Choosing between a partnership and a corporation is a critical decision for any U.S.-based business owner. Each structure has distinct features that impact taxes, liability, and management. Here’s a quick breakdown:

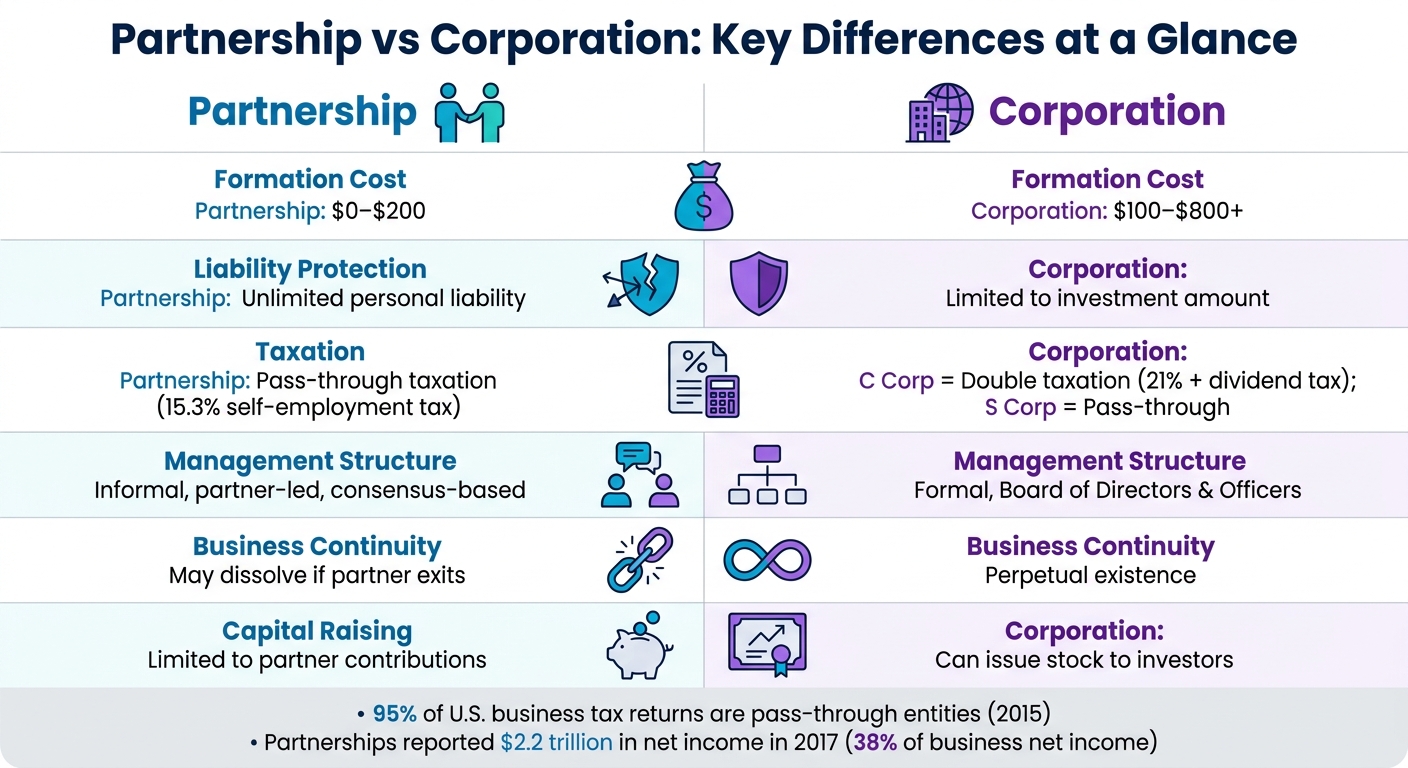

- Partnership: Simple setup, low cost ($0–$200), and pass-through taxation. However, partners face unlimited personal liability.

- Corporation: Offers liability protection and perpetual existence but involves higher costs ($100–$800+) and stricter compliance. Taxation depends on whether it’s a C corporation (21% corporate tax plus dividend taxes) or an S corporation (pass-through taxation with limits).

