Closing your LLC is more than just stopping operations. If you don’t formally dissolve it, you’ll still owe annual fees, taxes, and could face legal risks like personal liability for unpaid debts. This guide simplifies the process into 8 clear steps to help you avoid penalties, protect your credit, and wrap things up properly.

Key Takeaways:

- Why it matters: Without dissolution, your LLC stays legally active, racking up fees and obligations.

- Costs to consider: States like California charge $800 annually, even if your LLC is inactive.

- Personal risks: Creditors can hold you personally liable if debts aren’t settled before distributing assets.

- Steps to take: File dissolution paperwork, notify creditors, pay debts, file final taxes, and cancel licenses.

By following these steps, you can close your LLC smoothly and avoid financial and legal headaches.

Why You Can’t Just Stop Operating Your LLC

Here’s the reality: your LLC doesn’t vanish just because you stop running it. As far as the state is concerned, your LLC remains an active entity. That means fees, taxes, and legal responsibilities continue to accrue – even if you’re no longer conducting business. Ignoring these obligations can lead to mounting penalties and serious complications, making a formal dissolution process essential.

Annual Fees and State Penalties Don’t Go Away

State laws require you to pay annual fees and franchise taxes as long as your LLC is registered. Even if your business isn’t earning a dime, these obligations don’t disappear. For example, California charges a minimum $800 franchise tax each year, regardless of revenue [1][2]. In Delaware, the $300 annual franchise tax applies in full – even if you dissolve your LLC on January 2nd [1][2]. And if your LLC is registered in multiple states, you’ll need to pay fees in every jurisdiction unless you file withdrawal paperwork in each state where you are registered [2].

What happens if you ignore these fees? The consequences can be severe. Unpaid amounts lead to penalties, which can eventually be sent to collections. If that happens, members listed as responsible parties could see their personal credit scores take a hit [1]. Additionally, an LLC that’s no longer in "Good Standing" can block you from starting new businesses in the same state, as many agencies check compliance history before granting approvals [1].

Tax Issues and IRS Penalties

Failing to file a final tax return can trigger hefty IRS penalties. The IRS requires annual filings, such as Form 1065 for multi-member LLCs or Form 1120-S for S-corporations, until you submit a return with the "Final Return" box checked [1][4]. If you don’t check that box, the IRS assumes your LLC is still active and will send penalty notices for future "missing" returns [2].

"In California, filing the cancellation form with the Secretary of State is not enough. If you do not also file a final Form 568 with the Franchise Tax Board and check the ‘Final’ box, the FTB keeps generating $800/year bills." – StartupOwl [2]

Some states, including Texas, Illinois, and New York, go a step further by requiring a tax clearance certificate before they’ll accept your dissolution paperwork [1][2]. Without this certificate, your dissolution filing can be rejected, leaving you responsible for ongoing fees and obligations.

Tax missteps can complicate the process, but unresolved asset distributions can create even bigger risks.

Personal Liability Risks

Failing to dissolve your LLC properly can expose members to personal liability. If you distribute business assets to yourself or other members before paying off debts, courts can "pierce the corporate veil" or reverse those distributions, making members personally responsible for the unpaid amounts [3][2]. Additionally, personal guarantees on business contracts – such as leases or loans – don’t disappear just because you’ve stopped operating. These obligations remain enforceable against you as an individual [1].

"If you pay members before creditors, courts can reverse those distributions and hold members personally liable." – StartupOwl [2]

Even after you stop using your LLC, creditors can still file claims against it. Without a formal dissolution that establishes a claims period (typically 90–180 days), there’s no clear end date for when creditors can come knocking [1]. This leaves you vulnerable to claims indefinitely, highlighting why it’s so important to follow the proper dissolution steps outlined next.

