Should your business accept cryptocurrency? Here’s the short answer: It depends on your goals, customer base, and readiness to manage the risks. Crypto payments can help you attract tech-savvy customers, cut transaction fees (1% vs. 2.9% for credit cards), and process payments faster – especially for global transactions. But challenges like price volatility, complex tax rules, and regulatory hurdles need careful planning.

Key Points:

- Benefits: Lower fees, faster settlements, access to 560M crypto users globally.

- Risks: Price swings, strict tax reporting, irreversible transactions.

- Getting Started: Choose a payment processor, train your team, and ensure compliance with IRS and AML rules.

Crypto can boost sales (72% of businesses accepting it report growth), but it’s not without challenges. Let’s dive into the details to see if it’s right for your business.

Benefits of Accepting Cryptocurrency

Cryptocurrency payments offer businesses global reach, reduced costs, and faster transaction processing. These advantages are especially appealing for companies catering to international markets or operating with tight profit margins.

Reach International Customers Without Currency Barriers

Cryptocurrency acts as a universal payment system, bypassing traditional banking hurdles. For instance, if a customer in Brazil wants to pay a U.S.-based business, there’s no need to deal with intermediary banks, SWIFT systems, or currency conversion fees. Instead, the transaction is processed directly on the blockchain, with exchange rates locked for a 10–15 minute checkout window.

This system offers access to a massive potential customer base: 560 million cryptocurrency holders and 1.4 billion unbanked individuals who have internet access and smartphones but lack traditional banking services. Stablecoins like USDC or USDT provide a solution for customers in regions with volatile currencies or limited access to U.S. dollars, allowing them to pay in a globally recognized value.

Next, let’s see how these benefits translate into cost savings for businesses.

