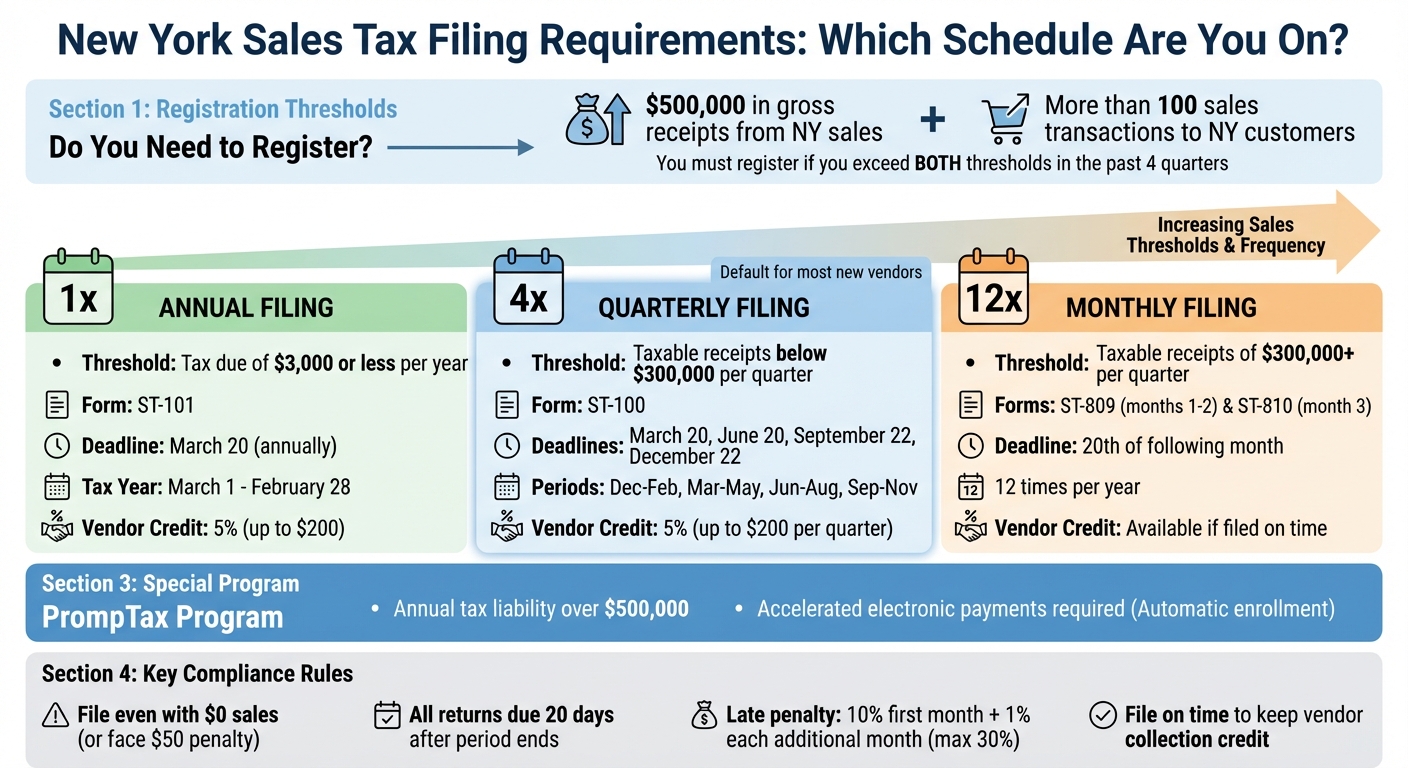

If your business ships to customers in New York, you might need to collect and file sales tax – even without a physical presence in the state. Remote sellers must register and comply if they exceed both of these thresholds in the past four quarters:

- $500,000 in gross receipts from New York sales.

- More than 100 sales transactions to New York customers.

Missing deadlines can result in penalties, daily interest, and lost vendor credits. Filing schedules depend on your sales volume:

- Monthly: Taxable receipts of $300,000 or more per quarter.

- Quarterly: Taxable receipts below $300,000 per quarter.

- Annual: Tax due of $3,000 or less per year.

