If your business invests in research and development (R&D), leveraging tax credits can significantly reduce your expenses. Here’s what you need to know:

- Federal R&D Tax Credit: Reduces your tax bill by 6%-13% of qualified research expenses (QREs). Startups can offset up to $500,000 annually in payroll taxes.

- State-Level Credits: Offered by ~38 states, these can add 5%-20% more savings. Some states even allow refunds or credit transfers.

- Qualified Expenses: Include wages, supplies, 65% of contractor payments, and certain cloud computing costs.

- Eligibility: Activities must meet the IRS’s four-part test, focusing on innovation, uncertainty, and experimentation.

- Filing: Use IRS Form 6765 for federal credits and follow state-specific processes. Starting in 2026, detailed reporting will be mandatory.

R&D tax credits are a powerful way to boost cash flow, especially for startups. Combining federal and state incentives can amplify savings, but proper documentation and timely filing are essential.

Federal R&D Tax Credit Overview

The federal R&D tax credit, outlined in IRC Section 41, offers a direct reduction to your tax liability. This credit can generate savings of up to 13% of qualified research expenses, making it one of the most impactful incentives in the U.S. tax system. If the credit exceeds your tax liability for the year, you can carry it back one year or forward for up to 20 years.

What Qualifies as R&D?

To qualify, activities must meet all criteria defined by the IRS. These are evaluated through a four-part test, and every component must be satisfied:

| Test | Description |

|---|---|

| Permitted Purpose | The work must aim to create or improve a product, process, software, technique, formula, or invention. This improvement must focus on functionality, performance, reliability, or quality. |

| Technological in Nature | The research must rely on principles of science, such as physics, biology, engineering, or computer science. |

| Elimination of Uncertainty | Activities should address unknowns about whether something can be created, how to create it, or the best design approach. |

| Process of Experimentation | The work must involve systematic experimentation, like modeling, simulation, prototyping, or trial and error. |

Each business component – whether it’s a product, process, or software project – is evaluated separately under this test. However, certain activities are excluded, such as work conducted outside the U.S., adaptations for a single customer, or efforts that occur after commercial production begins.

Once qualifying activities are identified, the next step is determining which related expenses can be claimed.

Key Qualifying Expenses

If your activities pass the four-part test, the following expense categories may qualify for the credit:

- Wages: Taxable W-2 wages for employees directly involved in, supervising, or supporting qualifying research.

- Supplies: Tangible materials consumed or destroyed during R&D, such as raw materials, prototypes, or test components. However, capital equipment and land do not qualify.

- Contract Research: Payments to third-party vendors or consultants for research activities performed on your behalf are partially eligible.

- Cloud Computing: Costs for cloud computing services directly tied to R&D activities can qualify, but detailed tracking is critical under updated reporting rules.

The Section 280C election allows businesses to choose between two options: claim the full credit by reducing the R&D deduction or take a reduced credit (approximately 79% of the gross amount) while keeping the full deduction. The best choice depends on your specific situation—compare business formation services to ensure your entity structure supports these incentives—and model both options before filing.

"The businesses that capture the full value of R&D tax credits are those that treat them not as an annual compliance exercise, but as a strategic component of innovation funding." – Boast

Starting in tax year 2026, the IRS will require more detailed project-level reporting through Section G of Form 6765. This includes mapping employees, wages, and supplies to specific business components. If your tracking processes aren’t already project-focused, now is the time to implement them to ensure compliance with these new rules.

sbb-itb-ba0a4be

State-Level R&D Tax Credits

After looking at federal R&D tax credits, it’s worth diving into how state-level programs can add even more value. On top of the federal credit, about 38 states offer their own R&D tax credits, which can be combined with federal benefits. This means you can claim both for the same qualifying expenses.

State credits, however, only apply to R&D activities performed within that specific state. This includes factors like where your engineers operate, where wages are paid, and where testing takes place.

