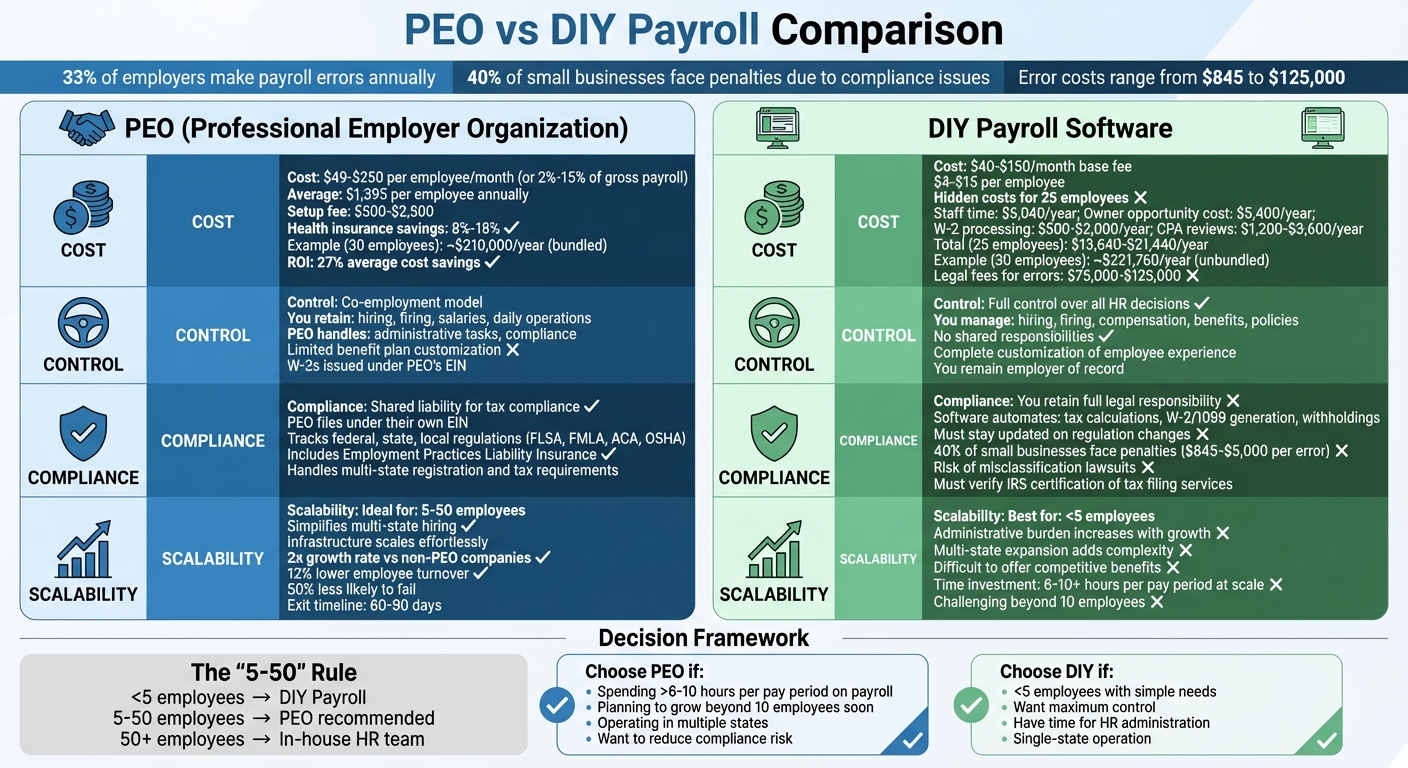

When your startup grows beyond a few employees, managing small business payroll basics and HR becomes increasingly complex – and costly if mistakes happen. Around 33% of employers make payroll errors annually, and 40% of small businesses face penalties due to compliance issues. These errors can cost anywhere from $845 to $125,000, depending on severity.

