Managing LLC vs Sole Proprietorship for real estate investors requires a solid banking setup to protect your assets, simplify taxes, and stay organized. Here’s the short answer: each LLC should ideally have its own bank account. This ensures liability protection, clean tax records, and easier bookkeeping. However, for small portfolios with limited transactions, a single account may work if you carefully track income and expenses for each property.

Key Points:

- Separate Accounts: Best for multiple LLCs or larger portfolios. Protects personal assets, simplifies tax prep, and reduces audit risks.

- Single Account: Works for 1-2 properties under one LLC if you maintain strict recordkeeping and use tools like transaction tags or sub-accounts.

- Why It Matters: Mixing funds can lead to legal risks (piercing the corporate veil) and tax challenges (messy Schedule E reporting).

Quick Setup Steps:

- Get an EIN for each LLC (free on the IRS website).

- Open a business bank account with a bank that supports real estate businesses.

- Use tools like sub-accounts or property management software to track transactions.

For growing portfolios or stricter compliance, separate accounts are the safer, more efficient choice.

Risks and Benefits of Using One Account for Multiple LLCs

Using a single bank account for multiple LLCs might seem like a convenient way to streamline finances, but it comes with serious legal and financial risks. While it does reduce the number of accounts you need to handle, the potential downsides – especially around protecting your personal assets and ensuring tax compliance – often outweigh the simplicity.

Legal Risks: Piercing the Corporate Veil

The corporate veil is what legally separates your personal assets from your LLC’s liabilities, shielding things like your home, savings, and investments from lawsuits or creditors. However, commingling funds – mixing money between LLCs or between business and personal accounts – is one of the fastest ways to lose that protection. Courts may decide to treat your LLCs as a single entity, jeopardizing your personal assets in the process.

Brandon Hall, CPA and Founder of Hall CPA PLLC, emphasizes this risk:

"Attorneys will attempt to ‘pierce the corporate veil’ and they will most certainly use your commingling patterns as reasoning to do so."

Different states have their own standards for piercing the veil. For instance, Florida looks at whether the LLC is just a "mere instrumentality" and if the owner engaged in "improper conduct", while Texas focuses on whether the entity was used to commit actual fraud. Regardless of the state, keeping separate accounts is critical for proving the independence of each LLC in a legal dispute. This separation also plays a key role in maintaining clean tax records.

Tax Risks: Schedule E Reporting Problems

The IRS requires landlords to report income and expenses for each property individually on Schedule E. Using a single account for multiple LLCs can make this process messy and raise red flags about poor financial practices. When accounts are mixed, it’s harder to prove that certain expenses were tied to a specific property, which could lead to the IRS disallowing deductions.

Saad Dar, VP of Sales and Partnerships at Baselane, explains the importance of keeping accounts separate:

"The IRS requires landlords to report income and expenses for each property on Schedule E. Having a dedicated account… provides clear transaction records for accurate landlord tax deductions."

Without clear, property-specific records, it becomes difficult to assess which properties are performing well and which ones are struggling, making it harder to make smart financial decisions.

Bookkeeping and Reconciliation Challenges

On top of the legal and tax risks, combining accounts makes bookkeeping much harder. Sorting through a single bank statement to figure out which expense belongs to which LLC can be a time-consuming and error-prone process. By contrast, using separate accounts for each LLC can cut bookkeeping and reconciliation time by as much as 50% to 60%.

Matas Pranckevicius, SMB Content Manager at Relay, highlights the benefits of account segregation:

"Whoever does your bookkeeping will be better set up for success if banking information for each property is segregated."

Additionally, unclear financial records can hurt your credibility with lenders when you’re looking for financing. Some states even require that specific funds, like tenant security deposits, be held in separate accounts, and failing to comply could lead to fines or penalties.

When One Account May Work for Your Portfolio

When it comes to managing a small portfolio, using a single account can simplify things and save money. However, this approach demands precise recordkeeping to avoid the legal and tax risks that come with mixing funds. If you’re meticulous about tracking every transaction, a single account might just work for you.

Small Portfolios with Limited Transactions

For portfolios with just 1 or 2 properties owned under a single entity, a single account can be a practical choice. The deciding factor here is transaction volume. If your properties only generate a few transactions – like one rent payment monthly, occasional utility bills, and sporadic maintenance costs – you can keep everything organized with proper systems.