"State R&D credits can significantly increase your total benefit, especially when they’re claimed alongside the federal credit." – Monika Diehl, Arvo

Which States Offer R&D Tax Credits

State programs differ widely in terms of benefits, application processes, and eligibility rules. Some states offer refundable credits, meaning if your credit exceeds your tax liability, you could get a cash refund. Others allow credits to be sold, giving companies a way to generate immediate working capital. These features are particularly helpful for startups that are still in the early stages and not yet profitable.

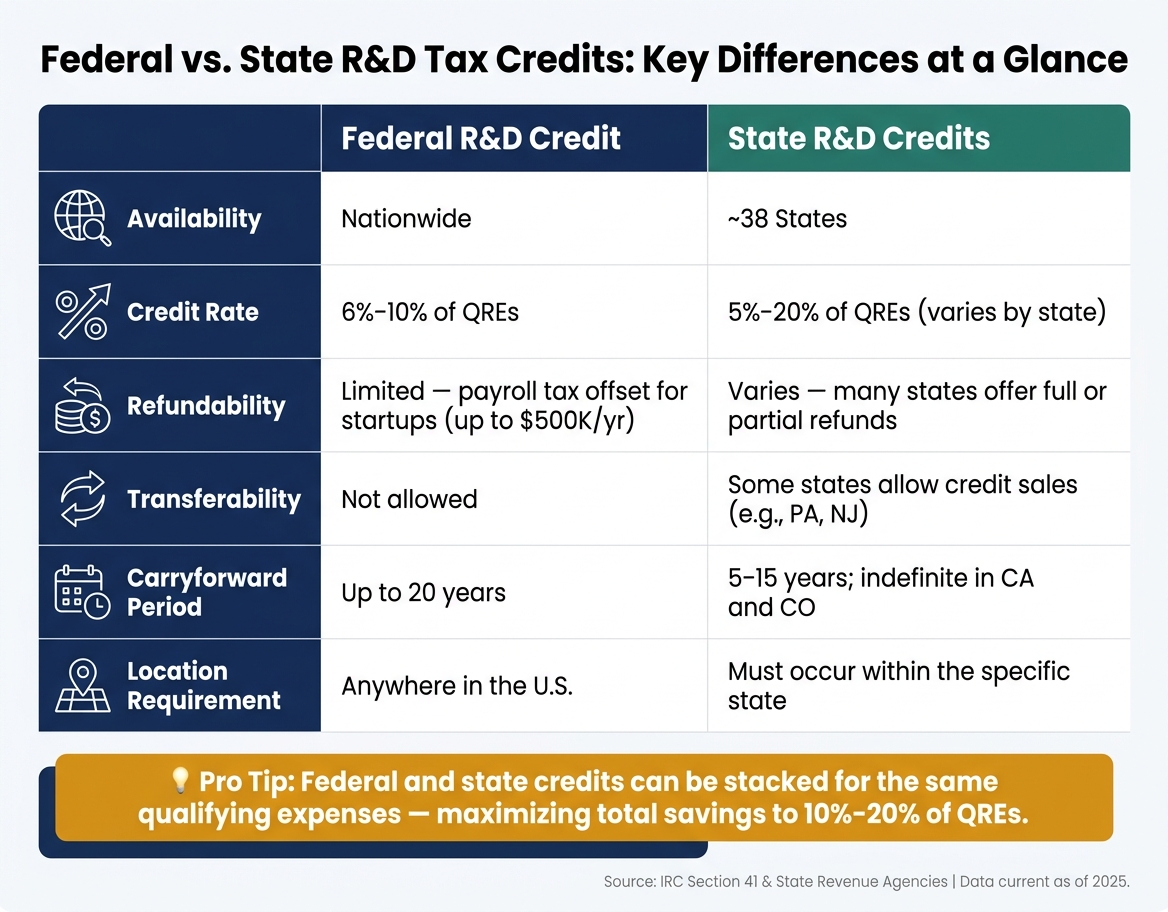

Here’s a quick comparison of how state credits stack up against the federal R&D credit:

| Feature | Federal R&D Credit | State R&D Credits |

|---|---|---|

| Availability | Nationwide | ~38 states |

| Credit Rate | 6%–10% of QREs | 5%–20% of QREs (varies by state) |

| Refundability | Limited to payroll tax offsets for startups | Varies; many states offer refunds |

| Transferability | Not allowed | Some states allow credit sales (e.g., PA, NJ) |

| Carryforward | 20 years | 5–15 years; indefinite in CA and CO |

| Location Requirement | Anywhere in the U.S. | Must occur within the specific state |

Some states also impose annual caps on credits. For instance, Florida limits total state R&D credits to $9 million per year, awarded on a first-come, first-served basis. New Hampshire caps its total credit pool at $7 million, with individual companies limited to $50,000. Iowa’s program, starting in 2026, will have a $40 million annual cap. In states with caps, filing early can make all the difference.

R&D Credit Rules by State

State R&D credits are far from one-size-fits-all. Variations in calculation methods, refundability, carryforward periods, and eligibility rules make it essential to understand each state’s specific approach. While some states align with the federal Alternative Simplified Credit (ASC) method, others – like California – use their own formulas. Additionally, certain states, such as Connecticut, Florida, and Kansas, restrict their credits to C-corporations, excluding pass-through entities.

Here’s a breakdown of some notable state programs:

| State | Credit Rate | Refundable? | Carryforward | Notes |

|---|---|---|---|---|

| Arizona | 24% (on the first $2.5M in QREs) | Partial (for small businesses) | 10–15 years | Requires pre-approval from the Commerce Authority |

| California | 15% (regular) / 3% (ASC) | No | Indefinite | Uses its own calculation method, not the federal ASC |

| Connecticut | Up to 6% | Yes (65%–90% for businesses with gross income ≤ $70M) | 15 years | Refundable for qualifying companies |

| Georgia | 10% | No | 5–10 years | Can offset payroll withholding taxes |

| Iowa | 3.5% (starting 2026) | Yes | None | Focused on advanced manufacturing and bioscience; CPA verification required |

| Minnesota | 10% (on the first $2M) | Yes (19.2% for 2025; 25% for 2026–2027) | 15 years | Refundability begins in 2025 |

| New York | 9%–20% (varies by program) | Yes | Indefinite (for QETCs) | Includes Life Sciences and NYC Biotech programs; capped at $500,000/year per company |

| Pennsylvania | 10% (20% for small businesses) | No | 15 years | Allows credit transfers, enabling startups to sell unused credits |

| Texas | 8.722% (starting 2026) | Yes (in certain cases) | 20 years | Rate increases to 10.903% for university research; program made permanent |

| Louisiana | 30% (for businesses with ≤50 employees) | Varies | Varies | Offers one of the highest rates for small businesses |

Refundability is becoming a growing trend among state programs. For example, Minnesota will introduce partial refundability in 2025, and Texas is revamping its program in 2026 to consolidate incentives into a single franchise tax credit with an increased rate. These changes highlight how states are competing to attract innovation-focused businesses.

Another key point: not all states align with federal rules. Following federal changes to Section 174, which now allows immediate expensing for R&D, states have adopted different approaches – rolling conformity, frozen conformity, or selective nonconformity. For instance, California and Arizona still require R&D costs to be amortized for state taxes, even though federal rules now allow full expensing. These differences can significantly impact how R&D expenses are treated at the state level.

"The federal government made Section 174 simple again; the states made it interesting." – Sanjay Keswani and Nick Thomsen, Plante Moran

Understanding these state-level differences is crucial for businesses aiming to maximize their R&D tax savings and strategically plan where to conduct their research activities.

How to Claim R&D Tax Credits

Claiming R&D tax credits involves navigating both federal and state requirements. The federal filing process is often the starting point, as it lays the groundwork for many state filings.

