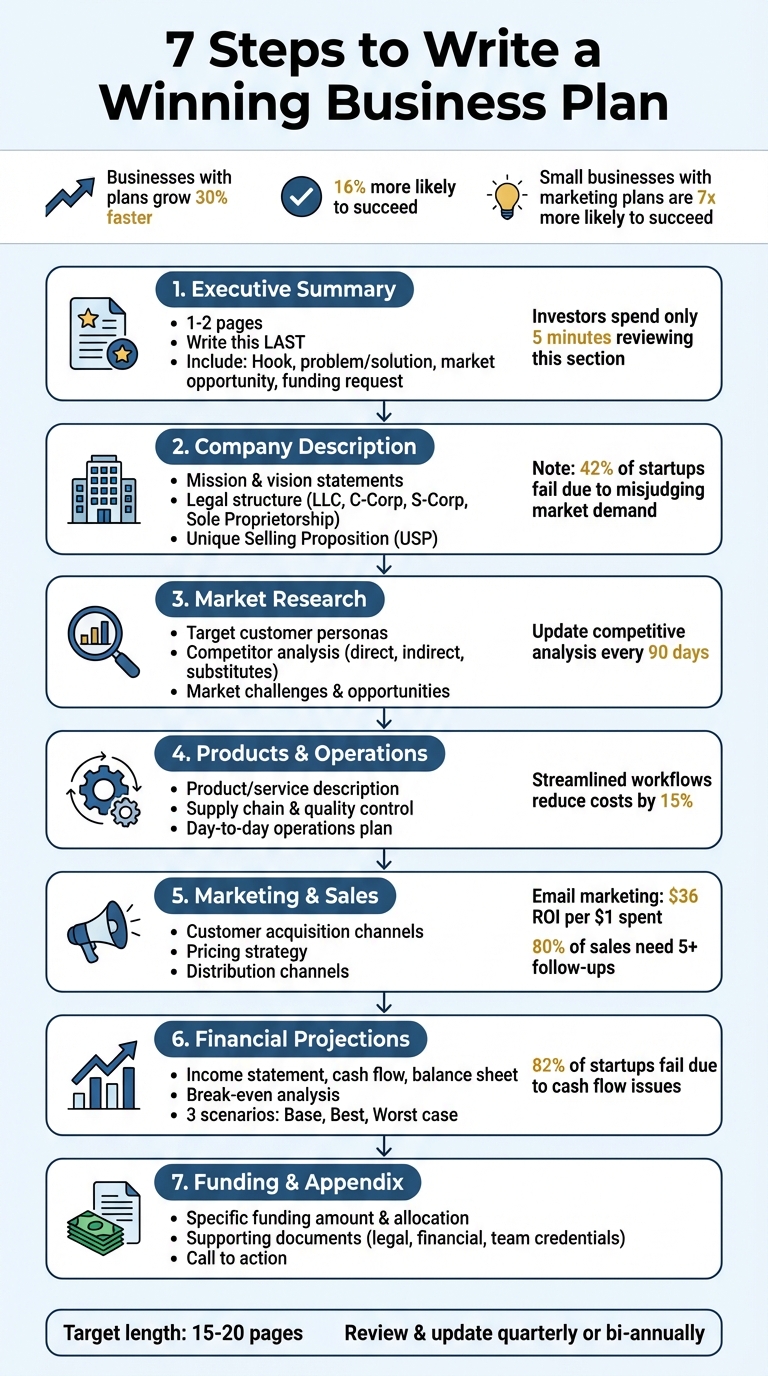

Creating a business plan is essential for any new founder. It provides clear direction, helps avoid costly mistakes, and increases your chances of success. Businesses with plans grow 30% faster and are 16% more likely to succeed. A strong business plan also attracts investors by showcasing your strategy, market understanding, and financial projections. Here’s what you need to include:

- Executive Summary: A concise overview of your business, market opportunity, and financial goals.

- Company Description: Your mission, vision, and legal structure and formation.

- Market Research: Detailed insights into your target audience, competitors, and industry trends.

- Products & Services: What you’re offering and how it solves customer problems.