Quick Comparison

| Feature | Partnership | Corporation |

|---|---|---|

| Formation Cost | $0–$200 | $100–$800+ |

| Liability | Unlimited for partners | Limited to investment |

| Taxation | Pass-through | C Corp: Double; S Corp: Pass-through |

| Management | Informal, partner-led | Formal, board of directors |

| Continuity | May dissolve if a partner exits | Perpetual existence |

| Capital Raising | Limited to partner contributions | Can issue stock |

Both options have pros and cons. Partnerships suit small, low-risk businesses with fewer formalities, while corporations are better for scaling, attracting investors, or limiting liability.

Formation and Legal Requirements

Building on our introduction, let’s dive into the specific steps and legal obligations for forming different business structures.

How to Form a Partnership

Starting a general partnership is incredibly straightforward. All it takes is an agreement – verbal or even a handshake – between two or more people who decide to run a business together. No state filings are required, so you can begin operating immediately [1].

However, skipping formal documentation can be risky. A written partnership agreement is highly recommended. This document outlines critical details like each partner’s responsibilities, profit-sharing arrangements, voting rights, and exit strategies [1][5]. Without it, conflicts over money or decision-making can escalate quickly, leading to costly disputes.

For a Limited Partnership (LP) or Limited Liability Partnership (LLP), the process involves more formalities. You’ll need to file a Certificate of Limited Partnership with your state and include a designation like "LP" in your business name [5].

"If you ink obligations first and only later organize, you may be personally liable for business debts and liabilities incurred pre‑formation." – Turley Law [5]

How to Form a Corporation

Incorporating a business is a more structured process. To start, you must file Articles of Incorporation with your state’s Secretary of State. Filing fees range from $100 to $800+, depending on the state [1]. This document officially establishes your corporation as a separate legal entity.

After filing, you’ll need to create corporate bylaws – a set of rules that govern internal operations. These bylaws cover everything from electing directors to conducting shareholder meetings [1][3]. You’ll also need to appoint a board of directors and issue shares of stock to your initial shareholders [5][3].

Once established, corporations must meet ongoing obligations, such as holding annual shareholder and director meetings, keeping detailed minutes, and filing annual reports to maintain liability protection [1][3][5].

Formation Requirements Compared

Here’s a quick breakdown of the key differences between partnerships and corporations:

| Feature | Partnership | Corporation |

|---|---|---|

| Formation Complexity | Simple; minimal paperwork [1] | Complex; formal state filings required [1] |

| Primary Document | Partnership Agreement [5] | Articles of Incorporation & Bylaws [1] |

| Initial Cost | $0–$200 [1] | $100–$800+ [1] |

| State Filing Required | No (for GPs) [1] | Yes [1] |

| Ownership Units | Partnership interests [5] | Shares of stock [3] |

| Ongoing Requirements | Minimal; few annual filings [1] | High; annual meetings, minutes, reports [1] |

The comparison highlights a key distinction: partnerships allow for quick and easy setup with minimal bureaucracy, while corporations require more documentation and ongoing administrative work. For entrepreneurs managing a remote business, these differences can significantly affect how much time and effort you’ll spend on compliance. Tools like BusinessAnywhere simplify the process by handling everything from initial registration to ongoing filings through a single online platform, so you don’t have to juggle deadlines and paperwork.

Ownership and Liability Protection

Now that you’ve got a handle on forming these business structures, let’s break down how ownership works and how it impacts your personal assets.

How Partnership Ownership Works

In a partnership, ownership is shared between two or more individuals who directly own and manage the business. Instead of issuing stock, each partner holds a partnership interest, which represents their stake in the company. Decision-making is usually split equally, unless a written partnership agreement outlines different voting rights or management responsibilities.

One drawback of partnerships is the limited ability to transfer ownership. If a partner decides to leave or passes away, the partnership might need to dissolve and be restructured under a new agreement.

How Corporate Ownership Works

Corporations take a different approach, dividing ownership into shares of stock. These shares can be transferred easily without interrupting business operations. Shareholders elect a board of directors to oversee big-picture decisions, while corporate officers handle daily management. This setup simplifies raising capital – new shares can be issued to investors or transferred to bring in additional owners. Plus, standardized regulations, like those under the Uniform Commercial Code, make transferring shares straightforward.