Reduce Transaction Costs

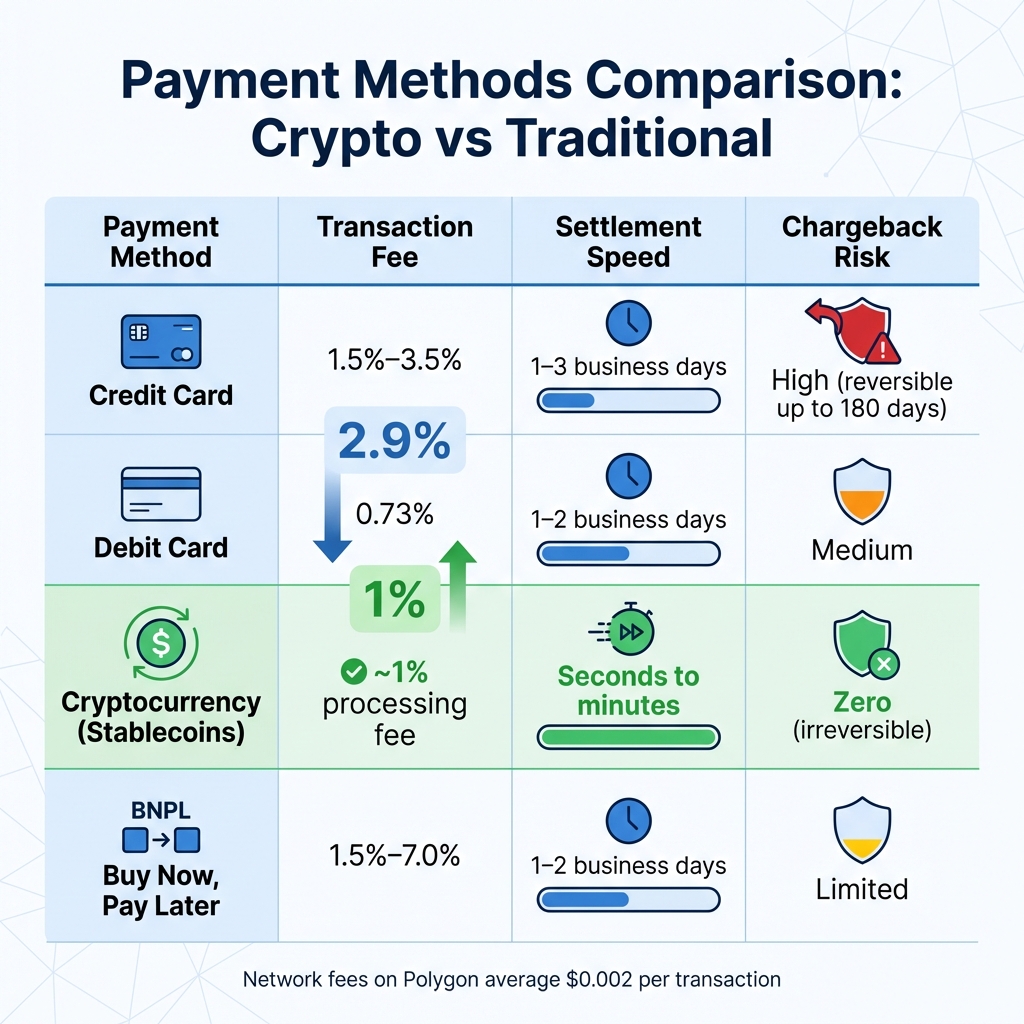

Cryptocurrency payments can significantly lower transaction fees. While credit card processors typically charge around 2.9% plus $0.30 per transaction, crypto processing fees average about 1%. These savings come from cutting out intermediaries like banks and card networks.

| Payment Method | Transaction Fee | Settlement Speed | Chargeback Risk |

|---|---|---|---|

| Credit Card | 1.5%–3.5% | 1–3 business days | High (reversible up to 180 days) |

| Debit Card | 0.73% | 1–2 business days | Medium |

| Cryptocurrency (Stablecoins) | ~1% processing fee | Seconds to minutes | Zero (irreversible) |

| Buy Now, Pay Later | 1.5%–7.0% | 1–2 business days | Limited |

On high-throughput blockchains like Polygon, network fees average just $0.002 per transaction, making crypto ideal for high-volume businesses. As Nikolai Kariuk from B2BInPay explains:

Switching to digital currencies isn’t just tech innovation; it is an immediate 2% raise on your bottom line.

Additionally, because blockchain transactions are irreversible once confirmed, businesses eliminate the risks and costs tied to chargebacks.

Beyond cost savings, cryptocurrency also speeds up cross-border payments significantly.

Speed Up Cross-Border Payments

Traditional wire transfers can take 1–5 business days and often involve hefty fees. In contrast, cryptocurrency transactions settle in seconds and come with minimal network fees. Blockchains like Polygon and Solana process transactions almost instantly, eliminating the delays associated with traditional banking systems.

This speed has a direct impact on cash flow management. Faster settlements mean businesses can reduce the capital tied up in transit and rely less on short-term credit to cover operating expenses. As Polygon Labs highlights:

Faster settlement can improve cash flow, reduce reliance on short-term credit, and speed up payouts to suppliers or marketplace sellers.

For companies managing international supply chains or operating marketplace platforms, this efficiency can lead to smoother and more reliable operations.

Drawbacks of Accepting Cryptocurrency

While cryptocurrency payments come with certain perks, they also bring challenges that can impact your finances and day-to-day operations. Being aware of these risks can help you decide if crypto fits your business model.

Price Fluctuations and Value Loss

The value of cryptocurrencies can swing wildly in a short amount of time. For instance, a $1,500 payment in Bitcoin might drop to $1,300 overnight. This unpredictability makes it tricky to maintain steady revenue or plan finances effectively.

Stablecoins like USDC and USDT aim to maintain a 1:1 value with the U.S. dollar, offering more stability. However, they’re not entirely risk-free. In moments of market stress or when doubts arise about their reserves, stablecoins can experience “de-pegging,” where their value temporarily falls below $1.00.

| Feature | Volatile Crypto (BTC/ETH) | Stablecoins (USDC/USDT) | US Dollar (USD) |

|---|---|---|---|

| Price Stability | Low; value can change dramatically overnight | High; pegged to real-world assets like USD | Absolute; standard for business accounting |

| Risk of Value Loss | High; $1,500 payment could be worth $1,300 the next day | Low; though "de-pegging" is a rare risk | None (excluding inflation) |

| Primary Use Case | Investment or brand signaling | Everyday commerce and cross-border payments | Standard operations |

Some payment processors try to address this issue by offering rate-locking for 10–15 minutes during checkout and converting crypto payments to fiat instantly. While these tools reduce exposure to volatility, they don’t eliminate it entirely. Businesses must still prepare for potential value losses within processing windows.

On top of market instability, regulatory challenges also add complexity to accepting cryptocurrency.