- Operations Plan: Day-to-day processes to deliver your product or service efficiently.

- Marketing & Sales: Strategies to attract, convert, and retain customers.

- Financial Projections: Income statement, cash flow, and balance sheet to show profitability and funding needs.

- Funding Request: How much money you need and how it will be used.

- Appendix: Supporting documents like licenses, contracts, and team resumes.

A business plan isn’t just for investors – it’s your roadmap for building and growing your company. Regularly update it to reflect new data and market changes.

Step 1: Write Your Executive Summary

The executive summary is the cornerstone of your business plan – it’s often the first section investors read, and sometimes the only one. This 1- to 2-page summary should distill your strategy into its most compelling elements.

"The executive summary is like an elevator pitch. You’re selling someone on reading your full plan while quickly summarizing the key points." – Tim Berry, Business Planning Expert

Investors typically spend just five minutes reviewing this section, so every word must earn its place. Replace vague statements with specific data. For example, instead of saying "significant revenue", state "$4.7M in revenue" to make a stronger impression.

What to Include in Your Executive Summary

Investors expect your executive summary to cover these eight key areas:

- Hook: Start with a compelling statistic, customer story, or industry challenge. For instance, "Managers waste over 6 hours weekly in unproductive meetings, costing businesses more than $100,000 annually in lost productivity".

- Company Description: Provide a concise, jargon-free explanation of what your company does and why it exists.

- Problem and Solution: Clearly define the market problem using data, then explain how your product or service offers a unique solution.

- Market Opportunity: Highlight the Total Addressable Market (TAM) and your specific target audience, using precise numbers.

- Competitive Advantage: Emphasize what sets your business apart – such as proprietary technology, exclusive partnerships, or team expertise.

- Business Model: Describe your revenue streams and pricing structure in straightforward terms.

- Management Team: Showcase the experience and achievements of your leadership team; investors often prioritize strong teams over great ideas.

- Financial Highlights and Funding Request: Share your current revenue, growth rates, and 3–5-year projections. Clearly state how much funding you need and how you plan to use it.

Keep your paragraphs concise (2–3 sentences each), and use headers or bullet points to make the summary easy to scan. Avoid tentative language like "Sales could reach" and instead use confident statements like "Sales will reach" to build trust.

When to Write This Section

Save the executive summary for last. Once you’ve completed the rest of your business plan, you’ll be better equipped to create a summary that accurately reflects your strategy. As Entrepreneur aptly puts it:

"It’s impossible to summarize a book until the book is written." – Entrepreneur

Once your executive summary is polished, you’ll be ready to move on to Step 2: detailing your company overview.

sbb-itb-ba0a4be

Step 2: Describe Your Company and Business Overview

After the executive summary, the company overview sets the stage by clearly outlining your mission, legal structure, and what makes your business stand out. Think of it as the foundation of your business plan. This section explains what your business does, who it serves, and why it matters – all in straightforward terms. It serves as the bridge between your high-level summary and the detailed strategies that follow.

Start with a short and impactful mission statement, such as: "We help [customers] achieve [outcome] through [method]." This should cover what you offer, who you serve, how you deliver it, and why your business exists.

Follow that with your vision statement, which outlines where you see your company in the next five to ten years. For example: "To become the leading platform for remote teams managing compliance across 50 states." A clear vision not only keeps your team aligned but also boosts employee engagement. Research shows that employees who find their organization’s vision meaningful are 52% more engaged than those who don’t.

Choose Your Business Structure

The legal structure of your business shapes everything from taxes to personal liability. Here’s a quick breakdown of the most common options:

- LLCs: These are popular, making up 85% of new U.S. business formations. They protect personal assets from business debts while offering tax flexibility. By default, profits are taxed as personal income, but you can opt for S-Corp taxation if your annual profits exceed $75,000.

- C Corporations: Often chosen by startups looking for venture capital, C-Corps attract 95% of venture capitalists and 94% of angel investors. However, they face double taxation – once at the corporate level and again on dividends.

- Sole Proprietorships: The simplest structure, ideal for low-risk side projects. However, they don’t offer personal liability protection, so they’re not suitable for higher-risk ventures.

