If you’re a landlord, protecting your personal assets is critical. The two most common strategies for liability protection are umbrella insurance and forming an LLC. But they serve different purposes, and neither fully replaces the other. Here’s the key takeaway:

- Umbrella insurance adds extra liability coverage (starting at $1M) beyond your landlord insurance, covering lawsuits, settlements, and legal fees. It costs $150–$350 annually, making it an affordable option for financial protection.

- LLCs create a legal barrier between your personal assets and your rental property. If someone sues, only the LLC’s assets are at risk, not your personal wealth. However, maintaining an LLC involves setup fees ($50–$500) and ongoing administrative work.

Which should you choose?

- Use umbrella insurance alone if you own a few properties and want simple, affordable coverage.

- Form an LLC alone if you prioritize legal separation of assets, privacy, and tax benefits.

- Combine both if you own multiple properties or have significant personal wealth to protect.

These tools work best together: umbrella insurance covers financial damages, while an LLC shields personal assets from lawsuits that exceed coverage limits.

What Is an Umbrella Insurance Policy?

Umbrella insurance acts like a financial backup plan, offering extra protection beyond your standard landlord insurance. It kicks in only when your primary policy’s liability limits – usually between $100,000 and $500,000 – are maxed out. For instance, if a tenant wins a $2 million lawsuit and your primary policy covers $500,000, the umbrella policy would step in to handle the remaining $1.5 million.

Insurers typically require you to have a minimum liability limit of $300,000 to $500,000 on your primary policies before you can purchase umbrella coverage. This ensures you’re not relying solely on the umbrella policy for basic protection. One advantage? A single umbrella policy can often cover multiple rental properties, even if they’re in different states, making it a practical alternative to setting up separate LLCs for each property.

Umbrella policies start at $1 million in coverage and can increase in $1 million increments, going up to $10 million or more. On average, they cost about $593 annually, with an additional $100–$150 per million in coverage.

What Umbrella Policies Cover

Umbrella insurance goes beyond the scope of standard landlord policies. While your primary insurance covers common incidents like slip-and-fall accidents or property damage, an umbrella policy provides additional protection for "personal injury" claims. These include libel, slander, defamation, false arrest, and even malicious prosecution.

A major perk of umbrella coverage is that it also covers legal defense costs, which can add up quickly – even if you win the case. For example, if a tenant sues you for defamation or wrongful eviction, the umbrella policy would cover attorney fees and any judgment awarded. It also often covers compensation for mental anguish or emotional distress, which can be substantial in landlord-tenant disputes.

"Umbrella insurance doesn’t just extend your liability limits. It also covers certain situations your standard landlord policy might not address, like slander claims, mental anguish awards, or unusual events such as riots and explosions." – Jeremy Layton, Web Marketing Lead, Steadily

What Umbrella Policies Don’t Cover

Despite their broad scope, umbrella policies have clear limits. They won’t cover damage to your own property – this coverage is strictly for third-party liability. So, if a fire destroys your rental building, your umbrella policy won’t help with repair costs.

Other exclusions include intentional or criminal acts, business losses, contract disputes, and personal injuries to you. If you manage a large rental portfolio as a business, a personal umbrella policy might not cover business-related claims, meaning you’d need a commercial umbrella policy instead. Common exclusions also include liability assumed under a contract, punitive damages, and claims related to the transmission of diseases.

It’s important to note that umbrella policies have maximum coverage limits. For instance, if a court awards $5 million in damages and your umbrella policy only covers $2 million, you’d be personally responsible for the remaining $3 million. This is different from the protection offered by an LLC, which can shield personal assets regardless of the judgment size.

There are several benefits of forming an LLC for rental property that go beyond simple liability coverage. Next, we’ll explore how an LLC offers a different layer of protection for landlords.

What Is an LLC for Rental Properties?

A Limited Liability Company (LLC) is a business structure that separates your personal finances from your rental property business. When your rental property is held in an LLC, the company – not you personally – owns the property. This setup means that if someone sues the LLC or the business racks up debts, creditors can only go after the LLC’s assets, such as the rental property or its bank accounts.

Unlike umbrella insurance, which has a set coverage limit, an LLC offers a different kind of protection – your personal assets like your home, car, or savings remain off-limits as long as you follow the rules for maintaining the LLC. There’s no preset cap on this protection, provided the LLC is properly managed.