Saad Dar, VP of Sales and Partnerships at Baselane, explains when this setup is feasible:

"If you own several properties under a single entity… One operating account with property-level transaction tracking… saves time and reduces account clutter."

That said, as the number of transactions grows, so does the likelihood of bookkeeping errors and fund mismanagement. If you find it hard to recall which expense belongs to which property, it’s a sign that managing everything through one account may no longer be viable.

Cost Savings for Properties with Low Cash Flow

For properties with limited cash flow, banking fees can quickly cut into profits. Many traditional business checking accounts charge $12 to $50 per month unless you maintain minimum balances between $500 and $30,000. If you’re managing five properties, that could mean monthly fees of $60 to $250 – or up to $3,000 annually – just to keep all accounts active.

With a single account, you only need to meet one fee-waiver requirement, which can significantly lower costs. For instance, maintaining $2,000 in one Chase Business Complete Banking account (waiving its $15 monthly fee) is much easier than spreading $10,000 across five accounts. Additionally, some modern banking platforms tailored to landlords, like Baselane, Bluevine, and Grasshopper, offer $0 monthly fees with no minimum balance requirements, further reducing expenses.

While the cost advantages are clear, staying compliant with legal and tax obligations is critical when using one account.

Staying Compliant with a Single Account

If you choose to manage multiple properties under one LLC with a single account, maintaining compliance boils down to disciplined recordkeeping. Never mix personal and business funds. Keeping these separate is essential to protect your LLC’s liability shield and tax benefits.

Leverage transaction tagging in your accounting software to assign every income and expense to the appropriate property and Schedule E category. Many property management platforms can automate this process, minimizing manual errors. You can also create sub-accounts within your main account to allocate funds for specific purposes, such as "Property A Operating", "Property B Reserves", or "Tax Savings". Some banking platforms even allow up to 20 sub-accounts under one primary login, helping you stay organized without juggling multiple bank statements.

To keep everything running smoothly, reconcile your transactions monthly, automate transfers (like setting aside 5% to 10% of rent for reserves), and document any personal contributions as formal capital inputs. While this approach requires consistent effort, it’s the only way to make a single-account system work without exposing yourself to unnecessary risks.

Benefits of Separate Bank Accounts for Each LLC

Keeping separate bank accounts for each LLC provides clear, practical advantages that can strengthen your business framework and simplify daily operations. These benefits only grow in importance as your portfolio expands or if you find yourself dealing with legal challenges.

Stronger Liability Protection

Having individual bank accounts for each LLC reinforces the legal separation between your rental property businesses and your personal assets. By maintaining distinct accounts, you clearly show that each LLC operates as a standalone business entity, not as an extension of your personal finances.

One of the biggest dangers of shared accounts is commingling funds. If personal and business expenses are mixed in the same account, courts may decide to "pierce the corporate veil." This legal action allows plaintiffs to go after your personal savings, home, and other assets to satisfy a judgment.

"A single bank account containing both personal grocery purchases and rent deposits is evidence that the business and your personal life are one and the same. This allows plaintiffs to ‘pierce the corporate veil,’ making your personal savings and home vulnerable to a judgment." – Saad Dar, VP of Sales and Partnerships, Baselane

By keeping accounts separate, any lawsuit or debt tied to one property remains confined to that specific LLC. This ensures that your other properties and personal wealth stay protected. Bank statements from dedicated accounts also provide clear documentation that each LLC handles its own income and expenses, reinforcing its legal independence in any dispute.

Easier Tax Preparation

Tax season becomes much more manageable when each property operates with its own bank account. The IRS requires landlords to report income and expenses for each rental property separately on Schedule E. With transactions already sorted by property, you can generate clean financial reports and streamline the Schedule E process without the headache of sifting through mixed data.

This separation also offers protection during IRS audits. Only the records for the specific LLC under review will need to be examined, keeping other entities out of the spotlight. Additionally, organized accounts can save you money on professional fees, as your accountant won’t have to spend extra time untangling transactions.

Better Financial Organization

Separate accounts provide a clear, real-time view of each property’s financial health. You can easily track net operating income (NOI), maintenance costs, and cash flow without relying on complicated spreadsheets or manual calculations. This transparency helps you make smarter decisions, like identifying which properties are performing well and which ones may need rent adjustments, reinvestment, or even consideration for sale.