Filing fees vary by state, so it’s important to decide where to base your business. Remote founders often establish their headquarters either where the CEO is located or where the majority of founders are based. As Alex Kehayias, founder of Mosey, advises:

"As a general rule for remote businesses, headquarters (HQ) is either 1) wherever the highest concentration of founders is or 2) where the CEO is located."

Even if you incorporate in Delaware – a favorite for 68% of Fortune 500 companies – you may still need to register as a foreign entity in the state where you operate. Don’t forget to open a business bank account for your LLC to maintain a clear legal separation between personal and business finances. Failing to do so could jeopardize your liability protection.

| Structure | Personal Asset Protection | Tax Treatment | Best For |

|---|---|---|---|

| Sole Proprietorship | None | Pass-through (Schedule C) | Low-risk side hustles |

| LLC | Strong | Flexible (Default: Pass-through) | Most small businesses |

| S-Corp | Strong | Pass-through (No tax on distributions) | High earners ($75k+ profit) |

| C-Corp | Strong | Double Taxation (Corporate + Personal) | VC-backed startups |

Once your legal structure is set, focus on defining what makes your business stand out.

Explain What Makes Your Business Different

Your Unique Selling Proposition (USP) is the reason customers will choose you over competitors. Avoid vague claims – be specific and measurable. For instance, instead of saying, "Our software improves efficiency," try: "Our software reduces customer churn by 18% by identifying behavioral drop-off points".

One approach to defining your USP is identifying "three uniques" – three strengths that, when combined, make your offering hard to replicate. For instance, you might highlight same-day delivery, a lifetime warranty, and 24/7 customer support. As Logan Shinholser from Contractor Growth Network explains:

"If your messaging feels generic, your product will, too."

To uncover your USP, analyze competitors and focus on the specific problems your target audience faces. Then, determine how you solve these issues better or differently. Surveying your current customers can also reveal hidden strengths you might not have recognized. This step is crucial – 42% of startups fail because they misjudge market demand or misunderstand their audience.

With your USP clarified, you’ll have a strong foundation to move forward.

How Remote Services Simplify Business Operations

Running a remote business comes with its own set of challenges, such as maintaining a consistent address, receiving legal documents, and staying compliant across multiple states. Here are some solutions that can make things easier:

- Virtual mailbox services: These provide a professional U.S. address where you can receive, scan, and forward mail. This eliminates the hassle of updating your address with multiple agencies.

- Registered agent services: Legally required in all 50 states, a registered agent handles official documents on your behalf. Outsourcing this service (typically $100–$300 per year) ensures you stay compliant, even if you’re traveling or working across time zones. For example, BusinessAnywhere offers registered agent services starting at $147 per year, with the first year free when bundled with business registration.

A real-world example of proactive planning comes from Alex Kehayias, who changed his company’s legal name from Mosey, Inc. to Mosey Works, Inc. to avoid a name conflict in California. This decision saved thousands of dollars in legal fees and days of administrative work. It’s a reminder that careful planning around naming and address management can save you significant time and money.

With a clear company overview in place, you’re ready to move on to market analysis in the next section.

Step 3: Research and Analyze Your Market

Market research isn’t just a box to check – it’s the backbone of a solid business plan. It shows investors and partners that you’ve done your homework. Who will buy from you? Who are your competitors? What challenges lie ahead? The answers to these questions shape everything from pricing to marketing to hiring decisions.

To gather insights, use both primary research (like customer interviews and surveys) and secondary research (like industry reports and competitor data). Primary research gives you firsthand information but can take time and resources, while secondary research is quicker and often more affordable. For example, the global market research industry was valued at $142 billion in 2023, and 96% of marketers agree that understanding customers deeply is crucial for growth. Don’t overlook your own data either – CRM records, sales notes, and support tickets can be goldmines of information.

Identify Your Target Customers

Creating detailed customer profiles – or personas – is key to understanding your audience. These profiles should include demographics, buying habits, pain points, and what motivates their decisions. You can segment them by factors like location, spending habits, or sensitivity to price. For instance, if you’re starting a residential cleaning service in Austin, TX, you might focus on dual-income households, which make up 65% of the market and are projected to grow by 6% annually due to busy professionals.