Federal Filing Process

To claim the federal R&D tax credit, you’ll need to file IRS Form 6765 along with your annual tax return (such as Form 1120 or 1065). If you are just starting out, ensure you have completed your EIN application before filing. This must be done by your regular filing deadline, including any extensions.

Here’s a breakdown of Form 6765’s key sections:

| Form 6765 Section | Purpose | Notes |

|---|---|---|

| Section A or B | Credit calculation | Choose between the Regular Research Credit (RRC) or the Alternative Simplified Credit (ASC) |

| Item A | Section 280C Election | Election must be made on an original, timely filed return and is irrevocable |

| Section D | Payroll tax offset | Only available for Qualified Small Businesses |

| Section G | Business component detail | Optional for tax year 2025; mandatory starting in tax year 2026 |

A critical decision is the Section 280C election. If you opt for the full gross credit, it reduces your R&D deduction, which increases taxable income. Alternatively, you can choose the reduced credit (around 79% of the gross credit) to avoid this adjustment. Keep in mind, this election must be made with your original return and cannot be changed later .

If you’re a startup planning to use the payroll tax offset, you’ll also need to file IRS Form 8974 with your quarterly employment tax return (Form 941). This form should be submitted immediately after filing your original return to claim the offset, which can be as much as $500,000 annually . The offset will apply in the first quarter following the election on your filed return.

Starting in tax year 2026, the IRS will require project-level reporting in Section G. This includes detailed narratives about technical uncertainties and a breakdown of Qualified Research Expenses. Use tax year 2025 to test your systems and ensure you’re ready to meet these new requirements.

"Determining eligibility, aligning Section 174 treatment, and defending claims require technical, tax, and documentation expertise, which should be handled by a qualified R&D tax credit carryforward provider." – KBKG

Once your federal filing is set, you can move on to address state-specific requirements to maximize your R&D tax credit benefits.

State Filing Requirements

Each state has its own processes, forms, and deadlines, so it’s important to stay organized. Missing a state-specific deadline could mean losing the credit for that year.

Some states require applications to be submitted directly to a state agency rather than attaching a form to your tax return. For instance:

- Florida has a one-week application window (March 20–26) through its Department of Revenue, with a $9 million statewide cap allocated on a first-come, first-served basis.

- Delaware requires Form 2070AC to be submitted by September 15.

- Maryland sets its deadline at November 15 and requires filing with the Department of Commerce.

Here’s a quick overview of requirements for some states:

| State | Key Form/Process | Deadline | Notes |

|---|---|---|---|

| Federal | Form 6765 | With annual return (incl. extensions) | 3-year window for amended returns |

| Delaware | Form 2070AC | September 15 | Strict statutory deadline |

| Florida | State application | March 20–26 | One-week window; $9M statewide cap |

| Hawaii | Form N-346A | March 30 | Requires initial certification from DBEDT |

| Maryland | State application | November 15 | Filed with Department of Commerce |

| Michigan | Tentative claim | March 15 | Required to reserve a share of the $100M statewide cap |

If you need more time to complete your R&D study, filing for a tax extension can help. This ensures you don’t lose out on the payroll tax offset election. Following both federal and state procedures carefully strengthens your overall strategy and helps you capture the maximum benefit.

You can also claim R&D tax credits retroactively for open tax years – typically up to three years – by filing an amended return. However, the IRS has tightened its review of amended R&D claims, so you’ll need thorough, contemporaneous documentation to support your filing . State statutes of limitations vary, so check your state’s rules before submitting late claims.

Documentation Requirements for R&D Tax Credits

Getting your documentation right is absolutely crucial when claiming federal and state R&D tax credits. The IRS relies on records as the primary proof for both qualified research activities (QRAs) and qualified research expenses (QREs). A staggering 60% of R&D credit claims under audit are flagged due to documentation gaps, with missing technical narratives being the most common issue. These gaps can completely derail an otherwise valid claim.

