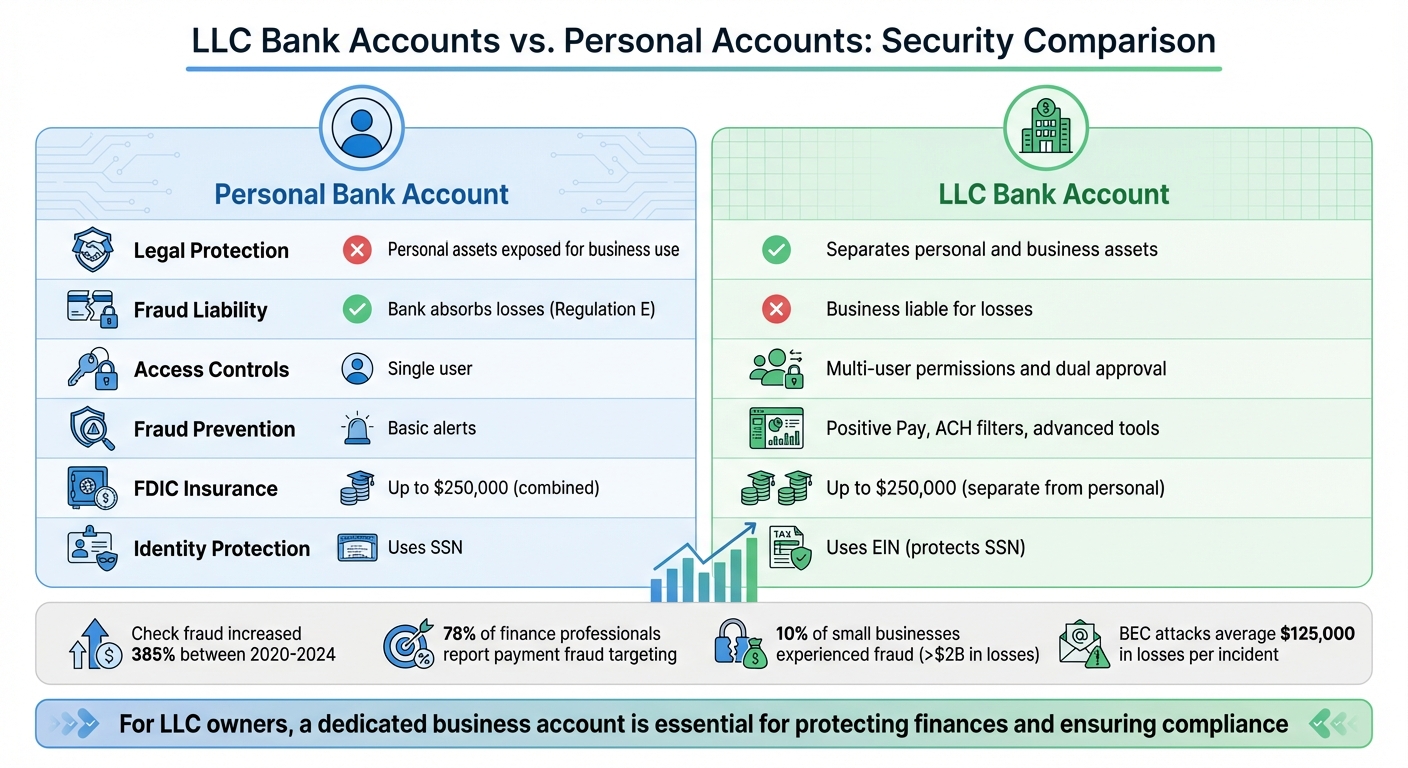

When it comes to financial security, LLC bank accounts and personal accounts serve very different purposes. An LLC account is designed to protect your personal assets by legally separating them from your business finances. Mixing personal and business funds risks exposing your personal assets to lawsuits or business debts. Personal accounts, while offering fraud protections under Regulation E, aren’t suited for business use and lack the advanced tools that LLC accounts provide.

Key Points:

- Legal Protection: LLC accounts help maintain the "corporate veil", shielding personal assets from business liabilities.

- Fraud Risks: LLC accounts are not covered by Regulation E, making businesses fully liable for fraud losses unless detected quickly.