When expanding your portfolio, having property-specific bank statements can also work in your favor. These statements act as a "financial resume", showcasing your professionalism to lenders and potential investment partners.

"Beautiful reports from a dedicated account… make you look reliable, disciplined, and credible. This trust is crucial for securing partnerships and joint ventures to fund your next purchase." – Saad Dar, VP of Sales and Partnerships, Baselane

Additionally, separate accounts make it easier to comply with state laws. Many states require landlords to hold security deposits in dedicated escrow or trust accounts, separate from operating funds. Property-specific accounts simplify this process, ensuring compliance without adding unnecessary administrative burdens. These organizational benefits pave the way for smoother management and better financial oversight.

How to Set Up Bank Accounts for Rental Property LLCs

Setting up bank accounts for your rental property LLCs doesn’t have to be complicated. By following these three steps, you can meet legal requirements while keeping your business operations smooth and organized.

Step 1: Obtain an EIN for Each LLC

To align with your liability protection strategy, the first thing you’ll need is an Employer Identification Number (EIN) for each LLC. This unique identifier, issued by the IRS, is mandatory for opening a business bank account.

The good news? Getting an EIN is free if you apply directly through the IRS website. The process is straightforward, takes just a few minutes, and you’ll receive your EIN immediately upon completing the online application. Be cautious of fee-based third-party services that charge for this free process.

If you prefer assistance, services like BusinessAnywhere offer EIN applications for $97. Once you have your EIN, gather all necessary documents and head to your chosen bank.

Step 2: Choose a Bank That Fits Your Needs

Finding the right bank is crucial, especially one that understands the needs of real estate businesses. Online banks and fintech platforms often process LLC applications faster – typically within 1–3 business days – and many don’t charge monthly maintenance fees. On the other hand, traditional banks may take longer (5–10 business days) and charge fees ranging from $10 to $30 per month.

When preparing to open your account, you’ll need the following documents:

- Articles of Organization (or Certificate of Formation)

- Operating Agreement

- EIN confirmation letter

- Government-issued ID for all authorized signers

Banks also require a physical business address for registration. If you want to streamline your finances, look for banks that allow unlimited virtual sub-accounts under one main login. This feature makes it easy to separate operating funds, security deposits, and tax reserves without needing multiple standalone accounts. Bonus: property-specific sub-accounts can save you 50–60% of your time on year-end bookkeeping.

Once you’ve chosen a bank and gathered your documents, you can take an extra step to enhance your LLC’s professional image by setting up a dedicated business address.

Step 3: Use a Virtual Mailbox for Your Business Address

Banks require a physical business address, not a P.O. Box, so using a virtual address to open a business bank account can be a great solution. It gives you a professional U.S. business address while keeping your home address private.

For example, BusinessAnywhere offers virtual mailbox services starting at $20 per month. Their plans include a legitimate U.S. business address, unlimited mail scanning, and global forwarding. This allows you to access your LLC’s banking documents digitally from anywhere, eliminating the hassle of waiting for physical mail delivery.

A virtual mailbox not only simplifies mail management but also helps maintain a clear boundary between your personal and business affairs – an important step in preserving the legal protection of your LLC structure.