There are some restrictions, though. For example, S corporations are limited to 100 shareholders, and all must be U.S. citizens or permanent residents [2]. In contrast, C corporations don’t have these limits, making them a popular choice for companies planning to go public or attract venture capital. Beyond ownership, these structures also affect how much personal liability you face.

Liability Protection Compared

Ownership structures also differ significantly when it comes to liability protection. In a general partnership, you’re on the hook for all business debts and legal actions – even those caused by your partners. Your personal assets could be at risk if the business runs into financial trouble.

"In a general partnership, you’re personally responsible for every debt your business – or your partner – incurs." – Beancount.io [1]

Corporations, by contrast, provide a liability shield that separates personal assets from business obligations. Shareholders typically only risk losing the money they’ve invested. However, this protection isn’t guaranteed. If corporate formalities – like holding annual meetings or keeping separate financial records – aren’t followed, courts could pierce the corporate veil, exposing personal assets.

| Feature | Partnership | Corporation |

|---|---|---|

| Personal Liability | Unlimited | Limited to the investment |

| Ownership Unit | Partnership interest | Shares of stock |

| Transferability | Difficult; may require new agreements | Generally straightforward |

| Management Control | Shared equally (or as defined in an agreement) | Managed by a board of directors |

| Business Continuity | May dissolve if a partner exits or dies | Perpetual existence |

| Capital Raising | Limited to partner contributions | Can issue additional shares |

This table highlights how each structure balances ownership with liability exposure. If your business involves significant risks – like debt or potential lawsuits – the liability protection of a corporation might outweigh the added complexity and cost of incorporation.

Taxation and Financial Implications

Your business’s tax structure plays a major role in shaping expenses and how much you can reinvest. Just like ownership structures determine risk, tax rules influence your financial strategy. Let’s break down how taxation works for different business structures and what that means for your bottom line.

How Partnerships Are Taxed

Partnerships don’t pay federal income tax at the business level. Instead, profits and losses pass directly to the partners, who report them on their personal tax returns using Schedule K-1. The partnership itself files Form 1065, but the actual taxes are paid by the partners.

General partners face a 15.3% self-employment tax on their entire share of the income, even on profits they leave in the business. Partnerships also allow flexibility in dividing profits and losses through special allocations, which can differ from ownership percentages if they meet certain economic requirements.

Partners can take advantage of the 20% Qualified Business Income (QBI) deduction, a benefit made permanent under the One Big Beautiful Bill Act of 2025. Starting in 2026, this deduction begins to phase out at $203,000 for single filers and $406,000 for married couples filing jointly. Additionally, a partner’s tax basis can increase based on their share of the partnership’s debt, which allows for larger loss deductions – an especially useful feature for real estate ventures.

How Corporations Are Taxed

Corporations fall into two main categories: C corporations and S corporations.

- C corporations face double taxation. The business pays a flat 21% corporate tax on profits, and then shareholders pay taxes again on dividends, usually at rates of 0%, 15%, or 20%.

- S corporations, on the other hand, avoid double taxation by passing profits directly to shareholders. However, S-corp owners must pay FICA taxes on a "reasonable salary", but distributions beyond that salary are not subject to self-employment tax.

For example, in January 2026, SDO CPA analyzed a business earning $200,000 in net income. As a general partnership, the owner would have paid $30,600 in self-employment tax. By electing S-corp status and taking an $80,000 salary, the owner paid just $12,240 in FICA taxes on the salary, with no taxes on the remaining $120,000 in distributions. This resulted in a tax saving of $18,360 [6].

"The S-Corp structure is often the optimal choice, combining pass-through taxation with meaningful payroll tax savings." – Antravia Advisory

S corporations have limitations, such as a cap of 100 shareholders, all of whom must be U.S. residents. Profit distribution must also follow strict pro-rata rules. In contrast, C corporations don’t have these restrictions, making them appealing for businesses seeking venture capital or planning to go public.

