.

Before transferring the property title to your newly formed LLC, check with your mortgage lender. Many loans include acceleration clauses, which could be triggered by a title transfer. Once you have lender approval, transfer the deed – commonly using a Quitclaim Deed – and immediately open a separate business bank account. This helps maintain the corporate veil and keeps your business operations distinct from personal finances.

Why You Need a Registered Agent

Legal Requirements for Registered Agents

If you’re forming an LLC, one essential step is appointing a registered agent. This is a person or entity with a physical street address in the state where your LLC operates. Their job? To receive critical legal documents, tax forms, and government notices on behalf of your business. A P.O. Box won’t cut it – the address must be a physical location, and the agent needs to be available during standard business hours (9 AM–5 PM) to accept these documents.

"You can think of your registered agent as the face of your LLC. This is the person who will be the go-to for business matters in the state where your company is formed."

– BiggerPockets

For investors from out of state, this requirement can be tricky. Without a registered agent, your LLC risks serious consequences. These include fines, losing your "good standing" status with the state, or even being administratively dissolved, which essentially shuts your business down. In some states, failing to maintain a registered agent can even lead to criminal charges.

"Without a registered agent, your business could face fines, lose its good standing, and, in some cases, get shut down by state authorities, meaning it can’t operate legally anymore."

Clearly, ensuring you have a reliable registered agent isn’t just a formality – it’s a necessity for staying compliant and protecting your LLC.

Choosing a Registered Agent Service

Just like forming your LLC correctly is crucial to protecting your business, choosing the right registered agent service is key to maintaining compliance over time. Registered agent services typically cost between $45 and $300 annually – a small investment compared to the potential legal headaches of going without one.

When selecting a service, look for providers with a legitimate physical presence in the state where your LLC operates. Avoid services that rely solely on virtual offices or mail forwarding addresses. Privacy is another big advantage of using a professional service. By doing so, you can keep your personal address off public records, reducing the risk of unwanted solicitations or the awkwardness of being served legal documents at home.

You’ll also want to consider services that offer compliance monitoring and automated reminders for important filings. Many modern providers include digital document management, scanning any received documents and uploading them to a secure online portal for immediate access.

For instance, BusinessAnywhere offers a registered agent service for $147 annually after the first year, which is free when you register your LLC through their platform. Their service includes a physical address in your state, compliance alerts, and digital document scanning – all managed through a single online dashboard. If you’re an investor managing properties in multiple states, this centralized solution can simplify compliance and ensure you never miss an important notice.

sbb-itb-ba0a4be

Managing Mail with Virtual Mailboxes

How Mail Scanning and Forwarding Work

Handling rental property mail from another state can be a real hassle. That’s where virtual mailboxes step in, offering a physical U.S. address where your mail is received, sorted, and digitized for easy access. Unlike a standard P.O. Box, these addresses meet state LLC registration requirements and can even accept packages from major carriers.

Here’s how it works: incoming mail is scanned into text-searchable PDFs and uploaded to a secure online dashboard. From there, you can review, forward, or archive it – all without leaving your home. This feature is a lifesaver for landlords managing properties from afar. It keeps tenant communication, vendor invoices, and tax documents organized without the need for constant travel.

"I live out of state and use [a virtual mailbox] as my single point of contact for all my tenant-related correspondence. Game changer."

– Louis M., Landlord

To use a virtual mailbox legally, you’ll need to complete USPS Form 1583, which gives the service provider permission to handle your mail. Many providers simplify this process with online notary services, typically costing around $25, so you can get it done without leaving your desk. Once set up, you’ll have a permanent digital archive of important documents – ideal for staying compliant with state regulations.

Virtual mailboxes also help reduce risks like check fraud. Some services even offer automatic check deposit, letting rent payments go straight into your business account without you ever handling a physical check.

This digital solution doesn’t just simplify mail management – it also streamlines your entire operation, especially when paired with customizable virtual mailbox plans.

BusinessAnywhere‘s Virtual Mailbox Plans

BusinessAnywhere offers virtual mailbox plans tailored for remote landlords and property investors. These plans, billed annually, include unlimited scanning, digital storage, and global forwarding. Pricing starts at $20/month for the Basic plan (2 recipients), $30/month for the Premium plan (5 recipients), and $65/month for the Advanced plan (20 recipients) [https://businessanywhere.io/virtual-mailbox/].

For landlords juggling multiple LLCs or properties in different states, the multi-recipient feature is a standout. It allows you to consolidate mail from various entities into a single dashboard. You can also invite team members – like property managers or maintenance staff – and assign specific permissions for handling mail. This setup keeps things professional by using a business address instead of your home address, which stays private.

BusinessAnywhere’s virtual mailbox service integrates seamlessly with their registered agent offering. When you form an LLC through their platform, the first year of registered agent service is included for free (normally $147/year). You can add a virtual mailbox to manage all your business correspondence in one place. The online dashboard also provides compliance alerts, so you’ll never miss a filing deadline or important legal notice.

Staying Compliant with State Regulations

Compliance is a crucial aspect for remote property investors managing portfolios across state lines. Ignoring these requirements can lead to costly penalties, loss of liability protection, or even legal disputes.