Deadlines fall on the 20th of the month following the reporting period, adjusted for weekends or holidays. Filing is required even if no sales occur, with a $50 minimum penalty for non-compliance. Stay compliant by using New York’s Sales Tax Web File system and keeping thorough records.

New York Sales Tax Filing Deadlines by Frequency

New York assigns sales tax filing schedules based on your sales volume, with each schedule having specific forms and deadlines. Returns must be submitted within 20 days after the reporting period ends. If the due date lands on a weekend or holiday, you can file on the next business day. Even if you have no sales during a period, you’re still required to file a return to stay compliant.

Monthly Filing Deadlines (Form ST-809)

Businesses with higher sales volumes often follow a monthly filing schedule. For the first two months of each quarter, monthly filers use Form ST-809. For the third month, they file Form ST-810, which summarizes the entire quarter. This schedule applies if your combined taxable receipts, purchases, rents, and amusement charges total $300,000 or more in a quarter. All returns are due by the 20th of the following month, with adjustments for weekends or holidays.

| Sales Period | Due Date |

|---|---|

| January 2025 | February 20, 2025 |

| February 2025 | March 20, 2025 |

| March 2025 | April 21, 2025 |

| April 2025 | May 20, 2025 |

| May 2025 | June 20, 2025 |

| June 2025 | July 21, 2025 |

| July 2025 | August 20, 2025 |

| August 2025 | September 22, 2025 |

| September 2025 | October 20, 2025 |

| October 2025 | November 20, 2025 |

| November 2025 | December 22, 2025 |

| December 2025 | January 20, 2026 |

Quarterly Filing Deadlines (Form ST-100)

If your sales volume isn’t high enough to require monthly filings, you’ll likely file quarterly using Form ST-100. This form is submitted four times a year, and most businesses complete the process online using the Sales Tax Web File system through their Business Online Services account. For timely filers who pay their taxes in full, New York offers a vendor collection credit of 5% of the tax collected, capped at $200 per quarter.

| Sales Tax Quarter | Period Covered | Due Date |

|---|---|---|

| 1st Quarter | December 1, 2024 – February 28, 2025 | March 20, 2025 |

| 2nd Quarter | March 1, 2025 – May 31, 2025 | June 20, 2025 |

| 3rd Quarter | June 1, 2025 – August 31, 2025 | September 22, 2025 |

| 4th Quarter | September 1, 2025 – November 30, 2025 | December 22, 2025 |

Annual Filing Deadlines (Form ST-101)

For businesses with lower sales volumes, filing happens just once a year using Form ST-101. The annual filing deadline is March 20. For example, the tax year covering March 1, 2025, through February 28, 2026, must be filed by March 20, 2026. Like quarterly filers, annual filers can claim the 5% vendor collection credit (up to $200) if they file and pay on time. If you close your business or stop selling in New York, you’re required to file a final return within 20 days and destroy your Certificate of Authority.

| Tax Year Period | Due Date |

|---|---|

| March 1, 2024 – February 28, 2025 | March 20, 2025 |

| March 1, 2025 – February 28, 2026 | March 20, 2026 |

Next, discover how New York determines your filing frequency based on your sales volume, or you can compare business formation services to see how they handle compliance for you.

How New York Assigns Your Filing Frequency

Sales Volume Determines Filing Frequency

In New York, your filing frequency for sales tax is determined by the Tax Department based on your taxable sales, purchases subject to use tax, or the total tax you owe. Essentially, your sales activity dictates how often you need to file.

If you owe $3,000 or less in sales tax during the annual filing period (March 1 through February 28/29), you’ll be classified as an annual filer. For most new vendors, the default is quarterly filing, which applies when your taxable receipts, rents, and amusement charges stay below $300,000 per quarter. However, if your taxable receipts hit $300,000 or more in any quarter, you’ll need to file monthly.

For businesses with an annual tax liability over $500,000, you’ll be automatically enrolled in the PrompTax program, requiring accelerated electronic payments. You can check your assigned filing schedule and required forms under the "Current filing" section of your Business Online Services account.