- Advanced Security: LLC accounts offer features like dual authorization, Positive Pay, and ACH filters to mitigate fraud risks.

- FDIC Coverage: Deposits in LLC accounts are insured separately from personal accounts, up to $250,000 each.

- Privacy: LLC accounts use an EIN, reducing exposure of your SSN to vendors and customers.

Quick Comparison:

| Feature | Personal Bank Account | LLC Bank Account |

|---|---|---|

| Legal Protection | Personal assets exposed for business use | Separates personal and business assets |

| Fraud Liability | Bank absorbs losses (Regulation E) | Business liable for losses |

| Access Controls | Single user | Multi-user permissions and dual approval |

| Fraud Prevention | Basic alerts | Positive Pay, ACH filters, advanced tools |

| FDIC Insurance | Up to $250,000 (combined) | Up to $250,000 (separate from personal) |

If you own an LLC, opening a dedicated business account isn’t just a smart move – it’s essential for protecting your finances and ensuring compliance. If you haven’t yet, you should obtain an EIN for your LLC to streamline the application process.

Main Differences Between LLC and Personal Bank Accounts

Legal Separation and Account Purpose

The key distinction between LLC and personal bank accounts lies in their legal identity. An LLC bank account is tied to your business as a separate legal entity, using its own Employer Identification Number (EIN). In contrast, a personal account is directly linked to you as an individual, relying on your Social Security Number (SSN).

Keeping these accounts separate is crucial for maintaining the "corporate veil", which protects your personal assets from business-related liabilities. If you mix personal and business funds by using a personal account for business transactions, courts may "pierce the veil", potentially holding you personally responsible for business debts.

Additionally, most banks explicitly prohibit using personal accounts for business purposes. Violating these terms can lead to immediate account closure. LLC accounts also offer features tailored to businesses, such as merchant services for credit card payments, payroll integration, and multi-user access controls – features typically unavailable with personal accounts.

Now, let’s dive into how these distinctions impact fraud risks and cybersecurity measures.

Fraud and Cybersecurity Threats

Fraud protection rules vary significantly between personal and LLC accounts. Personal accounts are covered by Regulation E, which limits liability for unauthorized transactions. LLC accounts, however, are not protected under federal consumer regulations. As the FDIC explains:

Consumer protection rules do not apply to transactions conducted by a business, whether it be a deposit account or loan.

For LLC accounts, protection depends on state laws and the terms outlined in your bank’s deposit agreement. If your business account is hacked, you could be fully liable for losses unless the fraud is detected and reported quickly.

Business accounts are frequent targets for cybercriminals because they often hold larger balances and process higher transaction volumes. Threats such as ransomware, phishing emails, smishing (text scams), and vishing (voice scams) are commonly aimed at stealing business credentials.

Privacy and Account Anonymity

Another important difference is privacy. LLC accounts use an EIN instead of an SSN, adding a layer of protection. Your EIN appears on checks, invoices, and other documents, helping to separate your business’s credit profile from your personal one and reducing the risk of identity theft.

While banks collect personal information like your date of birth, address, and government-issued ID for fraud prevention, this data may also be shared with third parties for marketing purposes unless you opt out. Separating business and personal finances ensures your SSN isn’t exposed to vendors, customers, or potential cybercriminals.

Lastly, FDIC insurance treats LLC and personal accounts as distinct entities. Deposits held by an LLC are insured up to $250,000 separately from personal accounts at the same bank. This separation provides an extra layer of financial security.

Security Features of LLC Bank Accounts

Advanced Fraud Detection and Monitoring

LLC bank accounts come equipped with robust tools to help prevent fraud. One standout feature is Positive Pay, a service that cross-checks every check or ACH transaction against a list of pre-approved items from your business. If there’s a mismatch – like an incorrect amount, altered payee, or suspicious check number – the bank flags it for your review. As Mike Watercott, Working Capital Consultant at U.S. Bank, explains:

"Positive pay with payee verification significantly reduces the likelihood of fraudulent checks being processed."

This is particularly relevant when you consider that check fraud spiked by an alarming 385% between 2020 and 2024, according to U.S. Treasury data. Moreover, 78% of finance professionals report their organizations have been targeted by payment fraud, with 70% experiencing check fraud specifically.