You have two main options for handling payroll:

- DIY Payroll: Software tools that automate payroll calculations and filings but leave compliance and legal responsibility on your shoulders.

- PEO (Professional Employer Organization): A co-employment model where the PEO handles payroll, benefits, and compliance, sharing legal responsibilities with your business.

Key Considerations:

- Cost: DIY payroll is cheaper upfront, but hidden costs (e.g., time, errors) can add up. PEOs cost more but bundle services like benefits and compliance support.

- Control: DIY offers full control over HR decisions, while PEOs take on administrative tasks.

- Compliance: PEOs share liability and offer expert compliance support, reducing risk.

- Scalability: PEOs are ideal for businesses with 5-50 employees, while DIY suits very small teams.

Quick Tip: If you’re spending more than 6–10 hours per pay period on payroll or planning to grow beyond 10 employees soon, a PEO might save you time, money, and headaches.

1. Professional Employer Organizations (PEOs)

A Professional Employer Organization (PEO) operates using a co-employment model. While you handle the day-to-day management of your team, the PEO acts as the Employer of Record for tax purposes. This means your employees’ paychecks and tax forms will list the PEO as their employer, even though they remain part of your team. Unlike DIY payroll tools, PEOs provide a comprehensive HR solution, reducing your administrative workload significantly.

Cost Analysis

PEOs typically charge either a flat monthly fee per employee (ranging from $49 to $250) or a percentage of gross payroll (2% to 15%), with the average cost landing around $1,395 per employee annually. Additionally, there may be a one-time setup fee between $500 and $2,500.

One of the key advantages of working with a PEO is access to enterprise-level health insurance rates. By leveraging pooled buying power, businesses can save approximately 8% to 18% compared to negotiating independently. Many companies report an average return on investment of 27% in cost savings and are 50% less likely to fail when they partner with a PEO.

Deepa Gandhi, Co-founder of Dagne Dover, highlighted the convenience of this model:

"I do not have any desire to build out a full in-house HR team that manages all the different parts. I’d rather be able to keep that team focused on culture and employee development and then they can leverage TriNet to manage the administrative logistics of people operations."

Operational Control

While PEOs handle many administrative functions, you maintain control over critical HR decisions, such as hiring, firing, setting salaries, and managing daily operations. However, benefit plan customization may be limited since employees are typically enrolled under the PEO’s master policy structure.

Compliance and Risk Management

PEOs take on shared liability for tax compliance by filing payroll taxes under their own Employer Identification Number (EIN). This arrangement helps shield your business from potential IRS audits. They also keep track of ever-changing regulations at federal, state, and local levels, including FLSA, FMLA, ACA, and OSHA requirements, ensuring you remain compliant. This is particularly important given that around 40% of small businesses face penalties annually due to payroll errors.

Additional risk management benefits include Employment Practices Liability Insurance and assistance with workers’ compensation claims. For businesses hiring in multiple states, PEOs handle complex registration and tax requirements. Selecting a PEO with Certified Professional Employer Organization (CPEO) status from the IRS is recommended, as this certification guarantees adherence to strict federal guidelines.

Scalability and Growth

PEOs are especially helpful for businesses looking to expand. They simplify hiring in new states by managing local employment laws and tax accounts, allowing you to focus on growth. Their infrastructure scales effortlessly as your team grows, whether you’re managing 10 employees or 50.

These services are most beneficial for companies with 5 to 50 employees. For startups with fewer than 10 employees, payroll software may be a more affordable option. On the other hand, businesses with over 50 employees might have the resources to build their own in-house HR teams. Companies using PEOs often experience twice the growth rate and 12% lower employee turnover compared to those that don’t.