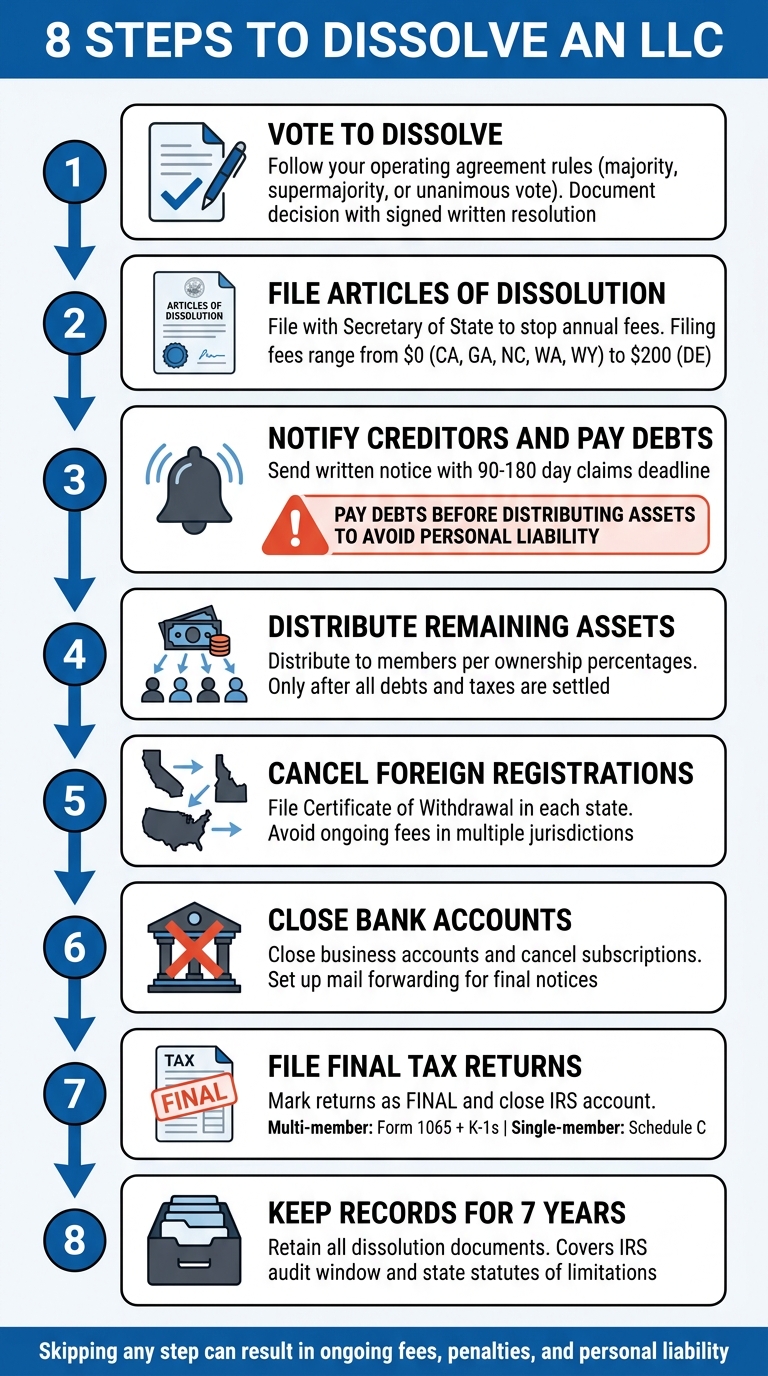

How to Dissolve an LLC: 8 Steps

Closing your LLC isn’t just about shutting the doors and walking away. There’s a specific process you need to follow to avoid legal and financial headaches. Each step is essential, and skipping any can lead to unnecessary complications. Here’s a breakdown of the LLC dissolution checklist to help you wrap things up the right way.

Step 1: Vote to Dissolve (Follow Your Operating Agreement)

Your operating agreement outlines how decisions like dissolution should be handled. Most require a majority vote, but some may need unanimous approval or a supermajority. If your agreement doesn’t specify voting rules, state laws will apply – usually requiring a majority vote [1].

Once the vote is finalized, document it with a signed written resolution. This serves as a formal record and protects you from disputes down the road. Even single-member LLCs should record their decision in writing [1].