Dive deeper with "why" interviews – 30 to 45-minute one-on-one conversations that uncover emotional drivers surveys might miss. Negative reviews on platforms like G2, Capterra, or Amazon can also reveal unmet needs. A great example is Cleeng, a subscription platform that analyzed session replays and product analytics after a 92% drop in feature usage following a UI redesign. By addressing user friction, they boosted page visits by 75% in just days. As Jenny Romanchuk from HubSpot puts it:

"The real advantage comes from looking beyond the obvious – diving deeper than your competition is willing to go."

Make these personas relatable by giving them names, photos, and backstories. Update them quarterly to keep pace with changes in technology, the economy, or consumer behavior.

Study Your Competitors and Market Trends

Understanding your competition is just as important as knowing your customers. Start by identifying three types of competitors:

- Direct competitors: Businesses offering similar products to the same audience.

- Indirect competitors: Companies solving the same problem but in a different way.

- Substitutes: Alternatives that meet the same customer needs.

Never claim you have no competition – if there’s demand, there’s competition. Investors know this. In fact, one major venture capital firm reviews thousands of business plans yearly but invests in only about six, often penalizing founders who fail to grasp their market.

To stay informed, create a comparison matrix. Map your business against three to five key competitors based on factors like pricing, features, distribution channels, and customer service. Tools like G2, Trustpilot, LinkedIn, Crunchbase, and SimilarWeb can help you gather insights on user reviews, funding history, and traffic trends. Even monitoring competitors’ job boards can hint at growth or new product launches. Refresh your competitive analysis every 90 days to stay ahead. As Pitchgrade notes:

"The purpose of the competitive analysis is not to prove you have no competition, but to show you understand the landscape and know where you win."

By understanding both competitors and trends, you’ll be better equipped to refine your strategy.

Market Challenges and Opportunities

Every market comes with hurdles and openings. High barriers to entry – like steep capital requirements or exclusive supplier contracts – can protect your position once established but make launching harder. Regulations, such as licensing and data privacy laws like GDPR, add complexity and cost. Economic factors like inflation and high interest rates may reduce consumer spending, while strong brand loyalty to existing leaders can make it tough to gain traction.

On the flip side, challenges often reveal opportunities. Look for unmet pain points by analyzing competitor reviews for gaps between what they promise and deliver. Emerging trends, like sustainability initiatives or AI adoption, can spark new demand. Niche markets that big players overlook often mean less competition and more loyal customers. Finally, technological advances can help you solve old problems more efficiently or affordably. Free resources like the Census Bureau, Bureau of Labor Statistics, Google Trends, and trade associations can help you gather data without breaking the bank.

| Market Challenges | Market Opportunities |

|---|---|

| High Barriers to Entry: Capital needs, patents, or exclusive supplier deals. | Unmet Pain Points: Gaps between competitor promises and results. |

| Regulatory Hurdles: Licensing, safety standards, data privacy laws like GDPR. | Emerging Trends: Sustainability efforts or AI adoption. |

| Economic Factors: Inflation, high interest rates, reduced consumer spending. | Niche Segments: Overlooked groups with specific needs. |

| Brand Loyalty: Strong ties to existing market leaders. | Technological Disruption: New tools solving problems more efficiently. |

Step 4: Outline Your Products, Services, and Operations

After gathering your market insights, it’s time to clearly define what you’re offering and how you plan to operate. This step is about showing investors and partners that you not only have a great idea but also the ability to bring it to life. They’ll want to see exactly what you’re selling, the problem it solves, and how you’ll consistently deliver it to your customers. A detailed plan here demonstrates you’re prepared to handle both the big picture and the nitty-gritty details.

Describe What You’re Selling

Start by explaining the problem your product or service solves. Go beyond listing features – highlight what makes your solution stand out. This could be anything from eco-friendly materials to exclusive technology, same-day delivery, or a pricing model that offers standout value. Whatever your unique selling proposition (USP) is, make it crystal clear.