Regulatory Requirements and Compliance Issues

The IRS treats cryptocurrency as property rather than legal tender. This means every crypto transaction is taxable, requiring you to calculate and report any capital gains or losses. For example, when you sell crypto for cash, swap one coin for another, or use crypto to pay for goods or services, you must determine its fair market value in USD at the time of the transaction.

If your business only accepts crypto as payment for goods or services, you’re likely not considered a "money transmitter" under FinCEN regulations. However, if you exchange crypto for cash or hold customer funds, you may need to register with FinCEN and comply with Anti-Money Laundering (AML) and Know Your Customer (KYC) rules. Additionally, any crypto payment over $10,000 requires filing Form 8300 with the IRS.

State-level regulations further complicate things. For example, New York mandates a "BitLicense" for many crypto-related activities, whereas Wyoming offers more lenient rules, exempting most crypto transactions from money transmitter laws. Standard sales taxes still apply to crypto transactions, and if you pay employees in crypto, taxes must be withheld based on the USD value at the time of payment.

While compliance can address legal risks, crypto also introduces security challenges.

Security Threats and Fraud Prevention

Digital wallets are vulnerable to theft, especially if private keys are stored online or in insecure locations. Unlike traditional bank accounts, cryptocurrency holdings aren’t protected by the Federal Deposit Insurance Corporation (FDIC). This means that if your funds are stolen or lost, there’s no government safety net to recover them.

Cryptocurrency transactions are irreversible, which reduces chargeback fraud but introduces other risks. Once a payment is confirmed, it cannot be undone by a bank or payment processor. This makes it essential to verify customer wallet addresses carefully before issuing refunds. If you send funds to the wrong wallet, recovery is impossible. Combined with the volatility issues mentioned earlier, these risks can amplify potential financial losses.

To safeguard your business, use trusted payment processors that handle sanctions screening, AML checks, and monitor for suspicious activity. Enable multi-factor authentication (MFA) for all accounts and wallets, and store large balances in “cold wallets” – offline hardware devices that protect private keys from hackers. It’s worth noting that standard business insurance policies typically don’t cover cryptocurrency theft or fraud, so you may need specialized crypto insurance.

Steps to Start Accepting Cryptocurrency

If you’ve decided to accept cryptocurrency payments for your business, careful planning will ensure a smooth and secure implementation. Here’s how to get started.

Assess Your Business Needs

Before diving in, evaluate whether cryptocurrency aligns with your customer base and operations. Crypto payments are particularly useful for businesses catering to tech-savvy customers, global markets, or underbanked regions. They’re also a good fit for e-commerce platforms, companies with frequent international transactions, or businesses handling large transaction amounts.

Next, assess your team’s readiness. Does your staff have the knowledge to manage digital wallets, secure private keys, and troubleshoot blockchain-related issues? You’ll also need to decide whether to hold cryptocurrency as an asset or convert it to dollars immediately using a payment processor to avoid market volatility. Don’t forget to confirm compliance with local regulations and ensure you meet anti-money laundering (AML) and know-your-customer (KYC) requirements.

Consider running a pilot program to test customer interest and identify any challenges. The growing adoption of cryptocurrency is worth noting: as of September 2025, approximately 18,000 businesses globally accepted Bitcoin, and an estimated 560 million people held cryptocurrency. Once your business needs are clear, the next step is choosing a payment processor.

Select a Payment Processor

Your choice of payment processor will determine how easily cryptocurrency integrates into your operations. Decide between non-custodial processors, which require more technical expertise but offer direct wallet transfers, and custodial processors, which simplify fiat conversion but may involve additional risks.

For straightforward e-commerce setups, platforms like Coinbase Commerce or BitPay are solid options. Larger enterprises or those handling high-value B2B transactions may require more advanced solutions. Look for processors that offer instant fiat conversion to reduce exposure to crypto’s price fluctuations. Compliance is critical, so ensure the processor holds valid licenses, such as U.S. Money Transmission Licenses or the New York BitLicense.

Transaction fees for crypto payments typically range from 0.5% to 2%, lower than the 1.5% to 3.5% charged by traditional credit card processors. Opt for a processor that locks exchange rates for 10–15 minutes during checkout to protect against price swings. Also, verify the processor’s financial stability and ability to settle funds promptly.

“When you’re working with a company whose primary function is crypto payments, you’re going to get their full attention. Whereas you may not if it were just a side business.” – Stephen Pair, CEO, BitPay

Once you’ve chosen a processor, it’s time to integrate cryptocurrency into your payment options.