sbb-itb-ba0a4be

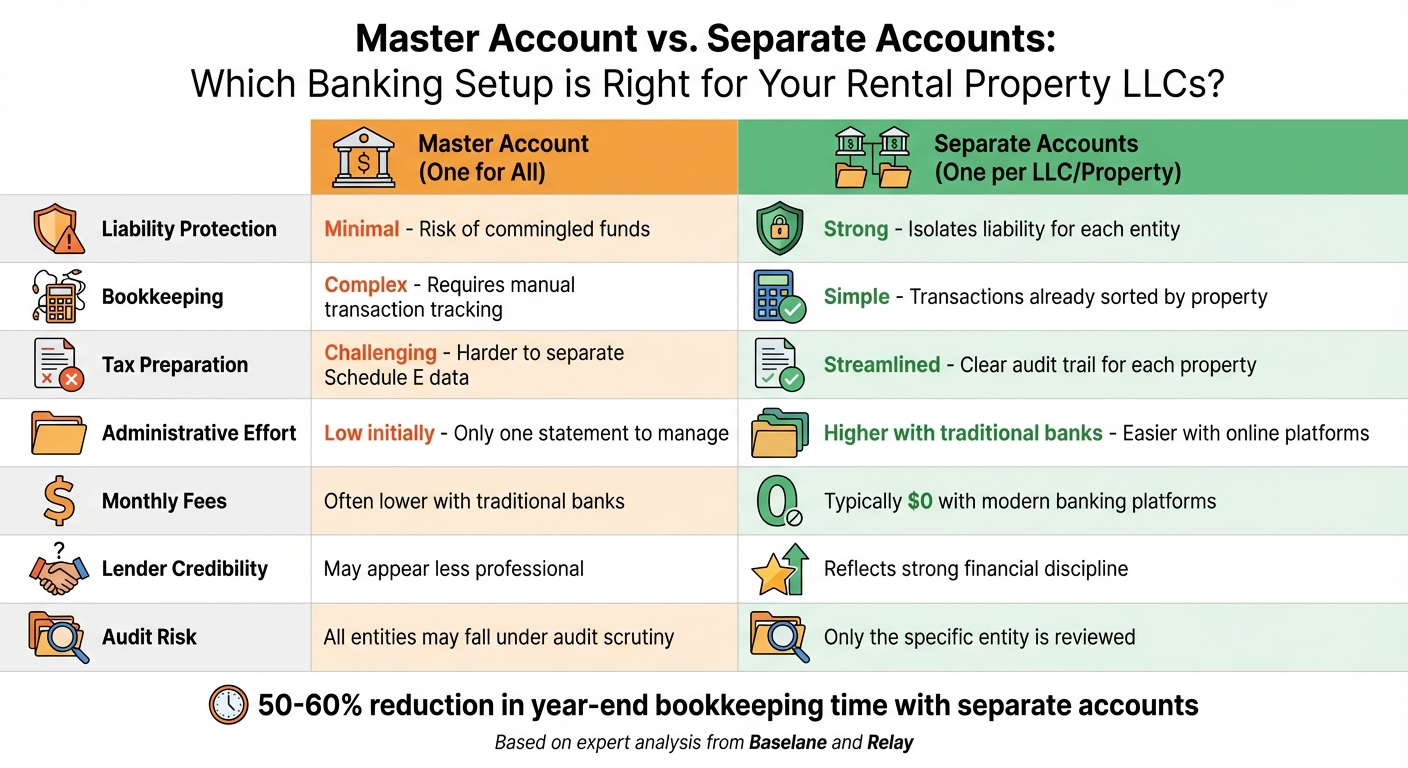

Master Account vs. Separate Accounts: A Comparison

When managing rental property LLCs, deciding between a master account and separate accounts boils down to factors like portfolio size, risk tolerance, and bookkeeping preferences. Both approaches come with their own set of advantages and disadvantages, particularly in liability protection, tax reporting, and operational efficiency.

A master account offers simplicity upfront, requiring just one monthly reconciliation. However, this convenience comes at a cost. Combining funds from multiple properties can weaken liability protection, potentially piercing the corporate veil. Additionally, manually allocating transactions to each property adds complexity during tax season.

On the other hand, separate accounts provide stronger liability protection by keeping each LLC’s finances distinct. This setup also simplifies tax preparation, as property-specific records are already organized. While traditional banks used to charge fees for maintaining multiple accounts, many online banking platforms now offer fee-free accounts, no minimum balance requirements, and even virtual sub-accounts accessible from a single login.

"Maintaining property-specific accounts can cut your year-end reconciliation and bookkeeping time by 50–60%."

- Saad Dar, VP of Sales and Partnerships at Baselane

"Your current portfolio is your resume for the bank or lending institution, telling them how safe a bet you are."

- Matas Pranckevicius, SMB Content Manager at Relay

Modern online banking platforms further reduce administrative burdens, making the separate accounts strategy more appealing. Below is a breakdown of the pros and cons of each approach.