Here’s a quick breakdown of the thresholds for each filing schedule:

| Filing Frequency | Taxable Sales / Tax Due Threshold | Form Used |

|---|---|---|

| Annual | Owe $3,000 or less in tax per year | ST-101 |

| Quarterly | Taxable receipts under $300,000 per quarter | ST-100 |

| Monthly | Taxable receipts of $300,000 or more in any quarter | ST-809 & ST-810 |

| PrompTax | Annual tax liability over $500,000 | ST-810 (accelerated payments) |

Up next, we’ll look at how you can adjust your filing frequency if your sales volume changes.

Changing Your Filing Frequency

Once your filing frequency is set, it may need to be adjusted if your sales volume changes. The Tax Department monitors your activity and will automatically reclassify your filing schedule as needed, notifying you by mail. For example, if you’re a quarterly filer and your tax due is $3,000 or less for four consecutive quarters, you may be reclassified as an annual filer. Similarly, if your taxable receipts exceed $300,000 in a single quarter, you’ll be switched to monthly filing starting the first month of the next sales tax quarter.

If you’re looking to move from monthly to quarterly filing, you’ll need to take action yourself. Your taxable receipts must stay below $300,000 for four consecutive quarters before you can request a change. To initiate this, contact the Sales Tax Information Center at 518-485-2889 and provide documentation confirming your lower sales volume.

It’s important not to change your filing frequency on your own. Any adjustments should be made only after receiving official notification or approval from the Tax Department. If you qualify for a downgrade after meeting the necessary criteria, reach out to the Sales Tax Information Center at 518-485-2889 for assistance.

Penalties and How to Avoid Them

Late Filing and Payment Penalties

New York enforces strict penalties for missing tax filing or payment deadlines. If you’re late, the state charges a penalty starting at 10% of the tax owed for the first month, plus an additional 1% for each month after that, up to a maximum of 30%. However, there’s always a minimum penalty of $50. If your return is more than 60 days late, the penalty becomes even harsher: it’s the greater of the standard penalty, $100 (or 100% of the tax owed, whichever is less), or the $50 minimum.

Interest on unpaid taxes compounds daily – even if you’ve been granted an extension – and the rate adjusts quarterly. If your reported tax is short by more than 10% or $2,000 (whichever is greater), you’ll face an extra 10% penalty on the shortfall. Negligence triggers a 5% penalty, plus 50% of the interest due, while deliberate tax evasion can lead to a penalty equal to 200% of the unpaid amount.

Late filers also lose out on New York’s vendor collection credit, which offers a 5% credit on taxes collected (up to $200 per quarter) but only applies if you file on time and pay in full. Additionally, failing to maintain proper records can result in penalties of up to $1,000 for the first quarter of non-compliance and $5,000 for subsequent quarters.

To avoid these costly consequences, it’s essential to meet all filing deadlines and ensure payments are accurate and on time.

Tips for Staying Compliant

- File a return even with no sales: If you’ve had no taxable activity, New York still requires you to file by the deadline. Failing to do so can result in a $50 penalty.

- Use the Sales Tax Web File system: Through your Business Online Services account, this tool calculates taxes, penalties, and interest automatically, minimizing errors. It also allows you to schedule payments in advance, ensuring they’re processed on time.

- Set reminders for deadlines: Returns are due 20 days after the end of the reporting period. For quarterly filers, deadlines typically fall on March 20, June 20, September 20, and December 20. You can also subscribe to Tax Department email alerts to stay updated on deadlines and rate changes.

- Keep thorough records: Maintain detailed and auditable records, including exemption certificates (like Form ST-120) and sales data. Ensure electronic records are preserved in their original format for audits. Using Web File worksheets can help you organize data before filing.

If you miss a deadline due to a reasonable cause (not intentional neglect), you can request a penalty waiver. For those who need to catch up on past filings, New York’s Voluntary Disclosure Program provides an opportunity to report back taxes and potentially avoid certain penalties or criminal charges.

sbb-itb-ba0a4be

How BusinessAnywhere Helps with Sales Tax Compliance

Compliance Support for Remote Sellers

Staying on top of New York sales tax deadlines is crucial for remote sellers, and BusinessAnywhere makes this task much easier. With automated alerts, the platform ensures you never miss a filing deadline, helping you avoid costly penalties for late submissions.

BusinessAnywhere also provides registered agent and virtual mailbox services, ensuring you promptly receive all communications from the New York State Department of Taxation and Finance. This includes updates on tax rate changes, reporting requirements, and any additional information requests.