LLC accounts also provide ACH blocks and filters, which let you control which transactions are allowed. For instance, you can block all ACH debits or create a whitelist of trusted partners. Additionally, tools like the Universal Payment Identification Code (UPIC) hide your actual account number, enabling customers to send payments without exposing sensitive banking details.

Many banks now use real-time account validation tools to confirm recipient information before processing transactions. Kasia Harvell, Risk Officer at U.S. Bank, highlights the importance of these tools:

"Using account validation tools can preclude fraudulent transactions by confirming account details in real-time."

Modern LLC accounts also integrate AI-powered monitoring systems to detect unusual activity instantly. Dave Pilot, Head of the Financial Crime Disruption team at U.S. Bank, elaborates:

"We employ real-time monitoring and advanced analytics to detect anomalies that may indicate fraud."

Some banks are even leveraging behavioral biometrics, which analyze how users interact with online banking – such as mouse movements and typing patterns – to verify identity and detect potential account takeovers [15, 18]. These proactive measures, combined with strict access controls, create a strong line of defense against fraud.

Dual Authorization and User Access Controls

LLC accounts offer a level of flexibility and control that personal accounts simply don’t. With these accounts, you can assign specific permissions to team members. For example, you might give your bookkeeper view-only access while requiring dual authorization for larger transactions – where one person initiates the transaction, and another approves it. As the FDIC explains:

"The separation makes it safe and easy to authorize employees to handle day-to-day business banking tasks without being involved in your personal finances."

This setup is especially effective in reducing risks, such as Business Email Compromise (BEC) attacks, which average over $125,000 in losses per incident.

To maintain security, it’s essential to regularly audit user permissions and limit account access. Your LLC operating agreement should clearly designate authorized signers, ensuring only specific individuals can withdraw funds or sign checks. These measures not only enhance security but also align with legal protections that safeguard your business.

Higher Liability Protection and Insurance Coverage

One of the key benefits of an LLC account is the protection it provides for your personal assets. By keeping business and personal finances separate, you help maintain the corporate veil – a legal barrier that shields your personal assets from business liabilities. Mixing personal and business funds could lead courts to "pierce the veil", potentially putting your home and savings at risk.

A separate business account also serves as evidence of your LLC’s legal separation, which is crucial if you face litigation or bankruptcy. In these cases, only business assets – not personal ones – are exposed. It’s worth noting that most banks explicitly prohibit using personal accounts for business purposes, and violating this rule could result in account closure.

LLC accounts also offer access to specialized fraud monitoring through merchant accounts and business credit cards. These tools not only enhance security but also help build a separate credit profile for your business. Additionally, by keeping LLC and personal accounts distinct, you could effectively secure up to $500,000 in total FDIC coverage at the same bank.

However, business accounts operate under stricter rules for disputes. For example, you typically have just 24 hours to report unauthorized ACH transactions, compared to 60 days for personal accounts. This makes daily reconciliation a must – preferably handled by an independent party – to catch fraudulent activity as early as possible.

Security Features of Personal Bank Accounts

Basic Fraud Protection Measures

Personal bank accounts come equipped with essential security features to help protect your money. These include multifactor authentication, biometric verification, real-time alerts, and encrypted mobile apps to safeguard against unauthorized transactions. If you use tools like tap-to-pay or mobile wallets such as Apple Pay, your actual card numbers are shielded by temporary tokens, adding an extra layer of protection.

Charles Banks, Vice President of Information Security at U.S. Bank, highlights the growing focus on digital security:

"Banking is a digital-first practice now… making sure those digital platforms are secure. That’s the biggest concern from a cybersecurity perspective."

These security measures are critical, especially in light of recent statistics. In 2023, the FBI received over 880,000 cybercrime complaints, with losses exceeding $12.5 billion. Check fraud has also surged, increasing by 84% in 2022 and causing $815 million in consumer losses. Thankfully, personal accounts offer consumer protection limits – if fraud is reported quickly, liability for unauthorized transactions is typically capped at $50.

While these protections are effective for personal use, they aren’t designed to handle the complexities of business transactions.