Be upfront about where your product stands in its lifecycle. If you’re still in the pre-launch phase, include details about prototypes, testing schedules, and feedback from early users. If you’re already selling, share performance metrics like sales trends, repeat purchases, or customer reviews to back up your claims. Outline your pricing strategy and, if applicable, mention any intellectual property protections, such as patents or trademarks, to emphasize your competitive advantage.

Next, map out your supply chain. This helps readers understand how you source materials and manage inventory. For instance, if you promise "premium quality", explain the steps you take to ensure rigorous quality control. Identify any potential supply chain challenges and how you plan to address them. You can include visuals in an appendix to keep this section clean and focused.

Plan Your Day-to-Day Operations

Once you’ve defined the value of your product or service, outline how your daily operations will ensure consistent delivery. This part of your plan demonstrates that you can efficiently turn your vision into reality. Break down how your product is manufactured or how your service reaches the customer. If you’re in the service industry, focus on measurable factors like scheduling, utilization rates, and customer follow-ups – not just sales figures.

List the resources you’ll need, including personnel, technology, capital, and systems like Customer Relationship Management (CRM), Supply Chain Management (SCM), or Enterprise Resource Planning (ERP) platforms. If remote administrative tools are part of your setup, make sure to include them too.

Be sure to document your assumptions so they can be tested and updated as new data comes in. For example, if you assume "50 leads per week with a 20% conversion rate", make that assumption clear. Also, include a log of major risks along with your mitigation strategies. Note any dependencies, whether they involve external vendors or internal teams. Establish governance routines, such as weekly task updates or monthly KPI reviews, to keep everything aligned.

Research shows that businesses with a written plan are 16% more likely to succeed, and those with a clear plan tend to grow 30% faster. On top of that, streamlined workflows can reduce labor and material costs by up to 15% in just one fiscal year. By presenting a well-thought-out operational plan, you not only strengthen your business model but also build investor confidence.

| Planning Level | Focus | Time Horizon |

|---|---|---|

| Strategic | Long-term goals and direction | 3–5 years |

| Tactical | Department-specific targets and resource management | 1 year |

| Operational | Day-to-day execution and short-term budgets | Quarterly/Monthly |

Step 5: Build Your Marketing and Sales Strategy

After laying the groundwork with your market research and operational plans, it’s time to develop a strategy for attracting and retaining customers. Essentially, this is your roadmap for generating revenue. Fun fact: small businesses with a written marketing plan are nearly seven times more likely to succeed than those without one.

How to Attract and Keep Customers

Start by figuring out where your target audience spends their time. Professionals? They’re likely on LinkedIn and email. Gen Z? You’ll find them scrolling TikTok and Instagram. Stick to 2–3 main channels for a few months before branching out. Tools like HubSpot’s "Make My Persona" can help you identify key demographics, pain points, and preferred platforms before diving into ad spending.

Email marketing should be your go-to. Why? It’s incredibly effective, delivering an average return of $36 for every $1 spent. Plus, it’s 40 times better at acquiring customers than social media. As StartupOwl wisely puts it:

"If you aren’t building an email list, you’re renting attention instead of owning it".

Set clear, measurable goals like “gain 50 new email subscribers per month by September 2026” instead of vague objectives. Use UTM parameters on your links to track which campaigns are driving results. For budgeting, the U.S. Small Business Administration advises spending 7–8% of gross revenue on marketing if your business earns under $5 million annually.

When it comes to keeping customers, a CRM is your best friend. It helps you track interactions and create personalized experiences that build lasting trust. Consider offering subscription programs with recurring deliveries and perks like a 10% discount to boost retention. Automated email sequences can also guide new customers toward understanding the full value of your product. Want even more loyal fans? Launch referral campaigns like “Give 20%, Get 20%” to turn happy customers into enthusiastic brand advocates.

Once you’ve nailed your customer acquisition channels, you can fine-tune your revenue model and distribution approach.

Set Your Pricing and Distribution Channels

Your pricing should reflect the value your product offers. If you’re offering premium features, don’t shy away from premium pricing. Tiered pricing or bundle discounts can encourage bigger purchases without eating into your margins. For instance, you could offer a basic plan, a premium tier with extras, or a subscription option that includes a 10% discount for recurring orders.