"By forming an LLC, only the LLC is liable for the debts and liabilities incurred by the business – not the owners or managers." – Stephen Fishman, J.D., Nolo

LLCs also come with tax perks. They use pass-through taxation, meaning the company itself doesn’t pay federal income tax. Instead, profits and losses are reported on your personal tax return, and you might even qualify for up to a 20% deduction on your rental income. This setup avoids the double taxation that corporations often face.

However, this protection only works if you treat the LLC as a separate entity. That means keeping personal and business finances separate, using dedicated bank accounts, and signing contracts or leases in the LLC’s name (e.g., "John Doe, Member of ABC Rentals LLC"). If you mix personal and business funds, a court could "pierce the corporate veil", leaving you personally liable. Keeping this separation intact not only protects you legally but also sets the foundation for practical advantages, which we’ll explore next.

How LLCs Protect Landlords

The main benefit of an LLC is shielding your personal assets. If a tenant or visitor sues over an injury or property issue, the lawsuit targets the LLC, not you. This means your personal home, retirement savings, and other assets stay protected. Similarly, if the LLC takes on debt or faces a contract dispute, only the LLC’s assets are at risk – as long as you’ve followed the proper rules.

That said, an LLC won’t shield you from liability for your own negligence or fraudulent actions.

How to Form and Maintain an LLC

To create an LLC, you’ll need to file Articles of Organization with your state’s business office to set up an LLC for real estate. Most states allow you to do this online, and the process can take a few days to a few weeks. You’ll also need an Employer Identification Number (EIN) from the IRS, which is usually required for opening a business bank account.

To keep your LLC’s protection intact, you’ll need to stay on top of annual state filings and maintain a clear separation between your personal and business finances. Open a business bank account for all rental income and expenses, and ensure all leases, contracts, and vendor agreements are signed in the LLC’s name. If you originally bought the property under your name, you’ll need to transfer the title to the LLC using a deed – just check with your lender first to see if there’s a "due-on-sale" clause.

"If a third party cannot differentiate between the entity and the individual owner, then the entity’s limited liability veil could be pierced." – Kevin Kim, Partner and Department Head of Corporate and Securities, Fortra Law

In addition to legal protection, LLCs offer tax benefits that can make a big difference for landlords.

Tax Treatment of LLCs

LLCs benefit from pass-through taxation, meaning rental income and expenses are reported directly on your personal tax return, typically on Schedule E for single-member LLCs. This avoids the double taxation that C-corporations face.

On top of that, eligible LLC owners can take advantage of the Qualified Business Income (QBI) deduction, which allows up to a 20% deduction on net rental income. For example, if your LLC earns $50,000 in net rental income, you could potentially deduct $10,000, reducing your taxable income.

You can also claim standard rental property deductions like mortgage interest, property taxes, repairs, depreciation, insurance, and even travel expenses related to managing your properties. Keeping detailed records and using the LLC’s bank account exclusively for business expenses is crucial to ensuring you can claim these deductions.

For multi-member LLCs, the IRS treats the entity as a partnership by default, requiring you to file Form 1065 and issue Schedule K-1s to each member. Single-member LLCs, on the other hand, are considered "disregarded entities", so all income and expenses are reported on your personal tax return.