Comparison Table: Pros and Cons

| Factor | Master Account (One for All) | Separate Accounts (One per LLC/Property) |

|---|---|---|

| Liability Protection | Minimal; risk of commingled funds impacting protection | Strong; isolates liability for each entity |

| Bookkeeping | Complex; requires manual transaction tracking | Simple; transactions already sorted by property |

| Tax Preparation | Challenging; harder to separate Schedule E data | Streamlined; clear audit trail for each property |

| Administrative Effort | Low initially; only one statement to manage | Higher with traditional banks; easier with online platforms |

| Monthly Fees | Often lower with traditional banks | Typically $0 with modern banking platforms |

| Lender Credibility | May appear less professional | Reflects strong financial discipline |

| Audit Risk | All entities may fall under audit scrutiny | Only the specific entity is reviewed |

Tax and Audit Benefits of Separate Accounts

Simpler Schedule E Reporting

Keeping separate accounts for each rental property LLC doesn’t just help with liability protection and bookkeeping – it also makes tax reporting on Schedule E much easier. When every property has its own bank account, transactions are already sorted by property, eliminating the need to manually allocate expenses.

Many modern banking platforms tailored for real estate can automatically categorize transactions into IRS Schedule E buckets like mortgage interest, property taxes, repairs, and utilities. This means your financial records are essentially "tax-ready" throughout the year. Instead of spending hours sifting through receipts, you can generate property-specific reports directly from your bank. This ensures all deductible expenses are captured in one place, making it simpler to justify them if the IRS ever questions your return.

Additionally, accurate records specific to each property support the legal separation of each LLC and make complex filings, like Form 1065 and Schedule K-1, much more manageable. For multi-member LLCs, issuing Schedule K-1 forms requires precise profit and loss tracking – something that’s nearly impossible if funds are mixed together. This level of organization also helps lower the chances of an audit.

Lower Audit Risk

Separate accounts don’t just simplify reporting – they also create a clear financial boundary between your personal life and each business entity. This distinction is crucial because mixing personal and business funds is a major red flag for IRS auditors. If the same account is used for groceries, personal credit card payments, and rental property expenses, it can draw unwanted attention and potentially lead to "piercing the corporate veil", where courts disregard your LLC’s legal protections.

In the unfortunate event of an audit, having dedicated accounts ensures that only the finances of the specific entity under review are examined. Your personal funds and other properties remain shielded from unnecessary scrutiny.

"If you face an audit, it is definitely better if only the funds from the entity (or entities) being audited are reviewed" – Matas Pranckevicius, SMB Content Manager at Relay

Clear, property-specific records also reduce bookkeeping errors and ensure no deductions are overlooked, which could otherwise raise IRS flags. The IRS mandates that business owners keep receipts for expenses over $75 for six years. With separate accounts, every transaction is documented, creating a transparent audit trail that can withstand IRS review.

Best Practices for Managing Your LLC Bank Accounts

Keep Accurate Records

Keeping accurate records is a cornerstone of managing your LLC bank accounts effectively. Each LLC should have its own separate bank account tied to its unique EIN. Mixing personal and business funds? That’s a big no-no. To stay on top of things, reconcile your bank statements every month and sync them with accounting software like QuickBooks. This not only helps you spot errors but also keeps your records clean and organized.

Many banking platforms now let you use internal tags or sub-accounts, making it easier to track income and expenses for specific properties. For even better organization, consider setting up sub-accounts for different purposes – like operating expenses, reserves, or security deposits. Speaking of security deposits, some states require these to be held in separate escrow or trust accounts, so double-check your local regulations.

A smart move? Automate reserve funding by setting up rules to transfer 5–10% of monthly rent into a maintenance fund. These steps not only help you stay organized but also strengthen your liability protection and prepare you for audits.

"The court will respect your LLC as much as you do. Treat it like a business, and it will protect you like one." – Toby Mathis, Esq., Founder, Anderson Business Advisors

Finally, schedule periodic reviews to ensure your records are always accurate and compliant.

Schedule Regular Financial Reviews

Accurate records are just the beginning – you also need to keep a close eye on them. Set up quarterly reviews to check account balances, spot potential errors, and adjust any automated transfers as needed. These reviews are especially important for staying on top of compliance requirements.

When the year wraps up, year-end reconciliations are a must. They’ll help you prep for taxes and make sure you’ve captured every deductible expense. Thanks to digital banking platforms, you can monitor cash flow and property performance metrics in real time. This way, you’ll always know where your money is going and can tweak your banking setup as needed.