Step 2: File Articles of Dissolution with Your State

To officially end your LLC’s legal existence, you’ll need to file dissolution paperwork with your state’s Secretary of State. This step stops the accumulation of annual fees and penalties. Depending on your state, the form may have a different name, such as Articles of Dissolution, Certificate of Cancellation, or Certificate of Termination [1].

| State | Filing Fee | Form Name |

|---|---|---|

| Delaware | $200 | Certificate of Cancellation |

| Alabama | $100 | Certificate of Dissolution |

| Pennsylvania | $70 | Certificate of Dissolution |

| New York | $60 | Articles of Dissolution |

| Texas | $40 | Certificate of Termination |

| Arizona | $35 | Articles of Termination |

| Alaska, Florida, Ohio, Virginia | $25 | Articles of Dissolution |

| Colorado | $10 | Statement of Dissolution |

| Illinois | $5 | Articles of Dissolution |

| California, Georgia, North Carolina, Washington, Wyoming | $0 | Certificate of Dissolution/Articles of Dissolution |

Fees as of February 2026 [1].

You’ll need to provide basic details like your LLC’s name, EIN, formation date, and confirmation that all debts and taxes are settled. In some states, such as Texas and New York, you’ll also need a tax clearance certificate before filing [1].

Step 3: Notify Creditors and Pay Off Debts

Send a written notice to all creditors, including vendors, landlords, and lenders, using a verifiable method. The notice should include a deadline (typically 90–180 days) for submitting claims, instructions on what information to provide, and a mailing address [1].

This notification sets a legal deadline for claims. After the deadline, most claims are no longer valid. In some states, you may need to publish a notice in a local newspaper to reach unknown creditors.

Make sure all valid debts are paid using LLC assets before distributing anything to members. Ignoring this step can lead to courts reversing distributions and holding you personally liable [1]. Also, terminate any ongoing contracts, like leases or utilities, to avoid further obligations.

Step 4: Distribute Remaining Assets to Members

Once all debts and taxes are settled, any remaining assets can be distributed to members. This should be done according to ownership percentages or as outlined in your operating agreement [1]. It’s critical to settle all creditor obligations first to avoid personal liability.

Document each distribution, including dates, amounts, and recipient details. Keep these records with your dissolution paperwork for future reference.

After distributions, focus on clearing up any lingering registrations or licenses.

Step 5: Cancel Foreign Registrations and Business Licenses

If your LLC operated in multiple states, you’ll need to file a Certificate of Withdrawal (or similar document) in each state. Without this step, you might still owe annual fees and franchise taxes even after dissolving your LLC in your home state [1].

Cancel all business licenses, permits, and DBA names. Procedures can vary, so contact the relevant agencies directly to ensure everything is properly closed.

Step 6: Close Bank Accounts and Cancel Subscriptions

Close your business bank accounts once all checks have cleared and tax payments are complete. Don’t forget to cancel any subscriptions tied to your LLC, such as software services, insurance policies, and utilities. You may also want to set up mail forwarding for your business address to catch any final notices or tax documents [1].

Step 7: File Final Tax Returns

Filing your final tax returns is a must to avoid future penalties. Mark them as final to signal the end of your obligations [1]. Multi-member LLCs should file Form 1065 and issue final K-1s, while single-member LLCs usually report on Schedule C.

"Simply stopping operations isn’t enough – if you don’t properly dissolve, you’ll continue owing annual fees, franchise taxes, and filing obligations indefinitely." – LLC.org [1]

Close payroll tax accounts by submitting final Forms 940 and 941. If you collected sales tax, file the final returns for those as well. To close your IRS account completely, send a letter to:

Internal Revenue Service

Cincinnati, OH 45999

Include your EIN, business name, address, and a copy of your Articles of Dissolution [1].

Step 8: Keep Records for 7 Years

Hold onto all dissolution-related records for at least seven years. This includes Articles of Dissolution, member voting documentation, creditor notices, final tax returns, asset distribution records, and bank account closure confirmations. Keeping these records will protect you in case of audits or legal claims [1].

A seven-year retention period generally covers the IRS audit window and most state statutes of limitations for business claims.

sbb-itb-ba0a4be

Dissolution vs. Withdrawal: What’s the Difference?

When closing or scaling back your LLC, it’s important to understand the difference between dissolution and withdrawal. These terms may seem interchangeable, but they apply to very different scenarios. Choosing the right process can save you from unexpected fees and lingering obligations in states where your business is registered.