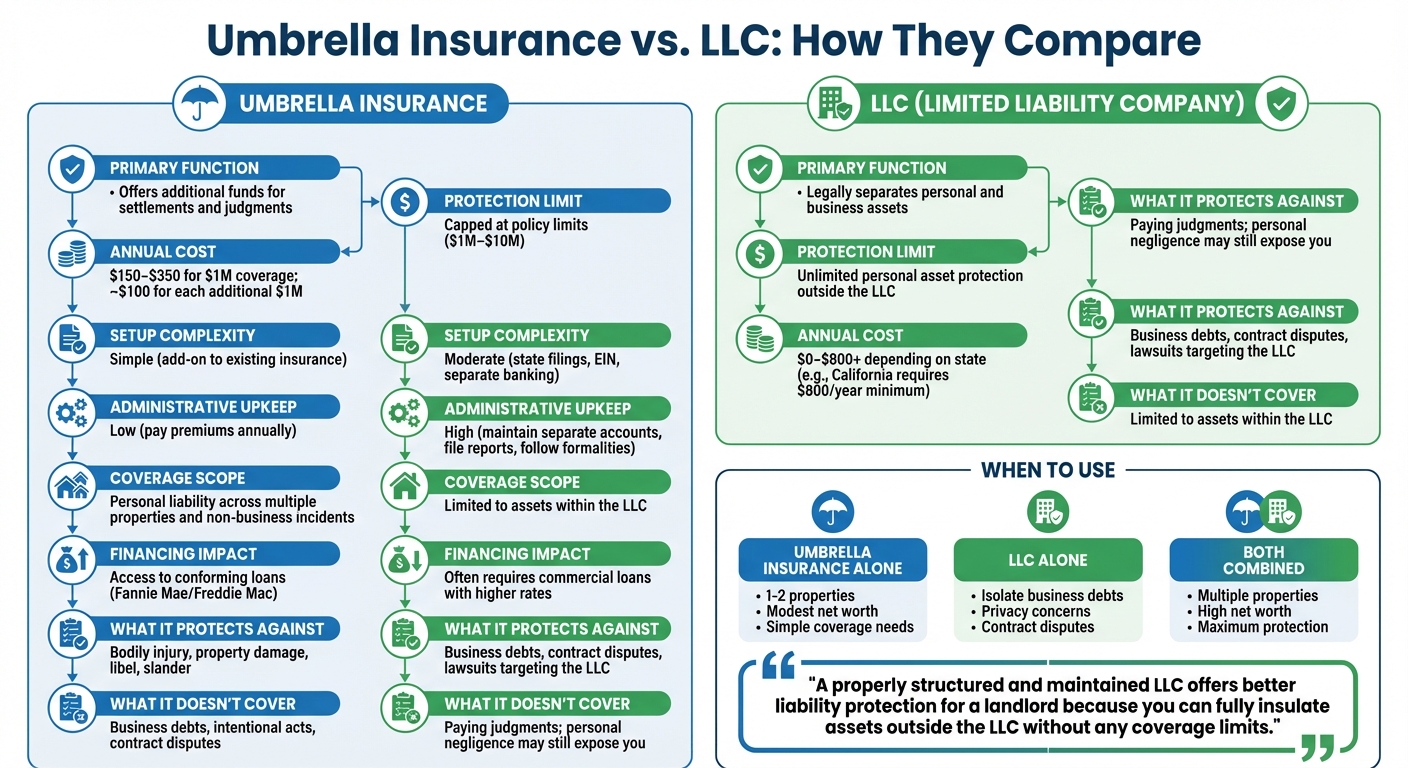

Umbrella Insurance vs. LLC: How They Compare

Umbrella insurance and LLCs serve landlords in very different ways. One provides financial backup for claims, while the other creates a legal barrier to shield personal assets. Neither can fully replace the other, so the choice – or combination – depends on your circumstances.

Side-by-Side Comparison: Protection, Costs, and Coverage

Here’s a breakdown of how umbrella insurance and LLCs differ across key factors:

| Feature | Umbrella Insurance | LLC (Limited Liability Company) |

|---|---|---|

| Primary Function | Offers additional funds for settlements and judgments | Legally separates personal and business assets |

| Protection Limit | Capped at policy limits ($1M–$10M) | Unlimited personal asset protection outside the LLC |

| Annual Cost | $150–$350 for $1M coverage; ~$100 for each additional $1M | $0–$800+ depending on state (e.g., California requires $800/year minimum) |

| Setup Complexity | Simple (add-on to existing insurance) | Moderate (state filings, EIN, separate banking) |

| Administrative Upkeep | Low (pay premiums annually) | High (maintain separate accounts, file reports, follow formalities) |

| Coverage Scope | Personal liability across multiple properties and non-business incidents | Limited to assets within the LLC |

| Financing Impact | Access to conforming loans (Fannie Mae/Freddie Mac) | Often requires commercial loans with higher rates |

| What It Protects Against | Bodily injury, property damage, libel, slander | Business debts, contract disputes, lawsuits targeting the LLC |

| What It Doesn’t Cover | Business debts, intentional acts, contract disputes | Paying judgments; personal negligence may still expose you |

"A properly structured and maintained LLC offers better liability protection for a landlord because you can fully insulate assets outside the LLC without any coverage limits." – Road Less Traveled Finance

Here’s the key difference: umbrella insurance helps pay judgments, while an LLC limits a plaintiff’s reach to the LLC’s assets. For example, if a $3 million judgment exceeds your $1 million umbrella coverage, you’re responsible for the remaining $2 million. However, with a well-maintained LLC, the plaintiff can only go after the LLC’s holdings – like the rental property and its accounts – leaving your personal assets untouched.