Why Personal Accounts Fall Short for Business Use

Although personal accounts offer strong fraud protections for individual users, they lack the advanced tools businesses need. According to the FDIC:

"Consumer protection rules do not apply to transactions conducted by a business, whether it be a deposit account or loan."

This means that Regulation E, which safeguards consumers from fraudulent transfers, does not extend to business transactions. In contrast, business accounts, such as those for LLCs, offer specialized features like Positive Pay and dual authorization – critical tools for preventing fraud. Personal accounts, however, do not provide these capabilities or other essentials like customized access controls, batch transaction limits, or multi-person approval workflows.

Using a personal account for business purposes can also undermine your LLC’s liability protection. Sharing login credentials, a common workaround for businesses using personal accounts, increases the risk of unauthorized access. The stakes are high: over 10% of small businesses have experienced fraud or hacking, resulting in more than $2 billion in losses. Additionally, 71% of businesses reported being targeted by payments fraud in 2021.

In short, personal accounts are built for individual needs, not the complexities of running a business. The risks of using them for business purposes can far outweigh their convenience.

sbb-itb-ba0a4be

LLC Bank Accounts vs. Personal Accounts: Security Comparison

When you put LLC and personal bank accounts side by side, the differences in security are striking. The biggest distinction lies in legal protection. Personal accounts are safeguarded under Regulation E of the Electronic Fund Transfer Act. This means that if fraud occurs, the bank usually absorbs the loss. However, LLC accounts – yes, even those for single-member LLCs – don’t enjoy this protection. Emily Heaslip from the U.S. Chamber of Commerce explains:

"Individual consumers are protected from fraudulent transfers under Regulation E of the Electronic Fund Transfer Act… But, small businesses aren’t covered by this regulation – not even those owned by a single individual."

In short, banks aren’t legally required to reimburse businesses for fraudulent activities. The table below breaks down the key differences between personal and LLC accounts.

Beyond legal protection, LLC accounts come equipped with features like Positive Pay, dual authorization, customizable transaction limits, and multi-user access controls. These tools are designed to reduce risks such as external hacking and internal fraud. On the other hand, personal accounts rely on basic monitoring and single-user access, leaving businesses more exposed to potential threats.

The risks are real. Over 10% of small businesses have faced fraud or hacking, leading to losses exceeding $2 billion. In 2021 alone, 71% of businesses were targeted by payments fraud. And let’s not forget the legal risk: using a personal account for business transactions could lead to "piercing the corporate veil", jeopardizing personal liability protections.

Security Features and Fraud Risk Comparison Table

Here’s a side-by-side look at how personal and LLC bank accounts stack up:

| Feature | Personal Bank Account | LLC Bank Account |

|---|---|---|

| Legal Fraud Protection | Protected under Regulation E (bank absorbs loss) | Not covered by Regulation E (business absorbs loss) |

| Authorization | Single-user authorization | Multi-user approval/dual authorization |

| Check/ACH Fraud Prevention | Basic signature verification | Positive Pay and ACH filtering services |

| Access Management | Single login credentials | Multiple user permissions |

| Transaction Limits | Standard daily limits | Customizable batch limits and ACH caps |

| Monitoring | Basic alerts for unusual activity | Advanced tools for detecting BEC and corporate account takeover |

| Liability Protection | Personal assets at risk for business liabilities | Separates personal assets from business debts |

| FDIC Insurance | Up to $250,000 (combined with personal funds) | Up to $250,000 (separate from personal funds) |

How BusinessAnywhere Helps with LLC Banking Setup

LLC Formation and Bank Account Setup Assistance

Opening an LLC bank account remotely can be tricky, especially when it comes to gathering the right documents. BusinessAnywhere simplifies this process by handling the paperwork and ensuring compliance with banking requirements. From formation documents to EIN verification letters, the platform prepares everything you need to meet the demands of banks.

If you’re a digital nomad or a remote business owner who can’t visit a bank in person, this service is especially helpful. BusinessAnywhere even assists with obtaining an EIN for $97, a crucial step for setting up your business account. Using an EIN instead of your Social Security Number not only protects your personal identity but also establishes your business as a separate credit entity. This is a valuable safeguard, even for single-member LLCs.