Use BusinessAnywhere Services for Easier Management

Managing multiple LLCs can get complicated, but tools like BusinessAnywhere make it easier. Their services are designed to complement your automated banking and accounting practices. For example, their virtual mailbox gives you a compliant U.S. business address, unlimited mail scanning, and global forwarding.

Need the [best registered agent service](https://businessanywhere.io/best-registered-agent-service/)? They’ve got you covered with a service that’s free for the first year and costs $147 annually after that. They also offer EIN application assistance for a one-time fee of $97. With everything centralized in one online dashboard, setting up and maintaining your LLC bank accounts becomes a lot more manageable.

Conclusion: Choosing the Right Banking Setup for Your Portfolio

Main Takeaways

The ideal banking setup for your rental property LLCs comes down to three main factors: portfolio size, liability protection needs, and administrative capacity. If you’re managing one or two properties under a real estate LLC, a single master account with tracking tags could be sufficient – provided you stay on top of detailed record-keeping. For those with three to five properties, virtual sub-accounts can offer better organization, especially for Schedule E reporting, without the hassle of juggling multiple logins. For portfolios with six or more units – or if you operate across multiple LLCs – fully separate accounts become a must. They ensure your legal structure is protected and make audits far less stressful.

Separate accounts not only safeguard liability protection but also simplify bookkeeping at tax time. While there may be some additional fees, the benefits outweigh the costs. Clear, property-specific financial records also enhance your credibility with lenders and reduce audit risks by creating an organized paper trail for each property.

Next Steps for Your LLC Banking Setup

Ready to set up your banking system? Here’s a straightforward plan: Start by obtaining an EIN for each LLC so you can open dedicated business accounts. Then, choose a bank that caters to small businesses, offering features like virtual sub-accounts, automated transfers, and reasonable fees. Keep in mind that banks require a physical business address – PO Boxes won’t cut it.

If you need help setting up, BusinessAnywhere can make the process smoother. Their virtual mailbox service provides a compliant U.S. business address, complete with unlimited mail scanning and global forwarding, starting at just $20/month for their Basic plan. Need an EIN? They’ll handle the application for a one-time fee of $97. Plus, their registered agent service is free for the first year, then $147 annually, giving you a professional address for legal documents. Everything is managed through a single online dashboard, so you can focus on growing your portfolio without worrying about compliance headaches.

Getting your banking structure right from the start will save you hours of reconciliation work and help you avoid potential legal pitfalls as your rental business grows.

FAQs

What are the risks of using the same bank account for multiple rental property LLCs?

Using one bank account for multiple rental property LLCs can create serious issues, starting with commingling of funds. This practice can undermine the liability protection that LLCs are meant to provide, potentially exposing your personal assets to legal risks. In some cases, it might even lead to the corporate veil being pierced during legal disputes, leaving you personally accountable.

On top of that, it makes bookkeeping and tax reporting much more complicated. Keeping track of income and expenses for each property becomes a challenge, increasing the chances of mistakes, compliance problems, or even audits. To safeguard your assets and maintain clear financial records, it’s usually a good idea to open separate bank accounts for each LLC.

Why is it helpful to have separate bank accounts for each rental property LLC when filing taxes?

Keeping separate bank accounts for each rental property LLC can make tax reporting much more straightforward. By isolating the income and expenses of each property, you’ll have a clear financial picture that allows for precise, property-specific reporting. This approach reduces the likelihood of mistakes when it’s time to prepare your tax filings.

On top of that, using distinct accounts streamlines bookkeeping and helps you stay aligned with IRS guidelines. It eliminates the risk of mixing personal and business funds, which is essential for preserving the liability protection that your LLC provides.

Can I use one bank account to manage multiple rental properties?

If all your rental properties are under the same LLC or legal entity, using a single business bank account is perfectly fine. It keeps things straightforward by centralizing income and expenses for that one entity, making financial tracking much easier.

On the other hand, if you manage properties through multiple LLCs, it’s a smart move to have separate accounts for each. This approach not only simplifies bookkeeping but also helps maintain clear liability boundaries between properties. For tailored advice, it’s always a good idea to consult a financial professional who can guide you on the best setup for your specific portfolio.