Dissolution: Closing Your LLC Entirely

Dissolution refers to formally ending your LLC’s existence in the state where it was originally established. This involves filing Articles of Dissolution (or an equivalent form) to officially terminate the LLC’s active status in its home state. However, this is only part of the process. If your LLC is also registered as a foreign entity in other states, you’ll need to file separate withdrawal documents in each of those states to fully cancel your registration there [1].

"If an LLC or corporation does not file articles of dissolution, the state will continue to see the business as active. The company will then still be required to file annual reports and pay state fees and taxes."

– Deborah Sweeney, GM & VP, Small Business Services, Deluxe Corporation [5]

Failing to dissolve properly can leave your LLC on the hook for annual fees and taxes, even if the business has ceased operations.

Withdrawal: Stopping Operations in a Specific State

Withdrawal, on the other hand, applies when your LLC remains active in its home state but stops doing business in a particular state. This process, often called cancellation of foreign qualification, is used to end your LLC’s registration in a specific state while keeping it operational elsewhere [1].

For instance, imagine you formed your LLC in Delaware but registered to operate in both New York and California. If you decide to stop doing business in New York, you would file a Certificate of Withdrawal (or a similar form) with New York’s Secretary of State. Withdrawal fees vary widely, ranging from $0 to $200 per state [2].

Timing matters here. In states like Delaware, the $300 annual franchise tax isn’t prorated – dissolving your LLC on January 2nd still means you owe the full amount for the year [2]. Similarly, in California, failing to cancel your foreign registration could leave you liable for the state’s minimum franchise tax of $800 annually [2]. By understanding the timing and requirements, you can avoid unnecessary costs and complications.

Knowing whether to dissolve or withdraw – and handling the paperwork correctly – can make all the difference in wrapping up your LLC’s affairs smoothly.

Conclusion

Properly dissolving an LLC is essential to protect yourself from ongoing financial and legal risks. Skipping this process could leave you exposed to annual fees, IRS penalties, and even personal responsibility for business debts [1][2].

The eight-step process detailed in this guide ensures a thorough and lawful closure. Overlooking key steps – like notifying creditors, filing final tax returns, or canceling foreign registrations – could lead to unresolved debts, state-imposed fees, or even audits down the line. Most states require a creditor notification period (usually 90 to 120 days), giving you a clear legal window to settle claims and avoid surprise lawsuits [1][2]. Ensuring all creditors are informed and paid before distributing assets helps maintain the liability protection that your LLC was designed to provide.

Keeping detailed records for at least seven years is another critical safeguard. The IRS can audit tax returns for up to three years, or up to six years in cases of significant income discrepancies [2]. Documents like dissolution filings, final tax returns, and creditor communications form a crucial paper trail to address any future inquiries. By meeting all obligations and maintaining these records, you ensure a clean and secure closure of your LLC.

Whether you’re wrapping up a business that didn’t pan out or preparing for your next big idea, following the proper dissolution process minimizes risks and ensures peace of mind. Companies like BusinessAnywhere are here to assist, handling the paperwork and ensuring no detail is overlooked during this final step in your business journey.

FAQs

How long does it take to dissolve an LLC?

Dissolving an LLC typically takes anywhere from 1 to 12 weeks, depending on the state. For example, states like Delaware and Wyoming are known for quicker processing, often completing filings in about a week. Since timelines can vary, it’s a good idea to review the specific requirements and processing times for your state.

Do I still owe taxes if my LLC had no income?

Yes, even if your LLC didn’t generate any income, you might still have tax obligations. For instance, many states require annual franchise taxes or other mandatory filings, regardless of income. These responsibilities continue until the LLC is officially dissolved. To prevent future tax or legal complications, make sure to file your final tax returns and address any unpaid liabilities as part of the dissolution process.

What happens to my EIN after I dissolve my LLC?

When you dissolve your LLC, the Employer Identification Number (EIN) assigned to it remains active. If you want to deactivate it, you’ll need to send a written request to the IRS. Be sure to include the following details in your request:

- The EIN

- The legal name of the business

- The business address

- The reason for deactivation

It’s important to note that while the IRS doesn’t cancel EINs, they can deactivate them. Before submitting your request, make sure all outstanding tax returns and payments are fully addressed.