Tax Structures Compared

Here’s a quick comparison of the key differences:

| Feature | Partnership | S Corporation | C Corporation |

|---|---|---|---|

| Entity-Level Tax | None | None | Yes (21% corporate tax) |

| Self-Employment Tax | 15.3% on all net income | 15.3% on salary only | N/A (taxed as W-2 salary only) |

| Profit Distribution | Flexible (special allocations) | Strict pro-rata | Pro-rata based on shares |

| QBI Deduction | Eligible (up to 20%) | Eligible (up to 20%) | Not eligible |

| Loss Deductions | Can include a share of entity debt | Generally limited to direct investment losses | Remains at the corporate level |

| Ownership Limits | Unlimited; any entity type | Maximum 100; U.S. persons only | Unlimited; any entity type |

If your business earns between $60,000 and $80,000 in annual net profit, switching to an S-corp might justify the added payroll and administrative expenses. Meanwhile, companies reinvesting a large portion of profits might find the 21% corporate tax rate of C corporations more appealing than individual tax rates. In industries like real estate, partnerships stand out by allowing entity-level debt to increase tax basis, enabling larger deductions tied to depreciation.

sbb-itb-ba0a4be

Management and Business Continuity

How a business operates daily and what happens when an owner steps away can vary greatly between partnerships and corporations. Just like the differences in formation and liability protection, management and continuity are also distinct.

How Partnerships Are Managed

Partnerships tend to have a hands-on and informal management style. Partners usually handle operations directly without needing formalities like board meetings, annual reports, or corporate minutes. Decisions are often made through consensus or unanimous agreement, and any partner can enter into contracts on behalf of the business (known as mutual agency).

While this flexibility allows for tailored management, it can also create challenges. Disputes or a lack of clear guidelines can stall operations. In fact, Richard Brothers Financial Advisors highlights that around 50% of businesses fail due to the "5Ds": Divorce, Death, Disagreement, Distress, and Disability [7]. Without detailed partnership agreement clauses, conflicts can lead to delays that disrupt day-to-day activities.

"The partnership agreement can be as detailed or simple as you choose." – Beancount.io

How Corporations Are Managed

Corporations operate with a structured hierarchy involving shareholders, a board of directors, and officers. Shareholders elect the board, which oversees strategy, while officers handle daily operations. Corporate bylaws guide this process, requiring formal approvals and documented minutes for key decisions.

"Decision-making [in a corporation] is hierarchical and guided by corporate bylaws." – G2B

Unlike partnerships, only authorized officers or agents can legally commit the corporation to contracts. This structured approach offers stability and scalability, making it easier for corporations to attract investors, issue stock options, and manage growth. These differences also shape how ownership changes and continuity are handled.

Business Continuity Compared

When it comes to continuity, partnerships and corporations take very different paths. Partnerships generally lack perpetual existence. If a partner dies, withdraws, or declares bankruptcy, the business might dissolve unless the partnership agreement includes specific provisions like a buy-sell clause. This can force remaining partners to reorganize or reestablish the business.

Corporations, on the other hand, have perpetual existence. Ownership changes – whether through share transfers to heirs or new buyers – don’t disrupt operations. As Beancount.io notes, "A corporation’s continuity is beneficial… if you’re building a business to outlast your involvement – something you might sell or pass to the next generation."

Between 1996 and 2017, the number of partnerships in the U.S. grew by 136%, reaching 3.9 million entities [4]. However, in the United Kingdom, partnerships have declined by 18% since 2019, while corporations have grown by 4%, indicating a shift toward the stability corporations offer [4].

Partnership vs Corporation: Complete Comparison

Here’s a detailed side-by-side breakdown of partnerships and corporations:

| Feature | Partnership | Corporation |

|---|---|---|

| Formation Complexity | Simple – requires minimal paperwork, and general partnerships often don’t need state filings | Complex – involves filing Articles of Incorporation, adopting Bylaws, and completing formal state filings |

| Formation Cost | $0 to $200 | $100 to $800+ |

| Legal Status | Tied to its owners; not a separate legal entity | Operates as a distinct legal entity |

| Liability Protection | General partners face unlimited personal liability; limited liability is available for LPs and LLPs | Shareholders are protected, risking only the amount they invest |

| Taxation | Pass-through taxation – profits are taxed at individual rates, with a 15.3% self-employment tax on applicable earnings | Can face double taxation (C corporations) or pass-through taxation (S corporations) |

| Management Structure | Flexible – partners manage directly, often by consensus | Hierarchical – governed by a Board of Directors and designated officers |

| Decision Making | Informal – any partner can usually bind the business | Formal – major decisions require board approval and documented minutes |

| Capital Raising | Limited – relies on partner contributions, loans, or adding new partners | Broader – can raise funds by issuing stock |

| Business Continuity | Limited – dissolves if a partner exits, dies, or goes bankrupt | Perpetual – continues regardless of ownership changes |

| Administrative Burden | Low – minimal record-keeping and no annual meeting requirements | High – includes annual meetings, corporate minutes, and regular state filings |

| Attractiveness to Investors | Less appealing to institutional investors | More appealing, especially to venture capitalists, due to stock issuance options |

This comparison highlights the balance between simplicity and legal protection, helping you determine which structure aligns with your business goals.