This comparison shows that while both tools offer valuable protections, they serve different purposes and work best when used together.

When to Use One or Both

Your choice between umbrella insurance, an LLC, or both depends on your risk tolerance and property portfolio.

- Go with umbrella insurance alone if you own one or two single-family rentals, have a modest net worth, and live in a state with high LLC fees (like California’s $800 minimum). Umbrella policies are straightforward, affordable ($150–$350 annually), and offer broad coverage for both personal and rental property liabilities.

- Choose an LLC alone if your main goal is to isolate business debts, handle contract disputes, or keep your name off public property records. Just remember, an LLC doesn’t provide funds for legal defense or settlements – you’ll need cash reserves or insurance for that.

- Combine both if you’re a high-net-worth landlord or own multiple properties, especially higher-risk ones like apartment buildings. The LLC protects your personal assets, while the umbrella policy ensures you have the funds to handle lawsuits or settlements. This layered approach is widely recommended by real estate professionals.

"Umbrella covers you personally. It won’t stop someone suing the LLC itself… LLCs won’t pay a verdict; you need insurance for that." – Jazzmin Lu, Licensed Insurance Broker

Using both tools together creates a safety net that’s especially valuable in real-world cases where risks are higher.

Examples: How Umbrella Insurance and LLCs Work in Practice

Real-life situations help illustrate how umbrella insurance and LLCs function when lawsuits arise, showing when it makes sense to use one or both. Let’s break down two scenarios to highlight their distinct roles.

Example 1: Tenant Injury Lawsuit

Imagine a tenant slips on an icy walkway at your rental property and sues for $300,000 to cover medical bills, lost wages, and pain and suffering. The property itself is worth $700,000, with $400,000 in equity.

If you only have umbrella insurance: Your primary landlord insurance covers the initial portion of the claim, typically between $300,000 and $500,000. After that, your umbrella policy steps in to cover the rest. In this case, you’d only be responsible for a deductible of about $10,000, while the insurance company takes care of the remaining amount. This approach protects the equity in your property.

If you only have an LLC: The tenant sues the LLC. If they win, the $300,000 judgment must be paid using the LLC’s assets. Since your property has $400,000 in equity, $300,000 of that could be used to satisfy the claim. While your personal assets remain safe, you’d lose a significant portion of your property’s value.

"Umbrella insurance is your first line of defense against personal lawsuits." – Jazzmin Lu, Licensed Insurance Broker

For smaller claims like this, umbrella insurance provides more direct financial protection because it pays the debt outright, rather than simply isolating it within a business structure. However, umbrella insurance alone may not be enough for more severe claims.

Example 2: Large Judgment Exceeding Coverage Limits

Now, consider a catastrophic incident at your rental property that results in a $20 million judgment against you. The property is worth $3 million, and you have a $2 million umbrella policy.

If you only have umbrella insurance: The policy covers its $2 million limit, but you’re still responsible for the remaining $18 million. Creditors could go after your personal assets, such as your home, savings, and retirement accounts, potentially leading to personal bankruptcy.

If you only have an LLC: The plaintiff can only claim assets owned by the LLC, which means they’re limited to your $3 million rental property. You’d lose the property, but your personal assets, including your home and savings, would remain protected by the corporate veil.

If you have both: The umbrella policy covers $2 million of the judgment, reducing your liability. The LLC limits the remaining exposure to the $3 million rental property, fully protecting your personal assets while minimizing your total loss.

"Think of insurance as your first line of defense and the LLC as the fortress protecting everything else you own." – Russo Law Group

Landlords with multiple properties or substantial assets often gain the most by combining both protections. Umbrella insurance handles routine claims, while the LLC serves as a safeguard against catastrophic judgments that exceed insurance limits. This layered approach ensures both financial stability and peace of mind.

sbb-itb-ba0a4be

Costs and Trade-Offs of Umbrella Insurance and LLCs

When deciding between umbrella insurance, LLCs, or sole proprietorships, landlords need to weigh both the financial costs and the practical implications of each option to determine the best protection strategy for their rental properties.