If you decide to leave a PEO, the process typically takes 60 to 90 days to re-establish state tax accounts and implement new benefits.

sbb-itb-ba0a4be

2. DIY Payroll Solutions

DIY payroll software lets you handle payroll in-house while keeping full legal responsibility as the employer. Unlike the co-employment model used by PEOs, this approach gives you total control over HR decisions and daily operations. These platforms automatically handle tax calculations at federal, state, and local levels, generate W-2s and 1099s, and update to reflect changing regulations. While this can work well for very small teams, hidden costs like labor and compliance risks can add up quickly.

Cost Analysis

The upfront costs of payroll software typically range from $40 to $150 per month, plus $4 to $15 per employee. But these visible expenses only tell part of the story. For a company with 25 employees, the total yearly cost can fall between $13,640 and $21,440 when you include:

- Staff time: Around $5,040 annually

- Owner opportunity cost: Estimated at $5,400

- Year-end W-2 processing: $500 to $2,000

- CPA reviews: $1,200 to $3,600

Beyond these, mistakes can be costly. Misclassifying a worker or missing a tax deadline could lead to legal fees ranging from $75,000 to $125,000 if you face an employment lawsuit.

Operational Control

One of the biggest advantages of DIY payroll is the control it gives you. You make all decisions regarding hiring, firing, compensation, and benefits without sharing responsibilities with a third party. This flexibility allows you to tailor HR policies and the employee experience to fit your business. However, this level of control demands a significant investment of time and effort, which can strain your resources as your team grows.

Compliance and Risk Management

Most payroll platforms handle compliance basics automatically. They calculate withholdings, file taxes, report new hires, and adjust for multi-state tax rates. For example, in 2026, this will include managing Florida’s $15 minimum wage, Georgia’s flat tax phase-in, and changing county tax rates in Indiana. However, you remain legally responsible for ensuring everything is accurate.

When switching to a new payroll platform, it’s wise to run at least one payroll cycle through both your old and new systems to confirm calculations before fully transitioning. Also, check that any third-party tax filing service you use is IRS-certified. If they aren’t, you could be held liable for unpaid federal employment taxes.

Scalability and Growth

DIY payroll works best for small businesses with fewer than five employees. Beyond that, the administrative workload often outweighs the cost savings. Growth introduces new challenges, especially if you expand into multiple states. Each state brings its own tax rules, leave laws, and wage requirements, adding layers of complexity. Offering competitive benefits like health insurance or 401(k) plans can also become unmanageable without specialized tools or strong negotiating leverage.

Dan, Head of HR at Accounting Prose, puts it this way:

"The real cost of DIY HR isn’t what you spend… It’s what you lose."

If you expect to scale to 25 or more employees in the next 18 months, starting with a more comprehensive solution now can save you from a disruptive transition later. This lays the groundwork for choosing a payroll approach that aligns with your long-term goals.

Pros and Cons

When deciding between PEOs and DIY payroll, it’s all about weighing cost, control, compliance, and scalability. Each option has its own set of trade-offs, and the best choice depends on your startup’s size, growth plans, and risk tolerance.

Cost

The cost comparison isn’t as straightforward as it seems. DIY payroll appears cheaper upfront, with fees ranging from $40–$150 per month plus $4–$15 per employee. However, hidden costs can add up quickly. For example, a 30-employee startup operating in multiple states might end up spending $221,760 annually when you include health insurance premiums, separate workers’ comp policies, outsourced HR consultants, and the time spent on administration. On the other hand, a PEO would cost about $210,000 annually for the same setup, bundling services like health insurance (with 10%–20% lower rates) and HR support into one predictable fee. The cost savings often come from economies of scale and consolidated services.

Control

How much control do you want over HR operations? This is a critical question. DIY payroll gives you full authority over hiring, compensation, benefits, and policies. However, PEOs use a co-employment model, where they act as the tax employer of record and issue W-2s under their EIN. While this setup transfers some responsibilities and legal liabilities to the PEO, it also means sharing decision-making. As Maya Patel explains:

"The right choice depends on how much HR infrastructure you want to outsource and how much you want to own".