Here’s the golden rule: records must be contemporaneous – created as the research happens, not pieced together at the end of the year. As Greg O’Brien, CPA at Anomaly CPA, explains:

"A defensible credit relies on clear project narratives and contemporaneous records."

Required Documentation Checklist

To build a strong claim, you need evidence for two things: that the activities qualify and that the expenses are legitimate and tied to those activities. The table below outlines the key documents you should gather for each category.

| Documentation Category | Required Documents & Evidence |

|---|---|

| Wages & Labor | W-2 forms, payroll registers, timesheets, meeting minutes, oral testimony |

| Technical Activity | Project descriptions, technical narratives, design drawings, CAD files, test results |

| Software Development | Git commit histories, code iterations, Jira/Asana tickets, sprint retros, architecture diagrams |

| Contract Research | Signed service contracts (highlighting IP ownership and financial risk), 1099-NEC forms, invoices |

| Supplies & Materials | Purchase orders, receipts, invoices, bills of lading for materials consumed during testing |

| Cloud/Computer Costs | AWS, Azure, or GCP invoices, lease agreements, usage logs for development and staging environments |

| Experimentation Evidence | Prototypes, photos or videos of testing, lab notebooks, records of failed iterations |

A quick note on contractors: To include contractor expenses (typically at the 65% rate), you need to show that your business retained substantial rights to the intellectual property and bore the financial risk if the research didn’t succeed. Be sure to review contractor agreements carefully before filing.

Keeping these records organized and updated is just as important as collecting them in the first place.

Best Practices for Record Keeping

- Track engineer hours in real time. Use tools like Harvest, Toggl, or Jira to log hours as they happen. Instead of allocating 100% of an engineer’s time to R&D, break it down by project with specific percentages (e.g., "Engineer X: 70% on Project Y"). This level of detail is critical in an audit.

- Maintain a project register. Create a running list of active R&D projects, complete with short narratives. Each narrative should explain the technical uncertainty at the start of the project and the alternatives considered during experimentation. This directly supports the Four-Part Test, especially the Process of Experimentation – a common area where claims fail during audits.

- Keep records for 5–7 years. While the federal standard is three years, state requirements can vary, and certain situations, such as choosing between an S-Corp or C-Corp, may extend the timeline. Ensure every cost – whether wages, supplies, or contractor invoices – is directly linked to a specific business component in your records.

How Startups Should Evaluate State R&D Tax Credits

Once you’ve nailed down solid documentation, the next step is evaluating which state’s R&D tax credit offers the most immediate cash benefits. This is where your startup’s unique tax situation, team composition, and the physical location of your engineers come into play. Pairing this evaluation with earlier guidance on documentation and filing can help you maximize both federal and state benefits.

Key Factors to Consider

For early-stage startups, refundability can be a game-changer. States like Hawaii (which offers a 20% fully refundable credit), Iowa, and Nebraska provide cash refunds even when your tax liability is zero.

If you’re in a state without refundable credits, transferability becomes important. For example, New Jersey allows startups to sell unused R&D credits or net operating losses (NOLs) for at least 80% of their face value, with a lifetime cap of $15 million. Pennsylvania has a similar program but operates within a $55 million annual credit pool.

Jonathan Forman, Managing Director at GTM Tax, highlights the value of these credits:

"State R&D credits can drive location decisions, and they can provide cashflow. Whether it is transferring credits for cash, or selling credits, they can provide immediate value even for start-ups."

Another option for startups with growing payroll but limited taxable income is payroll tax offsets. States like Georgia and Massachusetts allow R&D credits to be applied against payroll withholding taxes instead of income taxes, providing a vital benefit for companies in their early stages.

With these considerations in mind, it’s essential to analyze how your startup’s location and entity structure influence your ability to leverage R&D tax credits effectively.