Add Cryptocurrency to Your Payment Options

The integration process depends on whether your business operates online or in-person. For online stores, use e-commerce plugins like Shopify or WooCommerce, or integrate directly via API for custom websites. Shopify merchants, for instance, can now integrate stablecoin payments (such as USDC) directly into their checkout flows with minimal technical effort.

For in-person transactions, set up QR codes at your point of sale (POS) so customers can easily scan and pay using their digital wallets. To streamline accounting and reduce exposure to market swings, configure your payment processor to automatically convert received crypto into dollars.

Before launching, thoroughly test the user experience. Ensure the payment processor supports wallet connectivity and can resolve issues like payments sent to the wrong blockchain to minimize errors and lost transactions.

Prepare Your Team and Customers

Once your technical setup is in place, train your staff to handle crypto transactions confidently. Employees should understand the basics of how crypto payments work and be prepared to assist customers. Train support teams on blockchain confirmation times, which can vary from seconds to several minutes depending on network congestion.

Establish clear refund policies, as blockchain transactions are irreversible. Decide whether refunds will be issued in cryptocurrency or dollars, and set up a process to verify customer wallet addresses. Update your website FAQs to include information about crypto payments and add “Crypto Accepted Here” signage to let customers know about the new option. Highlight benefits like faster international transactions, lower fees, and increased privacy.

“In 2015, accepting crypto on an online store sounded experimental. In 2026, it’s a treasury decision.” – Diana Zander, CPAY

Set Up Tax Tracking and Compliance Systems

The IRS treats cryptocurrency as property, so every transaction must be reported for capital gains purposes. Use tools that automatically capture the USD value of each transaction at the time of payment. Software like CoinTracker can sync with your crypto wallets and accounting tools like QuickBooks to simplify tax reporting. These tools typically cost between $100 and $1,000+ annually.

Ensure your payment processor supports AML and KYC requirements. Additionally, if you receive more than $10,000 in crypto payments, you’ll need to file Form 8300 with the IRS. Work with an accountant or tax advisor to set up systems for tracking capital gains and losses, ensuring compliance from the start.

For businesses just starting out, having robust tax and compliance systems in place is crucial. Services like Business Anywhere can assist with EIN applications and compliance support, helping you navigate these requirements as your business grows.

sbb-itb-ba0a4be

Tax and Regulatory Requirements for US Businesses

Accepting cryptocurrency comes with its own set of tax and compliance responsibilities. Understanding these upfront can help you avoid penalties and make accounting smoother. Below, we’ll break down how the IRS handles cryptocurrency, state tax considerations, and anti-money laundering (AML) requirements.

How the IRS Treats Cryptocurrency

For tax purposes, the IRS treats cryptocurrency as property. This means the fair market value (FMV) of the cryptocurrency when you receive it counts as ordinary income and is subject to federal income tax and, if applicable, self-employment tax.

"Virtual currency is treated as property for U.S. federal tax purposes; general rules for property transactions apply."

– Internal Revenue Service

Using cryptocurrency to pay for expenses or converting it into cash creates a second taxable event. This triggers a capital gain or loss, depending on how the FMV has changed since you acquired it. Gains are taxed differently based on how long you’ve held the cryptocurrency: short-term gains are taxed at ordinary income rates (10%–37%), while long-term gains qualify for lower rates of 0%, 15%, or 20%.

To stay compliant, keep detailed records of every transaction. Include the date, amount, FMV in USD at the time of receipt and disposal, and any associated fees. Using the same cryptocurrency exchange to determine FMV can reduce your audit risk. Additionally, if your capital losses exceed your gains, you can offset up to $3,000 of those losses against your ordinary income, with any remaining losses carried forward to future tax years.

| IRS Form | Purpose for Crypto Businesses | Filing Deadline |

|---|---|---|

| Form 8949 | Report details of each crypto sale, exchange, or disposition | April 15 (with tax return) |

| Schedule D | Summarize total short- and long-term capital gains/losses | April 15 (with tax return) |

| Schedule C | Report cryptocurrency received as business income (sole proprietors) | April 15 (with tax return) |

| Form W-2 | Report wages paid to employees in cryptocurrency | January 31 |

| Form 1099-NEC/MISC | Report payments of $600+ to contractors or for miscellaneous income | January 31 |

| Form 1099-K | Issued by third-party processors for business transactions exceeding $600 | January 31 |

State Sales Tax on Cryptocurrency Transactions

States generally treat cryptocurrency as they would cash. Sales tax is calculated based on the FMV of the cryptocurrency at the time of the transaction and must be included in your gross income.