If you value autonomy, DIY payroll may feel more aligned with your goals. But if you’d rather offload some of the legal and administrative burdens, a PEO could be a better fit.

Compliance

Compliance is one area where PEOs shine, especially for startups that are scaling quickly. While DIY payroll software can automate tax filings and calculations, you’re still responsible for ensuring accuracy and keeping up with regulatory changes. This can be risky – 40% of small businesses face payroll penalties ranging from $845 to $5,000 per error. PEOs, on the other hand, share liability, stay updated on state-specific regulations, and often include Employment Practices Liability Insurance as part of their services. This added layer of compliance support can make a big difference as your business grows.

Scalability

Startups planning for rapid growth tend to benefit more from PEOs. DIY payroll works well for teams of fewer than 10 employees, but as your team grows, the administrative workload can become overwhelming. PEOs handle these growing pains seamlessly, taking care of HR operations so you don’t have to build an internal department from scratch. If you’re expecting to expand from 10 to 25+ employees in the next 18 months, starting with a PEO can save you the hassle of switching systems later. That said, once your company surpasses 50 employees, it often becomes more cost-effective to bring HR in-house using enterprise payroll tools.

Ultimately, balancing these factors – cost, control, compliance, and scalability – will help you choose the right HR solution for your startup.

Conclusion

Selecting the right HR solution for your startup boils down to understanding your current needs and anticipating how they might change. As Maya Patel wisely states, "The right answer evolves as the business evolves." Your decision should take into account factors like headcount, operational complexity, and the time you can realistically dedicate to HR tasks.

A helpful guideline is the "5-50" rule:

- If you have fewer than 5 employees, a DIY payroll system might be all you need.

- Between 5 and 50 employees, a PEO can offer added value through comprehensive support.

- For businesses with over 50 employees, building an in-house HR team could make more sense.

These thresholds can shift depending on specific circumstances, such as operating across multiple states, working in high-risk industries, or spending significant time – more than 5–10 hours a week – on HR-related responsibilities.

Each option comes with trade-offs. DIY payroll offers more control and lower upfront costs but leaves compliance and administrative tasks entirely on your plate. PEOs, on the other hand, handle these responsibilities and provide access to enterprise-level benefits, though at a higher cost.

Don’t forget to look beyond just the initial fees. The full cost of ownership includes hidden expenses like health insurance premiums, workers’ compensation, HR consultant fees, and the time spent on administrative tasks. Taking a closer look at these factors will help you understand the true financial impact of each option.

Ultimately, your HR strategy should align with your business goals. By doing so, you’ll not only streamline operations but also reduce risks as your startup grows.

FAQs

How do I calculate the real cost of DIY payroll?

When figuring out the real cost of DIY payroll, it’s important to look beyond just gross wages. You need to account for additional expenses like employer payroll taxes, employee benefits, administrative time spent managing payroll, and even the risk of penalties from errors.

For instance, if an employee earns a $100,000 salary, the actual cost to the employer can range between $180,000 and $240,000 annually when all these factors are included. In fact, payroll costs typically fall between 1.25 to 2.4 times the base salary, largely due to hidden costs like compliance risks and inefficiencies in the process.

Understanding these factors can help you make a more informed decision about whether to handle payroll yourself or explore other options.

What does co-employment change for my employees?

Co-employment means that your employees are considered to be employed by both your business and the PEO (Professional Employer Organization). This arrangement impacts areas like legal responsibilities, benefits administration, and compliance requirements. Generally, the PEO takes care of tasks like payroll processing and ensuring HR compliance, while you maintain control over daily operations and employee management.

When is the best time to switch to a PEO?

The best time to partner with a PEO is when your business starts needing more extensive HR support, assistance with navigating legal employment responsibilities, and help managing employee benefits. This typically occurs as your company grows and compliance requirements and operational demands become more complex. A PEO can streamline these tasks, freeing you up to focus on expanding your business effectively.