Privacy Protection and Compliance Services

Once your LLC bank account is set up, maintaining privacy and compliance becomes essential. BusinessAnywhere offers ongoing support to keep your business secure. For instance, their registered agent service (free for the first year, then $147 annually) provides a professional physical address for legal correspondence. This keeps your home address off public records, adding an extra layer of privacy.

Additionally, their virtual mailbox service (starting at $20/month) gives you a legitimate business address in states like Florida, Wyoming, Arizona, or New Mexico – states often required by banks. To ensure your business stays legally sound, BusinessAnywhere’s compliance support helps you avoid mixing personal and business funds, protecting the legal separation of your LLC.

Conclusion

Opening an LLC bank account provides a level of security and separation that personal accounts simply can’t match. By keeping your personal assets legally distinct from your business finances, you protect yourself from potential claims by business creditors or lawsuits. As Eric Calaman, Business Executive at Bank of America, puts it:

Generally no one can come after the owner’s personal assets.

Beyond this legal protection, LLC accounts come equipped with advanced fraud prevention tools that aren’t available with personal accounts. These include features like customized user access controls, dual authorization for significant transactions, and monitoring systems designed to detect scams targeting businesses, such as fake invoices or fraudulent wire transfers. These safeguards are especially critical if multiple individuals need access to your business finances.

Another key benefit is FDIC insurance, which covers your LLC account separately from personal accounts – up to $250,000 per account. This effectively doubles your coverage at the same bank. Additionally, the separation simplifies compliance and audits, making it easier to manage your financial records. Combined with tailored insurance options, these features enhance your overall risk management strategy.

Keeping your business and personal finances separate also ensures a clean audit trail, which simplifies tax preparation and helps you stay compliant with IRS regulations. Blurring the lines between the two can lead to serious consequences, such as "piercing the corporate veil", where courts might hold you personally liable for business debts. No matter the size or scope of your business, the security and organizational advantages of an LLC account far outweigh the minimal costs involved.

If you’ve gone through the effort of forming an LLC, don’t overlook the importance of opening a business bank account for your LLC. It’s a critical step to protect your finances and maintain the legal protections your LLC was designed to provide.

FAQs

How does an LLC bank account provide better security than a personal account?

LLC bank accounts come equipped with robust security measures tailored to safeguard business finances. Features like multi-factor authentication, strong password requirements, and real-time alerts for unusual activity work together to block unauthorized access and quickly identify potential risks.

Banks also utilize sophisticated fraud prevention tools, including access controls and transaction monitoring, to ensure only authorized individuals can handle the account. These protections are especially critical for high-risk activities, such as wire transfers or ACH payments, providing an added shield against cyberattacks and financial fraud.

How does an LLC bank account help protect my personal assets?

Using a dedicated bank account for your LLC is a smart way to safeguard your personal assets. It sets a clear boundary between your business and personal finances, reinforcing the LLC’s status as a separate legal entity. This separation ensures that if your business faces debts or legal issues, only the assets owned by the LLC are at risk – not your personal belongings like your home or savings.

By keeping your LLC’s finances in their own account, you avoid the pitfalls of mixing personal and business funds, a practice known as commingling. Commingling can weaken the liability protection your LLC provides, potentially putting your personal assets in jeopardy. A separate LLC bank account not only helps maintain these legal protections but also shows that you’re following sound financial practices.

What are the risks of using a personal bank account for business purposes?

Using your personal bank account for business transactions might seem convenient at first, but it can quickly lead to a host of problems. Mixing personal and business finances can cause accounting headaches, make tracking expenses a nightmare, and even create confusion around cash flow. For LLC owners, it’s an even bigger risk – it could blur the lines between personal and business assets, potentially putting your personal property at risk in the event of legal issues.

Another concern? Personal accounts often lack the robust security features that business accounts offer, leaving you more vulnerable to fraud or theft. On top of that, managing taxes and staying compliant with financial regulations becomes far more complicated, which could result in penalties or other legal troubles. By opening a dedicated business account, you can protect your assets, simplify your financial processes, and ensure your business stays on solid legal and financial ground.