Cost Breakdown

Umbrella insurance tends to be the more budget-friendly option upfront. A $1 million policy usually costs between $150 and $350 per year, with each additional $1 million in coverage adding around $100 annually. For instance, a $10 million policy might total approximately $1,578 per year. However, insurers often require higher limits on primary policies (typically increasing from $100,000 to $300,000–$500,000), which could raise existing premiums.

On the other hand, forming and maintaining an LLC involves both one-time and recurring expenses. State filing fees range from $50 to $500, with an average cost of about $132. Hiring an attorney for proper setup can add $500 to $2,000 in legal fees. Annual fees also vary by state – for example, California imposes an $800 franchise tax, while states like Texas and New Mexico have no such requirement. Additionally, tax preparation for multiple LLCs can become costly, as each entity requires separate filings, potentially adding thousands of dollars annually.

With these costs in mind, let’s explore the specific benefits and limitations of umbrella insurance and LLCs.

Benefits and Drawbacks of Umbrella Policies

Advantages:

Umbrella insurance offers extensive liability coverage that kicks in once your primary policy limits are exceeded. It can help cover legal judgments, settlements, and defense costs, all at a relatively low cost – often less than $1 per day for $1 million in coverage. These policies also frequently cover claims like libel, slander, and false arrest, which are typically excluded from standard insurance. Adding an umbrella policy is usually simple and can often be done through your current insurance provider.

Disadvantages:

While umbrella insurance provides valuable coverage, it doesn’t create a legal separation between your personal and business assets. If a claim exceeds your policy limits, creditors could still go after personal assets like your home or retirement savings. Additionally, umbrella policies generally exclude intentional acts, criminal behavior, and certain business-related liabilities. Some landlords worry that having a high coverage amount might make them a more appealing target for lawsuits seeking large payouts.

Benefits and Drawbacks of LLCs

Advantages:

An LLC establishes a "corporate veil", which legally separates your personal assets from your rental business. This means creditors cannot typically access personal assets, such as your primary residence or personal savings, to settle business debts. LLCs also provide tax flexibility, including the option to elect S-Corp status, and can help preserve privacy by keeping your name off public property records.

Disadvantages:

An LLC doesn’t pay claims directly, so without insurance, the LLC’s assets – like your rental property – could still be at risk in a lawsuit. Additionally, maintaining an LLC requires strict adherence to administrative rules, such as maintaining separate bank accounts, keeping detailed records, and filing timely paperwork. Failing to comply with these requirements could lead to "piercing the corporate veil", which would eliminate the liability protection. Financing can also be more challenging, as lenders often prefer individuals over business entities for favorable loan terms.

"If a third party cannot differentiate between the entity and the individual owner, then the entity’s limited liability veil could be pierced."

- Kevin Kim, Partner and Department Head of Corporate and Securities, Fortra Law

Do Landlords Need Both Umbrella Insurance and an LLC?

The short answer: it depends on your portfolio and how much risk you’re willing to take on. For many landlords, combining both provides the best protection. An LLC isolates your personal assets legally, while umbrella insurance offers financial reserves. Here’s how to decide what works best for your situation.

Recommendations by Landlord Type

Small-scale landlords with just one or two properties might find umbrella insurance sufficient to start. It’s an affordable option that provides immediate protection without the hassle of setting up and maintaining an LLC. For example, in states like California, where the annual $800 franchise tax applies, the cost of an LLC might outweigh the risk exposure of a single rental property.

Landlords with growing portfolios should consider forming LLCs early. Once you own three or more properties or rely heavily on rental income, the legal protection of an LLC becomes vital. Setting up multiple LLCs – or a Series LLC in states like Texas – can shield each property individually. This way, a lawsuit involving one property won’t jeopardize your other investments. Pair this structure with a single umbrella insurance policy to cover your entire portfolio, and you’ll have strong, cost-effective protection.

High-net-worth landlords need both. If your personal assets – like retirement accounts, investments, or home equity – exceed $1 million, umbrella insurance alone may not be enough. An LLC ensures that plaintiffs can’t go after your personal wealth, while umbrella insurance provides the financial cushion to handle large judgments.

"Smart landlords recognize that these strategies work together to create comprehensive liability protection that neither achieves alone."

- Jeremy Layton, Web Marketing Lead, Steadily

High-risk properties – like older buildings, multi-unit complexes, or rentals with pools and shared spaces – come with higher liability concerns. In these cases, combining LLCs with robust umbrella insurance provides the layered protection you’ll need to handle serious injury claims or other legal challenges.