By 2015, pass-through entities like partnerships and S corporations made up 95% of all business tax returns in the U.S., accounting for around 33.4 million filings [4]. Fast forward to 2017, and partnerships alone reported $2.2 trillion in net income, representing 38% of the business net income that year [4]. Clearly, these structures dominate in terms of numbers, but choosing between them goes beyond tax considerations – it’s about finding the legal framework that matches your business model.

"A corporation is a separate legal entity from its owners, offering liability protection. A partnership is legally tied to its owners, offering greater simplicity." – 1800Accountant [2]

From formation to management, understanding these distinctions allows you to align your business structure with your vision, risk tolerance, and growth ambitions. Which option fits your goals best?

Choosing the Right Structure for Your Business

What to Consider When Choosing

When deciding on a business structure, think about your long-term goals and how you prefer to operate. For instance, if you’re aiming to attract venture capital or go public within the next 5–10 years, it’s wise to incorporate early. Restructuring later can be both complicated and costly. Similarly, businesses in high-risk industries often benefit from the stronger liability protection that corporations provide.

Tax considerations also play a big role. As your profits grow – especially beyond the $60,000–$80,000 range – an S corporation might help you reduce self-employment taxes. While partnerships offer the simplicity of pass-through taxation, corporations allow you to retain earnings at a flat 21% corporate tax rate, which can be reinvested into your business.

Your management preferences matter too. Partnerships typically allow for more informal and collaborative decision-making among partners. On the other hand, corporations require formal board approvals and detailed record-keeping for major decisions. If you value flexibility and direct control, a partnership might suit you better. But if your goal is to create a business that can outlast your personal involvement or attract institutional investors, a corporation’s governance structure might be a better fit.

How BusinessAnywhere Can Help

Navigating these choices and the accompanying paperwork can feel overwhelming, but BusinessAnywhere simplifies the process. They make U.S. business registration straightforward, starting at $0 plus state fees. Their services include handling formation documents, ongoing compliance, and providing a registered agent (free for the first year with formation). They also offer EIN applications for $97, S-Corp tax election filing for $97, and bookkeeping services – all managed through a remote dashboard with 24/7 access. It’s a one-stop solution for keeping your business on track.

FAQs

When is an S corp better than a partnership?

An S corporation can be a smart choice if you’re looking to lower self-employment taxes and want limited liability protection – particularly if your business’s net income is above $60,000 to $80,000. Here’s why:

S corporations let active owners pay payroll taxes solely on their salary. Any remaining profits can then be distributed as dividends, which are not subject to self-employment tax. This setup can result in significant tax savings compared to a partnership, where all net income is subject to self-employment taxes.

That said, S corporations come with stricter ownership rules and additional regulatory requirements. These include limits on the number and type of shareholders and the need to maintain formalities like issuing stock and holding regular meetings.

How can partners reduce personal liability?

Partners can protect their personal assets by choosing a business structure that offers limited liability protection, like a Limited Liability Partnership (LLP) or a corporation. These structures ensure that personal assets remain separate from business debts and responsibilities. For example, in a corporation, the owners (shareholders) are only liable up to the amount they’ve invested. Similarly, LLPs allow partners to actively manage the business while safeguarding their personal assets from the company’s liabilities.

What happens to the business if an owner leaves or dies?

Partnerships face a unique challenge: they can dissolve if an owner leaves or passes away, unless the partnership agreement specifically outlines plans for succession or buyouts. This lack of continuity can make partnerships less stable in the long term. On the other hand, corporations operate differently. They enjoy continuous existence because ownership is tied to shares, not individuals. This means the business remains intact and operational regardless of changes in ownership or the loss of a shareholder, as the corporation exists as an independent entity.