Annual Reports and Filing Requirements

Most states require LLCs to submit annual or biennial reports to update information like member details and addresses. These filings are necessary to maintain your LLC’s Good Standing status, which is essential for preserving liability protection and retaining access to state courts. Missing deadlines can result in penalties ranging from $25 to over $2,000.

If you’re investing in out-of-state properties, you’ll need to comply with foreign qualification rules. This means registering your LLC in the state where the property is located, which often involves paying fees in both states.

"If the state considers the act of renting property in its jurisdiction as ‘doing business,’ the LLC must be registered there – either as a domestic LLC or a foreign LLC." – Nellie Akalp, CEO, CorpNet

Some states also impose franchise taxes, regardless of whether your LLC generates income. For instance, California requires a minimum annual franchise tax of $800, while Delaware charges $300. On top of that, you might need local rental licenses or occupancy certificates, depending on the state.

Starting in March 2025, any foreign entity registering to do business in a U.S. state must file a Beneficial Ownership Information (BOI) report with FinCEN within 30 days of registration. This new rule applies to out-of-state LLCs managing rental properties.

Failing to comply with these regulations can have serious consequences, including administrative dissolution of your LLC. This would strip your business of its legal status and liability protections. A notable example is the case of Drake Manufacturing Company, Inc. v. Polyflow, Inc., where a manufacturer lost a $300,000 lawsuit – not because of the case’s merits, but due to its failure to register as a business in the state.

Thankfully, automated compliance tools are making it easier to stay on top of these requirements, minimizing the risk of missing critical deadlines.

Using Technology to Track Compliance

Managing compliance across multiple states can be overwhelming, but technology-driven tools are helping investors simplify the process. Instead of relying on spreadsheets, centralized dashboards can track registrations, statuses, and deadlines in one place.

Platforms like BusinessAnywhere offer features designed to automate compliance tasks. For example, their dashboard sends reminders for state franchise tax and annual report filings, ensures you stay ahead of deadlines, and even pulls real-time updates from Secretary of State databases to monitor your LLC’s status.

"Failing to regularly meet ongoing requirements in a timely manner can have big consequences for small businesses." – Dave Griswold, Senior Customer Service Operations Associate, Wolters Kluwer

For landlords managing properties across different states, advanced compliance algorithms can compare your company’s data against more than 22,000 regulatory filing requirements. This helps identify any gaps or upcoming obligations, ensuring you remain compliant without the stress of manual tracking.

Conclusion

Managing rental properties remotely becomes much simpler when you use LLCs for liability protection, registered agents for legal compliance, and virtual mailboxes to handle correspondence efficiently.

Treating your rental properties as legitimate businesses is key. This means keeping finances separate and staying on top of state filings. As Toby Mathis wisely notes:

"The court will respect your LLC as much as you do. Treat it like a business, and it will protect you like one".

With a disciplined approach, you can take full advantage of modern compliance tools. Today’s technology makes remote property management more accessible than ever. Features like automated compliance tracking, digital mail scanning, and centralized dashboards allow you to monitor your investments from anywhere while ensuring you meet state regulations. This is especially relevant given that 43% of all small businesses in the U.S. are structured as LLCs, many of which operate across multiple states.

Platforms like BusinessAnywhere simplify this process by integrating everything you need into one place. BusinessAnywhere offers $0 LLC formation (plus state fees), a free first-year registered agent service, and virtual mailbox plans starting at just $20/month, including unlimited scanning and global forwarding – all accessible through a single dashboard.

Whether you’re managing one property or a portfolio spanning multiple states, this streamlined approach helps you stay compliant and protect your assets. Start by forming your LLC, securing a dependable registered agent, and adopting digital tools that keep you connected to your business no matter where you are.

FAQs

Why is it beneficial to set up an LLC for each rental property?

Creating a separate LLC for each rental property can safeguard your personal assets and other investments by isolating liability. If one property encounters legal troubles – like a lawsuit or debt – the potential risks are confined to that specific LLC. This approach helps reduce financial exposure and adds an extra layer of protection to your overall portfolio.

On top of that, having individual LLCs simplifies managing the financial and legal responsibilities of each property. It allows you to handle state compliance more efficiently while keeping operations organized and easier to oversee.

What happens if an LLC doesn’t have a registered agent?

If an LLC fails to have a registered agent, it opens the door to serious legal and operational problems. Without one, the LLC might miss crucial legal notices, like a service of process for lawsuits or compliance-related documents from the state. This could lead to default judgments, fines, or other penalties.

On top of that, many states can take administrative action to dissolve an LLC that doesn’t meet this requirement. This puts the business at risk of losing its ability to operate and its liability protections. A registered agent plays a key role in keeping your LLC compliant and safeguarding it from these potential issues.

How can virtual mailboxes help out-of-state landlords manage compliance?

Virtual mailboxes give out-of-state landlords a legitimate street address in the state where their LLC is registered. This means they can receive critical documents – like tax notices, court filings, and official correspondence – without needing to maintain a physical office. The service scans and digitizes mail, making it simple to keep track of deadlines, respond to legal notices, and ensure their LLC stays compliant.

On top of that, virtual mailboxes create easily searchable digital records for things like rent payments, lease agreements, and tenant communications. This helps landlords stay organized while also meeting legal requirements for landlord-tenant laws and tax reporting. Many services even provide a "virtual business address" for LLC registration and banking, offering privacy protection while fulfilling state physical presence rules.