Choosing the right distribution channels is just as important. For consumer-focused businesses, your website and email list should be at the core of your strategy. Social commerce is growing rapidly, with platforms like Instagram Shops and TikTok enabling customers to shop directly within the app. If you’re in the B2B space, focus on building a structured sales pipeline with clear stages – think Prospecting, Qualifying, Connecting, Meeting/Demo, Proposal, Negotiation, and Closing. Remember, 80% of sales require at least five follow-ups after the first contact.

Document your sales process with a sequence, such as sending an email on Day 1, making a call on Day 3, and following up with a LinkedIn message on Day 5. Use lead scoring to prioritize prospects based on their actions and fit, so your team focuses on the most promising opportunities. Businesses with solid sales plans see a 31% boost in forecast accuracy. Finally, track key metrics like repeat purchase rate (aim for 30% in Year 1) and churn rate (work to reduce it by 15% per quarter) to gauge how well your retention efforts are working.

Step 6: Prepare Your Financial Projections

Your marketing and sales strategy outlines how you’ll attract customers – now it’s time to show the numbers behind the plan. Financial projections are the core of any business plan meant for investors. It’s worth noting that 82% of startups fail due to cash flow issues. Let’s dive into how to translate your strategies into solid financial projections that demonstrate your business’s potential.

Financial Statements You Need to Include

Your business plan must feature three essential financial statements. First, the Income Statement, which demonstrates your profitability. Next, the Cash Flow Statement, which tracks the timing of money coming in and going out. As StartupOwl aptly puts it:

"Profitable on paper does not mean cash in the bank".

Finally, include the Balance Sheet, which provides a snapshot of your financial health using the formula: Assets = Liabilities + Equity. Together, these documents offer investors a detailed view of your financial position and trajectory.

For the first year, break your projections into monthly intervals to account for seasonal trends. For years two and three, quarterly projections will suffice. Use bottom-up forecasting, which starts with specific customer acquisition costs and conversion rates, rather than relying on broad market share assumptions. To show you’re prepared for different scenarios, create three versions of your projections: Base Case, Best Case, and Worst Case. Don’t forget to include "fully loaded" hiring costs – benefits and payroll taxes typically add 20% to 30% to base salaries.

Calculate Your Break-Even Point and Funding Needs

The break-even point is the sales volume where your total revenue matches your total costs. You can calculate it using this formula:

Fixed Costs / (Price per Unit – Variable Cost per Unit).

This figure gives investors a clear idea of the minimum sales you need to cover expenses and start making a profit.

Next, identify any funding gaps. Many B2B customers operate on net-30 or net-60 payment terms, which means payments might not come in right away. Plan for this by maintaining a cash reserve equal to at least 90 days of operating expenses. Add a 10% to 20% buffer to your expense estimates to account for unexpected price increases or supply chain delays. Stress-test your projections by simulating worst-case scenarios, such as a 20% drop in sales or a 15% rise in supplier costs, to see how these challenges could affect your financial runway.

To ensure your projections are accurate and credible, have them reviewed by a CPA or a SCORE mentor. While this review can cost between $300 and $1,200, it’s a worthwhile investment to avoid costly mistakes that could hurt your credibility. Strong financial projections not only validate your strategy but also build trust with investors. With these safeguards in place, you’ll be ready to present a business plan that stands up to scrutiny.

Step 7: Add Your Funding Request and Appendix

With your financial projections in place, it’s time to focus on securing funding and backing up your plan with solid documentation. This involves crafting a clear funding request and assembling an appendix that supports your business plan.

Craft a Clear Funding Request

After laying out your financial projections, this step turns those numbers into a specific investment proposal. Clearly state the exact amount of funding you’re seeking and detail how you plan to allocate it. Break it down into categories like product development, marketing, staffing, and operational costs.

Tie your funding request to key business milestones. For example, explain how the funds will help achieve revenue goals or expand market share. Specify whether you’re asking for equity funding or a loan, and include details about repayment terms or exit strategies where applicable. Tailor your pitch to your audience: use metrics like growth rates and ROI for venture capitalists, while focusing on cash flow and debt repayment for lenders. Wrap it up with a call to action, such as requesting a meeting or outlining a timeline for fund usage.