Choosing a State and Entity Structure

Your startup’s location and entity structure aren’t just logistical details – they’re major factors in determining your access to state R&D incentives. A comparison by GTM Tax of two similar software startups illustrates this point. One company, based in Greenwich, CT, employed 10 developers earning $1.2 million in wages and spent $120,000 on cloud hosting. This Connecticut startup secured $121,000 in R&D incentives in its first year. Meanwhile, a comparable startup just 10 minutes away in Port Chester, NY, generated $0 in credits because New York’s primary R&D incentives are incremental and tied to specific job metrics that the company hadn’t yet met.

Entity structure also plays a critical role. Some states, like Florida, Connecticut, and Kansas, limit R&D credits to C-corporations, excluding pass-through entities like LLCs and S-corporations from eligibility. Connecticut recently expanded its eligibility in June 2025 to include certain single-member LLCs with over 3,000 in-state employees, but this threshold is far beyond the reach of most startups. If your startup operates as an LLC or S-corp, you’ll need to confirm eligibility and ensure your R&D expenses are clearly documented and allocated. For those still deciding on an entity structure, this is a key factor to weigh, as it can have long-term tax implications. Platforms like BusinessAnywhere can help simplify the process by offering registration and compliance support.

Lastly, don’t overlook application deadlines. Missing state-specific deadlines can disqualify you from receiving credits, no matter how well-documented your expenses are. Staying ahead of these deadlines is critical to securing the benefits your startup deserves.

Conclusion

R&D tax credits offer startups a chance to significantly reduce costs, yet many fail to take advantage of them. Federal credits alone can save businesses between 6%–10% of qualified research expenses, and when combined with state programs, the total savings can climb to 10%–20%. Despite this, a surprising number of startups miss out on these opportunities. In 2021, U.S. businesses claimed over $32 billion in R&D credits, highlighting the scale of potential savings.

Currently, 38 states provide R&D tax credits alongside federal incentives, with some states rolling out major legislative updates in recent years. For example, in 2025, states like Connecticut, Iowa, and Texas introduced significant changes to their credit programs. To maximize these benefits, startups need to stay informed about new regulations, carefully track eligible expenses, and ensure timely filing. However, navigating these requirements can be overwhelming for early-stage companies with limited resources.

That’s where platforms like BusinessAnywhere can step in. From managing entity registration to handling bookkeeping, BusinessAnywhere helps streamline your operations, keeping everything organized and compliant. This makes it easier for startups to claim the credits they’re entitled to without unnecessary stress.

The savings from R&D credits can be a game-changer. Whether reinvested in hiring, product development, or the next big idea, these credits can transform your tax strategy into a powerful growth engine for your company.

FAQs

Can I claim both federal and state R&D credits on the same expenses?

Yes, you can claim both federal and state R&D tax credits for the same qualifying research expenses. These programs operate independently – federal credits are managed by the IRS, while state credits are regulated by individual states. This isn’t considered double-dipping because they are separate incentives.

Federal credits apply across the U.S., but state credits usually require the research to take place within that specific state. To make the most of these savings, it’s essential to allocate expenses based on location and ensure you meet both the IRS Four-Part Test for federal credits and any additional requirements set by the state.

How do I track R&D work now to be ready for Form 6765 Section G in 2026?

To get ready for Form 6765 Section G, begin organizing qualified research expenses (QREs) by project and business component. Keep thorough documentation of your research activities, including the technical challenges tackled and associated costs, such as employee wages, supplies, and contract research. Make sure your financial records clearly connect these costs to specific components. Starting this process now is key to meeting the detailed disclosure requirements for tax years beginning January 1, 2026.

Which states give startups cash back or let them sell unused R&D credits?

Several states in the U.S. provide ways for startups to turn unused R&D tax credits into cash through refundable credits or transfer programs. States like Arizona, Connecticut, Hawaii, Louisiana, Minnesota, New York, and Texas offer refundable credits, which can provide direct financial benefits. Meanwhile, programs in New Jersey, Pennsylvania, and North Dakota allow businesses to sell unused credits to other taxpayers, offering an alternative source of non-dilutive funding to support early-stage growth.