"If someone pays you cryptocurrency in exchange for goods or services, the payment counts as taxable income, just as if they’d paid you via cash, check, credit card, or digital wallet."

– TurboTax

Since sales tax rules vary by state, it’s wise to consult a local CPA. Additionally, using crypto tax software that integrates with your point-of-sale system can help automate FMV calculations for each transaction, saving you time and reducing errors.

Anti-Money Laundering and Customer Verification Rules

Businesses accepting cryptocurrency must comply with Know Your Customer (KYC) and AML regulations, which vary depending on your jurisdiction and the volume of transactions. These rules require you to verify customer identities and monitor transactions for signs of money laundering or fraud.

It’s critical to ensure your payment processor has strong sanctions screening in place to block transactions with prohibited individuals or entities. In some regions, you may also need to report large or suspicious transactions. Choosing a payment processor that adheres to KYC and AML standards not only helps meet legal requirements but also reduces the administrative workload and potential risks.

Conclusion

Accepting cryptocurrency as a payment method offers several advantages. These include lower transaction fees, typically around 1% compared to the 1.5%–3.5% charged by traditional payment processors, 24/7 near-instant settlements, and the ability to tap into a growing market of approximately 560 million global crypto users. Additionally, crypto eliminates the risk of chargebacks, providing extra security for businesses .

That said, there are risks to consider. The price volatility of cryptocurrencies can pose challenges, tax obligations are more complex (since the IRS treats crypto as property), and businesses must navigate ever-changing regulations, including strict KYC (Know Your Customer) and AML (Anti-Money Laundering) requirements .

If you’re thinking about accepting digital currencies, take time to evaluate whether your customer base and internal team are prepared for the added responsibilities, like managing accounting and ensuring robust security. If you decide to move forward, consider using a payment processor that converts crypto to USD instantly to minimize exposure to price fluctuations. For businesses holding larger amounts of cryptocurrency, multi-signature wallets add an extra layer of protection, while tax-tracking software can simplify compliance.

Security and compliance are non-negotiable. Blockchain transactions are irreversible, meaning a lost private key or a compromised wallet results in permanent loss of funds. Staying compliant with federal and state reporting requirements is equally critical to avoid penalties.

Given the complexities involved, seeking expert guidance might be the best move. Business Anywhere can assist by helping you establish your company in crypto-friendly jurisdictions, ensuring compliance with state and federal regulations, and setting up the administrative systems you need for secure and efficient digital asset management. Whether you’re starting a new business or adapting an existing one, having a strong compliance framework makes accepting cryptocurrency much easier.

The tools to accept crypto payments are already in place and well-tested. The decision ultimately hinges on whether the benefits align with your business goals and if you’re ready to implement the systems required for safe and compliant adoption.

FAQs

Which cryptocurrencies should my business accept first?

Start by focusing on well-known cryptocurrencies such as Bitcoin (BTC). Its high liquidity and broad adoption make it a reliable choice. Another strong option is Litecoin (LTC), which stands out for its low transaction fees and frequent use in cryptocurrency payments. If you’re looking to reduce exposure to price swings, consider stablecoins like USDC, which are designed to maintain a stable value. Starting with these choices offers a practical mix of dependability and ease for integrating cryptocurrency payments.

How do I avoid losing money to crypto price swings?

To reduce losses caused by cryptocurrency price swings, it’s smart to convert crypto payments to fiat currency as soon as you receive them. Rely on secure payment processors that offer features like instant conversion or price stabilization to simplify this process. Holding onto cryptocurrencies for long periods can expose you to more market volatility, so it’s best to avoid that. These strategies help secure the value of your payments and minimize the risks tied to unpredictable crypto price changes.

What records do I need to keep for IRS crypto taxes?

The IRS mandates keeping thorough records of all digital asset transactions for tax reporting. This applies to activities like sales, trades, exchanges, transfers, payments for goods or services, and mining or staking. Important details to document include: transaction dates, types and amounts of assets involved, fair market value at the time of each transaction, and the purpose of the transaction. These records are essential for accurately reporting income and determining capital gains or losses.