What Belongs in the Appendix

The appendix is where you back up your claims with credible, verifiable documents. As Vinay Kevadiya, CEO of Upmetrics, explains:

"Often overlooked appendix in a business plan is an unsung hero that brings your vision to life in ways the main document simply can’t".

Start with a table of contents to keep everything organized. Then, group your documents into sections like Financials, Legal, Team Credentials, and Contracts.

- Financial documents: Include 3-to-5-year projections, bank statements, and tax returns.

- Legal documentation: Add business licenses, permits, articles of incorporation, patents, and trademarks.

- Operational agreements: Include supplier contracts, lease agreements, and customer Letters of Intent.

- Team credentials: Provide resumes, certifications, and awards to showcase your team’s expertise.

Use cross-references in your main plan (e.g., "See Appendix, Page 5") to guide readers to the relevant supporting documents. Finally, export the entire appendix as a PDF to preserve the formatting and make the document uneditable.

Conclusion: Turn Your Business Plan Into Action

What New Founders Should Remember

A well-thought-out business plan does more than just attract funding – it acts as a living guide for your startup’s journey. It validates your ideas and tests whether your business concept can succeed. By going through the research and planning process, you’ll be better prepared to make informed decisions and adapt to market changes quickly.

Your plan should clearly explain what you’re building, who your target audience is, and how you’ll make money. Most effective business plans are concise, running between 15 and 20 pages. Think of this document as your roadmap – it will guide you through every phase of launching, managing, and growing your venture. Keep this focus as you shift from planning to execution.

What to Do After You Finish Your Plan

Your business plan isn’t a static document to be filed away. Instead, treat it like a GPS for your business – something you adjust as market conditions and challenges evolve. Jesse Bardo, Executive Director in Startup Banking at J.P. Morgan, emphasizes this point:

"The best founders, the best startups are constantly iterating. These companies work to understand changes in their customer preferences and stay ahead of those shifts."

Make it a habit to review and update your plan regularly. Rapidly growing companies often revisit their plans quarterly, while others do so every six months or annually. During these updates, evaluate whether your initial goals are still relevant, assess staffing needs or the potential for hiring consultants, and adjust financial projections based on actual performance. Use feedback from customers after your product launch to refine your offerings and stay responsive to evolving market demands.

To keep your business running smoothly, consider using professional services for operational and compliance support. These services can help you manage your company’s structure and meet regulatory requirements, freeing you up to focus on executing your business plan effectively.

FAQs

How do I validate demand before writing the full plan?

To ensure there’s genuine market demand for your product or service, rely on a process rooted in data. Start by gathering real evidence through methods like customer interviews, testing ideas with minimum viable products (MVPs), and analyzing honest feedback.

Be cautious about leaning on input from friends or family – they might not provide the objective insights you need. Assumptions can also be misleading. Instead, focus on verifying that your solution solves a real problem. This way, you’ll avoid pouring resources into a product that lacks a true audience.

What should I include if I’m pre-revenue or pre-launch?

If your business hasn’t started generating revenue or is still in the pre-launch phase, it’s crucial to emphasize its potential and the strength of your planning. Focus on presenting key aspects such as your business concept, target audience, competitive analysis, and progress in product development. Additionally, outline your operational strategies to give a clear picture of how the business will function.

It’s also important to include realistic short-term financial projections. These should clearly show how you intend to achieve milestones and manage cash flow effectively. By doing this, you demonstrate to investors and stakeholders that you’re well-prepared and have a solid plan for growth, even if you haven’t started generating revenue yet.

How do I make my financial projections believable to investors?

To ensure your financial projections are solid and believable, base your assumptions on realistic, data-driven insights. Pay close attention to critical financial factors such as customer acquisition costs, profitability timelines, and cash flow management. Build a bottom-up financial model that draws on reliable market data to present a clear and persuasive narrative. Consistently updating your forecasts for sales, expenses, and growth shows that you’re well-prepared and can boost investor trust in your planning.