How BusinessAnywhere Simplifies LLC Formation

If you’re considering forming an LLC, BusinessAnywhere makes the process straightforward and cost-effective. They offer $0 service fees for LLC formation – you’ll only pay your state’s filing fee, which averages around $132 nationwide. Plus, you’ll get a free registered agent for the first year (a $147 value).

Everything is handled online through their dashboard, including filing paperwork, getting your EIN, and compliance reminders. For landlords managing properties in multiple states, their virtual mailbox service for real estate investors (starting at $20/month) provides a professional U.S. address for each LLC – no need for physical office space. Check out their business registration services for simple, transparent pricing with no hidden fees.

Conclusion

An umbrella policy and an LLC serve distinct purposes, but together, they create a strong defense strategy for landlords. Umbrella insurance acts as a financial safety net, covering claims that exceed your primary insurance limits. Meanwhile, an LLC establishes a legal barrier, keeping your personal assets separate from business liabilities. When used together, they provide a layered approach to protection.

For landlords, it’s not necessarily about choosing one over the other – it’s about timing. If you’re just starting out with one or two properties, umbrella insurance can provide quick and affordable coverage without the administrative responsibilities of an LLC. However, as your property portfolio grows or your personal wealth increases, forming an LLC becomes a smart move to shield your personal assets, though you should weigh the advantages and disadvantages of an LLC for a rental property first. This combination ensures both financial security and legal safeguards.

Your risk profile should guide your decisions. If you manage multiple properties or properties with higher risks, using both strategies becomes even more critical. Keep in mind that when forming an LLC, maintaining a clear separation between personal and business finances is essential. Failing to do so could result in piercing the corporate veil, which would compromise the protection an LLC offers.

The best approach is one tailored to your specific circumstances. Work with professionals like an insurance broker, real estate attorney, and CPA to review your liability coverage, understand state laws, and navigate tax considerations. While this may require an upfront investment, the guidance you receive can help you avoid costly errors in the future.

FAQs

Can an LLC protect my personal assets if a lawsuit goes beyond my umbrella insurance coverage?

Yes, a well-structured and properly maintained LLC can safeguard your personal assets, even in cases where a lawsuit leads to damages beyond your umbrella insurance coverage. To preserve this protection, it’s essential to keep the LLC’s financial and operational activities completely separate from your personal accounts. Additionally, you must adhere to all legal requirements for maintaining the entity.

When these steps are followed, the LLC acts as a legal shield, confining liability to the assets owned by the company and keeping your personal property out of reach from claims or judgments.

What are the ongoing costs and responsibilities of managing an LLC for rental properties?

Maintaining an LLC for rental properties comes with both financial responsibilities and administrative tasks. Depending on your state, you’ll need to budget for an annual report or renewal fee, which can range from just a few dollars to several hundred. Some states also require a yearly franchise or minimum tax. On top of that, you might need to hire professionals like attorneys or accountants to handle filings, update operating agreements, or ensure compliance. Other common expenses include bookkeeping software, fees for a business bank account, and essential insurance coverage.

On the administrative side, landlords must meet compliance requirements to ensure their LLC remains in good standing. This involves filing annual reports on time, keeping accurate records – such as maintaining separate bank accounts and an up-to-date operating agreement – and submitting the correct tax forms. Neglecting these formalities could jeopardize the LLC’s liability protection. Staying organized and proactive will help you manage these obligations smoothly.

Does umbrella insurance cover claims that a standard landlord policy doesn’t?

Umbrella insurance offers an extra layer of liability protection that steps in when the limits of your standard landlord insurance policy are maxed out. It’s designed to cover claims that exceed your primary policy’s coverage, such as costly lawsuits or damages that surpass your existing policy limits.

That said, umbrella insurance isn’t a substitute for other protections, like forming an LLC. It doesn’t protect your personal assets from legal risks connected to property ownership. Instead, it works alongside your other safeguards, providing additional financial coverage for large, unexpected claims.

Related Blog Posts

- LLC for Rental Property: Do You Actually Need One to Protect Your Personal Assets?

- LLCs and Series LLCs for Real Estate Asset Protection

- How to Title Rental Properties in an LLC Without Blowing Up Your Financing or Insurance

- The Most Common LLC Mistakes That Let Tenants’ Lawyers Come After Your Personal Assets