For remote sellers who need an Employer Identification Number (EIN) to register as a vendor and access New York’s Sales Tax Web File system, BusinessAnywhere offers an EIN application service to simplify the process.

The platform is designed to accommodate different filing frequencies, making it a flexible solution for businesses with varying needs.

Services for New York Remote Sellers

In addition to timely alerts, BusinessAnywhere customizes its support to match your specific filing schedule. Whether you file monthly (Form ST-809), quarterly (Form ST-100), or annually (Form ST-101), the platform tracks all deadlines and sends reminders to keep you on schedule. Filing on time also ensures you maintain benefits like vendor collection credits.

The virtual mailbox service adds another layer of convenience by providing a professional U.S. business address. You can access scanned mail through an online dashboard, which is especially useful for responding quickly to notices from the Tax Department. When paired with the registered agent service, you get comprehensive coverage for all official state communications, making compliance simple and accessible no matter where you are.

Conclusion

Staying on top of your New York sales tax obligations is crucial for remote sellers. Make sure to file within 20 days of each reporting period using the correct form – ST-809 for monthly, ST-100 for quarterly, or ST-101 for annual filers. Even if you haven’t made any taxable sales, filing is still required to avoid a $50 minimum penalty.

Keep a close eye on your sales volume. If your taxable receipts exceed $500,000, you’ll need to enroll in the PrompTax program. On the flip side, filing on time can earn you a 5% vendor collection credit, capped at $200 per reporting period.

New York also holds "responsible persons" – such as owners, officers, or managers with financial authority – personally liable for any unpaid sales tax. To protect yourself, ensure your business information is always up to date by submitting Form DTF-95. This step helps you avoid personal liability and ensures you receive all communications from the New York State Department of Taxation and Finance.

Using the right tools can make compliance much easier. The Sales Tax Web File system and services like BusinessAnywhere offer automated deadline alerts, registered agent services, and virtual mailbox access to keep you informed and maintain your eligibility for credits.

FAQs

What happens if I miss a New York sales tax filing deadline?

Missing a New York sales tax filing deadline can lead to some hefty penalties. For late filings, the penalty is 5% of the tax owed per month (or part of a month), capped at a maximum of 25%. On top of that, there’s a minimum penalty of either $50 or $100, depending on how much you owe.

If taxes remain unpaid, you’ll face an additional late payment penalty of 0.5% per month, also capped at 25%, plus daily compounded interest on the unpaid balance. Keeping track of deadlines is crucial to avoid these unnecessary costs.

How is my sales tax filing frequency determined in New York?

When it comes to sales tax in New York, your filing frequency – whether it’s monthly, quarterly, or annually – depends on the total taxable sales, taxable purchases subject to use tax, or the total tax owed by your business. Generally, businesses with higher numbers in these categories are required to file more often, while those with lower amounts might qualify for less frequent filing, like quarterly or annual submissions.

New York sets your filing frequency when you first register for a sales tax permit. However, this isn’t set in stone. The state may adjust your filing schedule later based on the sales and tax data you report. It’s a good idea to regularly check your filing requirements to ensure you’re meeting New York’s tax regulations. Staying on top of this can help you avoid unnecessary penalties or complications.

What should I do if changes in my sales volume affect how often I need to file sales tax in New York?

If your sales or taxable purchases experience a noticeable shift – whether rising or falling – your filing frequency might need to be adjusted. The New York State Department of Taxation and Finance determines whether you should file monthly, quarterly, or annually based on the volume of your reported taxable sales and purchases. Higher sales volumes typically require more frequent filings, while lower volumes may qualify for less frequent submissions.

To update your filing frequency, simply log in to your Business Online Services account. From there, review your business details and make any necessary changes to your filing schedule in the sales tax section. If this adjustment happens in the middle of a filing period, you may also need to submit an amended return to accurately reflect your updated sales figures. Remember, all sales tax filings must be completed electronically using the state’s Sales Tax Web File system.

For a hassle-free way to manage compliance, tools like BusinessAnywhere can be a game-changer. They help you keep track of sales thresholds, handle filings, and ensure everything is submitted on time – taking the stress out of staying compliant.